Key Insights

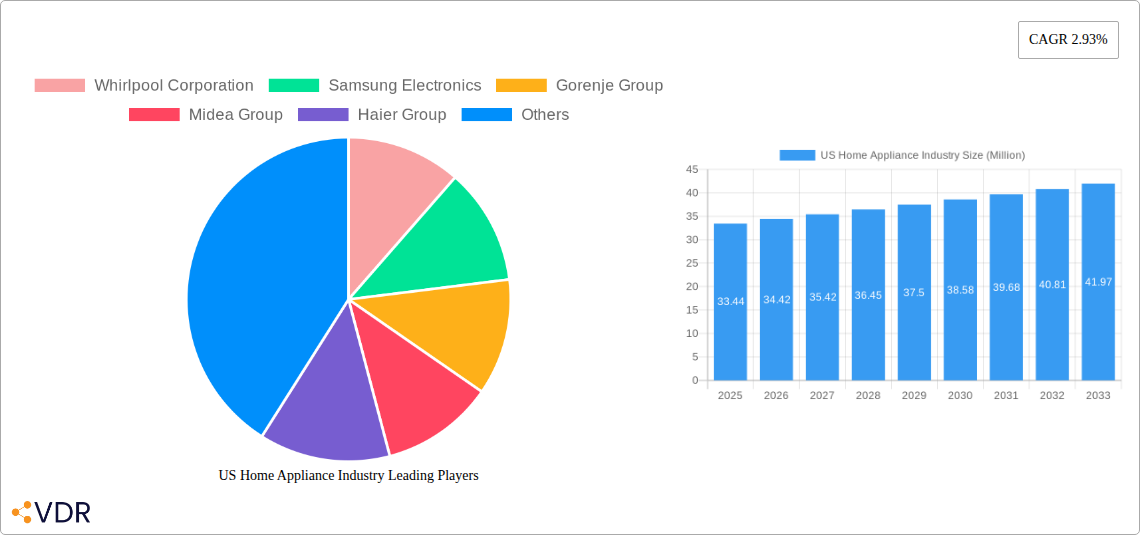

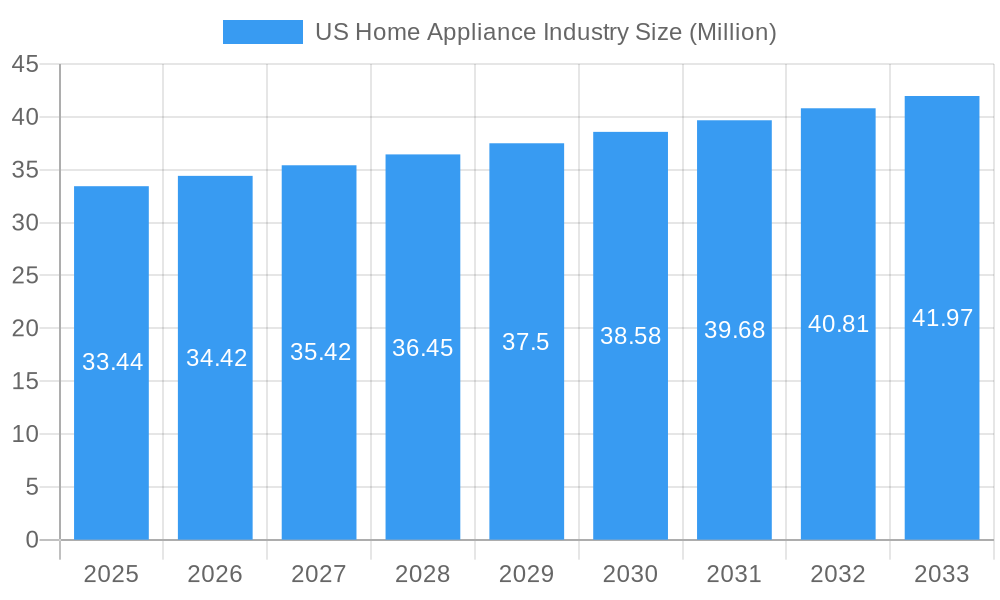

The US Home Appliance Industry is poised for steady growth, projected to reach approximately $33.44 million by 2025, with a Compound Annual Growth Rate (CAGR) of 2.93% expected to carry through the forecast period of 2025-2033. This sustained expansion is largely driven by evolving consumer preferences, technological advancements, and an increasing focus on energy efficiency and smart home integration. The demand for innovative kitchen appliances like advanced refrigerators with customizable cooling zones and multi-functional ovens continues to rise, mirroring a broader trend towards premiumization and enhanced user experience. Similarly, the market for energy-efficient washing machines and dishwashers is benefiting from heightened environmental awareness and potential utility cost savings. Air conditioners remain a consistent driver, particularly in regions experiencing warmer climates, with advancements focusing on superior cooling performance and reduced energy consumption.

US Home Appliance Industry Market Size (In Million)

Several key trends are shaping the competitive landscape. The proliferation of smart home ecosystems is pushing manufacturers to develop connected appliances that offer seamless integration and remote control capabilities, appealing to tech-savvy consumers. Furthermore, a growing emphasis on sustainability and eco-friendly products is influencing purchasing decisions, with consumers actively seeking appliances with high energy ratings and reduced environmental impact. Distribution channels are also evolving, with online sales platforms experiencing significant growth, offering consumers greater convenience and wider product selection. Exclusive brand outlets, however, continue to hold their ground by providing specialized customer service and brand experience. Despite this positive outlook, the industry faces certain restraints, including rising raw material costs which can impact profit margins and potentially lead to higher consumer prices. Supply chain disruptions, though easing, can still pose challenges to timely product delivery and inventory management.

US Home Appliance Industry Company Market Share

US Home Appliance Industry Market Dynamics & Structure

The US home appliance industry is characterized by a moderate to high level of market concentration, with a few global giants dominating a significant portion of market share. Key players such as Whirlpool Corporation, Samsung Electronics, LG Electronics, Haier Group, and Bosch are actively engaged in fierce competition, driving continuous innovation. Technological innovation is a primary driver, fueled by advancements in smart home integration, energy efficiency, and user convenience. The regulatory framework, including energy efficiency standards and environmental regulations, plays a crucial role in shaping product development and market access. Competitive product substitutes, while less common within core appliance categories, emerge in the form of multi-functional devices and increasingly integrated kitchen systems. End-user demographics, particularly the rising disposable income of the millennial and Gen Z populations, alongside an aging Baby Boomer demographic seeking ease of use, are influencing product design and marketing strategies. Mergers and acquisitions (M&A) trends are prevalent as companies seek to expand their product portfolios, gain market access, and leverage synergies.

- Market Concentration: Dominated by a few major players with substantial market share (e.g., Whirlpool Corporation holds approximately 20-25% market share in major appliances).

- Technological Innovation Drivers: Smart home connectivity, AI-powered features, enhanced energy efficiency (e.g., ENERGY STAR certifications), and sustainable materials.

- Regulatory Frameworks: Energy Policy and Conservation Act (EPCA) standards, Environmental Protection Agency (EPA) regulations on refrigerants.

- Competitive Product Substitutes: While direct substitutes are limited, integrated smart home ecosystems and multi-purpose countertop appliances present indirect competition.

- End-User Demographics: Growing demand for smart appliances among tech-savvy younger generations and the need for user-friendly, accessible appliances for the elderly.

- M&A Trends: Strategic acquisitions to enhance product offerings and market reach; for instance, Haier's acquisition of GE Appliances significantly boosted its US presence.

US Home Appliance Industry Growth Trends & Insights

The US home appliance industry is poised for sustained growth, projected to expand significantly throughout the forecast period. This expansion is driven by a confluence of factors, including a robust housing market, increasing consumer spending on home upgrades, and a growing preference for technologically advanced and energy-efficient appliances. The adoption rates for smart home appliances are accelerating, with consumers increasingly integrating connected devices into their living spaces for enhanced convenience and control. Technological disruptions are continually reshaping the market, with the introduction of AI-powered features, advanced sensor technologies, and innovative materials that enhance performance and durability. Consumer behavior shifts are also playing a pivotal role, with a growing emphasis on sustainability, personalized user experiences, and appliances that offer multi-functional capabilities. The market is witnessing a premiumization trend, where consumers are willing to invest more in high-quality, feature-rich appliances that offer long-term value and a superior user experience. The replacement cycle for older appliances, coupled with new home constructions, provides a steady demand stream. Furthermore, the increasing awareness of energy efficiency and its long-term cost savings is driving the adoption of ENERGY STAR certified products. The industry's ability to adapt to evolving consumer demands for convenience, connectivity, and sustainability will be key to unlocking its full growth potential.

- Market Size Evolution: The US home appliance market is projected to grow at a Compound Annual Growth Rate (CAGR) of approximately 4.5% from 2025 to 2033, reaching an estimated value of USD 150 billion by 2033.

- Adoption Rates: Smart appliance adoption is expected to reach over 60% of households by 2030, with a particular surge in smart refrigerators and washing machines.

- Technological Disruptions: The integration of voice control (e.g., Alexa, Google Assistant), advanced diagnostics for predictive maintenance, and induction cooking technology are transforming appliance functionality.

- Consumer Behavior Shifts: Increased demand for customizable appliance settings, eco-friendly product options, and appliances that simplify daily chores.

- Market Penetration: High penetration rates for core appliances like refrigerators and washing machines, with significant growth potential in niche categories like smart ovens and advanced dishwashers.

- Replacement Cycle: The average lifespan of major appliances ranges from 10-15 years, creating a consistent replacement market.

- Housing Market Influence: New home construction and renovation projects are significant drivers of appliance sales, contributing an estimated 25% of annual market growth.

Dominant Regions, Countries, or Segments in US Home Appliance Industry

The US home appliance industry exhibits distinct patterns of dominance across its product categories and distribution channels, each contributing uniquely to market growth. Refrigerators consistently hold the largest market share within the product segment, driven by essential household needs and continuous innovation in features like smart connectivity, advanced cooling technologies, and energy efficiency. The Refrigerators segment, in particular, is a significant growth engine, fueled by both replacement demand and new installations in a dynamic housing market. Its dominance is bolstered by technological advancements such as French door designs, internal water dispensers, and integrated touchscreens offering recipe suggestions and inventory management. The Online distribution channel has emerged as a formidable force, witnessing substantial growth due to its convenience, competitive pricing, and expansive product selection. E-commerce platforms provide consumers with a seamless shopping experience, from research to purchase, and have significantly influenced how appliances are bought and sold. The increasing prevalence of digital marketing and direct-to-consumer (DTC) models further solidifies online channels' ascendancy.

Dominant Product Segment: Refrigerators are the largest segment by revenue and unit sales, consistently driven by essential functionality and continuous feature innovation.

- Key Drivers: High replacement rates, new housing construction, demand for smart features (e.g., inventory tracking, recipe integration), and energy efficiency certifications (e.g., ENERGY STAR).

- Market Share: Refrigerators account for approximately 25-30% of the total US home appliance market.

- Growth Potential: Continued innovation in smart technology and premium designs will sustain strong growth.

Dominant Distribution Channel: Online channels are experiencing the most rapid growth, overtaking traditional retail in many segments.

- Key Drivers: Convenience, competitive pricing, wider product availability, ease of comparison, and the rise of e-commerce giants and DTC brands.

- Market Share: Online sales now represent over 35% of total home appliance sales and are projected to grow to over 50% by 2030.

- Growth Potential: Further expansion of same-day/next-day delivery services and immersive online product experiences will fuel continued dominance.

Other Significant Segments:

- Air-conditioners: Strong demand driven by climate conditions and energy efficiency improvements, accounting for approximately 15% of the market.

- Washing Machines: Steady demand from replacement cycles and new home installations, with innovations in steam technology and smart connectivity.

- Multi-Branded Stores: Remain a crucial channel for consumers seeking to physically compare products and receive expert advice, holding a significant share in overall sales.

US Home Appliance Industry Product Landscape

The US home appliance product landscape is characterized by rapid innovation focused on enhancing user experience, sustainability, and connectivity. Refrigerators are increasingly incorporating smart capabilities, such as AI-powered inventory management and personalized cooling zones, while also prioritizing energy efficiency to meet evolving consumer demands. Washing machines are witnessing advancements in drum design for superior cleaning performance and reduced water usage, alongside intelligent sensing technologies that optimize wash cycles. Air-conditioners are moving towards variable speed compressors and smart thermostat integration for optimized energy consumption and comfort control. Dishwashers are gaining features like advanced filtration systems and quieter operation, while ovens are embracing convection technology and smart cooking presets for precise culinary results. The overarching trend is the seamless integration of these appliances into the broader smart home ecosystem, offering consumers greater control and convenience.

Key Drivers, Barriers & Challenges in US Home Appliance Industry

Key Drivers:

- Technological Advancements: The integration of smart home technology, AI, and IoT is creating demand for connected and intelligent appliances, driving innovation and consumer interest.

- Economic Growth and Consumer Spending: A strong economy and rising disposable incomes encourage consumers to invest in new appliances and upgrades.

- Housing Market Dynamics: New home construction and renovation projects directly correlate with appliance sales, providing a consistent demand pipeline.

- Energy Efficiency Regulations and Consumer Awareness: Growing environmental consciousness and government mandates for energy efficiency encourage the purchase of newer, eco-friendly models.

Barriers & Challenges:

- Supply Chain Disruptions: Global supply chain volatility, including the availability of semiconductors and raw materials, can lead to production delays and increased costs.

- Rising Material Costs: Fluctuations in the prices of steel, aluminum, and plastics directly impact manufacturing expenses and can affect profit margins.

- Intense Competition and Price Sensitivity: The highly competitive nature of the market can lead to price wars, impacting profitability, especially for standard appliance models.

- Regulatory Hurdles: Evolving environmental and safety regulations require continuous product adaptation and compliance, incurring R&D and manufacturing costs.

- Skilled Labor Shortages: A lack of skilled labor in manufacturing and installation can pose challenges for companies seeking to scale production and operations.

Emerging Opportunities in US Home Appliance Industry

Emerging opportunities in the US home appliance industry lie in the continued expansion of the smart home ecosystem, offering consumers integrated and automated living experiences. The demand for sustainable and eco-friendly appliances presents a significant avenue for growth, with consumers increasingly seeking products that minimize their environmental footprint. Furthermore, the development of highly personalized appliance functionalities, catering to specific dietary needs, health concerns, or lifestyle preferences, offers a niche yet growing market. The aging population also presents an opportunity for the development of user-friendly, accessible appliances designed for ease of use and safety. Lastly, exploring subscription-based service models for appliance maintenance and upgrades could unlock new revenue streams and foster customer loyalty.

Growth Accelerators in the US Home Appliance Industry Industry

Several catalysts are accelerating growth in the US home appliance industry. Technological breakthroughs in AI and machine learning are enabling appliances to learn user preferences and proactively manage tasks, enhancing convenience. Strategic partnerships between appliance manufacturers and smart home technology providers are crucial for creating seamless integration and expanding product offerings. Market expansion strategies, including entering untapped segments like premium built-in appliances and focusing on direct-to-consumer (DTC) sales models, are further propelling growth. The increasing adoption of advanced materials, contributing to enhanced durability and energy efficiency, also plays a vital role in driving consumer adoption and market expansion.

Key Players Shaping the US Home Appliance Industry Market

- Whirlpool Corporation

- Samsung Electronics

- LG Electronics

- Haier Group

- Bosch

- Electrolux AB

- Panasonic Corporation

- Arcelik AS

- Gorenje Group

- Midea Group

Notable Milestones in US Home Appliance Industry Sector

- April 2023: Haier launched an innovative super drum washing machine with intelligent voice control, and the excellent drum ensures effective washing performance.

- November 2022: Lowe's, a retail company specializing in home improvement situated in America, expanded its assortment of premium appliances through a new partnership with Miele (a German manufacturer of high-end domestic appliances and commercial equipment). This partnership aimed to ensure new, high-quality offerings across all price points.

In-Depth US Home Appliance Industry Market Outlook

The US home appliance industry is on a robust growth trajectory, fueled by pervasive technological integration, a strong focus on sustainability, and evolving consumer expectations for convenience and personalization. Future market potential is immense, with smart home adoption continuing to be a primary driver, creating opportunities for interconnected appliance ecosystems. Strategic opportunities abound in developing appliances with advanced AI capabilities for predictive maintenance and energy optimization, alongside a continued emphasis on eco-friendly materials and manufacturing processes. The industry's ability to innovate and adapt to these evolving consumer preferences will be paramount in capitalizing on the substantial growth opportunities in the coming years.

US Home Appliance Industry Segmentation

-

1. Product

- 1.1. Refrigerators

- 1.2. Freezers

- 1.3. Air-conditioners

- 1.4. Dishwashers

- 1.5. Washing Machines

- 1.6. Ovens

-

2. Distribution Channel

- 2.1. Multi-Branded Stores

- 2.2. Exclusive Brand Outlets

- 2.3. Online

US Home Appliance Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

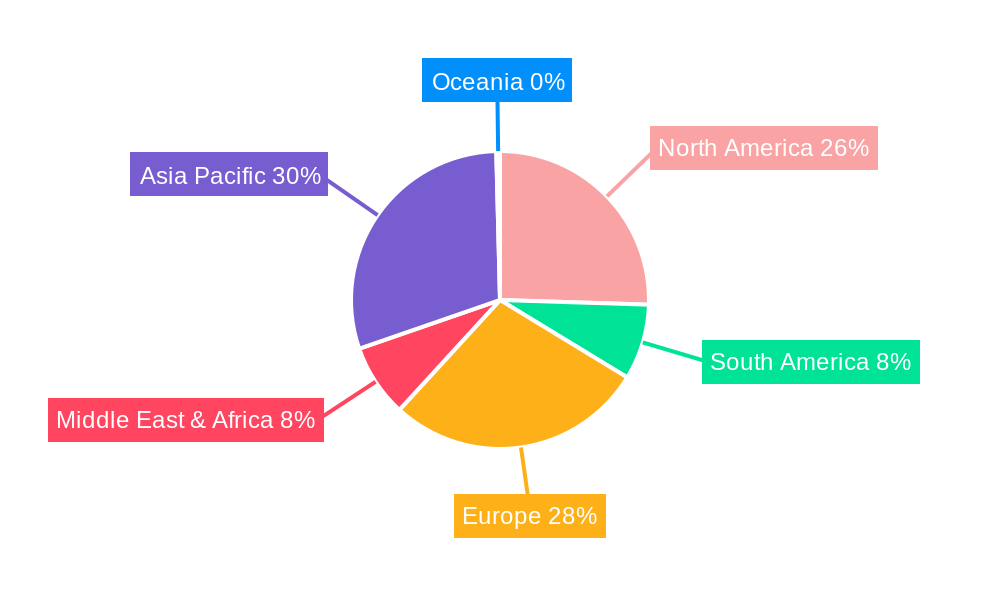

US Home Appliance Industry Regional Market Share

Geographic Coverage of US Home Appliance Industry

US Home Appliance Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.93% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Refrigerators

- 5.1.2. Freezers

- 5.1.3. Air-conditioners

- 5.1.4. Dishwashers

- 5.1.5. Washing Machines

- 5.1.6. Ovens

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Multi-Branded Stores

- 5.2.2. Exclusive Brand Outlets

- 5.2.3. Online

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. Global US Home Appliance Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Refrigerators

- 6.1.2. Freezers

- 6.1.3. Air-conditioners

- 6.1.4. Dishwashers

- 6.1.5. Washing Machines

- 6.1.6. Ovens

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Multi-Branded Stores

- 6.2.2. Exclusive Brand Outlets

- 6.2.3. Online

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. North America US Home Appliance Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Product

- 7.1.1. Refrigerators

- 7.1.2. Freezers

- 7.1.3. Air-conditioners

- 7.1.4. Dishwashers

- 7.1.5. Washing Machines

- 7.1.6. Ovens

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. Multi-Branded Stores

- 7.2.2. Exclusive Brand Outlets

- 7.2.3. Online

- 7.1. Market Analysis, Insights and Forecast - by Product

- 8. South America US Home Appliance Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Product

- 8.1.1. Refrigerators

- 8.1.2. Freezers

- 8.1.3. Air-conditioners

- 8.1.4. Dishwashers

- 8.1.5. Washing Machines

- 8.1.6. Ovens

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. Multi-Branded Stores

- 8.2.2. Exclusive Brand Outlets

- 8.2.3. Online

- 8.1. Market Analysis, Insights and Forecast - by Product

- 9. Europe US Home Appliance Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Product

- 9.1.1. Refrigerators

- 9.1.2. Freezers

- 9.1.3. Air-conditioners

- 9.1.4. Dishwashers

- 9.1.5. Washing Machines

- 9.1.6. Ovens

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. Multi-Branded Stores

- 9.2.2. Exclusive Brand Outlets

- 9.2.3. Online

- 9.1. Market Analysis, Insights and Forecast - by Product

- 10. Middle East & Africa US Home Appliance Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Product

- 10.1.1. Refrigerators

- 10.1.2. Freezers

- 10.1.3. Air-conditioners

- 10.1.4. Dishwashers

- 10.1.5. Washing Machines

- 10.1.6. Ovens

- 10.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.2.1. Multi-Branded Stores

- 10.2.2. Exclusive Brand Outlets

- 10.2.3. Online

- 10.1. Market Analysis, Insights and Forecast - by Product

- 11. Asia Pacific US Home Appliance Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Product

- 11.1.1. Refrigerators

- 11.1.2. Freezers

- 11.1.3. Air-conditioners

- 11.1.4. Dishwashers

- 11.1.5. Washing Machines

- 11.1.6. Ovens

- 11.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.2.1. Multi-Branded Stores

- 11.2.2. Exclusive Brand Outlets

- 11.2.3. Online

- 11.1. Market Analysis, Insights and Forecast - by Product

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Whirlpool Corporation

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Samsung Electronics

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Gorenje Group

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Midea Group

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Haier Group

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Bosch

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Arcelik AS**List Not Exhaustive

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Electrolux AB

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Panasonic Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 LG Electronics

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Whirlpool Corporation

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global US Home Appliance Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America US Home Appliance Industry Revenue (Million), by Product 2025 & 2033

- Figure 3: North America US Home Appliance Industry Revenue Share (%), by Product 2025 & 2033

- Figure 4: North America US Home Appliance Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 5: North America US Home Appliance Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 6: North America US Home Appliance Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America US Home Appliance Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America US Home Appliance Industry Revenue (Million), by Product 2025 & 2033

- Figure 9: South America US Home Appliance Industry Revenue Share (%), by Product 2025 & 2033

- Figure 10: South America US Home Appliance Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 11: South America US Home Appliance Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 12: South America US Home Appliance Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: South America US Home Appliance Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe US Home Appliance Industry Revenue (Million), by Product 2025 & 2033

- Figure 15: Europe US Home Appliance Industry Revenue Share (%), by Product 2025 & 2033

- Figure 16: Europe US Home Appliance Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 17: Europe US Home Appliance Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 18: Europe US Home Appliance Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Europe US Home Appliance Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa US Home Appliance Industry Revenue (Million), by Product 2025 & 2033

- Figure 21: Middle East & Africa US Home Appliance Industry Revenue Share (%), by Product 2025 & 2033

- Figure 22: Middle East & Africa US Home Appliance Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 23: Middle East & Africa US Home Appliance Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 24: Middle East & Africa US Home Appliance Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Middle East & Africa US Home Appliance Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific US Home Appliance Industry Revenue (Million), by Product 2025 & 2033

- Figure 27: Asia Pacific US Home Appliance Industry Revenue Share (%), by Product 2025 & 2033

- Figure 28: Asia Pacific US Home Appliance Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 29: Asia Pacific US Home Appliance Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 30: Asia Pacific US Home Appliance Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Asia Pacific US Home Appliance Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global US Home Appliance Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 2: Global US Home Appliance Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 3: Global US Home Appliance Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global US Home Appliance Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 5: Global US Home Appliance Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 6: Global US Home Appliance Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States US Home Appliance Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada US Home Appliance Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Mexico US Home Appliance Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Global US Home Appliance Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 11: Global US Home Appliance Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 12: Global US Home Appliance Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Brazil US Home Appliance Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Argentina US Home Appliance Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America US Home Appliance Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Global US Home Appliance Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 17: Global US Home Appliance Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 18: Global US Home Appliance Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom US Home Appliance Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Germany US Home Appliance Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: France US Home Appliance Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Italy US Home Appliance Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Spain US Home Appliance Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Russia US Home Appliance Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Benelux US Home Appliance Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Nordics US Home Appliance Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe US Home Appliance Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Global US Home Appliance Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 29: Global US Home Appliance Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 30: Global US Home Appliance Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 31: Turkey US Home Appliance Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Israel US Home Appliance Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: GCC US Home Appliance Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: North Africa US Home Appliance Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: South Africa US Home Appliance Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa US Home Appliance Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: Global US Home Appliance Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 38: Global US Home Appliance Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 39: Global US Home Appliance Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 40: China US Home Appliance Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 41: India US Home Appliance Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Japan US Home Appliance Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 43: South Korea US Home Appliance Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN US Home Appliance Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 45: Oceania US Home Appliance Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific US Home Appliance Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the US Home Appliance Industry?

The projected CAGR is approximately 2.93%.

2. Which companies are prominent players in the US Home Appliance Industry?

Key companies in the market include Whirlpool Corporation, Samsung Electronics, Gorenje Group, Midea Group, Haier Group, Bosch, Arcelik AS**List Not Exhaustive, Electrolux AB, Panasonic Corporation, LG Electronics.

3. What are the main segments of the US Home Appliance Industry?

The market segments include Product, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 33.44 Million as of 2022.

5. What are some drivers contributing to market growth?

Shifts in Consumer Preferences and Lifestyle Changes Drives the Market's Growth; Demand for Time Saving Solutions Drives the Market's Growth.

6. What are the notable trends driving market growth?

Increased Adoption of Multi and Advanced Products Driving the Market for Major Home Appliances.

7. Are there any restraints impacting market growth?

Supply Chain Disruptions; High Cost of Maintenance4.3.2.1; Market Oppurtunities4.; Technological Advancements in Major Home Appliances.

8. Can you provide examples of recent developments in the market?

April 2023: Haier launched an innovative super drum washing machine with intelligent voice control, and the excellent drum ensures effective washing performance.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "US Home Appliance Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the US Home Appliance Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the US Home Appliance Industry?

To stay informed about further developments, trends, and reports in the US Home Appliance Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence