Key Insights

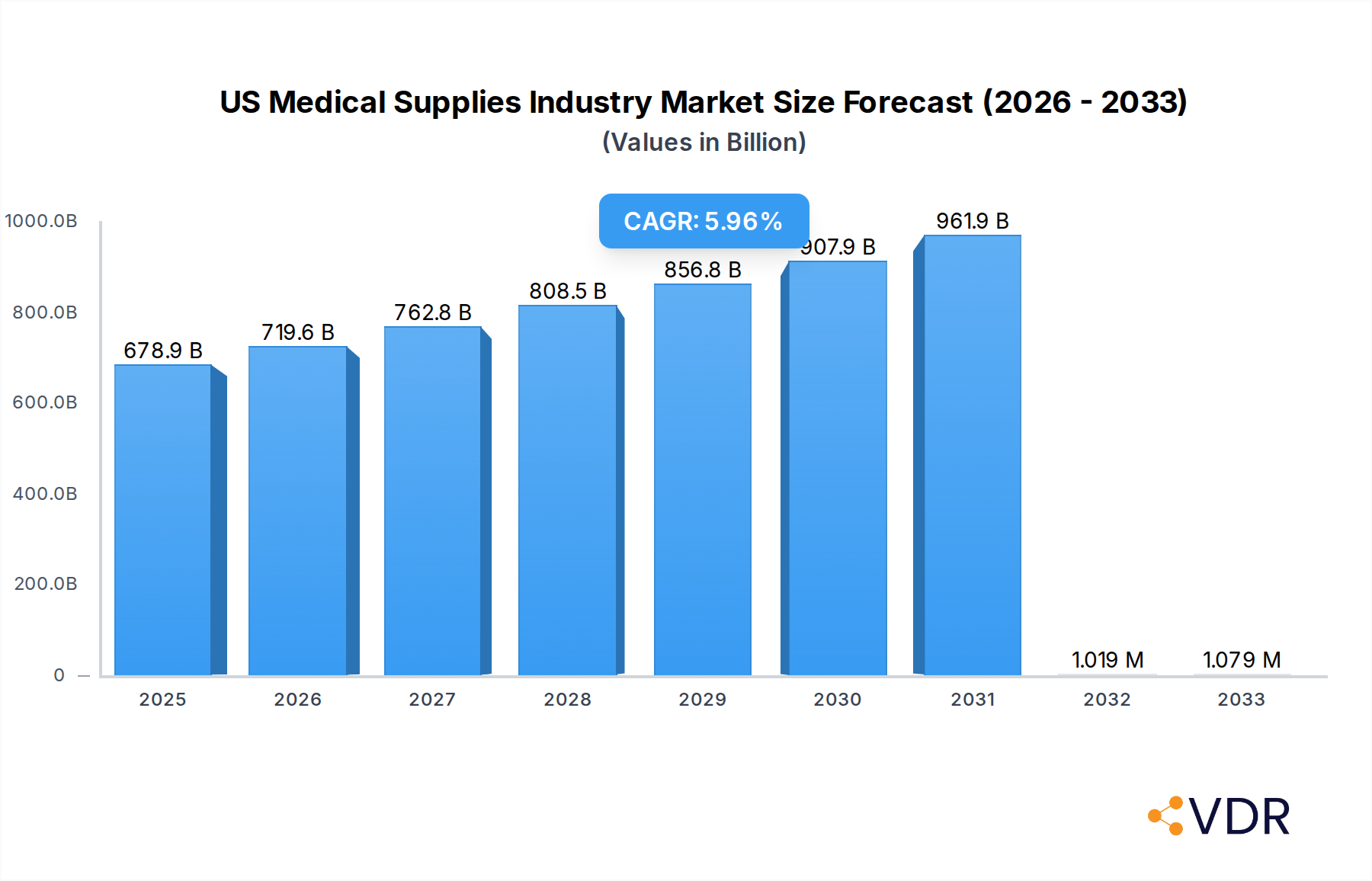

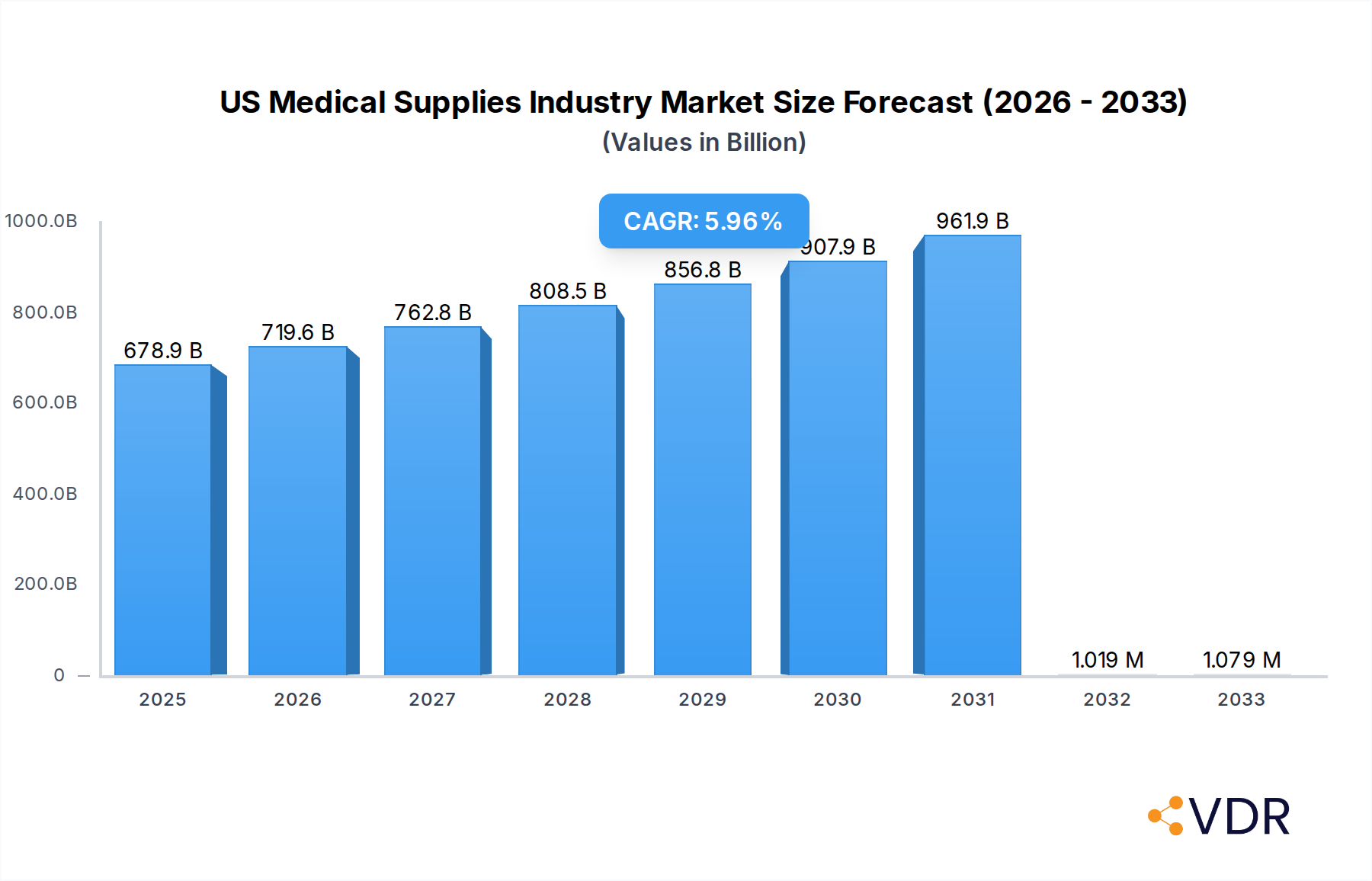

The US medical supplies market is poised for significant growth, projected to reach USD 678.88 billion by 2025. This expansion is fueled by a consistent CAGR of 6% over the forecast period. Several key drivers are propelling this upward trajectory, including the increasing prevalence of chronic diseases, an aging global population demanding more healthcare services, and continuous advancements in medical technology that necessitate updated and sophisticated supplies. The demand for sterile and single-use products, driven by enhanced infection control protocols, is particularly robust. Furthermore, government initiatives aimed at improving healthcare access and infrastructure contribute to market expansion. The integration of digital health solutions and smart medical devices is also creating new avenues for growth, as these technologies often require specialized and complementary medical supplies.

US Medical Supplies Industry Market Size (In Billion)

The market is segmented into several critical categories, with Patient Examination Devices and Disposable Hospital Supplies expected to be major contributors. Operating Room Equipment and Sterilization and Disinfectant Equipment are also experiencing sustained demand due to the continuous need for advanced surgical procedures and stringent hygiene standards. Mobility Aids and Transportation Equipment are witnessing growth driven by an aging demographic and increased focus on patient comfort and rehabilitation. The competitive landscape is dominated by major players such as Becton Dickinson and Company, Thermo Fisher Scientific Inc, and Cardinal Health Inc, who are actively engaged in product innovation, strategic collaborations, and mergers and acquisitions to maintain and expand their market share. The industry is characterized by a strong emphasis on regulatory compliance and product quality to ensure patient safety and efficacy.

US Medical Supplies Industry Company Market Share

US Medical Supplies Industry: Comprehensive Market Analysis and Future Outlook (2019-2033)

Unlock critical insights into the dynamic US medical supplies market with this in-depth report. Covering a comprehensive study period from 2019 to 2033, with a base and estimated year of 2025, this analysis delves into market dynamics, growth trends, product landscape, key players, and emerging opportunities. Essential for industry professionals, investors, and stakeholders seeking to navigate the competitive US medical supplies sector, this report provides actionable intelligence on market size evolution, technological disruptions, regulatory frameworks, and competitive strategies. Featuring quantitative market data and qualitative analysis, this report offers a definitive roadmap for strategic decision-making.

US Medical Supplies Industry Market Dynamics & Structure

The US medical supplies industry is characterized by a moderately concentrated market, with a few major players holding significant market share, but also a robust presence of specialized and niche manufacturers. Technological innovation is a paramount driver, fueled by advancements in materials science, miniaturization, and digital integration, leading to the development of more effective and patient-centric medical devices. Stringent regulatory frameworks, overseen by bodies like the FDA, play a crucial role in ensuring product safety and efficacy, albeit sometimes posing as innovation barriers. The competitive landscape is shaped by the constant threat of product substitutes, particularly as new technologies emerge and existing ones become more accessible. End-user demographics, including an aging population and an increasing prevalence of chronic diseases, create a consistently high demand for medical supplies. Mergers and acquisitions (M&A) trends are prevalent as larger companies seek to expand their product portfolios, gain access to new technologies, and consolidate market presence. In 2023, there were approximately 85 significant M&A deals within the broader healthcare sector, with a notable portion impacting medical supplies.

- Market Concentration: Dominated by key players like Becton Dickinson and Company, Thermo Fisher Scientific Inc., Cardinal Health Inc., 3M Company, Medtronic PLC, GE Healthcare, Johnson & Johnson, B Braun Melsungen AG, Boston Scientific Corporation, and Baxter International Inc.

- Technological Innovation Drivers: Miniaturization, AI integration, biocompatible materials, remote patient monitoring technologies.

- Regulatory Frameworks: FDA approval processes, stringent quality control standards, evolving reimbursement policies.

- Competitive Product Substitutes: Advancements in minimally invasive surgical techniques reducing the need for certain traditional supplies, growth of telehealth impacting the demand for some in-home diagnostic devices.

- End-User Demographics: Aging population (driving demand for mobility aids, chronic care supplies), rise in elective surgeries, increasing healthcare access.

- M&A Trends: Strategic acquisitions for portfolio expansion, technology integration, and market share consolidation.

US Medical Supplies Industry Growth Trends & Insights

The US medical supplies industry is poised for robust growth, projected to expand significantly in market size over the forecast period. This expansion is driven by a confluence of factors including an increasing healthcare expenditure, a growing and aging population demanding more medical interventions, and a continuous influx of technological advancements. The adoption rates for innovative medical supplies, particularly those enhancing patient outcomes and operational efficiency for healthcare providers, are steadily rising. Technological disruptions, such as the integration of artificial intelligence in diagnostic devices and the development of advanced biomaterials for implants and disposables, are reshaping the market landscape. Consumer behavior shifts are also playing a crucial role, with a greater emphasis on preventative care, home healthcare solutions, and personalized medicine, influencing the demand for specific product categories. The market size is estimated to reach $450 billion units by 2025, with a projected Compound Annual Growth Rate (CAGR) of 6.5% from 2025 to 2033. Market penetration of advanced surgical equipment is expected to reach 78% by 2030, while the adoption of smart diagnostic devices will likely exceed 60% within the same timeframe. The demand for disposable hospital supplies is projected to maintain a steady growth of 5.2% annually, driven by infection control protocols and the sheer volume of patient care. The burgeoning field of personalized medicine is also expected to spur demand for specialized diagnostic and delivery systems, contributing an additional 3% to the overall market growth.

Dominant Regions, Countries, or Segments in US Medical Supplies Industry

The Disposable Hospital Supplies segment is identified as a dominant driver of growth within the US medical supplies industry. This segment's prominence is attributed to its fundamental role in virtually every healthcare setting, from routine patient care to complex surgical procedures. The continuous need for sterile, single-use items to prevent healthcare-associated infections (HAIS) ensures a consistent and high-volume demand. Key drivers fueling the dominance of disposable hospital supplies include stringent infection control protocols mandated by regulatory bodies, a growing number of hospital admissions, and the expanding scope of outpatient surgical centers. Economic policies that support healthcare infrastructure development and increase access to medical services further bolster this segment's growth. Market share within this segment is significant, estimated to be 25% of the total US medical supplies market by 2025. The growth potential remains substantial, driven by innovations in material science leading to more sustainable and cost-effective disposable products, as well as the increasing adoption of advanced wound care and ostomy supplies.

- Patient Examination Devices: Contributing 12% to the market, driven by increased demand for diagnostic tools in primary care and home health.

- Operating Room Equipment: Holding 18% of the market, with strong growth fueled by advancements in surgical robotics and minimally invasive instrumentation.

- Mobility Aids and Transportation Equipment: Accounting for 10% of the market, primarily driven by the aging population and the rise of home healthcare.

- Sterilization and Disinfectant Equipment: Representing 8% of the market, with consistent demand linked to infection control mandates.

- Disposable Hospital Supplies: The leading segment at 25%, driven by infection prevention and high patient volumes.

- Syringes and Needles: Constituting 15% of the market, with steady demand from pharmaceutical administration and diagnostics.

- Other Products: The remaining 12%, encompassing a diverse range of specialized medical consumables.

US Medical Supplies Industry Product Landscape

The product landscape within the US medical supplies industry is characterized by relentless innovation and a focus on enhancing patient safety, improving clinical outcomes, and optimizing healthcare economics. Product innovations are consistently emerging, ranging from advanced wound care dressings that promote faster healing to sophisticated diagnostic tools that enable earlier and more accurate disease detection. Applications span across all healthcare settings, from hospitals and clinics to home healthcare and remote monitoring. Performance metrics are increasingly being scrutinized, with an emphasis on efficacy, durability, ease of use, and cost-effectiveness. Unique selling propositions often lie in proprietary technologies, superior material composition, and seamless integration with existing healthcare IT systems. Technological advancements, such as the development of antimicrobial coatings on surgical instruments and the creation of biodegradable medical plastics, are setting new industry standards.

Key Drivers, Barriers & Challenges in US Medical Supplies Industry

The US medical supplies industry is propelled by several key drivers. Technological advancements in medical device manufacturing, including automation and AI, are enhancing product capabilities and efficiency. An increasing prevalence of chronic diseases and an aging population are creating sustained demand for a wide range of medical supplies. Government initiatives promoting healthcare access and quality, along with favorable reimbursement policies for innovative medical technologies, also contribute significantly.

- Technological Advancements: Miniaturization, AI, advanced materials, connected devices.

- Demographic Shifts: Aging population, rising chronic disease rates.

- Healthcare Policy: Increased healthcare spending, focus on preventative care.

- Economic Factors: Growing disposable income for healthcare services.

However, the industry faces substantial barriers and challenges. Stringent and evolving regulatory approval processes can lead to lengthy product development timelines and increased costs. Supply chain vulnerabilities, highlighted by recent global disruptions, pose a significant risk to product availability and pricing. Intense competition from both established players and new entrants, coupled with the pressure for cost containment from payers, creates a challenging market environment.

- Regulatory Hurdles: FDA approval timelines, compliance costs.

- Supply Chain Disruptions: Geopolitical factors, raw material shortages.

- Pricing Pressure: Reimbursement challenges, payer negotiations.

- Intellectual Property Protection: Patent cliffs and generic competition.

Emerging Opportunities in US Medical Supplies Industry

Emerging opportunities in the US medical supplies industry are abundant, driven by the confluence of technological innovation and evolving healthcare needs. The rapid growth of telehealth and remote patient monitoring presents a significant avenue for companies offering connected medical devices and consumables that facilitate at-home diagnostics and treatment. The increasing demand for personalized medicine is creating a niche for highly specialized diagnostic kits, drug delivery systems, and customized implantable devices. Furthermore, the focus on sustainable healthcare practices is opening doors for manufacturers developing eco-friendly and biodegradable medical supplies, tapping into a growing market segment concerned with environmental impact. The untapped potential in underserved rural areas and emerging healthcare models, such as micro-hospitals and urgent care centers, also represents a considerable growth opportunity.

Growth Accelerators in the US Medical Supplies Industry Industry

Several catalysts are accelerating long-term growth in the US medical supplies industry. The relentless pace of technological breakthroughs, including the integration of artificial intelligence in diagnostic imaging and robotic surgery, is continuously expanding the utility and efficacy of medical supplies. Strategic partnerships between medical device manufacturers, pharmaceutical companies, and healthcare providers are fostering collaborative innovation and creating integrated solutions that address complex healthcare challenges. Market expansion strategies, such as targeting emerging healthcare markets within the US and developing tailored product offerings for specific patient populations, are also contributing significantly to sustained growth. The increasing investment in research and development by both established corporations and venture-backed startups is ensuring a steady pipeline of novel products and technologies.

Key Players Shaping the US Medical Supplies Industry Market

- Becton Dickinson and Company

- Thermo Fisher Scientific Inc.

- Cardinal Health Inc.

- 3M Company

- Medtronic PLC

- GE Healthcare

- Johnson & Johnson

- B Braun Melsungen AG

- Boston Scientific Corporation

- Baxter International Inc.

Notable Milestones in US Medical Supplies Industry Sector

- April 2022: GE Healthcare signed a partnership with Unilabs to provide MRI, CT Scan, ultrasound, mammography, and X-ray machines in Portugal.

- March 2022: Cardinal Health Inc. launched one of the first surgical incise drapes combined with chlorhexidine gluconate (CHG) to minimize the risk of onsite surgical contamination by gram-negative bacteria, offering a sturdy, breathable, and sterile surface.

In-Depth US Medical Supplies Industry Market Outlook

The future outlook for the US medical supplies industry is exceptionally bright, driven by sustained demand from a growing and aging population, coupled with the relentless pursuit of technological innovation. Growth accelerators such as AI-driven diagnostics, advanced biomaterials, and the expansion of personalized medicine will continue to redefine product offerings and clinical applications. Strategic partnerships and collaborative efforts will be pivotal in addressing complex healthcare needs and fostering integrated solutions. The industry is poised to capitalize on emerging opportunities in telehealth, remote patient monitoring, and sustainable healthcare practices, ensuring robust market expansion and continued value creation for stakeholders. The estimated market size is projected to reach $600 billion units by 2033, reflecting significant growth potential.

US Medical Supplies Industry Segmentation

-

1. Product

- 1.1. Patient Examination Devices

- 1.2. Operating Room Equipment

- 1.3. Mobility Aids and Transportation Equipment

- 1.4. Sterilization and Disinfectant Equipment

- 1.5. Disposable Hospital Supplies

- 1.6. Syringes and Needles

- 1.7. Other Products

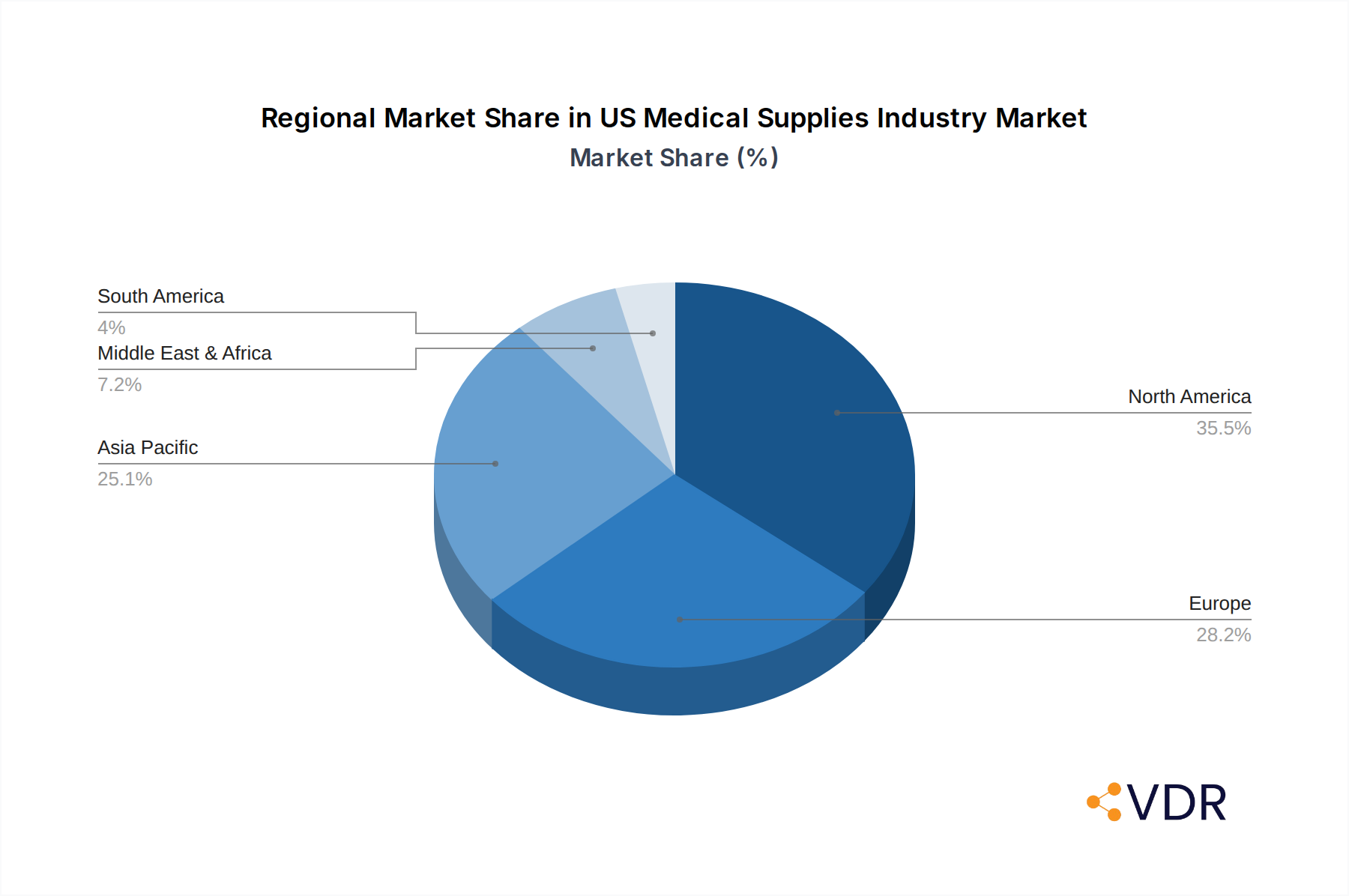

US Medical Supplies Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

US Medical Supplies Industry Regional Market Share

Geographic Coverage of US Medical Supplies Industry

US Medical Supplies Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Patient Examination Devices

- 5.1.2. Operating Room Equipment

- 5.1.3. Mobility Aids and Transportation Equipment

- 5.1.4. Sterilization and Disinfectant Equipment

- 5.1.5. Disposable Hospital Supplies

- 5.1.6. Syringes and Needles

- 5.1.7. Other Products

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. South America

- 5.2.3. Europe

- 5.2.4. Middle East & Africa

- 5.2.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. Global US Medical Supplies Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Patient Examination Devices

- 6.1.2. Operating Room Equipment

- 6.1.3. Mobility Aids and Transportation Equipment

- 6.1.4. Sterilization and Disinfectant Equipment

- 6.1.5. Disposable Hospital Supplies

- 6.1.6. Syringes and Needles

- 6.1.7. Other Products

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. North America US Medical Supplies Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Product

- 7.1.1. Patient Examination Devices

- 7.1.2. Operating Room Equipment

- 7.1.3. Mobility Aids and Transportation Equipment

- 7.1.4. Sterilization and Disinfectant Equipment

- 7.1.5. Disposable Hospital Supplies

- 7.1.6. Syringes and Needles

- 7.1.7. Other Products

- 7.1. Market Analysis, Insights and Forecast - by Product

- 8. South America US Medical Supplies Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Product

- 8.1.1. Patient Examination Devices

- 8.1.2. Operating Room Equipment

- 8.1.3. Mobility Aids and Transportation Equipment

- 8.1.4. Sterilization and Disinfectant Equipment

- 8.1.5. Disposable Hospital Supplies

- 8.1.6. Syringes and Needles

- 8.1.7. Other Products

- 8.1. Market Analysis, Insights and Forecast - by Product

- 9. Europe US Medical Supplies Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Product

- 9.1.1. Patient Examination Devices

- 9.1.2. Operating Room Equipment

- 9.1.3. Mobility Aids and Transportation Equipment

- 9.1.4. Sterilization and Disinfectant Equipment

- 9.1.5. Disposable Hospital Supplies

- 9.1.6. Syringes and Needles

- 9.1.7. Other Products

- 9.1. Market Analysis, Insights and Forecast - by Product

- 10. Middle East & Africa US Medical Supplies Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Product

- 10.1.1. Patient Examination Devices

- 10.1.2. Operating Room Equipment

- 10.1.3. Mobility Aids and Transportation Equipment

- 10.1.4. Sterilization and Disinfectant Equipment

- 10.1.5. Disposable Hospital Supplies

- 10.1.6. Syringes and Needles

- 10.1.7. Other Products

- 10.1. Market Analysis, Insights and Forecast - by Product

- 11. Asia Pacific US Medical Supplies Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Product

- 11.1.1. Patient Examination Devices

- 11.1.2. Operating Room Equipment

- 11.1.3. Mobility Aids and Transportation Equipment

- 11.1.4. Sterilization and Disinfectant Equipment

- 11.1.5. Disposable Hospital Supplies

- 11.1.6. Syringes and Needles

- 11.1.7. Other Products

- 11.1. Market Analysis, Insights and Forecast - by Product

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Becton Dickinson and Company

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Thermo Fisher Scientific Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Cardinal Health Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 3M Company

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Medtronic PLC

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 GE Healthcare

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Johnson & Johnson

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 B Braun Melsungen AG

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Boston Scientific Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Baxter International Inc

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Becton Dickinson and Company

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global US Medical Supplies Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America US Medical Supplies Industry Revenue (billion), by Product 2025 & 2033

- Figure 3: North America US Medical Supplies Industry Revenue Share (%), by Product 2025 & 2033

- Figure 4: North America US Medical Supplies Industry Revenue (billion), by Country 2025 & 2033

- Figure 5: North America US Medical Supplies Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: South America US Medical Supplies Industry Revenue (billion), by Product 2025 & 2033

- Figure 7: South America US Medical Supplies Industry Revenue Share (%), by Product 2025 & 2033

- Figure 8: South America US Medical Supplies Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: South America US Medical Supplies Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe US Medical Supplies Industry Revenue (billion), by Product 2025 & 2033

- Figure 11: Europe US Medical Supplies Industry Revenue Share (%), by Product 2025 & 2033

- Figure 12: Europe US Medical Supplies Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe US Medical Supplies Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Middle East & Africa US Medical Supplies Industry Revenue (billion), by Product 2025 & 2033

- Figure 15: Middle East & Africa US Medical Supplies Industry Revenue Share (%), by Product 2025 & 2033

- Figure 16: Middle East & Africa US Medical Supplies Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: Middle East & Africa US Medical Supplies Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific US Medical Supplies Industry Revenue (billion), by Product 2025 & 2033

- Figure 19: Asia Pacific US Medical Supplies Industry Revenue Share (%), by Product 2025 & 2033

- Figure 20: Asia Pacific US Medical Supplies Industry Revenue (billion), by Country 2025 & 2033

- Figure 21: Asia Pacific US Medical Supplies Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global US Medical Supplies Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 2: Global US Medical Supplies Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Global US Medical Supplies Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 4: Global US Medical Supplies Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 5: United States US Medical Supplies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 6: Canada US Medical Supplies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 7: Mexico US Medical Supplies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Global US Medical Supplies Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 9: Global US Medical Supplies Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Brazil US Medical Supplies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Argentina US Medical Supplies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Rest of South America US Medical Supplies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Global US Medical Supplies Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 14: Global US Medical Supplies Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 15: United Kingdom US Medical Supplies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Germany US Medical Supplies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: France US Medical Supplies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Italy US Medical Supplies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Spain US Medical Supplies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Russia US Medical Supplies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Benelux US Medical Supplies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Nordics US Medical Supplies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Rest of Europe US Medical Supplies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Global US Medical Supplies Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 25: Global US Medical Supplies Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 26: Turkey US Medical Supplies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Israel US Medical Supplies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: GCC US Medical Supplies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: North Africa US Medical Supplies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: South Africa US Medical Supplies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Rest of Middle East & Africa US Medical Supplies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Global US Medical Supplies Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 33: Global US Medical Supplies Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 34: China US Medical Supplies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: India US Medical Supplies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Japan US Medical Supplies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: South Korea US Medical Supplies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: ASEAN US Medical Supplies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: Oceania US Medical Supplies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Rest of Asia Pacific US Medical Supplies Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the US Medical Supplies Industry?

The projected CAGR is approximately 6%.

2. Which companies are prominent players in the US Medical Supplies Industry?

Key companies in the market include Becton Dickinson and Company, Thermo Fisher Scientific Inc, Cardinal Health Inc, 3M Company, Medtronic PLC, GE Healthcare, Johnson & Johnson, B Braun Melsungen AG, Boston Scientific Corporation, Baxter International Inc.

3. What are the main segments of the US Medical Supplies Industry?

The market segments include Product.

4. Can you provide details about the market size?

The market size is estimated to be USD 678.88 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Incidences of Communicable Diseases; Growing Public Awareness about Hospital Acquired Infections.

6. What are the notable trends driving market growth?

Disposable Hospital Supplies Segment is Expected to Witness Growth Over the Forecast Period.

7. Are there any restraints impacting market growth?

Stringent Regulatory Framework; Emergence of Home Care Services.

8. Can you provide examples of recent developments in the market?

April 2022: GE Healthcare signed a partnership with Unilabs. This partnership has been done in order to provide MRI, CT Scan, ultrasound, mammography, and X-ray machines in Portugal.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "US Medical Supplies Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the US Medical Supplies Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the US Medical Supplies Industry?

To stay informed about further developments, trends, and reports in the US Medical Supplies Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence