Key Insights

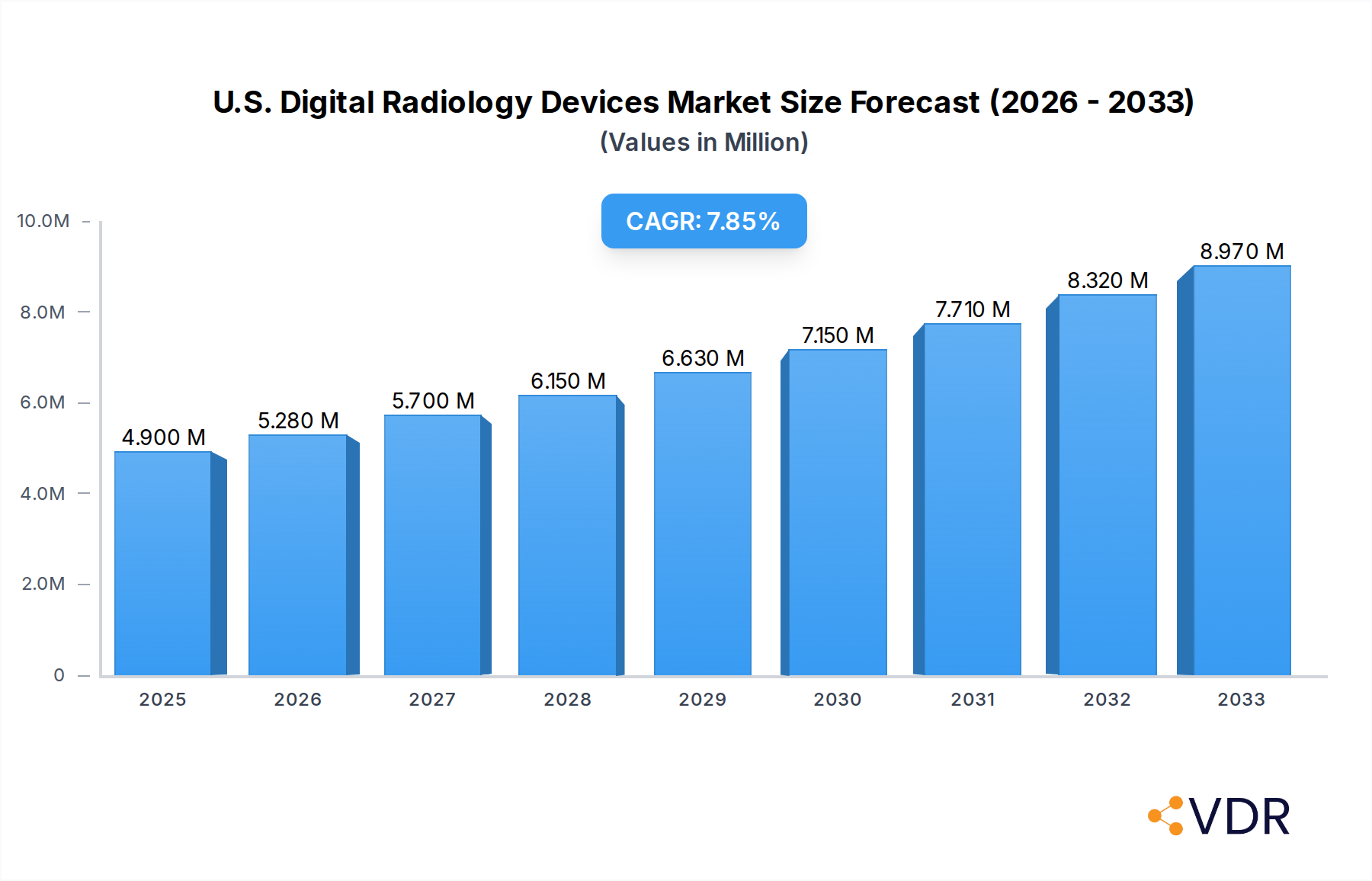

The U.S. Digital Radiology Devices Market is poised for significant expansion, projecting a market size of $4.90 million in 2025. This growth is fueled by an impressive CAGR of 7.79% over the forecast period of 2025-2033. Key drivers propelling this market include the escalating prevalence of chronic diseases such as orthopedic conditions, cancer, and cardiovascular ailments, all of which necessitate advanced diagnostic imaging solutions. The continuous technological advancements, particularly in areas like computed radiography and direct radiography, are enhancing image quality, reducing radiation exposure, and improving diagnostic accuracy. Furthermore, the increasing adoption of portable radiography systems is expanding access to critical imaging services, especially in remote areas and emergency situations, further bolstering market demand.

U.S. Digital Radiology Devices Market Market Size (In Million)

The U.S. Digital Radiology Devices Market is characterized by dynamic trends and strategic company activities. Innovations in detector technology and image processing software are leading to faster scan times and more detailed anatomical visualization, which are crucial for early and accurate disease detection. The growing emphasis on preventative healthcare and the subsequent rise in diagnostic procedures also contribute to market growth. While the market enjoys robust growth, certain restraints may emerge, such as the high initial investment costs for advanced digital radiology equipment and the need for skilled personnel to operate and maintain these sophisticated systems. However, the ongoing transition from traditional film-based radiography to digital systems, coupled with favorable reimbursement policies for diagnostic imaging services, continues to create substantial opportunities for market participants. The market segmentation reveals a strong demand across orthopedic, cancer, dental, and cardiovascular applications, with hospitals and diagnostic centers being the primary end-users.

U.S. Digital Radiology Devices Market Company Market Share

This comprehensive report offers an in-depth analysis of the U.S. Digital Radiology Devices Market, providing critical insights into market dynamics, growth trends, competitive landscape, and future opportunities. Spanning a study period from 2019 to 2033, with a base year of 2025, this report is an indispensable resource for industry stakeholders, investors, and decision-makers seeking to navigate the evolving U.S. digital radiography landscape. We meticulously examine key market segments, including Computed Radiography (CR) and Direct Radiography (DR) technologies, alongside application-specific segments like Orthopedic, Cancer, Dental, and Cardiovascular radiology. The analysis also delves into portability aspects, differentiating between Fixed Systems and Portable Systems, and scrutinizes end-user segments, including Hospitals, Diagnostic Centers, and Other End Users.

U.S. Digital Radiology Devices Market Market Dynamics & Structure

The U.S. Digital Radiology Devices Market is characterized by a moderately consolidated structure, with leading players holding significant market share. Technological innovation is the primary driver, propelled by advancements in detector technology, image processing algorithms, and AI integration for enhanced diagnostic accuracy and workflow efficiency. Stringent regulatory frameworks, including FDA approvals and adherence to medical device standards, shape product development and market entry. Competitive product substitutes, such as MRI and CT scanners, influence market penetration, though digital radiography remains a cost-effective and versatile imaging modality. End-user demographics, driven by an aging population and increasing prevalence of chronic diseases, further fuel demand. Mergers and acquisitions (M&A) activity is present, indicating strategic consolidation and a drive for market expansion.

- Market Concentration: Dominated by a mix of global conglomerates and specialized players, exhibiting moderate consolidation.

- Technological Innovation Drivers: AI-powered image analysis, enhanced detector sensitivity, portable and wireless solutions, and integrated PACS/RIS capabilities.

- Regulatory Frameworks: FDA clearance, HIPAA compliance, and adherence to quality management systems (e.g., ISO 13485).

- Competitive Product Substitutes: Advancements in Ultrasound, MRI, and CT imaging present indirect competition, necessitating continuous innovation in digital radiography.

- End-User Demographics: Growing demand from an aging population, increasing chronic disease burden, and expansion of outpatient diagnostic services.

- M&A Trends: Strategic acquisitions for technology integration, market access, and portfolio expansion are observed.

U.S. Digital Radiology Devices Market Growth Trends & Insights

The U.S. Digital Radiology Devices Market is poised for substantial growth, driven by an escalating demand for advanced diagnostic imaging solutions and the inherent advantages of digital radiography over traditional film-based systems. The transition from Computed Radiography (CR) to Direct Radiography (DR) continues to be a significant trend, offering superior image quality, reduced radiation dose, and faster examination times, thereby enhancing patient throughput and diagnostic confidence. The market size is projected to witness a healthy Compound Annual Growth Rate (CAGR) over the forecast period, reflecting increasing adoption rates across various healthcare settings. Technological disruptions, including the integration of Artificial Intelligence (AI) for automated image analysis, lesion detection, and workflow optimization, are revolutionizing diagnostic capabilities and contributing to improved patient outcomes. Shifts in consumer behavior, marked by a greater emphasis on preventive healthcare and early disease detection, further bolster the demand for advanced imaging technologies like digital radiography.

- Market Size Evolution: Expected to grow steadily, driven by increasing healthcare expenditure and the demand for sophisticated diagnostic tools.

- Adoption Rates: High adoption of DR systems is observed, gradually replacing older CR and film-based technologies.

- Technological Disruptions: AI integration, cloud-based image management, and advanced detector technologies are key disruptors.

- Consumer Behavior Shifts: Increased patient awareness regarding early disease detection and preference for minimally invasive diagnostic procedures.

- Market Penetration: Continued penetration into smaller clinics and specialized diagnostic centers, alongside established hospital systems.

- CAGR: Projected to be between 5-7% for the forecast period.

Dominant Regions, Countries, or Segments in U.S. Digital Radiology Devices Market

Within the U.S. Digital Radiology Devices Market, the Hospitals end-user segment stands out as a dominant force driving market growth. This dominance is attributed to several interconnected factors, including the substantial capital investment capabilities of hospitals, the sheer volume of diagnostic procedures performed, and the critical need for advanced imaging technologies to support a wide range of medical specialties. Hospitals are at the forefront of adopting new technologies to improve patient care, reduce examination times, and enhance diagnostic accuracy, making digital radiography an indispensable component of their radiology departments. The increasing prevalence of chronic diseases and an aging population directly translate to a higher demand for diagnostic imaging services within hospital settings.

Dominant End User: Hospitals:

- High Patient Volume: Hospitals perform the largest number of diagnostic imaging procedures, necessitating efficient and advanced radiology solutions.

- Technological Adoption Hubs: Hospitals are early adopters of cutting-edge technologies due to budget availability and a commitment to superior patient care.

- Comprehensive Service Offerings: The diverse range of medical specialties within hospitals drives demand for various digital radiography applications, from orthopedic imaging to cancer diagnosis.

- Reimbursement Policies: Favorable reimbursement policies for advanced diagnostic imaging services further encourage hospital investment.

- Infrastructure Development: Significant investment in radiology department upgrades and integration with hospital-wide IT systems.

- Market Share: Hospitals account for an estimated 60-65% of the U.S. Digital Radiology Devices Market.

Dominant Application: Orthopedic:

- Aging Population: The growing elderly demographic contributes to an increased incidence of orthopedic conditions like arthritis, fractures, and osteoporosis.

- Sports Medicine Growth: Rising participation in sports and recreational activities leads to a higher number of sports-related injuries requiring diagnostic imaging.

- Technological Advancements: Improved image clarity and detail in orthopedic imaging aids in precise diagnosis and treatment planning.

- Market Share: The orthopedic segment is estimated to hold approximately 25-30% of the total U.S. Digital Radiology Devices Market.

Dominant Technology: Direct Radiography (DR):

- Superior Image Quality: DR systems offer higher resolution and contrast compared to CR, leading to more accurate diagnoses.

- Faster Workflow: Instantaneous image acquisition and display significantly reduce patient scan times and increase departmental throughput.

- Reduced Radiation Dose: DR technology often allows for lower radiation doses while maintaining image quality, benefiting patient safety.

- Market Share: DR systems are projected to command over 70-75% of the digital radiography market by 2025.

U.S. Digital Radiology Devices Market Product Landscape

The U.S. Digital Radiology Devices Market is characterized by a dynamic product landscape featuring continuous innovation. Manufacturers are focusing on developing high-resolution detectors, advanced image processing software, and integrated solutions that enhance diagnostic accuracy and workflow efficiency. Products range from fixed radiography systems for dedicated imaging rooms to highly portable units designed for bedside examinations and use in emergency settings. Unique selling propositions often revolve around dose reduction technologies, AI-powered image enhancement and analysis, and seamless integration with Picture Archiving and Communication Systems (PACS) and Radiology Information Systems (RIS). The trend towards digital radiography continues to drive the phase-out of older film-based systems.

Key Drivers, Barriers & Challenges in U.S. Digital Radiology Devices Market

Key Drivers: The U.S. Digital Radiology Devices Market is propelled by several key drivers. The increasing prevalence of chronic diseases and an aging population necessitate advanced diagnostic imaging solutions. Technological advancements, particularly in detector technology, AI integration for image analysis, and the development of portable and wireless systems, are crucial. Favorable reimbursement policies for digital radiography procedures also play a significant role. Furthermore, the shift from traditional film-based radiography to digital systems offers improved workflow efficiency, reduced radiation doses, and enhanced image quality, driving adoption.

Key Barriers & Challenges: Despite the positive growth trajectory, the market faces several challenges. The high initial cost of digital radiography systems can be a barrier, especially for smaller healthcare facilities and diagnostic centers. Stringent regulatory requirements and the need for continuous compliance add to development and market entry costs. Competition from other advanced imaging modalities like MRI and CT also presents a challenge. Supply chain disruptions, global component shortages, and the need for skilled personnel to operate and maintain sophisticated equipment can also impact market growth.

Emerging Opportunities in U.S. Digital Radiology Devices Market

Emerging opportunities in the U.S. Digital Radiology Devices Market lie in the expansion of portable and point-of-care imaging solutions, particularly for remote and underserved areas, as well as for in-home patient monitoring. The increasing integration of AI for predictive diagnostics and personalized treatment planning presents a significant growth avenue. Furthermore, the development of hybrid imaging systems that combine different modalities for enhanced diagnostic capabilities, such as the FUJIFILM FDR Cross, offers untapped potential. The growing demand for teleradiology services, amplified by the need for efficient healthcare delivery and specialist access, also creates opportunities for advanced digital radiography solutions.

Growth Accelerators in the U.S. Digital Radiology Devices Market Industry

Several factors are accelerating growth within the U.S. Digital Radiology Devices Market. Technological breakthroughs in detector sensitivity and image processing continue to enhance diagnostic accuracy and workflow. Strategic partnerships and collaborations between device manufacturers and software companies are fostering the development of integrated AI-powered solutions. The increasing investment in healthcare infrastructure, particularly in outpatient diagnostic centers and ambulatory surgery centers (ASCs), is driving demand for flexible and efficient digital radiography systems. Furthermore, market expansion strategies focused on product diversification and catering to niche applications are contributing to sustained growth.

Key Players Shaping the U.S. Digital Radiology Devices Market Market

- Konica Minolta Inc

- Varex Imaging Corporation

- Toshiba Corporation

- Siemens Healthineers

- MinXray Inc

- Hologic Inc

- Hitachi Ltd

- Koninklinje Philips NV (Philips Healthcare)

- KUB Technologies Inc

- Carestream Health

- General Electric Company (GE Healthcare)

- Canon Medical Systems Corporation

- Agfa-Gevaert NV

- Shimadzu Corporation

- Fujifilm Holdings Corporation

- Samsung Electronics Co Ltd (Samsung Medison)

Notable Milestones in U.S. Digital Radiology Devices Market Sector

- April 2022: Boston Imaging introduces the GM85 Fit, a new configuration of the premium AccE GM85 digital radiography device, emphasizing user-centric design for efficient patient care.

- July 2022: FUJIFILM Healthcare Americas Corporation announces the U.S. launch of the FDR Cross, an innovative hybrid c-arm and portable x-ray solution designed for hospitals and ambulatory surgery centers (ASCs).

In-Depth U.S. Digital Radiology Devices Market Market Outlook

The U.S. Digital Radiology Devices Market is set for robust expansion, driven by ongoing technological advancements and increasing healthcare demand. The strategic integration of AI for enhanced diagnostic capabilities and workflow optimization represents a significant future market potential. Opportunities abound in the development of more compact, portable, and user-friendly digital radiography systems that can cater to diverse clinical settings, including remote patient care and point-of-care diagnostics. Furthermore, the continued evolution of hybrid imaging solutions and cloud-based platforms will unlock new avenues for market growth. Strategic collaborations and a focus on value-based healthcare solutions will be crucial for sustained success in this dynamic market.

U.S. Digital Radiology Devices Market Segmentation

-

1. Application

- 1.1. Orthopedic

- 1.2. Cancer

- 1.3. Dental

- 1.4. Cardiovascular

- 1.5. Other Applications

-

2. Technology

- 2.1. Computed Radiography

- 2.2. Direct Radiography

-

3. Portability

- 3.1. Fixed Systems

- 3.2. Portable Systems

-

4. End User

- 4.1. Hospitals

- 4.2. Diagnostic Centers

- 4.3. Other End Users

U.S. Digital Radiology Devices Market Segmentation By Geography

- 1. U.S.

U.S. Digital Radiology Devices Market Regional Market Share

Geographic Coverage of U.S. Digital Radiology Devices Market

U.S. Digital Radiology Devices Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.79% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Orthopedic

- 5.1.2. Cancer

- 5.1.3. Dental

- 5.1.4. Cardiovascular

- 5.1.5. Other Applications

- 5.2. Market Analysis, Insights and Forecast - by Technology

- 5.2.1. Computed Radiography

- 5.2.2. Direct Radiography

- 5.3. Market Analysis, Insights and Forecast - by Portability

- 5.3.1. Fixed Systems

- 5.3.2. Portable Systems

- 5.4. Market Analysis, Insights and Forecast - by End User

- 5.4.1. Hospitals

- 5.4.2. Diagnostic Centers

- 5.4.3. Other End Users

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. U.S.

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. U.S. Digital Radiology Devices Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Orthopedic

- 6.1.2. Cancer

- 6.1.3. Dental

- 6.1.4. Cardiovascular

- 6.1.5. Other Applications

- 6.2. Market Analysis, Insights and Forecast - by Technology

- 6.2.1. Computed Radiography

- 6.2.2. Direct Radiography

- 6.3. Market Analysis, Insights and Forecast - by Portability

- 6.3.1. Fixed Systems

- 6.3.2. Portable Systems

- 6.4. Market Analysis, Insights and Forecast - by End User

- 6.4.1. Hospitals

- 6.4.2. Diagnostic Centers

- 6.4.3. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Konica Minolta Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Varex Imaging Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Toshiba Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Siemens Healthineers

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 MinXray Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Hologic Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Hitachi Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Koninklinje Philips NV (Philips Healthcare)

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 KUB Technologies Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Carestream Health

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 General Electric Company (GE Healthcare)

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Canon Medical Systems Corporation

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Agfa-Gevaert NV

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Shimadzu Corporation

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 Fujifilm Holdings Corporation

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.16 Samsung Electronics Co Ltd (Samsung Medison)

- 7.1.16.1. Company Overview

- 7.1.16.2. Products

- 7.1.16.3. Company Financials

- 7.1.16.4. SWOT Analysis

- 7.1.1 Konica Minolta Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: U.S. Digital Radiology Devices Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: U.S. Digital Radiology Devices Market Share (%) by Company 2025

List of Tables

- Table 1: U.S. Digital Radiology Devices Market Revenue Million Forecast, by Application 2020 & 2033

- Table 2: U.S. Digital Radiology Devices Market Volume K Unit Forecast, by Application 2020 & 2033

- Table 3: U.S. Digital Radiology Devices Market Revenue Million Forecast, by Technology 2020 & 2033

- Table 4: U.S. Digital Radiology Devices Market Volume K Unit Forecast, by Technology 2020 & 2033

- Table 5: U.S. Digital Radiology Devices Market Revenue Million Forecast, by Portability 2020 & 2033

- Table 6: U.S. Digital Radiology Devices Market Volume K Unit Forecast, by Portability 2020 & 2033

- Table 7: U.S. Digital Radiology Devices Market Revenue Million Forecast, by End User 2020 & 2033

- Table 8: U.S. Digital Radiology Devices Market Volume K Unit Forecast, by End User 2020 & 2033

- Table 9: U.S. Digital Radiology Devices Market Revenue Million Forecast, by Region 2020 & 2033

- Table 10: U.S. Digital Radiology Devices Market Volume K Unit Forecast, by Region 2020 & 2033

- Table 11: U.S. Digital Radiology Devices Market Revenue Million Forecast, by Application 2020 & 2033

- Table 12: U.S. Digital Radiology Devices Market Volume K Unit Forecast, by Application 2020 & 2033

- Table 13: U.S. Digital Radiology Devices Market Revenue Million Forecast, by Technology 2020 & 2033

- Table 14: U.S. Digital Radiology Devices Market Volume K Unit Forecast, by Technology 2020 & 2033

- Table 15: U.S. Digital Radiology Devices Market Revenue Million Forecast, by Portability 2020 & 2033

- Table 16: U.S. Digital Radiology Devices Market Volume K Unit Forecast, by Portability 2020 & 2033

- Table 17: U.S. Digital Radiology Devices Market Revenue Million Forecast, by End User 2020 & 2033

- Table 18: U.S. Digital Radiology Devices Market Volume K Unit Forecast, by End User 2020 & 2033

- Table 19: U.S. Digital Radiology Devices Market Revenue Million Forecast, by Country 2020 & 2033

- Table 20: U.S. Digital Radiology Devices Market Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the U.S. Digital Radiology Devices Market?

The projected CAGR is approximately 7.79%.

2. Which companies are prominent players in the U.S. Digital Radiology Devices Market?

Key companies in the market include Konica Minolta Inc, Varex Imaging Corporation, Toshiba Corporation, Siemens Healthineers, MinXray Inc, Hologic Inc, Hitachi Ltd, Koninklinje Philips NV (Philips Healthcare), KUB Technologies Inc, Carestream Health, General Electric Company (GE Healthcare), Canon Medical Systems Corporation, Agfa-Gevaert NV, Shimadzu Corporation, Fujifilm Holdings Corporation, Samsung Electronics Co Ltd (Samsung Medison).

3. What are the main segments of the U.S. Digital Radiology Devices Market?

The market segments include Application, Technology, Portability, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 4.90 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Occurrence Levels of Orthopedic Diseases and Cancers; Increasing Number of Serious Injuries; Technological Advancements and Advantages of Digital X-ray Systems Over Conventional X-rays.

6. What are the notable trends driving market growth?

The Direct Radiography Segment is Expected to Witness a High CAGR Over the Forecast Period.

7. Are there any restraints impacting market growth?

High Initial Cost of Installation; New Sales Affected by the Increasing Use of Refurbished Devices.

8. Can you provide examples of recent developments in the market?

In April 2022, Boston Imaging, the United States headquarters of Samsung digital radiography and ultrasound systems, introduces the GM85 Fit, a new configuration of the premium AccE GM85; a digital radiography device featuring a user-centric design that aids in efficient and effective patient care.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "U.S. Digital Radiology Devices Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the U.S. Digital Radiology Devices Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the U.S. Digital Radiology Devices Market?

To stay informed about further developments, trends, and reports in the U.S. Digital Radiology Devices Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence