Key Insights

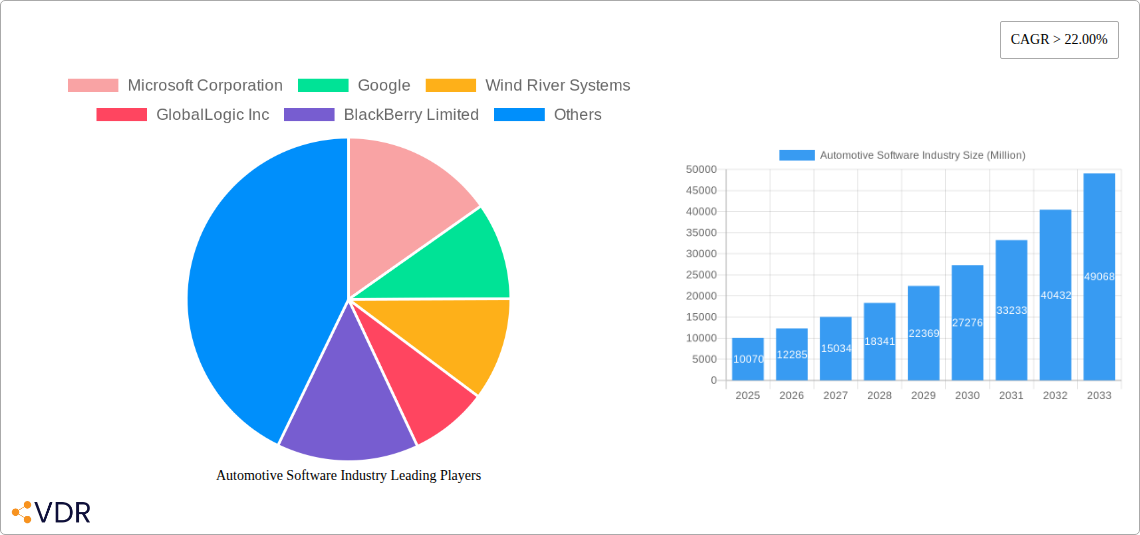

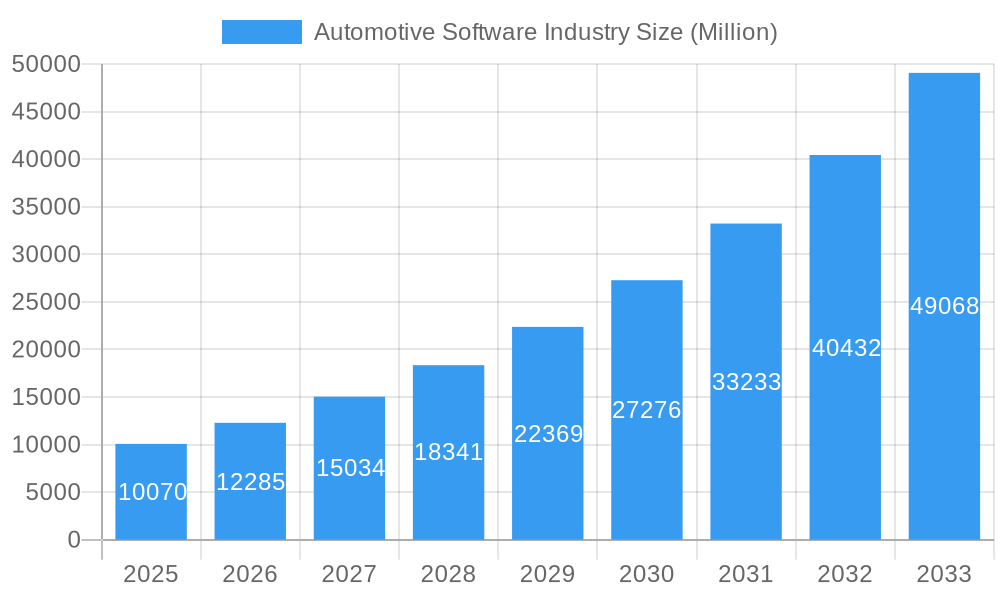

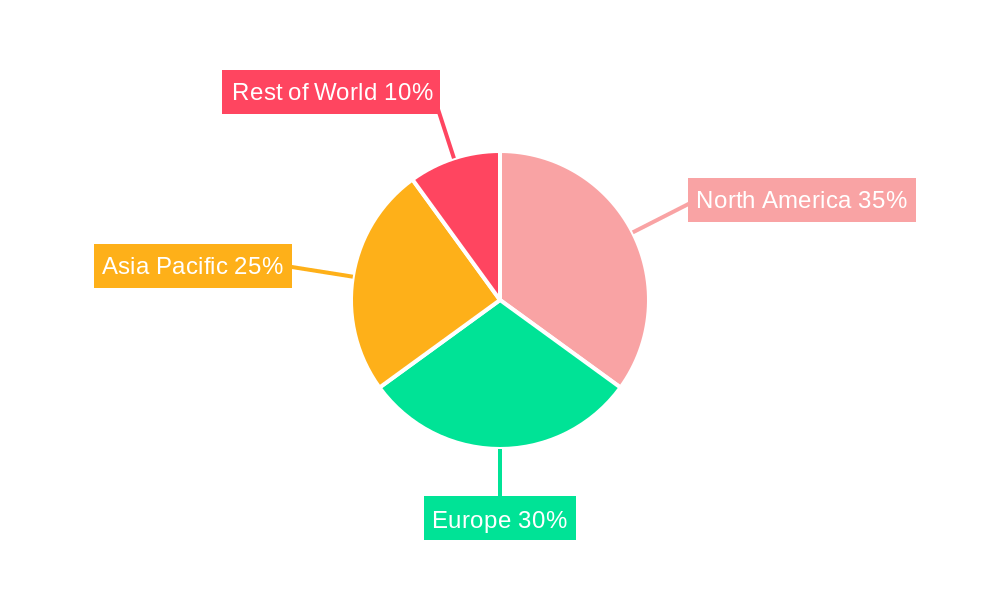

The automotive software market is experiencing explosive growth, projected to reach \$10.07 billion in 2025 and exhibiting a Compound Annual Growth Rate (CAGR) exceeding 22% from 2025 to 2033. This surge is driven by the increasing demand for advanced driver-assistance systems (ADAS), enhanced in-car infotainment, and seamless vehicle connectivity features. The proliferation of electric vehicles (EVs) and autonomous driving technologies further fuels this expansion, requiring sophisticated software solutions for powertrain management, battery control, and autonomous navigation. Key segments include safety and security software, infotainment and instrument cluster systems, and vehicle connectivity solutions, with passenger cars currently dominating the vehicle type segment. However, the commercial vehicle segment is poised for significant growth due to increasing adoption of fleet management and telematics systems. Leading players such as Microsoft, Google, and Bosch are actively investing in R&D and strategic partnerships to capture market share within this rapidly evolving landscape. Geographic expansion is also significant, with North America and Europe currently leading the market, followed by a rapidly growing Asia-Pacific region fueled by increasing vehicle production and technological adoption in countries like China and India.

Automotive Software Industry Market Size (In Billion)

The market's growth trajectory is influenced by several factors. Technological advancements in areas like artificial intelligence (AI), machine learning (ML), and 5G connectivity are creating opportunities for more sophisticated and feature-rich automotive software. However, challenges remain, including cybersecurity concerns related to connected vehicles, the high cost of development and integration, and the need for robust software testing and validation to ensure safety and reliability. Regulatory changes related to autonomous driving and data privacy also pose both opportunities and challenges for market participants. Overcoming these hurdles will be crucial for sustained growth and widespread adoption of advanced automotive software solutions. Future projections suggest a continued rise in market valuation, driven by the ongoing trend toward vehicle electrification and automation, along with continuous improvements in software capabilities and functionality.

Automotive Software Industry Company Market Share

Automotive Software Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the Automotive Software market, encompassing market dynamics, growth trends, regional dominance, product landscape, key challenges and opportunities, and key players shaping the industry. The study period spans 2019-2033, with 2025 as the base year and a forecast period of 2025-2033. The report analyzes parent markets (Automotive Industry) and child markets (e.g., Passenger Cars, Commercial Vehicles, Infotainment Systems). Market values are presented in Million units.

Automotive Software Industry Market Dynamics & Structure

The automotive software market is experiencing robust and accelerated growth, propelled by relentless technological innovation, increasingly stringent global safety and environmental regulations, and the escalating consumer demand for sophisticated connected and autonomous driving experiences. The market exhibits a dynamic structure characterized by a notable level of concentration, where a handful of dominant global players command a significant market share, complemented by a vibrant ecosystem of agile, specialized firms catering to niche requirements. The relentless pace of technological advancement, particularly in cutting-edge fields such as Artificial Intelligence (AI), advanced Machine Learning (ML) algorithms, and the transformative capabilities of 5G connectivity, serves as a primary catalyst. Evolving regulatory landscapes, encompassing critical areas like robust cybersecurity protocols and stringent data privacy mandates, are actively shaping the competitive arena and dictating product development roadmaps. The paradigm shift towards Software-Defined Vehicles (SDVs) is profoundly disrupting traditional automotive architectures, presenting both unprecedented opportunities for innovation and significant operational challenges. Mergers and Acquisitions (M&A) activity remains a prominent feature, with established industry leaders strategically pursuing acquisitions to rapidly expand their technological competencies, broaden their product portfolios, and enhance their global market reach.

- Market Concentration: The market is moderately concentrated, with the top 5 key players anticipated to hold approximately 55-60% of the market share by 2025.

- Technological Innovation: Key drivers of innovation include the rapid advancement and integration of AI, Machine Learning, 5G infrastructure, and the increasing adoption of Over-the-Air (OTA) software updates for seamless vehicle enhancement and maintenance.

- Regulatory Frameworks: Increasingly stringent global safety, cybersecurity, and emissions standards are elevating the complexity and development costs for automotive software solutions.

- Competitive Product Substitutes: While direct substitutes for integrated automotive software are limited, the growing influence and adoption of open-source software development models present an emerging competitive threat and collaborative opportunity.

- End-User Demographics: The primary end-users comprise automotive Original Equipment Manufacturers (OEMs), Tier-1 suppliers, specialized software development houses, and increasingly, technology companies entering the automotive space.

- M&A Trends: M&A activity is projected to escalate, driven by strategic consolidation, the pursuit of disruptive technologies, and the imperative to expand capabilities in emerging areas. Approximately 35-40 significant M&A deals are predicted in the automotive software sector for 2025.

Automotive Software Industry Growth Trends & Insights

The automotive software market is on a trajectory of substantial and sustained growth, largely fueled by the widespread adoption of sophisticated Advanced Driver-Assistance Systems (ADAS), highly interactive infotainment systems, and the proliferation of connected car technologies. The global automotive software market size is projected to reach an impressive USD 95-105 Billion by 2033, demonstrating a robust Compound Annual Growth Rate (CAGR) of approximately 10-12% during the forecast period. The foundational shift towards Software-Defined Vehicles (SDVs) is a pivotal disruptor, fundamentally rearchitecting vehicle development processes and introducing new software-centric paradigms. Consumer expectations are rapidly evolving towards highly personalized and seamlessly integrated in-car digital experiences, thereby driving an insatiable demand for advanced and intuitive software solutions. The market penetration of advanced autonomous driving capabilities is steadily increasing, leading to escalating software complexity, more rigorous testing requirements, and consequently, higher overall development costs.

Dominant Regions, Countries, or Segments in Automotive Software Industry

North America and Europe currently dominate the automotive software market, driven by robust automotive industries, high vehicle ownership rates, and early adoption of advanced technologies. However, Asia-Pacific is projected to experience the fastest growth due to increasing vehicle production and rising consumer demand for connected cars.

By Application:

- Safety and Security: This segment holds the largest market share (xx%) due to mandatory safety regulations and growing demand for cybersecurity solutions.

- Infotainment and Instrument Cluster: This segment is experiencing strong growth (xx% CAGR) due to increasing consumer demand for advanced infotainment features.

- Vehicle Connectivity: This segment is rapidly expanding (xx% CAGR) due to the proliferation of connected car technologies and the growing adoption of telematics systems.

- Other Applications (Powertrain): This segment is also growing significantly due to the increased adoption of electric and hybrid vehicles.

By Vehicle Type:

- Passenger Cars: This segment dominates the market, driven by high vehicle production volumes and increasing consumer demand.

- Commercial Vehicles: This segment is experiencing slower growth but is expected to expand significantly due to the increasing adoption of advanced driver-assistance systems.

Automotive Software Industry Product Landscape

The automotive software landscape is dynamic, with continuous innovations in areas such as over-the-air (OTA) updates, artificial intelligence (AI)-powered features, and enhanced cybersecurity measures. Products range from basic embedded systems to complex AI-driven applications for autonomous driving. Key performance metrics include functional safety compliance, software reliability, and real-time performance. Unique selling propositions often include superior integration capabilities, advanced security features, and customized solutions tailored to specific vehicle architectures.

Key Drivers, Barriers & Challenges in Automotive Software Industry

Key Drivers:

- The ever-increasing consumer and regulatory demand for highly connected, intelligent, and autonomous vehicle functionalities.

- Rapid advancements and widespread integration of Artificial Intelligence (AI), Machine Learning (ML), and 5G connectivity technologies.

- Stringent and evolving government regulations mandating enhanced vehicle safety, emission controls, and cybersecurity standards.

- The accelerating adoption and development of Software-Defined Vehicles (SDVs), transforming vehicle architectures and software integration.

- Growing consumer preference for enhanced in-car digital experiences, including advanced infotainment and personalized connectivity.

Key Challenges and Restraints:

- Significant capital investment and escalating development complexities associated with sophisticated and safety-critical software features.

- Pervasive cybersecurity risks and the constant threat of vulnerabilities within interconnected vehicle systems.

- The paramount importance of ensuring absolute software reliability, functional safety, and real-time performance in critical vehicle operational systems.

- A persistent and growing shortage of highly skilled software engineers and developers with specialized expertise in automotive applications. An estimated shortage of 80-100 thousand specialized automotive software engineers is projected for 2025.

- Navigating the intricate landscape of software updates and lifecycle management across diverse vehicle platforms and generations.

Emerging Opportunities in Automotive Software Industry

- The burgeoning demand for hyper-personalized and context-aware in-car digital experiences, including advanced entertainment and productivity tools.

- The significant expansion of the Electric Vehicle (EV) market, creating substantial opportunities for specialized software solutions related to battery management, charging infrastructure integration, and powertrain optimization.

- The continued development and refinement of sophisticated Advanced Driver-Assistance Systems (ADAS) and semi-autonomous driving features, moving towards higher levels of automation.

- The increasing integration and utilization of cloud-based services, big data analytics, and edge computing for enhanced vehicle performance, predictive maintenance, and fleet management.

- The rise of in-car app ecosystems and subscription-based software services, offering new revenue streams and user engagement models.

- Opportunities in vehicle-to-everything (V2X) communication technologies, enabling enhanced safety, traffic management, and smart city integration.

Growth Accelerators in the Automotive Software Industry

The long-term growth of the automotive software industry is primarily driven by the ongoing advancements in AI, autonomous driving technologies, and the rise of the software-defined vehicle (SDV) paradigm. Strategic partnerships between automotive manufacturers and technology companies are accelerating innovation and market expansion. Government initiatives promoting electric vehicle adoption and the development of smart transportation systems further fuel the growth trajectory.

Key Players Shaping the Automotive Software Industry Market

Notable Milestones in Automotive Software Industry Sector

- March 2023: Honda Motor and KPIT Technologies Ltd. signed a basic agreement for software development collaboration, focusing on next-generation E&E architecture, electrified powertrains, enhanced safety, and IVI systems.

- January 2023: Luxoft and Microsoft partnered on the Connected Fleets project, accelerating the transition to software-defined cars and leveraging Microsoft Azure and Azure IoT.

- January 2023: Marelli Corporation chose BlackBerry QNX Acoustics Management Platform for enhanced in-car audio experiences in SDVs, improving voice command accuracy and noise cancellation.

In-Depth Automotive Software Industry Market Outlook

The long-term outlook for the automotive software market is exceptionally bright and poised for sustained expansion, underpinned by continuous technological breakthroughs and the increasingly seamless convergence of the automotive and high-technology sectors. The strategic expansion into novel and high-impact application areas, such as fully autonomous driving systems, advanced V2X communication, and sophisticated in-cabin artificial intelligence, presents vast and lucrative growth avenues. Strategic alliances, collaborative partnerships, and targeted acquisitions will remain indispensable for market players striving to maintain a competitive advantage and navigate the rapid pace of innovation in this dynamic ecosystem. The industry's focus will increasingly shift towards the development of demonstrably more secure, exceptionally reliable, and highly efficient software solutions, meticulously engineered to meet the multifaceted demands of the increasingly complex and interconnected automotive value chain.

Automotive Software Industry Segmentation

-

1. Application

- 1.1. Safety and Security

- 1.2. Infotainment and Instrument Cluster

- 1.3. Vehicle Connectivity

- 1.4. Other Applications (Powertrain)

-

2. Vehicle Type

- 2.1. Passenger Cars

- 2.2. Commercial Vehicles

Automotive Software Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Rest of North America

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

-

4. Rest of the World

- 4.1. South America

- 4.2. Middle East and Africa

Automotive Software Industry Regional Market Share

Geographic Coverage of Automotive Software Industry

Automotive Software Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of > 22.00% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Safety and Security

- 5.1.2. Infotainment and Instrument Cluster

- 5.1.3. Vehicle Connectivity

- 5.1.4. Other Applications (Powertrain)

- 5.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.2.1. Passenger Cars

- 5.2.2. Commercial Vehicles

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Automotive Software Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Safety and Security

- 6.1.2. Infotainment and Instrument Cluster

- 6.1.3. Vehicle Connectivity

- 6.1.4. Other Applications (Powertrain)

- 6.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.2.1. Passenger Cars

- 6.2.2. Commercial Vehicles

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Automotive Software Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Safety and Security

- 7.1.2. Infotainment and Instrument Cluster

- 7.1.3. Vehicle Connectivity

- 7.1.4. Other Applications (Powertrain)

- 7.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 7.2.1. Passenger Cars

- 7.2.2. Commercial Vehicles

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Automotive Software Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Safety and Security

- 8.1.2. Infotainment and Instrument Cluster

- 8.1.3. Vehicle Connectivity

- 8.1.4. Other Applications (Powertrain)

- 8.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 8.2.1. Passenger Cars

- 8.2.2. Commercial Vehicles

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Asia Pacific Automotive Software Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Safety and Security

- 9.1.2. Infotainment and Instrument Cluster

- 9.1.3. Vehicle Connectivity

- 9.1.4. Other Applications (Powertrain)

- 9.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 9.2.1. Passenger Cars

- 9.2.2. Commercial Vehicles

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Rest of the World Automotive Software Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Safety and Security

- 10.1.2. Infotainment and Instrument Cluster

- 10.1.3. Vehicle Connectivity

- 10.1.4. Other Applications (Powertrain)

- 10.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 10.2.1. Passenger Cars

- 10.2.2. Commercial Vehicles

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Microsoft Corporation

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Google

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Wind River Systems

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 GlobalLogic Inc

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 BlackBerry Limited

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Robert Bosch GmbH

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Intellias Ltd

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 KPIT Technologies Limited

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 HARMAN International

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 MontaVista Software LLC

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 Airbiquity Inc

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.1 Microsoft Corporation

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Automotive Software Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Automotive Software Industry Revenue (Million), by Application 2025 & 2033

- Figure 3: North America Automotive Software Industry Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive Software Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 5: North America Automotive Software Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 6: North America Automotive Software Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Automotive Software Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Automotive Software Industry Revenue (Million), by Application 2025 & 2033

- Figure 9: Europe Automotive Software Industry Revenue Share (%), by Application 2025 & 2033

- Figure 10: Europe Automotive Software Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 11: Europe Automotive Software Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 12: Europe Automotive Software Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Automotive Software Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Automotive Software Industry Revenue (Million), by Application 2025 & 2033

- Figure 15: Asia Pacific Automotive Software Industry Revenue Share (%), by Application 2025 & 2033

- Figure 16: Asia Pacific Automotive Software Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 17: Asia Pacific Automotive Software Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 18: Asia Pacific Automotive Software Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Pacific Automotive Software Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Rest of the World Automotive Software Industry Revenue (Million), by Application 2025 & 2033

- Figure 21: Rest of the World Automotive Software Industry Revenue Share (%), by Application 2025 & 2033

- Figure 22: Rest of the World Automotive Software Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 23: Rest of the World Automotive Software Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 24: Rest of the World Automotive Software Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Rest of the World Automotive Software Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Software Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 2: Global Automotive Software Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 3: Global Automotive Software Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Automotive Software Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 5: Global Automotive Software Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 6: Global Automotive Software Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Rest of North America Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive Software Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 11: Global Automotive Software Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 12: Global Automotive Software Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Germany Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: United Kingdom Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: France Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Italy Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Rest of Europe Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Global Automotive Software Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 19: Global Automotive Software Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 20: Global Automotive Software Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: China Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Japan Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: India Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: South Korea Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Rest of Asia Pacific Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Global Automotive Software Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 27: Global Automotive Software Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 28: Global Automotive Software Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 29: South America Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Middle East and Africa Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Software Industry?

The projected CAGR is approximately > 22.00%.

2. Which companies are prominent players in the Automotive Software Industry?

Key companies in the market include Microsoft Corporation, Google, Wind River Systems, GlobalLogic Inc, BlackBerry Limited, Robert Bosch GmbH, Intellias Ltd, KPIT Technologies Limited, HARMAN International, MontaVista Software LLC, Airbiquity Inc.

3. What are the main segments of the Automotive Software Industry?

The market segments include Application, Vehicle Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 10.07 Million as of 2022.

5. What are some drivers contributing to market growth?

The Growth of The Global Automotive Turbocharger Market.

6. What are the notable trends driving market growth?

Growth of Connected Car Technology Aiding the Market's Growth.

7. Are there any restraints impacting market growth?

Increasing Complexity of Modern Vehicles.

8. Can you provide examples of recent developments in the market?

March 2023: Honda Motor signed a basic agreement for a software development relationship with KPIT Technologies Ltd (KPIT Technologies), one of the major software integration partners for the automotive and mobility industries. Through this collaboration, the two companies will pool their respective strengths, particularly Honda's software architecture, control and safety technologies, and KPIT Technologies' software development capabilities, to generate new value through software. As a result of this collaboration, the two companies will collaborate on software development in the following areas: next-generation electrical/electronic (E&E) architecture operating system (OS), electrified powertrains, enhanced safety and automated driving, and IVI (in-vehicle infotainment) and linked technologies.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Software Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Software Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Software Industry?

To stay informed about further developments, trends, and reports in the Automotive Software Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence