Key Insights

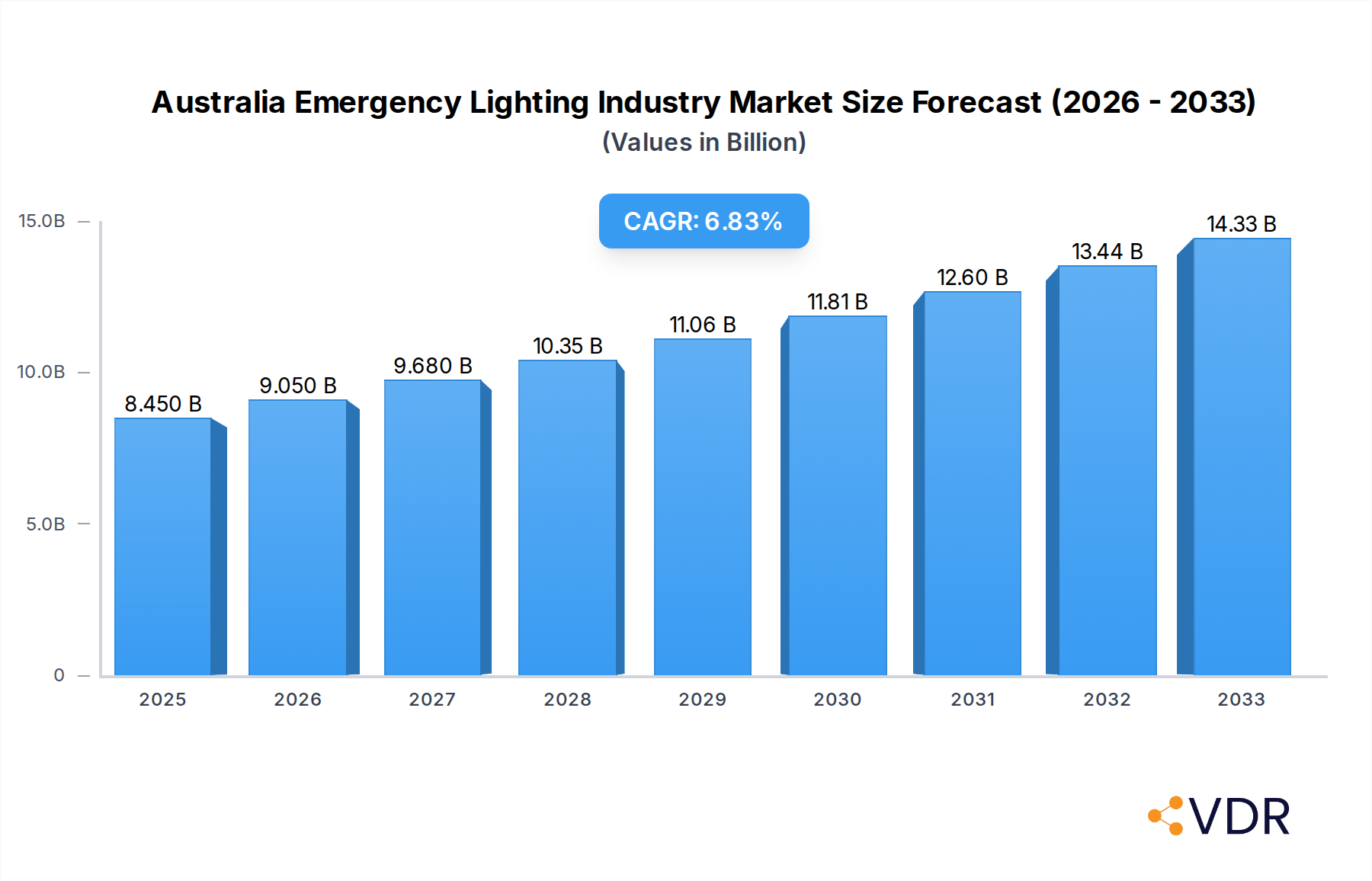

The Australian emergency lighting market is poised for significant expansion, projected to reach USD 8.45 billion by 2025. This robust growth is underpinned by a compelling Compound Annual Growth Rate (CAGR) of 7.13% from 2019 to 2033. This upward trajectory is primarily driven by increasingly stringent safety regulations across residential, industrial, and commercial sectors, mandating the installation and regular maintenance of reliable emergency lighting systems. Furthermore, a rising awareness of occupant safety during power outages and emergencies, coupled with the ongoing construction and renovation of buildings, particularly in urban centers, are crucial accelerators for market demand. The integration of smart technologies, offering enhanced monitoring, control, and energy efficiency, is also shaping the market, with a growing preference for self-contained power systems in smaller installations and central power systems for larger, complex facilities.

Australia Emergency Lighting Industry Market Size (In Billion)

Despite the positive outlook, certain factors may temper the market's pace. The initial high cost of advanced emergency lighting systems and installation can present a barrier, especially for smaller businesses and older residential buildings. Additionally, the availability of counterfeit or sub-standard products could pose a challenge to market integrity and consumer trust. However, the overarching trend towards improved safety standards and technological advancements in emergency lighting solutions is expected to outweigh these restraints. Key industry players are actively focusing on developing innovative, energy-efficient, and compliant products, while government initiatives promoting building safety further solidify the market's growth potential. The strategic adoption of emergency lighting solutions in both new constructions and retrofits will be critical in meeting the escalating safety demands across Australia.

Australia Emergency Lighting Industry Company Market Share

Comprehensive Australia Emergency Lighting Industry Report: Market Dynamics, Growth Prospects, and Key Player Analysis (2019-2033)

Gain unparalleled insights into the Australian emergency lighting market with this in-depth report. Covering the historical period of 2019–2024, the base and estimated year of 2025, and a robust forecast period of 2025–2033, this analysis provides a complete picture of market evolution, drivers, challenges, and future opportunities. Understand the intricate interplay of parent and child markets, explore technological innovations, and identify the key players shaping the industry. With a focus on high-traffic SEO keywords and actionable data, this report is essential for manufacturers, distributors, installers, safety professionals, and investors navigating the Australian emergency lighting landscape. The market is projected to reach $1.2 billion by 2025 and is expected to grow at a CAGR of 7.5% during the forecast period.

Australia Emergency Lighting Industry Market Dynamics & Structure

The Australian emergency lighting market exhibits a moderate to high concentration, with a few dominant players holding significant market share. Technological innovation, particularly in LED efficiency, smart connectivity, and interoperability, serves as a primary driver. Stringent regulatory frameworks, including Australian Standards like AS 2293, mandate compliance and drive demand for advanced systems. Competitive product substitutes, such as basic exit signs and non-integrated lighting solutions, exist but are increasingly being outpaced by feature-rich, networked emergency lighting. End-user demographics are shifting, with a growing emphasis on safety, sustainability, and intelligent building integration across residential, industrial, and commercial sectors. Mergers and acquisitions (M&A) are expected to play a role in consolidating the market, particularly among smaller innovators seeking wider distribution networks.

- Market Concentration: Dominated by a mix of established global players with local subsidiaries and strong domestic manufacturers.

- Technological Innovation: Driven by advancements in LED technology, battery longevity, wireless communication (IoT), and centralized monitoring systems.

- Regulatory Framework: Australian Standards (AS 2293) are crucial, influencing product design and installation requirements, creating demand for compliant solutions.

- Competitive Substitutes: Basic non-maintained emergency luminaires and standalone battery backup units are common but offer limited functionality compared to modern integrated systems.

- End-User Demographics: Growing demand from sectors requiring high safety standards, such as healthcare, education, and critical infrastructure, alongside a rising awareness in residential and general commercial spaces.

- M&A Trends: Potential for consolidation as larger companies acquire niche technology providers to enhance their product portfolios and market reach.

Australia Emergency Lighting Industry Growth Trends & Insights

The Australian emergency lighting industry is on a robust growth trajectory, fueled by evolving safety regulations, increasing construction activity, and a burgeoning demand for smarter, more reliable safety solutions. The market size, valued at approximately $1.0 billion in 2024, is projected to expand significantly to reach an estimated $1.2 billion by the base year 2025. This growth is further expected to accelerate, reaching an impressive valuation by the end of the forecast period in 2033. Adoption rates for advanced emergency lighting systems, particularly those incorporating LED technology and smart monitoring capabilities, are on the rise, driven by their energy efficiency, extended lifespan, and enhanced diagnostic features. Technological disruptions are playing a pivotal role, with the integration of IoT and wireless communication enabling real-time monitoring, automated testing, and seamless integration with building management systems. This not only improves operational efficiency but also significantly enhances safety outcomes. Consumer behavior is shifting towards prioritizing safety and compliance, influenced by a greater awareness of potential risks and the benefits of proactive safety measures. The increasing focus on sustainable building practices also favors LED-based emergency lighting due to its reduced energy consumption and longer operational life. The forecast period (2025-2033) anticipates a Compound Annual Growth Rate (CAGR) of approximately 7.5%, indicating sustained expansion. Market penetration is expected to deepen across all end-user verticals as building codes are updated and safety standards are continuously reinforced. The move towards centralized power systems, while still a smaller segment, is gaining traction, offering greater control and efficiency for large installations.

Dominant Regions, Countries, or Segments in Australia Emergency Lighting Industry

Within the Australian emergency lighting industry, the Commercial end-user vertical stands out as the dominant segment driving market growth. This dominance is propelled by a confluence of factors, including extensive construction and renovation projects across urban centers, stringent compliance requirements for public and private buildings, and a continuous need for reliable safety infrastructure in diverse commercial settings such as offices, retail spaces, hospitals, and educational institutions. The market share for the commercial segment is estimated to be around 45% of the total market value, with a projected CAGR of 8.2% during the forecast period.

- Commercial End-User Vertical:

- Market Drivers: High density of commercial buildings, ongoing infrastructure development, strict safety regulations for public access areas, and increasing adoption of smart building technologies.

- Market Share: Estimated at 45% of the total market value.

- Growth Potential: Significant due to a continuous pipeline of new constructions and retrofitting projects.

- Key Sub-segments: Office buildings, retail centers, healthcare facilities, educational institutions, and hospitality venues.

- Technological Adoption: High uptake of interconnected systems for centralized monitoring and automated testing.

The Industrial end-user vertical also represents a significant and growing segment, estimated at 30% of the market, with a CAGR of 7.0%. This segment is characterized by unique safety challenges in environments like manufacturing plants, warehouses, and mining operations. The implementation of advanced emergency lighting solutions is critical for worker safety, particularly in hazardous conditions.

- Industrial End-User Vertical:

- Market Drivers: High-risk environments requiring robust and reliable safety systems, increasing automation in industrial processes, and stringent safety protocols in sectors like mining and manufacturing.

- Market Share: Estimated at 30% of the total market value.

- Growth Potential: Steady growth driven by the need for enhanced safety in industrial settings and technological upgrades.

- Key Sub-segments: Manufacturing facilities, mining operations, warehouses, and energy production sites.

- Technological Adoption: Demand for durable, high-intensity lighting solutions and specialized systems for hazardous environments.

The Residential end-user vertical, accounting for the remaining 25% of the market with a CAGR of 6.5%, is witnessing a gradual but steady increase in adoption. This is attributed to rising consumer awareness regarding home safety, government initiatives promoting fire safety, and the integration of smart home technologies.

- Residential End-User Vertical:

- Market Drivers: Growing consumer awareness of home safety, increased adoption of smart home devices, and regulatory pushes for mandatory safety features in new builds.

- Market Share: Estimated at 25% of the total market value.

- Growth Potential: Expanding as smart home integration becomes more mainstream and safety becomes a higher priority for homeowners.

- Key Sub-segments: New home construction, apartment buildings, and existing home retrofits.

- Technological Adoption: Increasing interest in battery-backed lighting for power outages and integrated safety systems.

In terms of Power Systems, the Self-contained Power System segment currently holds the largest market share, estimated at 70%, due to its widespread use and ease of installation in smaller to medium-sized applications. However, the Central Power System segment, though smaller at 30%, is experiencing faster growth, projected at a CAGR of 8.5%, driven by its efficiency, scalability, and advanced monitoring capabilities, especially in large commercial and industrial complexes.

Australia Emergency Lighting Industry Product Landscape

The Australian emergency lighting product landscape is characterized by a strong shift towards energy-efficient LED technology, enhanced battery performance, and intelligent connectivity. Manufacturers are increasingly offering integrated solutions that combine emergency lighting with evacuation management systems, providing multi-directional light pulses and color cues for clearer guidance during emergencies. Unique selling propositions include extended battery backup times, self-testing functionalities, remote monitoring capabilities via web interfaces and mobile applications, and interoperability with third-party building management systems through open APIs. Advanced product features include networked controllers, low-cost smart emergency lighting solutions, and specialized lighting for hazardous environments like underground mines, demonstrating a commitment to innovation and safety across diverse applications. The market is seeing a proliferation of compact, aesthetically pleasing designs suitable for various architectural styles.

Key Drivers, Barriers & Challenges in Australia Emergency Lighting Industry

Key Drivers:

- Stringent Safety Regulations: Mandates like AS 2293 drive consistent demand for compliant emergency lighting.

- Technological Advancements: The transition to energy-efficient LEDs, smart connectivity, and IoT integration offers enhanced functionality and reliability.

- Increasing Construction Activity: New commercial, industrial, and residential building projects necessitate the installation of emergency lighting systems.

- Growing Safety Awareness: A heightened focus on occupant safety and emergency preparedness across all sectors.

Barriers & Challenges:

- High Initial Investment: Advanced, interconnected systems can have a higher upfront cost, impacting adoption in budget-constrained projects.

- Complex Installation & Maintenance: Some networked systems require specialized knowledge for installation and ongoing maintenance, increasing operational costs.

- Supply Chain Disruptions: Global and local supply chain vulnerabilities can impact the availability and cost of components.

- Competition from Lower-Cost Alternatives: The presence of basic, non-integrated emergency lighting solutions can pose a challenge in price-sensitive markets.

- Evolving Standards: Keeping pace with frequent updates and amendments to Australian Standards requires continuous product development and compliance efforts.

Emerging Opportunities in Australia Emergency Lighting Industry

Emerging opportunities lie in the expansion of smart emergency lighting solutions for interconnected buildings and the development of specialized systems for niche markets like aged care facilities and remote work sites. The increasing adoption of Building Information Modeling (BIM) presents an opportunity for manufacturers to integrate their product data, streamlining the design and installation process. Furthermore, the growing emphasis on cybersecurity for connected devices opens avenues for providers offering secure and resilient emergency lighting networks. The demand for sustainable and energy-efficient solutions will continue to drive innovation in battery technology and low-power LED components.

Growth Accelerators in the Australia Emergency Lighting Industry Industry

The long-term growth of the Australian emergency lighting industry is being accelerated by significant technological breakthroughs, strategic partnerships, and proactive market expansion strategies. The ongoing refinement of wireless IoT connectivity is enabling massive-scale, low-cost smart emergency lighting solutions, as exemplified by partnerships between leading manufacturers and connectivity providers. Furthermore, the development of interoperable emergency lighting systems that integrate seamlessly with existing building management and safety infrastructure is a key accelerator, enhancing system efficiency and data-driven decision-making. Strategic collaborations and alliances are fostering innovation and expanding market reach, leading to wider adoption of advanced safety technologies.

Key Players Shaping the Australia Emergency Lighting Industry Market

- BARDIC

- Haneco Lighting Australia Pty Ltd

- WBS Technology ABN

- Famco Lighting Pty Ltd

- Legrand Australia Pty Ltd

- EnLighten Australia

- ABB Australia (ABB Ltd)

- E&E Lighting Australia

- Clevertronics Pty Ltd

Notable Milestones in Australia Emergency Lighting Industry Sector

- September 2022: MineGlow launched em-Control, a technologically advanced, interoperable emergency lighting system designed to improve safety in underground mines. This intelligent, network-based solution provides multi-directional light pulses and colors to guide workers to safety, integrating em-Lighting, em-View, and em-Controller for API integration with third-party systems.

- October 2021: Clevertronics partnered with Wirepas, a wireless IoT connectivity provider. This collaboration is set to deliver massive-scale, low-cost smart emergency lighting solutions, already successfully deployed in 630 sites across Australia, New Zealand, and the United Kingdom.

In-Depth Australia Emergency Lighting Industry Market Outlook

The Australian emergency lighting industry is poised for substantial growth, driven by an increasing emphasis on safety, technological advancements, and evolving regulatory landscapes. Future market potential is high, with opportunities for smart, interconnected lighting solutions that offer enhanced monitoring and control. Strategic opportunities lie in catering to specific end-user verticals with tailored product offerings, such as specialized systems for critical infrastructure and hazardous environments. The continued adoption of LED technology, coupled with innovations in battery management and wireless communication, will further fuel market expansion. The industry's commitment to providing reliable, efficient, and intelligent emergency lighting solutions positions it for sustained success in safeguarding lives and property across Australia.

Australia Emergency Lighting Industry Segmentation

-

1. Power System

- 1.1. Self-contained Power System

- 1.2. Central Power System

-

2. End-user Vertical

- 2.1. Residential

- 2.2. Industrial

- 2.3. Commercial

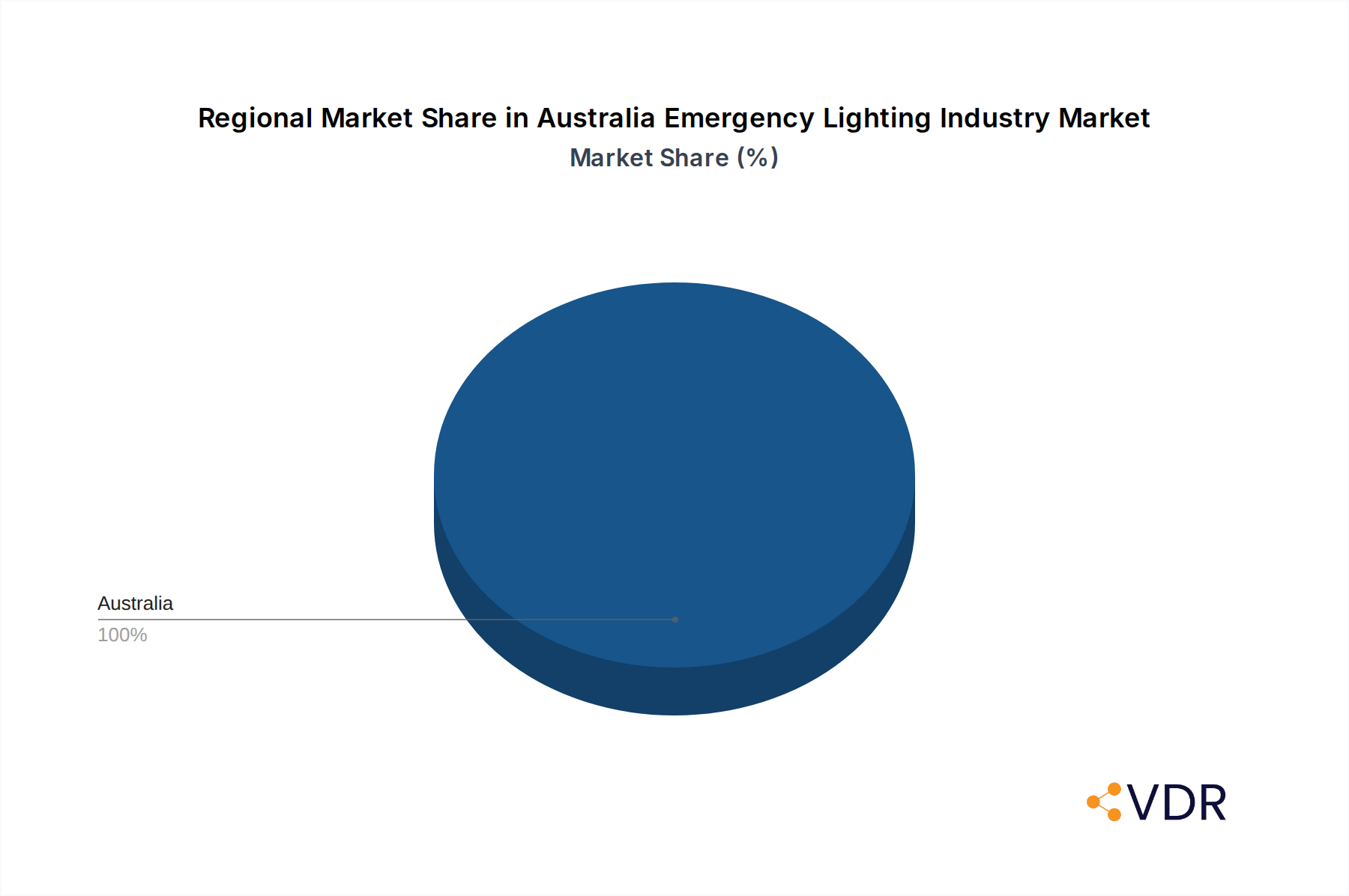

Australia Emergency Lighting Industry Segmentation By Geography

- 1. Australia

Australia Emergency Lighting Industry Regional Market Share

Geographic Coverage of Australia Emergency Lighting Industry

Australia Emergency Lighting Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.13% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Power System

- 5.1.1. Self-contained Power System

- 5.1.2. Central Power System

- 5.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 5.2.1. Residential

- 5.2.2. Industrial

- 5.2.3. Commercial

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Australia

- 5.1. Market Analysis, Insights and Forecast - by Power System

- 6. Australia Emergency Lighting Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Power System

- 6.1.1. Self-contained Power System

- 6.1.2. Central Power System

- 6.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 6.2.1. Residential

- 6.2.2. Industrial

- 6.2.3. Commercial

- 6.1. Market Analysis, Insights and Forecast - by Power System

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 BARDIC

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Haneco Lighting Australia Pty Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 WBS Technology ABN

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Famco Lighting Pty Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Legrand Australia Pty Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 EnLighten Australia

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 ABB Australia (ABB Ltd)

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 E&E Lighting Australia

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Clevertronics Pty Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 BARDIC

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Australia Emergency Lighting Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Australia Emergency Lighting Industry Share (%) by Company 2025

List of Tables

- Table 1: Australia Emergency Lighting Industry Revenue billion Forecast, by Power System 2020 & 2033

- Table 2: Australia Emergency Lighting Industry Volume K Unit Forecast, by Power System 2020 & 2033

- Table 3: Australia Emergency Lighting Industry Revenue billion Forecast, by End-user Vertical 2020 & 2033

- Table 4: Australia Emergency Lighting Industry Volume K Unit Forecast, by End-user Vertical 2020 & 2033

- Table 5: Australia Emergency Lighting Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Australia Emergency Lighting Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: Australia Emergency Lighting Industry Revenue billion Forecast, by Power System 2020 & 2033

- Table 8: Australia Emergency Lighting Industry Volume K Unit Forecast, by Power System 2020 & 2033

- Table 9: Australia Emergency Lighting Industry Revenue billion Forecast, by End-user Vertical 2020 & 2033

- Table 10: Australia Emergency Lighting Industry Volume K Unit Forecast, by End-user Vertical 2020 & 2033

- Table 11: Australia Emergency Lighting Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Australia Emergency Lighting Industry Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Australia Emergency Lighting Industry?

The projected CAGR is approximately 7.13%.

2. Which companies are prominent players in the Australia Emergency Lighting Industry?

Key companies in the market include BARDIC, Haneco Lighting Australia Pty Ltd, WBS Technology ABN, Famco Lighting Pty Ltd, Legrand Australia Pty Ltd, EnLighten Australia, ABB Australia (ABB Ltd), E&E Lighting Australia, Clevertronics Pty Ltd.

3. What are the main segments of the Australia Emergency Lighting Industry?

The market segments include Power System, End-user Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.45 billion as of 2022.

5. What are some drivers contributing to market growth?

Supporting Government Regulations (Building Code of Australia (BCA)).

6. What are the notable trends driving market growth?

Commercial Segment in Australia is Expected to Drive the Market.

7. Are there any restraints impacting market growth?

Lack of Awareness Amongst Non-data Center Applications.

8. Can you provide examples of recent developments in the market?

September 2022: MineGlow has launched em-Control, a new technologically advanced, interoperable emergency lighting system designed to improve the safety of underground mines. The em-Control is an intelligent, network-based solution that warns and directs an underground workforce to safety with multi-directional light pulses and colors. The complete system comprises em-Lighting, the LED light strip, em-View, a web interface, and em-Controller, a network-based controller that integrates with third-party systems via an open application programming interface (API).

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Australia Emergency Lighting Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Australia Emergency Lighting Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Australia Emergency Lighting Industry?

To stay informed about further developments, trends, and reports in the Australia Emergency Lighting Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence