Key Insights

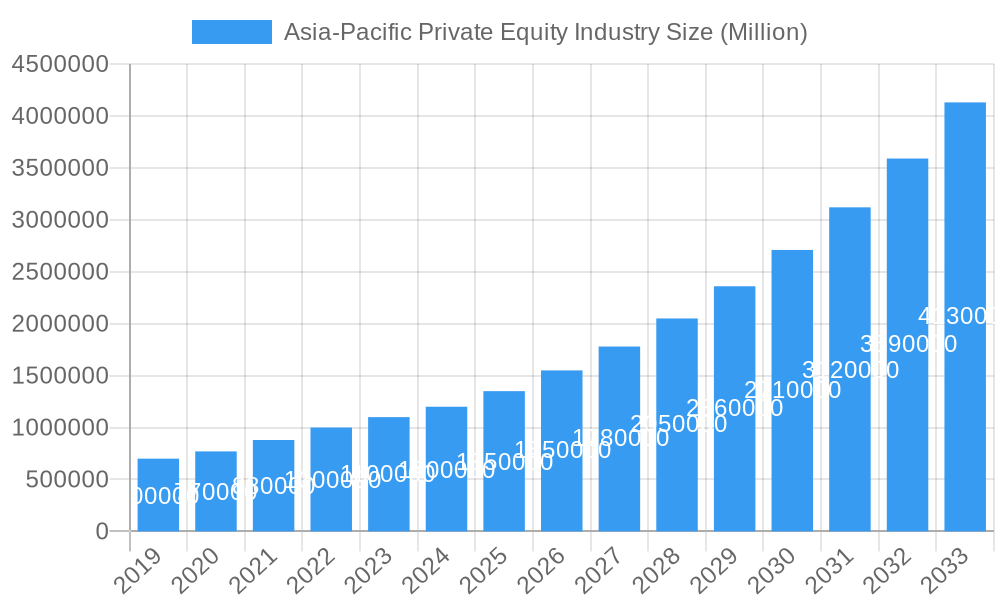

The Asia-Pacific private equity industry is experiencing robust expansion, driven by a confluence of factors including burgeoning economies, a growing pool of institutional investors, and increasing deal activity across diverse sectors. The market, estimated to be valued at approximately $1.2 trillion in 2025, is poised for significant growth, projecting a Compound Annual Growth Rate (CAGR) of around 15% over the study period from 2019 to 2033. This upward trajectory is underpinned by a dynamic investment landscape characterized by a surge in venture capital funding for technology and digital transformation initiatives, coupled with a sustained interest in established industries like infrastructure and consumer goods. The region's large and increasingly affluent population, coupled with favorable government policies supporting foreign investment and business development, further fuels this expansion. Emerging markets within Asia-Pacific are particularly attractive, offering higher return potential and a less saturated investment environment compared to more developed economies.

Asia-Pacific Private Equity Industry Market Size (In Billion)

Looking ahead, the Asia-Pacific private equity sector is expected to witness continued innovation in investment strategies, with a greater emphasis on Environmental, Social, and Governance (ESG) factors becoming a key differentiator for investors. The forecast period from 2025 to 2033 will likely see a continued influx of both domestic and international capital, attracted by the region's long-term growth prospects. Sectors such as healthcare, renewable energy, and fintech are anticipated to be major beneficiaries of this investment boom. Deal sizes are also expected to increase, reflecting the growing maturity of the market and the increasing confidence of private equity firms in the region's economic resilience. Strategic partnerships and co-investment opportunities are also likely to become more prevalent as firms seek to leverage each other's expertise and mitigate risks. The industry's evolution will be closely monitored by global investors seeking diversification and substantial returns.

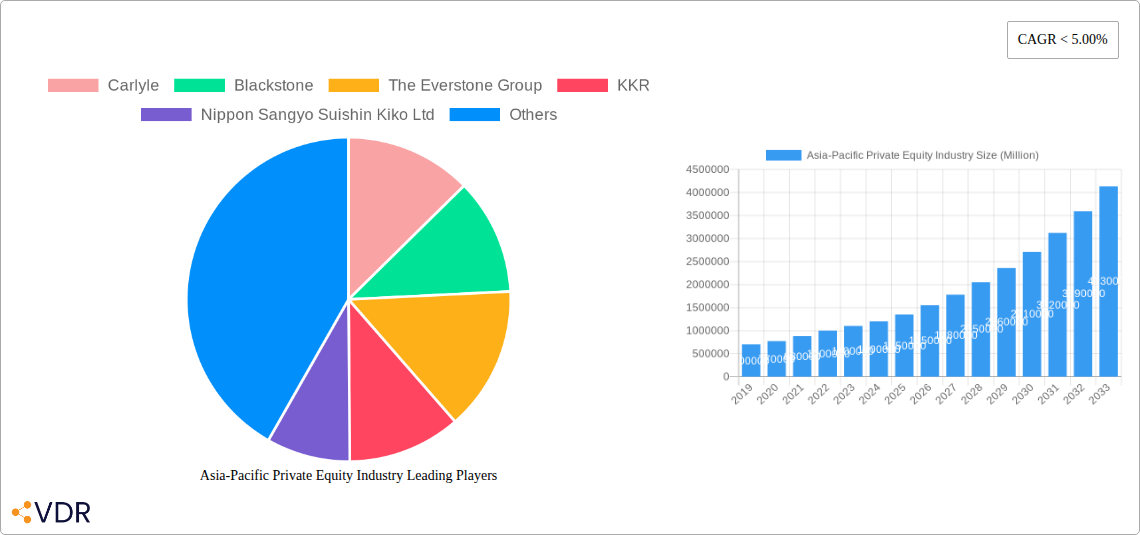

Asia-Pacific Private Equity Industry Company Market Share

Asia-Pacific Private Equity Industry: Market Analysis, Growth Trends, and Future Outlook (2019-2033)

This comprehensive report delves into the dynamic Asia-Pacific Private Equity (PE) industry, offering an in-depth analysis of its market dynamics, growth trajectory, regional dominance, and future potential. Covering the period from 2019 to 2033, with a base year of 2025, this study provides critical insights for investors, fund managers, and industry stakeholders navigating this rapidly evolving landscape. We explore key segments like Real Estate, Private Investment in Public Equity (PIPE), Buyouts, and Exits, alongside pivotal industry developments and the strategic plays of leading firms.

Asia-Pacific Private Equity Industry Market Dynamics & Structure

The Asia-Pacific private equity market is characterized by a moderately concentrated structure, with a few dominant global players and a growing number of regional specialists vying for attractive deals. Technological innovation acts as a significant driver, particularly in FinTech, HealthTech, and Digital Infrastructure, enabling new investment models and enhancing operational efficiency for portfolio companies. Regulatory frameworks are diverse across the region, presenting both opportunities and challenges, with increasing scrutiny on ESG compliance and cross-border investments. Competitive product substitutes are limited, primarily revolving around venture capital, hedge funds, and direct investments, though the unique illiquidity and long-term growth potential of private equity continue to attract significant capital. End-user demographics are shifting towards a burgeoning middle class with increasing disposable income and a growing demand for sophisticated financial products. Mergers and Acquisitions (M&A) trends are robust, driven by consolidation, cross-border expansion, and the pursuit of scale.

- Market Concentration: Dominated by a mix of global powerhouses and specialized regional funds, with increasing competition for prime assets.

- Technological Innovation: Crucial for deal sourcing, due diligence, portfolio management, and value creation, especially in growth sectors.

- Regulatory Environment: Varied across countries, with a growing emphasis on transparency, ESG, and investor protection.

- M&A Trends: Active deal-making, including sector consolidation, platform acquisitions, and divestitures, to optimize portfolios and achieve strategic objectives.

Asia-Pacific Private Equity Industry Growth Trends & Insights

The Asia-Pacific private equity industry is poised for substantial growth, projected to witness a Compound Annual Growth Rate (CAGR) of xx% from 2025 to 2033. This expansion is fueled by a confluence of factors, including robust economic expansion across key Asian economies, a burgeoning pool of institutional and high-net-worth investors seeking higher yields, and a continuous pipeline of attractive investment opportunities. Adoption rates for private equity investments are escalating as more limited partners (LPs) recognize the asset class's potential for superior risk-adjusted returns compared to traditional public markets. Technological disruptions are not only creating new investment verticals but also transforming the way PE firms operate, from data analytics for deal evaluation to digital platforms for portfolio management. Consumer behavior shifts, marked by increased digital engagement and a growing appetite for innovative products and services, are creating fertile ground for PE-backed companies in sectors like e-commerce, digital media, and personalized healthcare. The increasing sophistication of regional markets and the ongoing liberalization of investment policies further contribute to this upward trend, making the Asia-Pacific region a focal point for global private equity capital. The market penetration of private equity is expected to deepen significantly, with a substantial increase in Assets Under Management (AUM) by the forecast period.

Dominant Regions, Countries, or Segments in Asia-Pacific Private Equity Industry

The Asia-Pacific private equity industry's dominance is most pronounced in the Buyouts segment, closely followed by Real Estate investments and Exits. China, India, and Southeast Asian nations are emerging as key growth hubs, driven by their large populations, expanding middle class, and supportive government policies aimed at fostering economic development and foreign investment. China, despite recent regulatory shifts, continues to be a major destination for PE capital, particularly in technology and consumer-focused sectors. India presents a compelling growth story with its rapidly developing economy, a vibrant startup ecosystem, and a significant appetite for growth capital across various industries. Southeast Asia, encompassing countries like Singapore, Indonesia, and Vietnam, is gaining traction due to its demographic advantages, increasing digitalization, and a strategic geographic position.

- Buyouts: Represent the largest segment, driven by the desire of PE firms to acquire mature businesses, implement operational improvements, and achieve capital appreciation through strategic exits. Deal sizes in this segment are often substantial, reflecting the maturity of target companies and the scale of required transformations.

- Real Estate: A consistently strong performer, fueled by rapid urbanization, infrastructure development, and demand for commercial, residential, and logistics properties across the region. Major cities continue to attract significant PE interest for both core and opportunistic real estate investments.

- Exits: The efficiency of exit strategies, including IPOs and trade sales, is crucial for the overall health of the PE ecosystem and directly influences investor returns. A robust exit environment signals market maturity and investor confidence.

- Private Investment in Public Equity (PIPE): While smaller than buyouts, PIPE transactions are gaining traction as an alternative to traditional buyouts, allowing PE firms to acquire stakes in publicly traded companies, often to drive strategic change or capitalize on undervalued market opportunities.

Key drivers for regional dominance include favorable economic policies, government initiatives to attract foreign capital, and the continuous development of infrastructure that supports business growth and accessibility. The sheer size of the addressable markets in China and India, coupled with the entrepreneurial spirit in Southeast Asia, positions these regions to continue leading the Asia-Pacific PE landscape.

Asia-Pacific Private Equity Industry Product Landscape

The Asia-Pacific private equity industry's product landscape is characterized by a diverse range of investment vehicles and strategies designed to cater to varying risk appetites and return expectations. Beyond traditional buyout and growth equity funds, the market is witnessing a rise in specialized products such as credit funds, real estate funds, infrastructure funds, and venture capital arms. These products leverage unique market opportunities, from investing in distressed debt to capitalizing on the burgeoning demand for renewable energy infrastructure. Performance metrics are increasingly scrutinized, with LPs demanding transparency on Gross IRR, Net IRR, and DPI. Technological advancements are influencing product development, with PE firms exploring digital platforms for LP reporting and portfolio management, thereby enhancing client experience and operational efficiency. Unique selling propositions often lie in the depth of regional expertise, proprietary deal sourcing capabilities, and a proven track record of value creation in specific sectors or geographies.

Key Drivers, Barriers & Challenges in Asia-Pacific Private Equity Industry

The Asia-Pacific private equity industry is propelled by several key drivers. Economic growth across major Asian economies fuels deal flow and provides fertile ground for portfolio company expansion. A rising tide of institutional capital, including pension funds, sovereign wealth funds, and insurance companies, seeking attractive risk-adjusted returns, further bolsters the industry. Government initiatives promoting foreign investment and deregulation in certain sectors create a more conducive environment. Technological advancements and the ongoing digital transformation across the region offer new avenues for investment and value creation, particularly in FinTech, HealthTech, and E-commerce.

However, the industry faces significant barriers and challenges. Regulatory divergence across various Asian countries creates complexity for cross-border transactions and fund domiciliation. Geopolitical risks and trade tensions can impact investment sentiment and deal execution. Limited availability of high-quality, scalable investment opportunities in certain mature markets and the increasing competition among PE firms can lead to higher valuations and compressed deal spreads. Furthermore, talent acquisition and retention in specialized investment roles remain a challenge across many parts of the region. Supply chain disruptions and the potential for rising interest rates can also impact portfolio company performance and exit multiples.

Emerging Opportunities in Asia-Pacific Private Equity Industry

Emerging opportunities within the Asia-Pacific private equity industry are abundant, particularly in the ESG and sustainability-focused investments. As environmental and social consciousness grows, PE firms are increasingly channeling capital into renewable energy, clean technology, and companies with strong sustainability credentials, aligning with global trends and regulatory pressures. The digitalization of traditional industries presents a significant avenue, where PE can invest in companies looking to enhance their online presence, adopt new technologies, and improve operational efficiency. The rapidly growing healthcare and life sciences sectors, driven by an aging population and increasing healthcare expenditure, offer substantial potential for growth and innovation. Furthermore, the consumer sector, buoyed by rising disposable incomes and evolving consumer preferences, particularly in emerging markets, continues to be a rich area for PE investment. Untapped markets within emerging economies, with their vast demographic potential and developing infrastructure, also represent promising long-term opportunities for astute investors.

Growth Accelerators in the Asia-Pacific Private Equity Industry Industry

Long-term growth in the Asia-Pacific private equity industry is significantly accelerated by continued economic liberalization and supportive government policies across key markets, fostering an environment conducive to foreign investment and business expansion. Technological breakthroughs, especially in artificial intelligence, data analytics, and biotechnology, are creating new sectors and enabling innovative business models, thereby expanding the investment universe. Strategic partnerships and collaborations between global and local PE firms are also crucial, leveraging combined expertise, networks, and capital to unlock value in complex markets. Market expansion strategies, including cross-border M&A and the development of specialized funds catering to specific regional needs or asset classes, are further propelling growth. The increasing sophistication of LPs and their growing comfort with private equity as an asset class ensure a steady inflow of capital, acting as a consistent growth catalyst.

Key Players Shaping the Asia-Pacific Private Equity Industry Market

- Carlyle

- Blackstone

- The Everstone Group

- KKR

- Nippon Sangyo Suishin Kiko Ltd

- Bain Capital

- Warburg Pincus

- J-Star

- Ascent Capital

- CVC Capital Partners

Notable Milestones in Asia-Pacific Private Equity Industry Sector

- September 2022: The Asian Development Bank (ADB) signed a USD 15 million equity investment in KV Asia Capital Fund II LP, a private equity fund managed by KV Asia, to provide growth capital to companies in the health care, financial services, education, manufacturing, business services, and consumer sectors across Southeast Asia.

- July 2022: Malaysia-headquartered private equity firm Navis Capital Partners has launched an Asia Credit Platform, Navis Asia Credit.

In-Depth Asia-Pacific Private Equity Industry Market Outlook

The future outlook for the Asia-Pacific private equity industry is exceptionally bright, driven by persistent demographic tailwinds, an expanding middle class, and a maturing investment landscape. Growth accelerators such as ongoing technological innovation, particularly in digital transformation and sustainable solutions, will continue to redefine investment opportunities. Strategic partnerships and the increasing focus on ESG integration are poised to further shape fund strategies and investor demand. The region's dynamic economic environment, coupled with supportive regulatory reforms in key markets, presents substantial untapped potential for value creation. As global capital continues to seek out higher returns, the Asia-Pacific region is expected to remain a pivotal destination for private equity investments, promising significant growth and attractive opportunities for discerning investors.

Asia-Pacific Private Equity Industry Segmentation

-

1. Investment

- 1.1. Real Estate

- 1.2. Private Investment in Public Equity (PIPE)

- 1.3. Buyouts

- 1.4. Exits

Asia-Pacific Private Equity Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. Japan

- 1.3. South Korea

- 1.4. India

- 1.5. Australia

- 1.6. New Zealand

- 1.7. Indonesia

- 1.8. Malaysia

- 1.9. Singapore

- 1.10. Thailand

- 1.11. Vietnam

- 1.12. Philippines

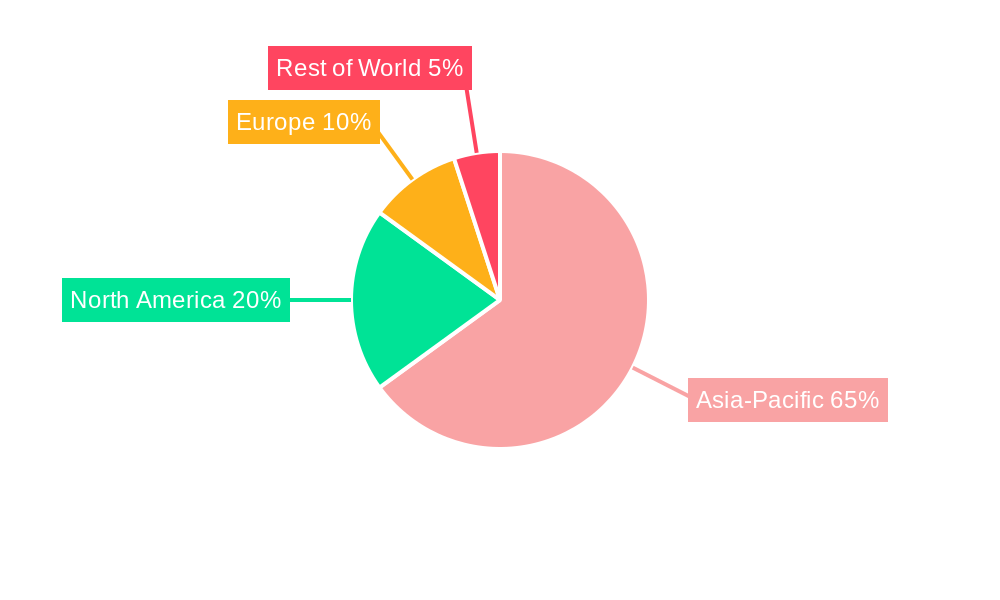

Asia-Pacific Private Equity Industry Regional Market Share

Geographic Coverage of Asia-Pacific Private Equity Industry

Asia-Pacific Private Equity Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of < 5.00% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Investment

- 5.1.1. Real Estate

- 5.1.2. Private Investment in Public Equity (PIPE)

- 5.1.3. Buyouts

- 5.1.4. Exits

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Investment

- 6. Asia-Pacific Private Equity Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Investment

- 6.1.1. Real Estate

- 6.1.2. Private Investment in Public Equity (PIPE)

- 6.1.3. Buyouts

- 6.1.4. Exits

- 6.1. Market Analysis, Insights and Forecast - by Investment

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Carlyle

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Blackstone

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 The Everstone Group

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 KKR

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Nippon Sangyo Suishin Kiko Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Bain Capital

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Warburg Pincus

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 J-Star

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Ascent Capital

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 CVC Capital Partners**List Not Exhaustive

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Carlyle

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Asia-Pacific Private Equity Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Asia-Pacific Private Equity Industry Share (%) by Company 2025

List of Tables

- Table 1: Asia-Pacific Private Equity Industry Revenue Million Forecast, by Investment 2020 & 2033

- Table 2: Asia-Pacific Private Equity Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Asia-Pacific Private Equity Industry Revenue Million Forecast, by Investment 2020 & 2033

- Table 4: Asia-Pacific Private Equity Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 5: China Asia-Pacific Private Equity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 6: Japan Asia-Pacific Private Equity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 7: South Korea Asia-Pacific Private Equity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: India Asia-Pacific Private Equity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Australia Asia-Pacific Private Equity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: New Zealand Asia-Pacific Private Equity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Indonesia Asia-Pacific Private Equity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Malaysia Asia-Pacific Private Equity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Singapore Asia-Pacific Private Equity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Thailand Asia-Pacific Private Equity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Vietnam Asia-Pacific Private Equity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Philippines Asia-Pacific Private Equity Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia-Pacific Private Equity Industry?

The projected CAGR is approximately < 5.00%.

2. Which companies are prominent players in the Asia-Pacific Private Equity Industry?

Key companies in the market include Carlyle, Blackstone, The Everstone Group, KKR, Nippon Sangyo Suishin Kiko Ltd, Bain Capital, Warburg Pincus, J-Star, Ascent Capital, CVC Capital Partners**List Not Exhaustive.

3. What are the main segments of the Asia-Pacific Private Equity Industry?

The market segments include Investment.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Deals Made a Remarkable Rebound in Asia-Pacific Private Equity Market.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

September 2022: The Asian Development Bank (ADB) signed a USD 15 million equity investment in KV Asia Capital Fund II LP, a private equity fund managed by KV Asia to provide growth capital to companies in the health care, financial services, education, manufacturing, business services, and consumer sectors across Southeast Asia.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia-Pacific Private Equity Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia-Pacific Private Equity Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia-Pacific Private Equity Industry?

To stay informed about further developments, trends, and reports in the Asia-Pacific Private Equity Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence