Key Insights

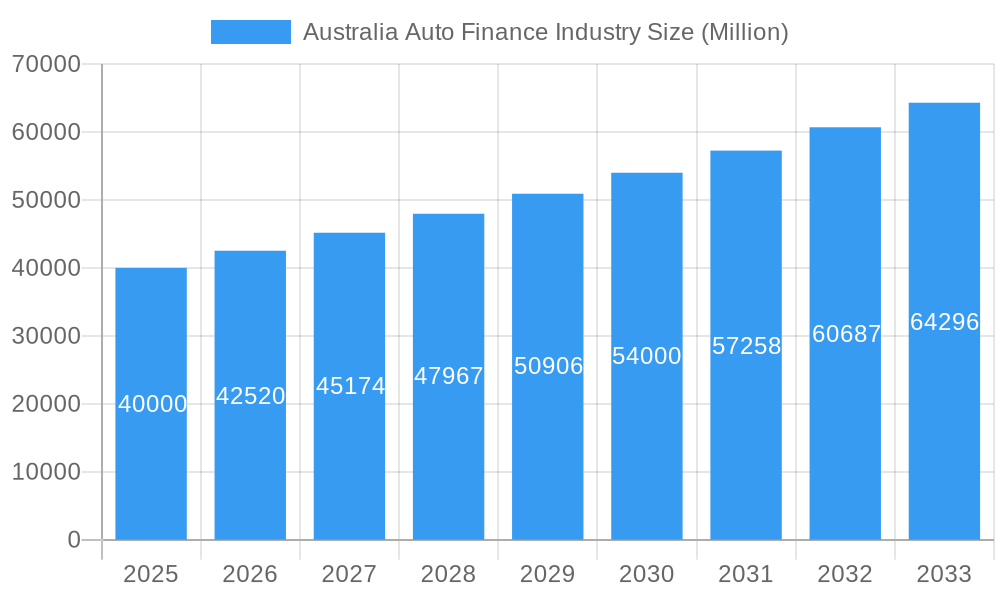

The Australian auto finance sector is projected to experience significant expansion. With a base year of 2025, the market is estimated at 183.4 billion AUD. This market is expected to grow at a Compound Annual Growth Rate (CAGR) of 1.4% from 2025 to 2033. Key growth catalysts include sustained demand for new and used vehicles, evolving consumer preferences, and increased accessibility of financing. Emerging demographics entering the vehicle ownership market, economic recovery boosting consumer spending, and the adoption of digital platforms for streamlined loan processes are also significant drivers. The increasing popularity of electric and hybrid vehicles, supported by government incentives, is reshaping market dynamics and creating new avenues for finance providers.

Australia Auto Finance Industry Market Size (In Billion)

Digitalization is a dominant trend, with online applications and approvals becoming standard in auto finance. The integration of Buy Now, Pay Later (BNPL) solutions for vehicle purchases is enhancing customer convenience and broadening the reach of finance providers. Challenges include stringent regulatory frameworks and fluctuating interest rates, which can impact consumer affordability and lender margins. Intense competition among traditional banks, credit unions, and specialized finance companies necessitates continuous innovation in products and customer service. Passenger cars continue to dominate financing, while the commercial vehicle segment shows a steady increase in demand.

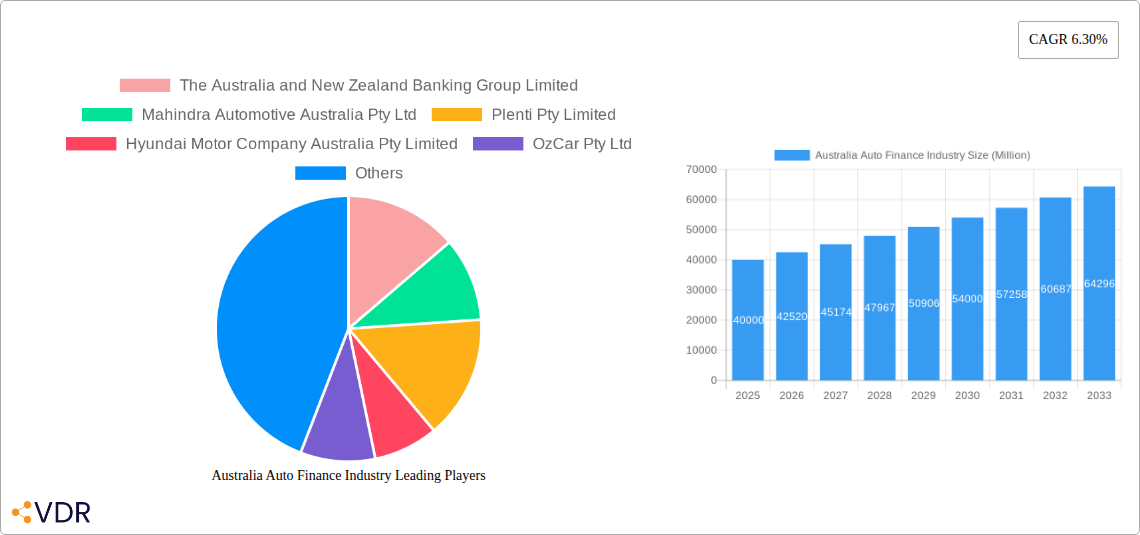

Australia Auto Finance Industry Company Market Share

This report offers an in-depth analysis of the Australian Auto Finance Industry, examining market dynamics, growth trends, regional insights, product offerings, key drivers, challenges, and emerging opportunities. It provides a detailed outlook for the period 2019–2033, with 2025 designated as the base and estimated year. The analysis utilizes high-traffic keywords and detailed market segmentation to deliver actionable intelligence for industry professionals, investors, and stakeholders.

Australia Auto Finance Industry Market Dynamics & Structure

The Australian auto finance industry is characterized by a moderately concentrated market, with established banks and financial institutions holding significant market share. Technological innovation is a key driver, pushing for digitalized loan application processes, online comparison tools, and the integration of AI for risk assessment. Regulatory frameworks, overseen by bodies like the Australian Securities and Investments Commission (ASIC), emphasize consumer protection and responsible lending, influencing product development and operational procedures. Competitive product substitutes include outright cash purchases, leasing, and personal loans from non-automotive lenders, though auto finance remains the dominant financing method. End-user demographics are evolving, with younger consumers increasingly seeking flexible financing options and digital experiences, while traditional buyers still value established lender relationships. Merger and acquisition (M&A) trends are present, driven by a desire to expand market reach, acquire technological capabilities, and consolidate market share.

- Market Concentration: Dominated by major banking groups and specialized auto finance providers.

- Technological Innovation Drivers: Digitalization of loan origination, AI-powered credit scoring, mobile-first customer interfaces.

- Regulatory Frameworks: Focus on consumer credit reforms, responsible lending obligations, and data privacy.

- Competitive Product Substitutes: Personal loans, leasing options, peer-to-peer lending platforms.

- End-User Demographics: Growing demand for flexible repayment plans, online accessibility, and transparent fee structures.

- M&A Trends: Strategic acquisitions aimed at market consolidation and technological enhancement.

Australia Auto Finance Industry Growth Trends & Insights

The Australia Auto Finance Industry is projected to witness robust growth throughout the forecast period, driven by increasing vehicle sales, evolving consumer preferences for financing, and technological advancements in the fintech sector. The market size is expected to grow from approximately $XX,XXX million in 2019 to an estimated $XX,XXX million by 2033, exhibiting a compound annual growth rate (CAGR) of approximately X.XX%. Adoption rates for digital lending platforms are on the rise, significantly streamlining the application and approval process for both new and used vehicle financing. Technological disruptions, such as the integration of blockchain for secure transaction verification and the use of big data analytics for personalized loan offerings, are transforming the competitive landscape. Consumer behavior shifts are evident, with a growing preference for convenient, transparent, and mobile-accessible finance solutions. This includes a rising interest in flexible loan terms, a greater willingness to explore alternative lenders, and an increased focus on understanding the total cost of ownership beyond the vehicle price. The resurgence in demand for personal vehicles, coupled with the increasing complexity of vehicle purchasing decisions influenced by factors like electrification and autonomous driving, further fuels the need for specialized auto finance solutions. The market penetration of auto finance is expected to remain high, as the upfront cost of vehicles continues to be a significant barrier for many Australian consumers.

Dominant Regions, Countries, or Segments in Australia Auto Finance Industry

Within the Australia Auto Finance Industry, the New Vehicle segment, specifically within Passenger Cars, driven by Banks as a source type, currently demonstrates the most significant market dominance and growth potential. This dominance is underpinned by several key factors, including the consistent demand for new passenger vehicles across the country, particularly in major urban centers like Sydney and Melbourne. Banks, as established financial institutions, leverage their strong brand recognition, extensive customer base, and competitive interest rates to capture a substantial share of this market. The infrastructure in these dominant regions, characterized by well-developed road networks and a high population density, supports consistent vehicle sales and, consequently, auto finance uptake.

- Key Drivers for New Vehicle Passenger Car Segment Financed by Banks:

- High Consumer Demand: Consistent sales of new passenger cars, fueled by new model releases and consumer preference for modern features and fuel efficiency.

- Economic Policies: Government incentives for new car purchases or favorable depreciation policies for businesses can indirectly boost financed sales.

- Infrastructure Development: Urban sprawl and the need for personal mobility in growing metropolitan areas drive demand.

- Bank's Competitive Advantage: Established trust, broad product offerings, and competitive rates offered by major banking groups.

- Technological Integration: Banks are increasingly offering online application and approval processes, enhancing customer convenience for new vehicle purchases.

The Used Vehicle segment also presents substantial growth, particularly for Financial Institutions and OEM (Original Equipment Manufacturer) finance arms, reflecting the affordability factor and ongoing demand for pre-owned cars. While Passenger Cars lead in volume, Commercial Vehicles are experiencing significant growth in financing, driven by the expansion of small businesses and the logistics sector. The Credit Unions and Financial Institutions are increasingly competing with banks by offering more specialized and sometimes more flexible financing options, particularly for used vehicles and commercial fleets. The growth potential in these sub-segments is attributed to the increasing affordability concerns for new vehicles and the ongoing need for commercial transport solutions.

Australia Auto Finance Industry Product Landscape

The Australia Auto Finance Industry is evolving with innovative product offerings designed to meet diverse consumer needs. This includes competitive loan products with flexible repayment schedules, low-interest rate introductory offers, and balloon payment options for used vehicles. Innovations in digital platforms allow for instant pre-approval and online loan management, enhancing customer experience. Performance metrics often focus on competitive Annual Percentage Rates (APRs), loan tenure flexibility, and the ease of the application process. Unique selling propositions include tailored finance packages for specific vehicle types, such as electric vehicles or commercial fleets, and integrated insurance or warranty options. Technological advancements are also seen in the development of risk assessment models that can offer more personalized loan terms based on individual credit profiles.

Key Drivers, Barriers & Challenges in Australia Auto Finance Industry

Key Drivers: The Australia Auto Finance Industry is propelled by a confluence of factors, including sustained consumer demand for personal mobility, particularly for new and used passenger vehicles. Technological advancements in digital lending platforms are streamlining the application and approval process, enhancing customer convenience. Favorable economic conditions, characterized by low unemployment rates and stable interest rates, encourage borrowing. Government initiatives aimed at stimulating the automotive sector and promoting newer, more fuel-efficient vehicles also act as significant drivers. The increasing popularity of electric vehicles (EVs) is creating a new financing frontier, with specialized loan products emerging to support this transition.

Barriers & Challenges: A primary challenge remains the increasing cost of vehicles, which can deter potential buyers and strain affordability, even with financing. Stringent regulatory frameworks, while crucial for consumer protection, can sometimes lead to longer approval times and increased compliance costs for lenders. Competition from non-bank lenders and fintech companies is intensifying, putting pressure on margins. Supply chain disruptions affecting vehicle availability can also indirectly impact the auto finance market by limiting the pool of available vehicles for financing. Rising interest rates pose a significant challenge, increasing the cost of borrowing for consumers and potentially slowing down demand.

Emerging Opportunities in Australia Auto Finance Industry

Emerging opportunities within the Australia Auto Finance Industry lie in the growing demand for financing electric and hybrid vehicles, driven by environmental consciousness and government incentives. The expansion of the used car market presents a significant opportunity, with consumers seeking more affordable options. Fintech innovations, such as AI-powered loan origination and blockchain for enhanced security and transparency, offer pathways to improve efficiency and customer experience. Furthermore, the increasing demand for flexible and personalized finance solutions, including pay-as-you-go or usage-based models, presents an untapped market. Partnerships between automotive manufacturers, dealerships, and fintech companies can unlock new distribution channels and customer segments.

Growth Accelerators in the Australia Auto Finance Industry Industry

Several catalysts are accelerating long-term growth in the Australia Auto Finance Industry. Technological breakthroughs in data analytics and artificial intelligence are enabling more sophisticated credit risk assessment, leading to faster approvals and more personalized loan products. Strategic partnerships between automotive OEMs and financial institutions are crucial for developing integrated buying and financing experiences, enhancing customer loyalty and driving sales. The ongoing digital transformation of the financial services sector, with a focus on seamless online customer journeys and mobile accessibility, is a key growth accelerator. Furthermore, market expansion strategies targeting underserved demographics and regional areas, coupled with the development of innovative financing solutions for emerging vehicle technologies, are vital for sustained growth.

Key Players Shaping the Australia Auto Finance Industry Market

- The Australia and New Zealand Banking Group Limited

- Mahindra Automotive Australia Pty Ltd

- Plenti Pty Limited

- Hyundai Motor Company Australia Pty Limited

- OzCar Pty Ltd

- Toyota Finance Australia Limited

- Kia Australia Pty Ltd

- Mozo Pty Ltd

- National Australian Bank

- Dutton Group

Notable Milestones in Australia Auto Finance Industry Sector

- 2019: Introduction of stricter responsible lending guidelines by ASIC, impacting loan origination processes.

- 2020: Surge in online car sales and financing applications due to COVID-19 lockdowns, accelerating digital adoption.

- 2021: Increased availability of EV-specific finance products from major lenders and specialized providers.

- 2022: Significant growth in the used car market, driving demand for used vehicle finance solutions.

- 2023: Expansion of buy-now-pay-later (BNPL) options extending into the automotive accessories and smaller vehicle segments.

- 2024: Growing integration of AI and machine learning in credit assessment and fraud detection by leading financiers.

In-Depth Australia Auto Finance Industry Market Outlook

The outlook for the Australia Auto Finance Industry remains exceptionally positive, driven by continued innovation and evolving consumer needs. Future growth will be significantly influenced by the accelerated adoption of electric vehicles and the increasing demand for flexible, digital-first financing solutions. Strategic collaborations between automotive manufacturers, technology providers, and financial institutions will be paramount in creating seamless customer experiences and expanding market reach. The industry is poised for further consolidation and technological advancement, with a strong focus on data-driven insights to personalize offerings and manage risk effectively. Opportunities abound in catering to niche markets, such as specialized commercial vehicle financing and flexible personal mobility solutions, ensuring sustained growth and profitability.

Australia Auto Finance Industry Segmentation

-

1. Type

- 1.1. New Vehicle

- 1.2. Used Vehicle

-

2. Source Type

- 2.1. OEM

- 2.2. Banks

- 2.3. Credit Unions

- 2.4. Financial Institution

-

3. Vehicle Type

- 3.1. Passenger Cars

- 3.2. Commercial Vehicles

Australia Auto Finance Industry Segmentation By Geography

- 1. Australia

Australia Auto Finance Industry Regional Market Share

Geographic Coverage of Australia Auto Finance Industry

Australia Auto Finance Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 1.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. New Vehicle

- 5.1.2. Used Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Source Type

- 5.2.1. OEM

- 5.2.2. Banks

- 5.2.3. Credit Unions

- 5.2.4. Financial Institution

- 5.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.3.1. Passenger Cars

- 5.3.2. Commercial Vehicles

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Australia

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Australia Auto Finance Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. New Vehicle

- 6.1.2. Used Vehicle

- 6.2. Market Analysis, Insights and Forecast - by Source Type

- 6.2.1. OEM

- 6.2.2. Banks

- 6.2.3. Credit Unions

- 6.2.4. Financial Institution

- 6.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.3.1. Passenger Cars

- 6.3.2. Commercial Vehicles

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 The Australia and New Zealand Banking Group Limited

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Mahindra Automotive Australia Pty Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Plenti Pty Limited

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Hyundai Motor Company Australia Pty Limited

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 OzCar Pty Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Toyota Finance Australia Limited

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Kia Australia Pty Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Mozo Pty Ltd *List Not Exhaustive

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 National Australian Bank

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Dutton Group

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 The Australia and New Zealand Banking Group Limited

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Australia Auto Finance Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Australia Auto Finance Industry Share (%) by Company 2025

List of Tables

- Table 1: Australia Auto Finance Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Australia Auto Finance Industry Revenue billion Forecast, by Source Type 2020 & 2033

- Table 3: Australia Auto Finance Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 4: Australia Auto Finance Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Australia Auto Finance Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Australia Auto Finance Industry Revenue billion Forecast, by Source Type 2020 & 2033

- Table 7: Australia Auto Finance Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 8: Australia Auto Finance Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Australia Auto Finance Industry?

The projected CAGR is approximately 1.4%.

2. Which companies are prominent players in the Australia Auto Finance Industry?

Key companies in the market include The Australia and New Zealand Banking Group Limited, Mahindra Automotive Australia Pty Ltd, Plenti Pty Limited, Hyundai Motor Company Australia Pty Limited, OzCar Pty Ltd, Toyota Finance Australia Limited, Kia Australia Pty Ltd, Mozo Pty Ltd *List Not Exhaustive, National Australian Bank, Dutton Group.

3. What are the main segments of the Australia Auto Finance Industry?

The market segments include Type, Source Type, Vehicle Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 183.4 billion as of 2022.

5. What are some drivers contributing to market growth?

Government Initiatives to Promote Sales of Electric Vehicle.

6. What are the notable trends driving market growth?

Used Vehicle to Gain Momentum.

7. Are there any restraints impacting market growth?

High Initial Investment for Installing Electric Vehicle Charging Infrastructure.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Australia Auto Finance Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Australia Auto Finance Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Australia Auto Finance Industry?

To stay informed about further developments, trends, and reports in the Australia Auto Finance Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence