Key Insights

Algeria's Oil and Gas Upstream Industry is projected for robust growth, fueled by sustained demand and strategic project development. The market is anticipated to reach $43.17 billion by 2023, demonstrating a Compound Annual Growth Rate (CAGR) of 4.7% through 2033. This expansion is underpinned by Algeria's significant hydrocarbon reserves and government initiatives to boost exploration and production. Key growth drivers include the continued development of onshore projects and the potential for substantial offshore discoveries. The adoption of advanced technologies and strategic collaborations with international energy leaders are crucial for industry advancement. Sonatrach SPA plays a central role in coordinating these efforts and ensuring national energy security.

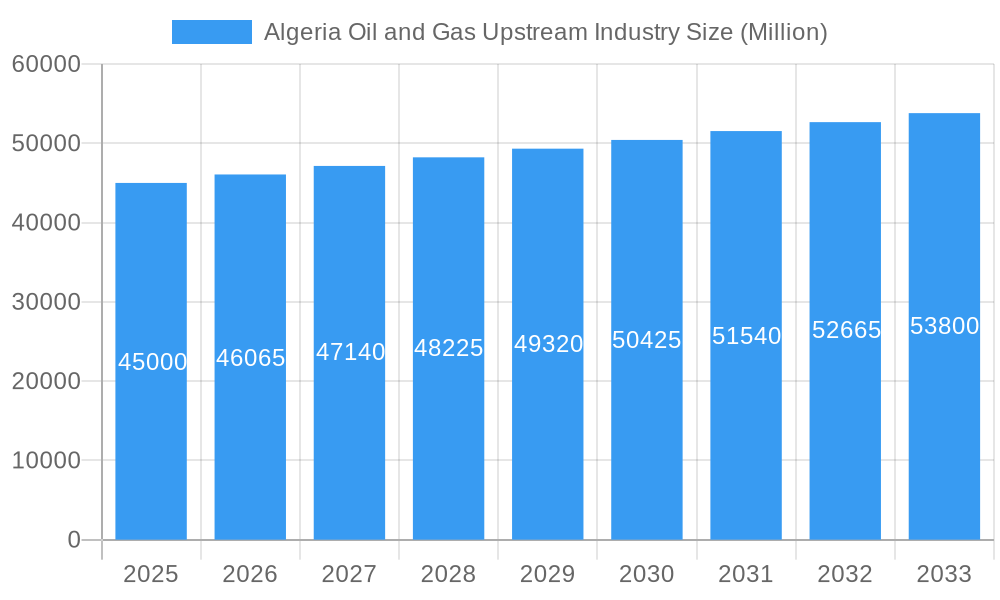

Algeria Oil and Gas Upstream Industry Market Size (In Billion)

While the industry shows positive growth, it encounters challenges such as the evolving global energy landscape, necessitating a shift towards sustainable practices and diversification. High capital expenditure and operational complexities in offshore exploration present hurdles. Nevertheless, Algeria's vast natural gas reserves offer significant opportunities, supporting domestic energy needs and increasing exports to European markets. The market is segmented by location, with a strong focus on onshore activities and growing interest in offshore exploration. The industry's dynamic landscape is shaped by a blend of national and international stakeholders, underscoring its economic importance to Algeria.

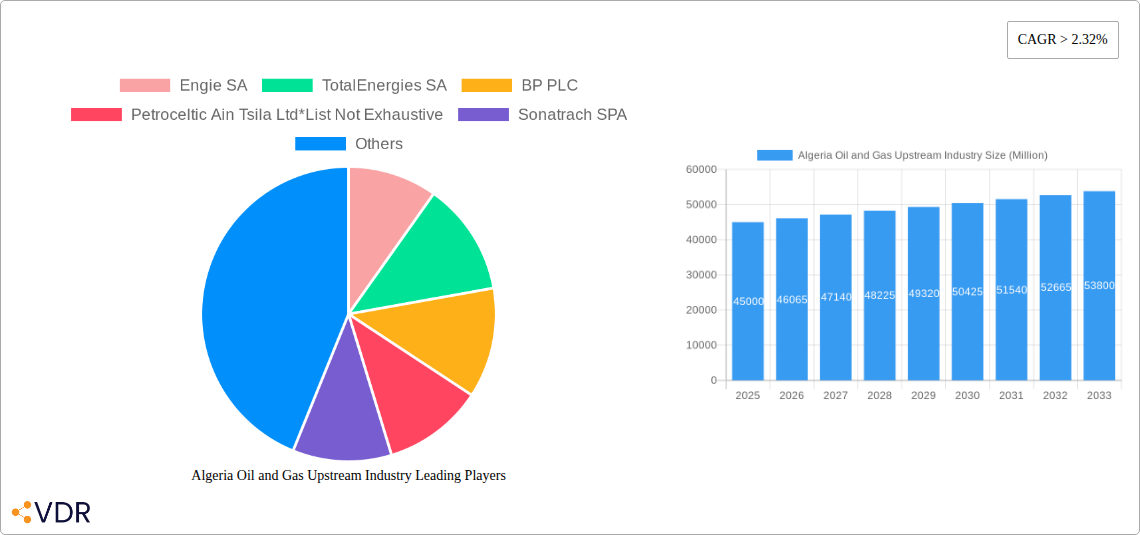

Algeria Oil and Gas Upstream Industry Company Market Share

Algeria Oil and Gas Upstream Industry Market Dynamics & Structure

The Algerian oil and gas upstream industry is characterized by a moderate market concentration, with state-owned Sonatrach SPA holding a dominant position. However, international oil companies (IOCs) like TotalEnergies SA, BP PLC, and Engie SA play significant roles through joint ventures and production sharing agreements, contributing to a dynamic competitive landscape. Technological innovation is a key driver, particularly in enhancing extraction efficiency from mature fields and exploring new frontiers. Regulatory frameworks, overseen by the Ministry of Energy and Mines, are crucial in shaping investment attractiveness and production sharing, with recent reforms aimed at attracting foreign direct investment. While direct competitive product substitutes for crude oil and natural gas are limited in the short to medium term, the increasing global focus on renewable energy sources presents a long-term strategic challenge. End-user demographics are primarily driven by global energy demand and Algeria's export capabilities. Mergers and acquisitions (M&A) trends are influenced by evolving energy policies and asset valuations. In the historical period (2019-2024), several strategic partnerships have been forged, and asset divestments have occurred, reflecting a continuous restructuring of market players. For instance, Eni SpA's planned acquisition of BP's upstream assets in Algeria signifies a strategic consolidation aimed at expanding operational footprint.

- Market Concentration: Dominated by Sonatrach SPA, with significant participation from IOCs.

- Technological Innovation: Focus on enhanced oil recovery (EOR) techniques and exploration technologies.

- Regulatory Frameworks: Evolving policies designed to attract foreign investment and modernize the sector.

- Competitive Product Substitutes: Long-term threat from renewable energy sources.

- M&A Trends: Driven by strategic consolidation and portfolio optimization.

Algeria Oil and Gas Upstream Industry Growth Trends & Insights

The Algerian oil and gas upstream industry is poised for substantial growth, driven by its significant hydrocarbon reserves and strategic location. The market size is expected to witness a considerable evolution throughout the study period (2019-2033), with the base year 2025 serving as a critical reference point for future projections. The adoption rates of advanced exploration and production (E&P) technologies are on the rise, fueled by the need to maximize recovery from existing fields and to tap into previously inaccessible reserves. Technological disruptions, such as the implementation of digital E&P solutions and advanced seismic imaging, are enhancing operational efficiency and reducing discovery costs. Consumer behavior shifts, while less direct in the upstream sector, are indirectly influencing the industry through global demand patterns for energy commodities and the increasing emphasis on cleaner energy alternatives. For the forecast period (2025-2033), a projected Compound Annual Growth Rate (CAGR) of approximately 3.5% is anticipated, underscoring the sector's robust expansion. Market penetration of enhanced oil recovery techniques is steadily increasing, contributing to sustained production levels.

The industry's resilience is further bolstered by ongoing exploration activities and the development of new discoveries. For example, the substantial oil and accompanying gas discovery in the Zemlet el Arbi concession, announced in March 2022, with an estimated 140 million barrels of oil in place, is a significant indicator of the untapped potential within Algeria. This discovery, a joint venture between Eni and Sonatrach, highlights the collaborative approach that will likely characterize future growth. Furthermore, the planned acquisition of gas-producing concessions in Amenas and Salah by Eni SpA from BP's upstream business in Algeria, scheduled for September 2022, signals a strategic realignment and potential for optimized production. These developments are crucial for maintaining Algeria's position as a key energy supplier. The shift towards more efficient extraction methods and the exploration of deeper offshore reserves are also critical components of the industry's growth trajectory. The estimated market size for the Algerian oil and gas upstream sector is projected to reach approximately $35,000 million by 2033, a testament to its enduring importance in the global energy landscape.

Dominant Regions, Countries, or Segments in Algeria Oil and Gas Upstream Industry

The Onshore segment is unequivocally the dominant region driving growth within the Algerian oil and gas upstream industry. This dominance is a direct consequence of the country's vast proven reserves, established infrastructure, and extensive exploration history within its terrestrial territories. The overview of onshore operations reveals a multifaceted landscape comprising existing projects, projects in the pipeline, and upcoming projects, all contributing to sustained production and future potential.

- Existing Projects: These form the backbone of current Algerian oil and gas output. Regions like the Ghadames Basin and the Berkine Basin are mature but remain highly productive due to continuous optimization and the application of advanced recovery techniques. These projects benefit from decades of operational experience and established logistical networks, ensuring consistent revenue streams.

- Projects in Pipeline: Several significant projects are currently in various stages of development within the onshore sector. These often involve expanding existing fields or developing newly discovered reserves. For instance, the recent substantial oil and gas discovery in the Zemlet el Arbi concession, located in the Berkine North Basin, exemplifies the ongoing exploration success onshore. This discovery, with preliminary assessments of 140 million barrels of oil in place, represents a considerable addition to Algeria's reserves and is expected to contribute significantly to future production.

- Upcoming Projects: The Algerian government and its national oil company, Sonatrach, are actively pursuing new exploration bids and development plans for onshore blocks. These initiatives are designed to sustain production levels beyond current horizons and to leverage emerging technologies for deeper and more complex geological formations. The commitment to onshore development is further evidenced by strategic partnerships with international players aiming to bring new technologies and capital into these ventures.

The economic policies of Algeria strongly favor the continued exploitation of its onshore hydrocarbon resources. Significant government investment in infrastructure, including pipelines, processing facilities, and transportation networks, underpins the efficiency and profitability of onshore operations. Furthermore, the geological characteristics of many onshore fields, while mature, still offer considerable potential for incremental production through enhanced oil recovery (EOR) methods. Market share within the onshore segment is heavily influenced by the production volumes of major concessions, where Sonatrach maintains a commanding presence, often in partnership with international energy giants. The growth potential remains substantial, as evidenced by recent discoveries and the ongoing drive to modernize exploration and production techniques. The onshore segment is projected to account for over 85% of Algeria's total upstream production during the forecast period, solidifying its position as the primary engine of growth for the nation's oil and gas sector. The exploration and production of unconventional resources within onshore territories also represent a significant, albeit less developed, area of future growth potential.

Algeria Oil and Gas Upstream Industry Product Landscape

The Algerian oil and gas upstream industry primarily focuses on the extraction and initial processing of crude oil and natural gas. The core products are light to medium crude oil with varying API gravities and natural gas, including associated gas. Innovations in this sector are geared towards optimizing the recovery of these commodities from both conventional and unconventional reservoirs. This includes the adoption of advanced seismic imaging for more precise subsurface mapping, the implementation of artificial lift systems to enhance production from mature wells, and the utilization of digital technologies for real-time monitoring and control of extraction processes. Performance metrics are largely measured by production volumes, extraction efficiency, and the cost of production per barrel of oil equivalent (BOE). Unique selling propositions for Algerian upstream operations lie in its significant reserve base and strategic export capabilities to European markets. Technological advancements are continuously being integrated to improve operational safety and environmental stewardship.

Key Drivers, Barriers & Challenges in Algeria Oil and Gas Upstream Industry

Key Drivers:

- Vast Hydrocarbon Reserves: Algeria possesses substantial proven reserves of crude oil and natural gas, providing a strong foundation for continued upstream activity.

- Global Energy Demand: Persistent global demand for oil and gas, particularly from European markets, ensures a consistent market for Algerian production.

- Government Support and Investment: The Algerian government actively promotes the oil and gas sector through favorable policies and direct investment via Sonatrach.

- Strategic Location: Proximity to major energy-consuming markets in Europe offers significant logistical advantages for exports.

- Technological Advancements: The adoption of new exploration and production technologies enhances recovery rates and efficiency.

Barriers & Challenges:

- Infrastructure Limitations: While improving, certain areas may face challenges with outdated or insufficient infrastructure, impacting exploration and transportation.

- Regulatory Hurdles: Complex bureaucratic processes and evolving fiscal regimes can pose challenges for international investors.

- Security Concerns: Geopolitical instability in the wider region can create perceived or actual security risks, deterring investment.

- Aging Fields and Declining Production: Many existing fields are mature, requiring significant investment in EOR to maintain production levels.

- Competition from Renewable Energy: The global shift towards cleaner energy sources presents a long-term challenge to fossil fuel demand.

- Financing Challenges: Securing adequate funding for large-scale upstream projects can be a barrier, especially for smaller entities.

- Skilled Workforce Development: Ensuring a sufficient supply of skilled labor for complex upstream operations is an ongoing challenge.

Emerging Opportunities in Algeria Oil and Gas Upstream Industry

Emerging opportunities in the Algerian oil and gas upstream industry lie in the untapped potential of its deeper offshore blocks and the exploration of unconventional resources, such as shale gas. The development of advanced technological solutions for subsea exploration and production presents a significant growth avenue. Furthermore, the increasing global emphasis on gas as a transition fuel to renewables creates a sustained demand for Algerian natural gas exports. Opportunities also exist in enhancing the efficiency of existing onshore fields through digital transformation and the application of artificial intelligence for predictive maintenance and optimized production. Collaborations with international technology providers to develop and implement cutting-edge extraction techniques will be crucial for unlocking these opportunities. The monetization of associated gas, which is often flared, represents another area for value creation and emission reduction.

Growth Accelerators in the Algeria Oil and Gas Upstream Industry Industry

Several catalysts are propelling long-term growth in the Algerian oil and gas upstream industry. Technological breakthroughs in seismic data interpretation, directional drilling, and enhanced oil recovery (EOR) are crucial for maximizing hydrocarbon extraction from existing and new reserves. The strategic partnerships between Sonatrach and major international oil companies (IOCs) are vital, as they bring in essential capital, advanced expertise, and access to global markets. These collaborations facilitate the development of complex projects that might otherwise be unattainable. Market expansion strategies, particularly those focused on diversifying export destinations and securing long-term supply agreements with European and African nations, are also key accelerators. Furthermore, the government's commitment to a more attractive investment climate through regulatory reforms and the offering of new exploration blocks is directly fostering growth. Investment in human capital development, ensuring a skilled workforce, also plays a critical role in sustaining the industry's momentum.

Key Players Shaping the Algeria Oil and Gas Upstream Industry Market

- Sonatrach SPA

- Engie SA

- TotalEnergies SA

- BP PLC

- Petroceltic Ain Tsila Ltd*List Not Exhaustive

- Eni SpA

Notable Milestones in Algeria Oil and Gas Upstream Industry Sector

- March 2022: Eni and Sonatrach announced a substantial oil and accompanying gas discovery in the Zemlet el Arbi concession in the Algerian desert's Berkine North Basin. This concession is being operated in a joint venture with Sonatrach (51%), Eni (49%), and other parties. According to preliminary assessments of the extent of the discovery, there may be 140 million barrels of oil in place.

- September 2022: The gas-producing concessions in Amenas and Salah, which produced a combined 11 billion cubic meters of gas and 12 million barrels each of condensate and LPG in 2021, will be acquired by Eni SpA from BP's upstream business in Algeria.

In-Depth Algeria Oil and Gas Upstream Industry Market Outlook

The outlook for the Algeria oil and gas upstream industry remains robust, driven by sustained global energy demand and the nation's significant hydrocarbon endowment. Growth accelerators such as advancements in extraction technologies, strategic international partnerships, and government initiatives to attract investment will continue to propel the sector forward. The onshore segment is projected to remain the primary contributor to production, with ongoing exploration and development of existing and newly discovered fields. Opportunities in the offshore sector, though requiring higher capital investment and advanced technology, also present substantial long-term potential. The industry's ability to adapt to evolving energy landscapes, including the transition to cleaner fuels, will be critical for its sustained relevance. Strategic investments in digitalization, enhanced oil recovery, and the efficient monetization of natural gas will shape the future market, ensuring Algeria's continued role as a key global energy supplier. The market is anticipated to experience a consistent upward trajectory, supported by a favorable investment climate and the inherent value of its energy resources.

Algeria Oil and Gas Upstream Industry Segmentation

-

1. Location

-

1.1. Onshore

-

1.1.1. Overview

- 1.1.1.1. Existing Projects

- 1.1.1.2. Projects in Pipeline

- 1.1.1.3. Upcoming Projects

-

1.1.1. Overview

- 1.2. Offshore

-

1.1. Onshore

Algeria Oil and Gas Upstream Industry Segmentation By Geography

- 1. Algeria

Algeria Oil and Gas Upstream Industry Regional Market Share

Geographic Coverage of Algeria Oil and Gas Upstream Industry

Algeria Oil and Gas Upstream Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Location

- 5.1.1. Onshore

- 5.1.1.1. Overview

- 5.1.1.1.1. Existing Projects

- 5.1.1.1.2. Projects in Pipeline

- 5.1.1.1.3. Upcoming Projects

- 5.1.1.1. Overview

- 5.1.2. Offshore

- 5.1.1. Onshore

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Algeria

- 5.1. Market Analysis, Insights and Forecast - by Location

- 6. Algeria Oil and Gas Upstream Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Location

- 6.1.1. Onshore

- 6.1.1.1. Overview

- 6.1.1.1.1. Existing Projects

- 6.1.1.1.2. Projects in Pipeline

- 6.1.1.1.3. Upcoming Projects

- 6.1.1.1. Overview

- 6.1.2. Offshore

- 6.1.1. Onshore

- 6.1. Market Analysis, Insights and Forecast - by Location

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Engie SA

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 TotalEnergies SA

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 BP PLC

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Petroceltic Ain Tsila Ltd*List Not Exhaustive

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Sonatrach SPA

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.1 Engie SA

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Algeria Oil and Gas Upstream Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Algeria Oil and Gas Upstream Industry Share (%) by Company 2025

List of Tables

- Table 1: Algeria Oil and Gas Upstream Industry Revenue billion Forecast, by Location 2020 & 2033

- Table 2: Algeria Oil and Gas Upstream Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Algeria Oil and Gas Upstream Industry Revenue billion Forecast, by Location 2020 & 2033

- Table 4: Algeria Oil and Gas Upstream Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Algeria Oil and Gas Upstream Industry?

The projected CAGR is approximately 4.7%.

2. Which companies are prominent players in the Algeria Oil and Gas Upstream Industry?

Key companies in the market include Engie SA, TotalEnergies SA, BP PLC, Petroceltic Ain Tsila Ltd*List Not Exhaustive, Sonatrach SPA.

3. What are the main segments of the Algeria Oil and Gas Upstream Industry?

The market segments include Location .

4. Can you provide details about the market size?

The market size is estimated to be USD 43.17 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Demand for Clean Energy Sources4.; Supportive Government Policies.

6. What are the notable trends driving market growth?

Onshore Gas Field Production to Witness Growth.

7. Are there any restraints impacting market growth?

4.; Increasing Adoption of Other Alternative Clean Energy Sources.

8. Can you provide examples of recent developments in the market?

In March 2022, Eni and Sonatrach announced a substantial oil and accompanying gas discovery in the Zemlet el Arbi concession in the Algerian desert's Berkine North Basin. This concession is being operated in a joint venture with Sonatrach (51%), Eni (49%), and other parties. According to preliminary assessments of the extent of the discovery, there may be 140 million barrels of oil in place.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Algeria Oil and Gas Upstream Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Algeria Oil and Gas Upstream Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Algeria Oil and Gas Upstream Industry?

To stay informed about further developments, trends, and reports in the Algeria Oil and Gas Upstream Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence