Key Insights into the Biomass Electric Power Generation Market

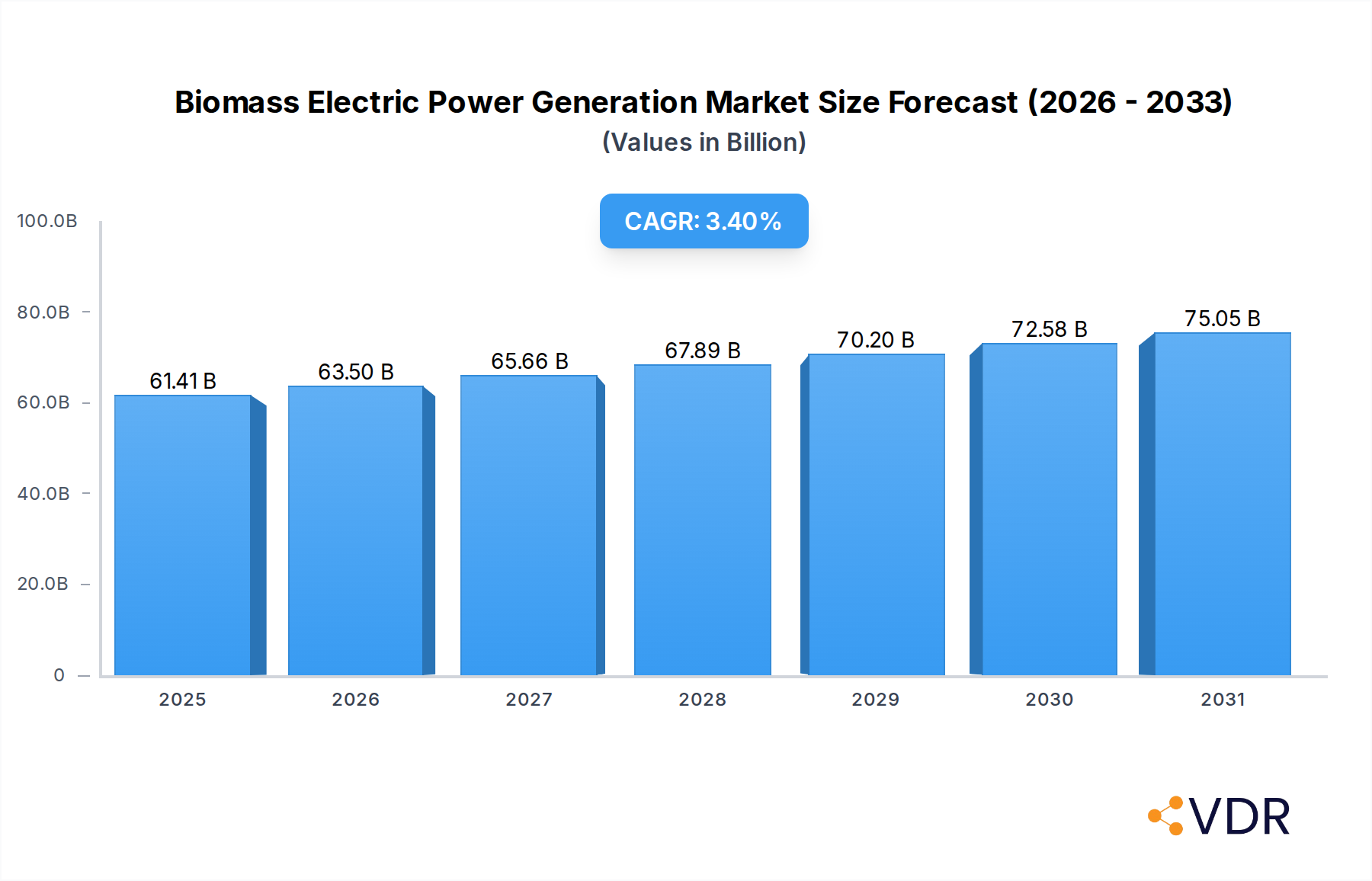

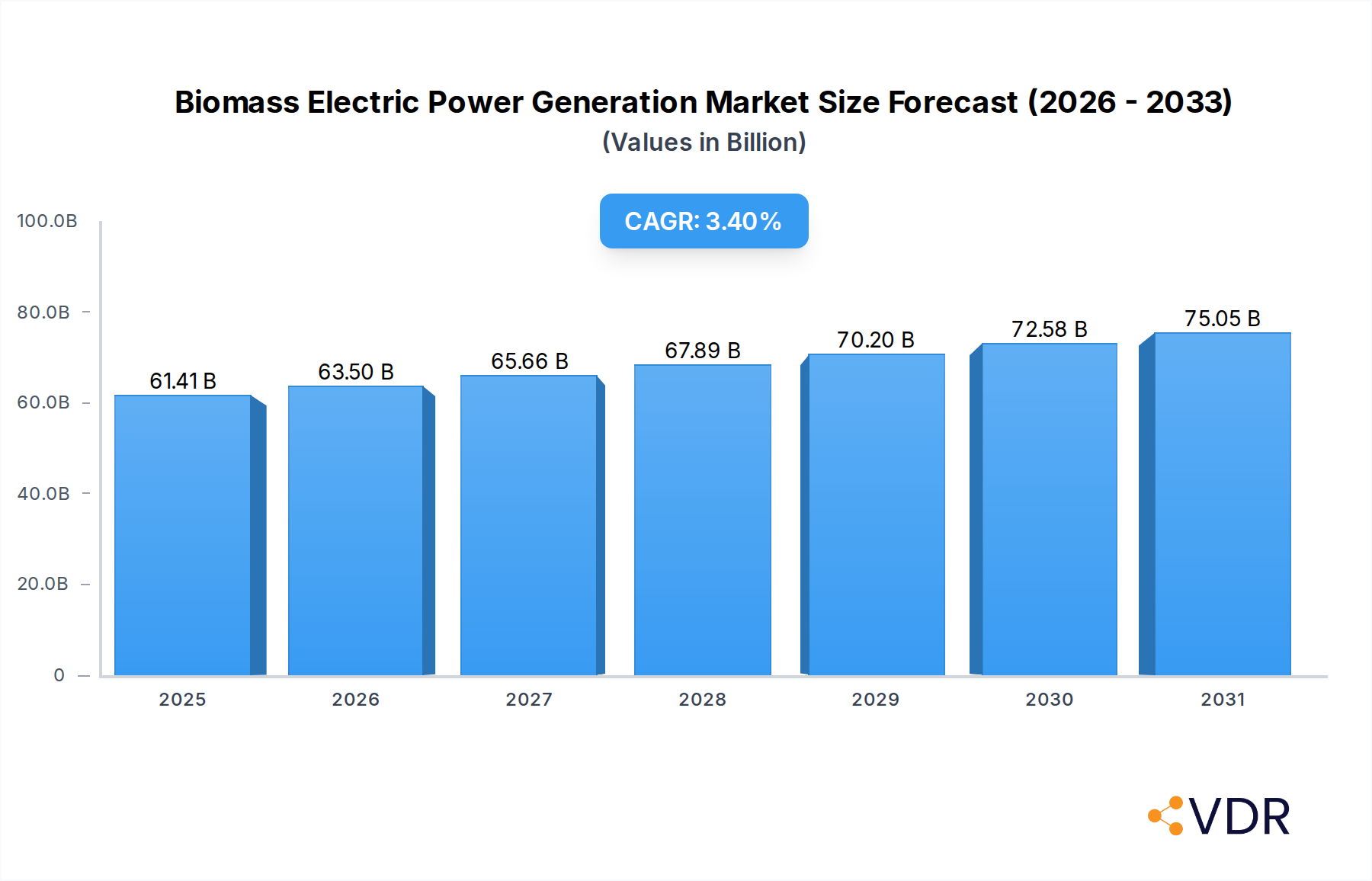

The global Biomass Electric Power Generation Market is a crucial component of the broader Renewable Energy Generation Market, demonstrating robust growth driven by escalating demands for sustainable energy solutions and effective waste management. Valued at an estimated $59390 million in the current period, the market is projected to expand at a Compound Annual Growth Rate (CAGR) of 3.4% through 2032, reaching an impressive $77750 million. This trajectory is underpinned by significant policy support for decarbonization, advancements in bioenergy conversion technologies, and the increasing viability of diverse feedstock sources.

Biomass Electric Power Generation Market Size (In Billion)

The primary demand drivers include global commitments to net-zero emissions, energy security concerns, and the need to process organic waste streams efficiently. Governments worldwide are implementing various incentives, such as feed-in tariffs, renewable energy certificates, and carbon credits, which significantly enhance the economic attractiveness of biomass projects. Macro tailwinds, including volatile fossil fuel prices and growing corporate sustainability mandates, further accelerate adoption. The integration of biomass into existing energy infrastructure, particularly for grid stability and dispatchable power, also presents a substantial opportunity. Furthermore, the strategic shift towards circular economy principles accentuates the value proposition of biomass, especially in the context of the Waste-to-Energy Market, where energy recovery from municipal solid waste and other organic byproducts mitigates landfill burdens while generating electricity. The market's forward-looking outlook remains highly optimistic, with continuous innovation in biomass gasification, pyrolysis, and anaerobic digestion processes enhancing efficiency and reducing environmental footprints. Strategic partnerships between technology providers and energy off-takers are expected to drive further scaling, solidifying biomass's role as a versatile and reliable renewable energy source within the global energy mix.

Biomass Electric Power Generation Company Market Share

Agricultural and Forest Residues Segment Dominance in Biomass Electric Power Generation Market

Within the Biomass Electric Power Generation Market, the Agricultural and Forest Residues segment, under the broader Feedstock category, stands as the single largest contributor to revenue share, demonstrating its indispensable role in the sector's current structure and future growth. This dominance is primarily attributable to the vast and widespread availability of these materials, which include crop stalks, husks, straw, forestry thinning, wood chips, and sawmill waste. Unlike dedicated energy crops, which require land and resources that might otherwise be used for food production, agricultural and forest residues are byproducts of existing economic activities, making their utilization both environmentally sound and economically attractive. The sheer volume generated annually across agricultural and forestry industries ensures a consistent and large-scale supply, which is critical for the continuous operation of biomass power plants.

The established supply chains for collection, processing, and transportation of these residues, often leveraging existing infrastructure from agricultural and logging operations, contribute significantly to their cost-effectiveness. Furthermore, the utilization of these residues addresses a critical waste management challenge for farmers and foresters, often transforming a disposal cost into a revenue stream. This dual benefit of waste valorization and renewable energy generation enhances the segment's appeal. Key players within this segment include large integrated energy companies, independent power producers, and specialized biomass processing firms. These entities often engage in long-term supply agreements with agricultural cooperatives and forestry companies to secure stable feedstock volumes.

The dominance of agricultural and forest residues is expected to continue, though its share might experience minor shifts as other feedstock sources, such as Energy Crops Market, gain traction with technological advancements and optimized cultivation practices. Nonetheless, the inherent advantages of readily available, sustainable, and often low-cost residues solidify their position. Moreover, advancements in biomass pre-treatment technologies, such as torrefaction and pelletization, further enhance the energy density and transportability of these residues, making them more competitive. This ensures a stable foundation for the overall Biomass Electric Power Generation Market, supporting both large-scale utility operations and distributed power generation projects. The constant generation of these materials provides a continuous, renewable resource that contrasts with the intermittent nature of solar or wind power, offering a base-load capacity crucial for grid stability, thereby maintaining this segment's leading position.

Key Market Drivers in Biomass Electric Power Generation Market

The Biomass Electric Power Generation Market is significantly influenced by a confluence of potent drivers, each contributing to its sustained expansion. One primary driver is the global imperative for decarbonization and climate change mitigation. Over 190 countries have ratified the Paris Agreement, setting ambitious targets for reducing greenhouse gas emissions. Biomass power, as a carbon-neutral energy source when sustainably managed, directly supports these objectives, enabling nations to transition away from fossil fuels. This translates into policy instruments like the European Union's Renewable Energy Directive, which mandates specific shares of renewable energy, including bioenergy, in the final energy consumption, often exceeding 32% by 2030.

Secondly, enhanced energy security and independence serve as a critical catalyst. Diversifying energy portfolios away from volatile imported fossil fuels strengthens national energy resilience. Biomass, sourced domestically from agricultural and forest industries, reduces reliance on global energy markets, a factor amplified by recent geopolitical tensions. For example, countries like Sweden and Finland have built robust biomass sectors, with bioenergy contributing over 30% of their total energy supply, significantly enhancing their energy self-sufficiency.

A third major driver is waste management and valorization. The growing global population and industrial activity generate enormous quantities of organic waste, posing significant environmental and logistical challenges. Utilizing municipal solid waste, agricultural residues, and industrial organic byproducts for energy generation offers a dual benefit: reducing landfill volumes and generating clean electricity. This is particularly relevant for the Municipal Solid Waste Management Market, where innovative solutions turn waste into a valuable resource. For instance, cities are increasingly adopting waste-to-energy facilities that convert thousands of tons of waste daily into power, exemplified by numerous plants across Europe and Asia.

Lastly, policy support and financial incentives remain crucial. Government subsidies, tax credits, power purchase agreements (PPAs), and research & development funding significantly de-risk biomass projects and improve their economic viability. Feed-in tariffs, such as those historically offered in Germany or the UK's Renewables Obligation Certificates, have directly spurred investment in the Combustion Technology Market and Anaerobic Digestion Market segments, making project development more attractive for investors and developers alike.

Competitive Ecosystem of Biomass Electric Power Generation Market

Players in the Biomass Electric Power Generation Market are diverse, ranging from global energy conglomerates to specialized technology providers. The competitive landscape is characterized by strategic partnerships, technological innovation, and a strong focus on optimizing feedstock supply chains.

- SUEZ Group: A global leader in environmental services, SUEZ Group is heavily involved in the Waste-to-Energy Market, operating numerous facilities that convert municipal and industrial waste into electricity and heat, aligning with sustainable resource management.

- ENGIE: A multinational energy company, ENGIE focuses on low-carbon energy generation, including significant investments in biomass power plants as part of its broader strategy to expand its Renewable Energy Generation Market portfolio and reduce carbon emissions.

- ACCIONA: A Spanish conglomerate with a strong presence in renewable energy, ACCIONA develops, constructs, and operates biomass plants, contributing to its diverse renewable asset base and commitment to sustainable infrastructure.

- EPH: Energetický a Průmyslový Holding (EPH) is a Central European energy utility with substantial assets in conventional and renewable power generation, including several biomass facilities, bolstering regional energy security.

- Xcel Energy Inc.: An American utility company, Xcel Energy incorporates biomass into its energy mix to meet state-mandated renewable energy targets and provide reliable power to its customers, particularly in the Utility Power Generation Market.

- Ramboll Group A/S: A global engineering, architecture, and consultancy company, Ramboll provides expertise in the design, planning, and implementation of biomass energy projects, focusing on optimizing efficiency and environmental performance.

- EDF: Électricité de France (EDF) is a major player in the European energy sector, with strategic investments in biomass power generation as part of its broader push towards decarbonization and expanding its renewable capacity.

- Babcock & Wilcox Enterprises, Inc.: A long-standing leader in energy and environmental technologies, Babcock & Wilcox supplies advanced biomass boiler technologies and solutions, crucial for the efficient operation of biomass power plants.

- Orsted A/S: A Danish multinational power company, Ørsted is transitioning from fossil fuels to renewable energy, including significant investments in sustainable biomass-fired power plants to provide flexible and dispatchable power.

- Ameresco: A leading clean technology integrator, Ameresco develops, installs, and manages energy solutions, including biomass plants, for public and private sector clients, emphasizing energy efficiency and renewable energy deployment.

- Siemens Energy: A major global energy technology company, Siemens Energy offers solutions for biomass power generation, including steam turbines and generators, supporting the infrastructure development for biomass facilities.

- Statkraft: Europe's largest generator of renewable energy, Statkraft has a portfolio that includes hydropower, wind power, solar power, and biomass power, demonstrating its commitment to a diversified clean energy future.

- General Electric: A global industrial powerhouse, General Electric provides critical components and services for power generation, including steam turbines and environmental control systems used in biomass electric power generation.

- RWE: A leading European energy company, RWE is actively investing in renewable energy sources, including biomass, to diversify its generation portfolio and support the transition to a low-carbon economy.

- AXIS Tech: Specializes in combustion technologies and energy solutions, providing key equipment and services for biomass-fired power plants, enhancing efficiency and reducing emissions in the Combustion Technology Market.

- Veolia: A global leader in optimized resource management, Veolia operates numerous waste-to-energy facilities, converting various organic waste streams into renewable electricity and heat, thereby contributing to the Waste-to-Energy Market.

- Vattenfall: A Swedish state-owned power company, Vattenfall is committed to fossil-free living within one generation, with significant investments in biomass-fueled combined heat and power plants.

- Infinite Energy Pvt. Ltd.: An Indian renewable energy company, Infinite Energy focuses on developing and operating biomass power projects, contributing to India's growing renewable energy capacity and rural electrification efforts.

- Others: This category includes numerous regional players, specialized technology firms, and emerging startups contributing to niche segments or innovative solutions within the Biomass Electric Power Generation Market.

Recent Developments & Milestones in Biomass Electric Power Generation Market

Recent developments in the Biomass Electric Power Generation Market highlight a continued focus on efficiency, sustainability, and expanded feedstock utilization.

- January 2023: Several European utilities announced significant investments in upgrading existing coal-fired power plants to co-fire with biomass, reducing carbon emissions while maintaining baseload generation capacity. This trend supports the Renewable Energy Generation Market's growth by repurposing existing infrastructure.

- April 2023: A major partnership was formed between a leading agricultural cooperative and an energy firm to establish a new facility dedicated to converting Agricultural Residues Market waste into biogas for electricity, optimizing rural resource utilization.

- July 2023: New government incentives were rolled out in Southeast Asia targeting smaller-scale, distributed biomass power plants, particularly those utilizing palm oil mill effluent (POME) and rice husks, to enhance energy access in remote areas.

- September 2023: Breakthroughs in gasification technology for municipal solid waste were reported, promising higher conversion efficiencies and lower emissions, thereby bolstering the viability of the Waste-to-Energy Market.

- November 2023: A consortium of universities and industrial partners secured significant funding for research into advanced pyrolysis techniques for Energy Crops Market, aiming to produce bio-oil with enhanced properties for power generation.

- February 2024: A new regulatory framework was introduced in North America to streamline the permitting process for Anaerobic Digestion Market facilities, encouraging more rapid deployment of biogas-to-electricity projects.

- May 2024: Several large industrial manufacturers announced plans to integrate on-site biomass combined heat and power (CHP) systems, leveraging their own process waste for energy, which significantly impacts the Industrial Power Generation Market.

- August 2024: The launch of a new digital platform designed to optimize biomass feedstock logistics and supply chain management for the entire Biomass Electric Power Generation Market was announced, promising to reduce operational costs and enhance reliability.

- October 2024: Governments in several South American countries initiated public-private partnerships to develop large-scale biomass projects, focusing on sustainably sourced forest residues and dedicated bioenergy plantations.

- December 2024: A new standard for sustainable biomass sourcing and certification was adopted by a major international body, aiming to ensure the environmental and social integrity of biomass supply chains globally.

- March 2025: Significant funding rounds were closed for several startups developing modular biomass power generation units, capable of rapid deployment and scalable operations in diverse settings.

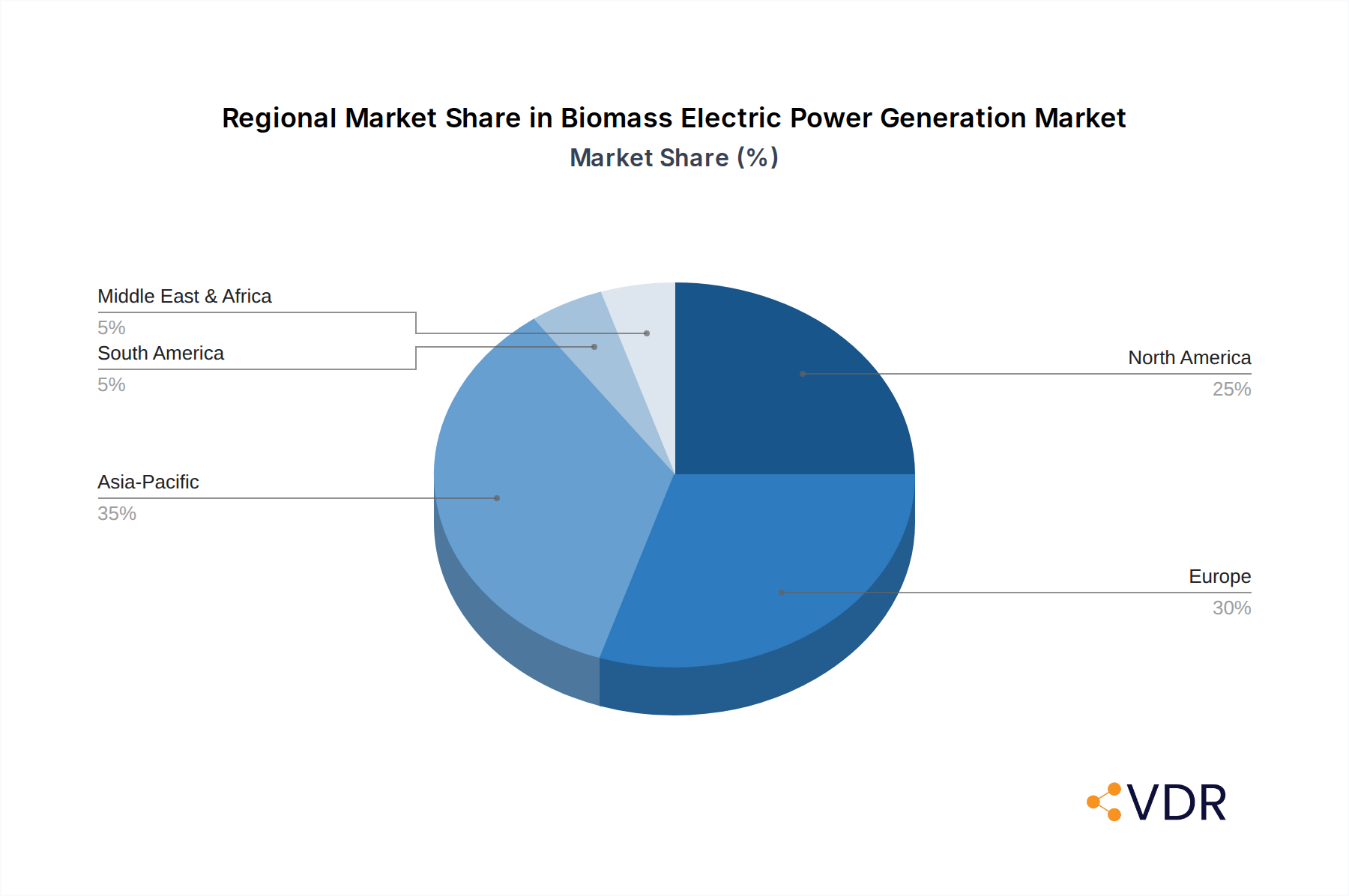

Regional Market Breakdown for Biomass Electric Power Generation Market

The global Biomass Electric Power Generation Market exhibits significant regional variations in growth, maturity, and primary demand drivers. Each region presents a unique landscape influenced by resource availability, policy frameworks, and economic development.

Asia Pacific currently represents the largest and fastest-growing region in the Biomass Electric Power Generation Market. Driven by rapid industrialization, burgeoning energy demand, and severe waste management challenges, countries like China and India are making substantial investments. India, for example, is leveraging its vast agricultural residues to expand its bioenergy capacity. The region's CAGR is projected to be above the global average, reflecting strong government support for renewable energy deployment, waste-to-energy initiatives, and the vast availability of feedstock, including Agricultural Residues Market and Municipal Solid Waste. This region's focus on energy access and environmental sustainability fuels its market leadership.

Europe is a mature market, holding a significant revenue share due to early adoption of renewable energy policies and a well-established regulatory framework. Countries like Germany, the UK, and the Nordic nations have extensive biomass power infrastructure, primarily utilizing forest residues, wood pellets, and anaerobic digestion of organic waste. The region is characterized by stringent emission standards and a strong emphasis on the circular economy, driving continuous innovation in the Waste-to-Energy Market. While its growth rate may be more moderate compared to Asia Pacific, Europe remains a hub for advanced biomass technologies and sustainable sourcing practices.

North America, particularly the United States and Canada, demonstrates a robust market, propelled by renewable energy mandates, incentives for bioenergy production, and abundant forest and agricultural resources. The Utility Power Generation Market in these countries increasingly integrates biomass to achieve portfolio standards and enhance grid reliability. Policies like the Renewable Fuel Standard (RFS) in the U.S. indirectly support biomass electricity generation by promoting biofuel production, which often co-produces residues suitable for power. The market here is growing steadily, focusing on feedstock diversification and efficiency improvements.

Middle East & Africa is an emerging market with substantial untapped potential. While currently a smaller share, the region is expected to witness accelerated growth, driven by increasing energy demand, diversification away from fossil fuels, and urgent needs for waste management solutions. Countries within the GCC are exploring biomass from agricultural waste and municipal solid waste to supplement their energy mix, particularly in the context of urban development and sustainability goals. The adoption of the Waste-to-Energy Market concepts is a key driver, alongside the need for resilient, localized power generation.

South America presents a dynamic growth opportunity, with Brazil leading the charge due to its vast sugarcane industry. Sugarcane bagasse is a significant feedstock for the Biomass Electric Power Generation Market, contributing substantially to the country's energy matrix. Other nations are also exploring their agricultural and forest resources for bioenergy, driven by economic development and the desire to reduce carbon footprints. The region's growth is tied to sustainable agriculture practices and the valorization of industrial byproducts, aiming for increased energy autonomy.

Biomass Electric Power Generation Regional Market Share

Investment & Funding Activity in Biomass Electric Power Generation Market

Investment and funding activity within the Biomass Electric Power Generation Market have shown resilience and strategic reorientation over the past 2-3 years, reflecting the broader push towards sustainable infrastructure and energy transition. While traditional project financing continues to be a cornerstone, a notable trend is the increased participation of institutional investors and impact funds drawn to the sector's ESG credentials and predictable revenue streams under long-term power purchase agreements.

Mergers & Acquisitions (M&A) activity has primarily focused on consolidation and expansion. Larger utilities and energy developers are acquiring smaller, operational biomass plants to bolster their Renewable Energy Generation Market portfolios and meet regulatory mandates. For instance, European utilities have been active in acquiring established assets to ensure compliance with decarbonization targets. There has also been M&A activity in the technology sector, with companies acquiring specialized firms to gain proprietary rights over advanced gasification or Anaerobic Digestion Market solutions.

Venture funding rounds, though less frequent than in solar or wind, are increasingly targeting innovative technologies that enhance efficiency, diversify feedstock, or address logistical challenges. Startups developing modular biomass power units, advanced pre-treatment technologies for Agricultural Residues Market, and AI-driven feedstock management platforms are attracting seed and Series A funding. These investments aim to overcome operational bottlenecks and improve the economic viability of smaller-scale, distributed biomass projects. The bioenergy-to-hydrogen segment is also beginning to attract exploratory capital, recognizing biomass's potential as a feedstock for green hydrogen production.

Strategic partnerships are crucial, often involving technology providers, feedstock suppliers, and off-takers. These alliances de-risk projects, optimize supply chains, and facilitate market entry. For example, partnerships between large agricultural firms and energy companies ensure a stable supply of dedicated Energy Crops Market or residues for power generation. Furthermore, collaborations between waste management companies and energy firms are driving the expansion of the Waste-to-Energy Market, attracting capital into integrated waste-to-power facilities. The sub-segments attracting the most capital are those offering proven technologies with reliable feedstock supply, particularly those that can integrate into existing infrastructure or address pressing waste management issues, demonstrating the market's emphasis on practical, scalable solutions.

Sustainability & ESG Pressures on Biomass Electric Power Generation Market

The Biomass Electric Power Generation Market is profoundly shaped by sustainability and ESG (Environmental, Social, and Governance) pressures, which influence everything from feedstock sourcing to investor perception and regulatory compliance. Environmental regulations are tightening globally, focusing on air emissions (particulate matter, NOx, SOx) and water usage, compelling operators to invest in advanced pollution control technologies. Strict carbon accounting rules dictate that biomass is only considered carbon-neutral if feedstock is sustainably sourced and lifecycle emissions are net-zero, pushing for robust tracking and certification systems.

Carbon targets, often mandated at national or regional levels, act as a primary driver for biomass adoption, positioning it as a key component of decarbonization strategies alongside other renewable energy sources. However, these targets also necessitate rigorous scrutiny of the entire biomass value chain to avoid unintended environmental consequences, such as deforestation or land-use change. This pressure leads to increased demand for sustainably certified biomass, impacting sourcing strategies for the Agricultural Residues Market and Energy Crops Market segments.

Circular economy mandates are particularly impactful, especially in the context of the Waste-to-Energy Market. Governments and municipalities are increasingly prioritizing resource recovery and waste valorization, making biomass power from municipal solid waste and industrial organic waste an attractive solution. This reduces landfill dependency, mitigates methane emissions, and generates renewable energy, aligning with circular economy principles. New policies are emerging that favor energy recovery over landfilling for organic waste streams, providing a strong tailwind for facilities utilizing such feedstocks, including the Municipal Solid Waste Management Market.

ESG investor criteria are transforming capital allocation. Investors are increasingly screening projects based on their environmental footprint, social impact (e.g., local job creation, fair labor practices), and robust governance structures. Projects that can demonstrate clear sustainability credentials, transparent supply chains, and positive community engagement are more likely to attract patient capital. This pressure encourages innovation in biomass conversion technologies (e.g., more efficient Anaerobic Digestion Market processes, advanced Combustion Technology Market designs with lower emissions) and reinforces the need for best practices across the entire Biomass Electric Power Generation Market. Companies that fail to adapt to these evolving ESG expectations risk losing investor confidence and market access, making sustainability an integral part of strategic planning and operational excellence.

Biomass Electric Power Generation Segmentation

-

1. Feedstock

- 1.1. Agricultural and Forest Residues

- 1.2. Energy Crops

- 1.3. Animal Waste

- 1.4. Municipal Solid Waste

- 1.5. Landfill Gas & Biogas

- 1.6. Algae

- 1.7. Others

-

2. Power Capacity

- 2.1. Below 10 MW

- 2.2. 10 MW to 50 MW

- 2.3. 51 MW to 100 MW

- 2.4. Above 100 MW

-

3. Technology

- 3.1. Combustion

- 3.2. Gasification

- 3.3. Anaerobic Digestion

- 3.4. Pyrolysis

- 3.5. Oil Exaction

- 3.6. Fermentation

-

4. End User

- 4.1. Utilities

- 4.2. Industrial Sector

- 4.3. Commercial Sector

- 4.4. Municipalities

- 4.5. Independent Power Producers (IPPs)

Biomass Electric Power Generation Segmentation By Geography

- 1. undefined

- 2. undefined

- 3. undefined

- 4. undefined

- 5. undefined

Biomass Electric Power Generation Regional Market Share

Geographic Coverage of Biomass Electric Power Generation

Biomass Electric Power Generation REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Feedstock

- 5.1.1. Agricultural and Forest Residues

- 5.1.2. Energy Crops

- 5.1.3. Animal Waste

- 5.1.4. Municipal Solid Waste

- 5.1.5. Landfill Gas & Biogas

- 5.1.6. Algae

- 5.1.7. Others

- 5.2. Market Analysis, Insights and Forecast - by Power Capacity

- 5.2.1. Below 10 MW

- 5.2.2. 10 MW to 50 MW

- 5.2.3. 51 MW to 100 MW

- 5.2.4. Above 100 MW

- 5.3. Market Analysis, Insights and Forecast - by Technology

- 5.3.1. Combustion

- 5.3.2. Gasification

- 5.3.3. Anaerobic Digestion

- 5.3.4. Pyrolysis

- 5.3.5. Oil Exaction

- 5.3.6. Fermentation

- 5.4. Market Analysis, Insights and Forecast - by End User

- 5.4.1. Utilities

- 5.4.2. Industrial Sector

- 5.4.3. Commercial Sector

- 5.4.4. Municipalities

- 5.4.5. Independent Power Producers (IPPs)

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1.

- 5.5.2.

- 5.5.3.

- 5.5.4.

- 5.5.5.

- 5.1. Market Analysis, Insights and Forecast - by Feedstock

- 6. Global Biomass Electric Power Generation Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Feedstock

- 6.1.1. Agricultural and Forest Residues

- 6.1.2. Energy Crops

- 6.1.3. Animal Waste

- 6.1.4. Municipal Solid Waste

- 6.1.5. Landfill Gas & Biogas

- 6.1.6. Algae

- 6.1.7. Others

- 6.2. Market Analysis, Insights and Forecast - by Power Capacity

- 6.2.1. Below 10 MW

- 6.2.2. 10 MW to 50 MW

- 6.2.3. 51 MW to 100 MW

- 6.2.4. Above 100 MW

- 6.3. Market Analysis, Insights and Forecast - by Technology

- 6.3.1. Combustion

- 6.3.2. Gasification

- 6.3.3. Anaerobic Digestion

- 6.3.4. Pyrolysis

- 6.3.5. Oil Exaction

- 6.3.6. Fermentation

- 6.4. Market Analysis, Insights and Forecast - by End User

- 6.4.1. Utilities

- 6.4.2. Industrial Sector

- 6.4.3. Commercial Sector

- 6.4.4. Municipalities

- 6.4.5. Independent Power Producers (IPPs)

- 6.1. Market Analysis, Insights and Forecast - by Feedstock

- 7. undefined Biomass Electric Power Generation Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Feedstock

- 7.1.1. Agricultural and Forest Residues

- 7.1.2. Energy Crops

- 7.1.3. Animal Waste

- 7.1.4. Municipal Solid Waste

- 7.1.5. Landfill Gas & Biogas

- 7.1.6. Algae

- 7.1.7. Others

- 7.2. Market Analysis, Insights and Forecast - by Power Capacity

- 7.2.1. Below 10 MW

- 7.2.2. 10 MW to 50 MW

- 7.2.3. 51 MW to 100 MW

- 7.2.4. Above 100 MW

- 7.3. Market Analysis, Insights and Forecast - by Technology

- 7.3.1. Combustion

- 7.3.2. Gasification

- 7.3.3. Anaerobic Digestion

- 7.3.4. Pyrolysis

- 7.3.5. Oil Exaction

- 7.3.6. Fermentation

- 7.4. Market Analysis, Insights and Forecast - by End User

- 7.4.1. Utilities

- 7.4.2. Industrial Sector

- 7.4.3. Commercial Sector

- 7.4.4. Municipalities

- 7.4.5. Independent Power Producers (IPPs)

- 7.1. Market Analysis, Insights and Forecast - by Feedstock

- 8. undefined Biomass Electric Power Generation Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Feedstock

- 8.1.1. Agricultural and Forest Residues

- 8.1.2. Energy Crops

- 8.1.3. Animal Waste

- 8.1.4. Municipal Solid Waste

- 8.1.5. Landfill Gas & Biogas

- 8.1.6. Algae

- 8.1.7. Others

- 8.2. Market Analysis, Insights and Forecast - by Power Capacity

- 8.2.1. Below 10 MW

- 8.2.2. 10 MW to 50 MW

- 8.2.3. 51 MW to 100 MW

- 8.2.4. Above 100 MW

- 8.3. Market Analysis, Insights and Forecast - by Technology

- 8.3.1. Combustion

- 8.3.2. Gasification

- 8.3.3. Anaerobic Digestion

- 8.3.4. Pyrolysis

- 8.3.5. Oil Exaction

- 8.3.6. Fermentation

- 8.4. Market Analysis, Insights and Forecast - by End User

- 8.4.1. Utilities

- 8.4.2. Industrial Sector

- 8.4.3. Commercial Sector

- 8.4.4. Municipalities

- 8.4.5. Independent Power Producers (IPPs)

- 8.1. Market Analysis, Insights and Forecast - by Feedstock

- 9. undefined Biomass Electric Power Generation Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Feedstock

- 9.1.1. Agricultural and Forest Residues

- 9.1.2. Energy Crops

- 9.1.3. Animal Waste

- 9.1.4. Municipal Solid Waste

- 9.1.5. Landfill Gas & Biogas

- 9.1.6. Algae

- 9.1.7. Others

- 9.2. Market Analysis, Insights and Forecast - by Power Capacity

- 9.2.1. Below 10 MW

- 9.2.2. 10 MW to 50 MW

- 9.2.3. 51 MW to 100 MW

- 9.2.4. Above 100 MW

- 9.3. Market Analysis, Insights and Forecast - by Technology

- 9.3.1. Combustion

- 9.3.2. Gasification

- 9.3.3. Anaerobic Digestion

- 9.3.4. Pyrolysis

- 9.3.5. Oil Exaction

- 9.3.6. Fermentation

- 9.4. Market Analysis, Insights and Forecast - by End User

- 9.4.1. Utilities

- 9.4.2. Industrial Sector

- 9.4.3. Commercial Sector

- 9.4.4. Municipalities

- 9.4.5. Independent Power Producers (IPPs)

- 9.1. Market Analysis, Insights and Forecast - by Feedstock

- 10. undefined Biomass Electric Power Generation Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Feedstock

- 10.1.1. Agricultural and Forest Residues

- 10.1.2. Energy Crops

- 10.1.3. Animal Waste

- 10.1.4. Municipal Solid Waste

- 10.1.5. Landfill Gas & Biogas

- 10.1.6. Algae

- 10.1.7. Others

- 10.2. Market Analysis, Insights and Forecast - by Power Capacity

- 10.2.1. Below 10 MW

- 10.2.2. 10 MW to 50 MW

- 10.2.3. 51 MW to 100 MW

- 10.2.4. Above 100 MW

- 10.3. Market Analysis, Insights and Forecast - by Technology

- 10.3.1. Combustion

- 10.3.2. Gasification

- 10.3.3. Anaerobic Digestion

- 10.3.4. Pyrolysis

- 10.3.5. Oil Exaction

- 10.3.6. Fermentation

- 10.4. Market Analysis, Insights and Forecast - by End User

- 10.4.1. Utilities

- 10.4.2. Industrial Sector

- 10.4.3. Commercial Sector

- 10.4.4. Municipalities

- 10.4.5. Independent Power Producers (IPPs)

- 10.1. Market Analysis, Insights and Forecast - by Feedstock

- 11. undefined Biomass Electric Power Generation Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Feedstock

- 11.1.1. Agricultural and Forest Residues

- 11.1.2. Energy Crops

- 11.1.3. Animal Waste

- 11.1.4. Municipal Solid Waste

- 11.1.5. Landfill Gas & Biogas

- 11.1.6. Algae

- 11.1.7. Others

- 11.2. Market Analysis, Insights and Forecast - by Power Capacity

- 11.2.1. Below 10 MW

- 11.2.2. 10 MW to 50 MW

- 11.2.3. 51 MW to 100 MW

- 11.2.4. Above 100 MW

- 11.3. Market Analysis, Insights and Forecast - by Technology

- 11.3.1. Combustion

- 11.3.2. Gasification

- 11.3.3. Anaerobic Digestion

- 11.3.4. Pyrolysis

- 11.3.5. Oil Exaction

- 11.3.6. Fermentation

- 11.4. Market Analysis, Insights and Forecast - by End User

- 11.4.1. Utilities

- 11.4.2. Industrial Sector

- 11.4.3. Commercial Sector

- 11.4.4. Municipalities

- 11.4.5. Independent Power Producers (IPPs)

- 11.1. Market Analysis, Insights and Forecast - by Feedstock

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 SUEZ Group

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 ENGIE

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 ACCIONA

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 EPH

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Xcel Energy Inc.

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Ramboll Group A/S

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 EDF

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Babcock & Wilcox Enterprises Inc.

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Orsted A/S

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Ameresco

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Siemens Energy

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Statkraft

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 General Electric

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 RWE

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 AXIS Tech

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Veolia

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Vattenfall

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 Infinite Energy Pvt. Ltd.

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 Others

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.1 SUEZ Group

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Biomass Electric Power Generation Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: undefined Biomass Electric Power Generation Revenue (million), by Feedstock 2025 & 2033

- Figure 3: undefined Biomass Electric Power Generation Revenue Share (%), by Feedstock 2025 & 2033

- Figure 4: undefined Biomass Electric Power Generation Revenue (million), by Power Capacity 2025 & 2033

- Figure 5: undefined Biomass Electric Power Generation Revenue Share (%), by Power Capacity 2025 & 2033

- Figure 6: undefined Biomass Electric Power Generation Revenue (million), by Technology 2025 & 2033

- Figure 7: undefined Biomass Electric Power Generation Revenue Share (%), by Technology 2025 & 2033

- Figure 8: undefined Biomass Electric Power Generation Revenue (million), by End User 2025 & 2033

- Figure 9: undefined Biomass Electric Power Generation Revenue Share (%), by End User 2025 & 2033

- Figure 10: undefined Biomass Electric Power Generation Revenue (million), by Country 2025 & 2033

- Figure 11: undefined Biomass Electric Power Generation Revenue Share (%), by Country 2025 & 2033

- Figure 12: undefined Biomass Electric Power Generation Revenue (million), by Feedstock 2025 & 2033

- Figure 13: undefined Biomass Electric Power Generation Revenue Share (%), by Feedstock 2025 & 2033

- Figure 14: undefined Biomass Electric Power Generation Revenue (million), by Power Capacity 2025 & 2033

- Figure 15: undefined Biomass Electric Power Generation Revenue Share (%), by Power Capacity 2025 & 2033

- Figure 16: undefined Biomass Electric Power Generation Revenue (million), by Technology 2025 & 2033

- Figure 17: undefined Biomass Electric Power Generation Revenue Share (%), by Technology 2025 & 2033

- Figure 18: undefined Biomass Electric Power Generation Revenue (million), by End User 2025 & 2033

- Figure 19: undefined Biomass Electric Power Generation Revenue Share (%), by End User 2025 & 2033

- Figure 20: undefined Biomass Electric Power Generation Revenue (million), by Country 2025 & 2033

- Figure 21: undefined Biomass Electric Power Generation Revenue Share (%), by Country 2025 & 2033

- Figure 22: undefined Biomass Electric Power Generation Revenue (million), by Feedstock 2025 & 2033

- Figure 23: undefined Biomass Electric Power Generation Revenue Share (%), by Feedstock 2025 & 2033

- Figure 24: undefined Biomass Electric Power Generation Revenue (million), by Power Capacity 2025 & 2033

- Figure 25: undefined Biomass Electric Power Generation Revenue Share (%), by Power Capacity 2025 & 2033

- Figure 26: undefined Biomass Electric Power Generation Revenue (million), by Technology 2025 & 2033

- Figure 27: undefined Biomass Electric Power Generation Revenue Share (%), by Technology 2025 & 2033

- Figure 28: undefined Biomass Electric Power Generation Revenue (million), by End User 2025 & 2033

- Figure 29: undefined Biomass Electric Power Generation Revenue Share (%), by End User 2025 & 2033

- Figure 30: undefined Biomass Electric Power Generation Revenue (million), by Country 2025 & 2033

- Figure 31: undefined Biomass Electric Power Generation Revenue Share (%), by Country 2025 & 2033

- Figure 32: undefined Biomass Electric Power Generation Revenue (million), by Feedstock 2025 & 2033

- Figure 33: undefined Biomass Electric Power Generation Revenue Share (%), by Feedstock 2025 & 2033

- Figure 34: undefined Biomass Electric Power Generation Revenue (million), by Power Capacity 2025 & 2033

- Figure 35: undefined Biomass Electric Power Generation Revenue Share (%), by Power Capacity 2025 & 2033

- Figure 36: undefined Biomass Electric Power Generation Revenue (million), by Technology 2025 & 2033

- Figure 37: undefined Biomass Electric Power Generation Revenue Share (%), by Technology 2025 & 2033

- Figure 38: undefined Biomass Electric Power Generation Revenue (million), by End User 2025 & 2033

- Figure 39: undefined Biomass Electric Power Generation Revenue Share (%), by End User 2025 & 2033

- Figure 40: undefined Biomass Electric Power Generation Revenue (million), by Country 2025 & 2033

- Figure 41: undefined Biomass Electric Power Generation Revenue Share (%), by Country 2025 & 2033

- Figure 42: undefined Biomass Electric Power Generation Revenue (million), by Feedstock 2025 & 2033

- Figure 43: undefined Biomass Electric Power Generation Revenue Share (%), by Feedstock 2025 & 2033

- Figure 44: undefined Biomass Electric Power Generation Revenue (million), by Power Capacity 2025 & 2033

- Figure 45: undefined Biomass Electric Power Generation Revenue Share (%), by Power Capacity 2025 & 2033

- Figure 46: undefined Biomass Electric Power Generation Revenue (million), by Technology 2025 & 2033

- Figure 47: undefined Biomass Electric Power Generation Revenue Share (%), by Technology 2025 & 2033

- Figure 48: undefined Biomass Electric Power Generation Revenue (million), by End User 2025 & 2033

- Figure 49: undefined Biomass Electric Power Generation Revenue Share (%), by End User 2025 & 2033

- Figure 50: undefined Biomass Electric Power Generation Revenue (million), by Country 2025 & 2033

- Figure 51: undefined Biomass Electric Power Generation Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Biomass Electric Power Generation Revenue million Forecast, by Feedstock 2020 & 2033

- Table 2: Global Biomass Electric Power Generation Revenue million Forecast, by Power Capacity 2020 & 2033

- Table 3: Global Biomass Electric Power Generation Revenue million Forecast, by Technology 2020 & 2033

- Table 4: Global Biomass Electric Power Generation Revenue million Forecast, by End User 2020 & 2033

- Table 5: Global Biomass Electric Power Generation Revenue million Forecast, by Region 2020 & 2033

- Table 6: Global Biomass Electric Power Generation Revenue million Forecast, by Feedstock 2020 & 2033

- Table 7: Global Biomass Electric Power Generation Revenue million Forecast, by Power Capacity 2020 & 2033

- Table 8: Global Biomass Electric Power Generation Revenue million Forecast, by Technology 2020 & 2033

- Table 9: Global Biomass Electric Power Generation Revenue million Forecast, by End User 2020 & 2033

- Table 10: Global Biomass Electric Power Generation Revenue million Forecast, by Country 2020 & 2033

- Table 11: Global Biomass Electric Power Generation Revenue million Forecast, by Feedstock 2020 & 2033

- Table 12: Global Biomass Electric Power Generation Revenue million Forecast, by Power Capacity 2020 & 2033

- Table 13: Global Biomass Electric Power Generation Revenue million Forecast, by Technology 2020 & 2033

- Table 14: Global Biomass Electric Power Generation Revenue million Forecast, by End User 2020 & 2033

- Table 15: Global Biomass Electric Power Generation Revenue million Forecast, by Country 2020 & 2033

- Table 16: Global Biomass Electric Power Generation Revenue million Forecast, by Feedstock 2020 & 2033

- Table 17: Global Biomass Electric Power Generation Revenue million Forecast, by Power Capacity 2020 & 2033

- Table 18: Global Biomass Electric Power Generation Revenue million Forecast, by Technology 2020 & 2033

- Table 19: Global Biomass Electric Power Generation Revenue million Forecast, by End User 2020 & 2033

- Table 20: Global Biomass Electric Power Generation Revenue million Forecast, by Country 2020 & 2033

- Table 21: Global Biomass Electric Power Generation Revenue million Forecast, by Feedstock 2020 & 2033

- Table 22: Global Biomass Electric Power Generation Revenue million Forecast, by Power Capacity 2020 & 2033

- Table 23: Global Biomass Electric Power Generation Revenue million Forecast, by Technology 2020 & 2033

- Table 24: Global Biomass Electric Power Generation Revenue million Forecast, by End User 2020 & 2033

- Table 25: Global Biomass Electric Power Generation Revenue million Forecast, by Country 2020 & 2033

- Table 26: Global Biomass Electric Power Generation Revenue million Forecast, by Feedstock 2020 & 2033

- Table 27: Global Biomass Electric Power Generation Revenue million Forecast, by Power Capacity 2020 & 2033

- Table 28: Global Biomass Electric Power Generation Revenue million Forecast, by Technology 2020 & 2033

- Table 29: Global Biomass Electric Power Generation Revenue million Forecast, by End User 2020 & 2033

- Table 30: Global Biomass Electric Power Generation Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Biomass Electric Power Generation?

The projected CAGR is approximately 3.4%.

2. Which companies are prominent players in the Biomass Electric Power Generation?

Key companies in the market include SUEZ Group , ENGIE, ACCIONA, EPH, Xcel Energy Inc., Ramboll Group A/S, EDF, Babcock & Wilcox Enterprises, Inc., Orsted A/S, Ameresco, Siemens Energy, Statkraft, General Electric, RWE, AXIS Tech, Veolia, Vattenfall, Infinite Energy Pvt. Ltd., Others.

3. What are the main segments of the Biomass Electric Power Generation?

The market segments include Feedstock, Power Capacity, Technology, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 59390 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Biomass Electric Power Generation," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Biomass Electric Power Generation report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Biomass Electric Power Generation?

To stay informed about further developments, trends, and reports in the Biomass Electric Power Generation, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence