Key Insights

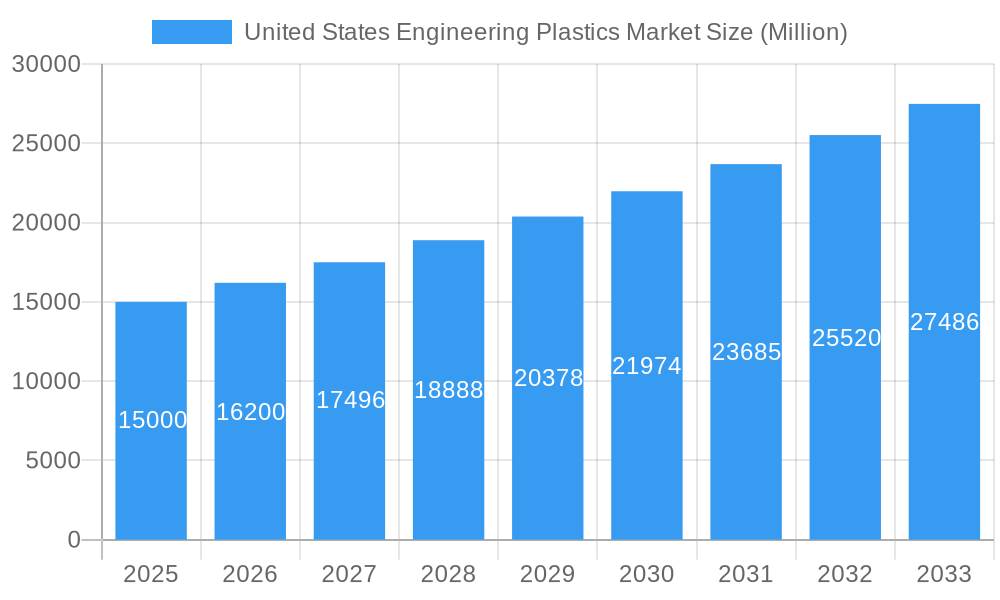

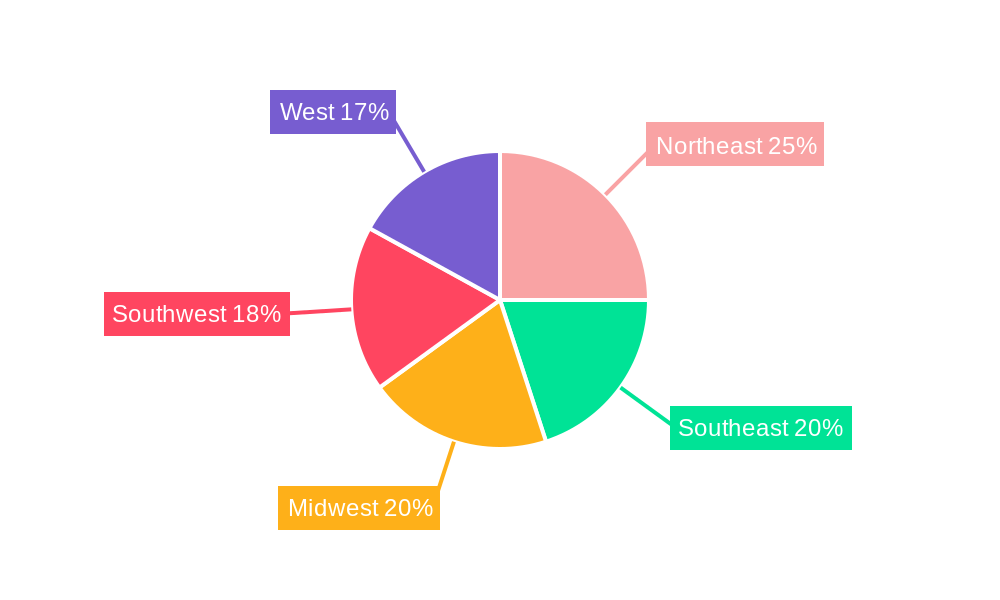

The United States engineering plastics market is projected for substantial growth, fueled by increasing demand across various sectors. With a projected Compound Annual Growth Rate (CAGR) of 6.28%, the market, valued at 15.8 billion in the base year 2025, is expected to expand significantly. Key growth drivers include the burgeoning automotive and aerospace industries, the adoption of lightweighting solutions for enhanced fuel efficiency and performance, and the rising demand for robust, high-performance materials in electrical and electronics applications. The robust construction sector, particularly in infrastructure and commercial projects, also contributes significantly to market expansion. High-demand resin types include Polybutylene Terephthalate (PBT), Polycarbonate (PC), and Polyether Ether Ketone (PEEK), valued for their superior mechanical properties and thermal resistance. Challenges include raw material price volatility and the availability of substitute materials. The market is segmented by resin type (Fluoropolymer, Polyphthalamide, PBT, PC, PEEK, PET, Polyimide, PMMA, POM, Styrene Copolymers) and end-user industry (Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging). Geographic segments within the US are Northeast, Southeast, Midwest, Southwest, and West, with regional growth influenced by industrial presence and infrastructure development. Leading companies such as Arkema, Formosa Plastics Group, Solvay, and BASF SE are key market influencers through innovation, strategic alliances, and capacity enhancements.

United States Engineering Plastics Market Market Size (In Billion)

The future trajectory of the US engineering plastics market is intrinsically linked to technological advancements, particularly in the development of sustainable and high-performance materials. Government initiatives promoting sustainable practices and environmental stewardship will increasingly shape the adoption of eco-friendly engineering plastics. Furthermore, the integration of automation and advanced manufacturing techniques across industries will sustain demand. Intense competition among established players necessitates continuous innovation and strategic investment in research and development. Market performance is also closely correlated with the overall economic health of the US, especially the manufacturing and construction sectors. Exploring niche applications such as medical devices and advanced robotics presents lucrative growth avenues. The anticipated sustained CAGR underscores the US engineering plastics market as a promising investment opportunity, notwithstanding existing challenges.

United States Engineering Plastics Market Company Market Share

United States Engineering Plastics Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the United States engineering plastics market, encompassing market dynamics, growth trends, key players, and future outlook. The report covers the period 2019-2033, with 2025 as the base year and a forecast period of 2025-2033. The market is segmented by resin type (Fluoropolymer, Polyphthalamide, Polybutylene Terephthalate (PBT), Polycarbonate (PC), Polyether Ether Ketone (PEEK), Polyethylene Terephthalate (PET), Polyimide (PI), Polymethyl Methacrylate (PMMA), Polyoxymethylene (POM), Styrene Copolymers (ABS and SAN)) and end-user industry (Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging, Other End-user Industries). The market size is presented in million units.

Key players analyzed include: Arkema, Formosa Plastics Group, Solvay, Koch Industries Inc, INEOS, Celanese Corporation, Indorama Ventures Public Company Limited, Ascend Performance Materials, BASF SE, SABIC, RTP Company, DuPont, Alfa S A B de C V, Covestro AG, and The Chemours Company.

United States Engineering Plastics Market Dynamics & Structure

The United States engineering plastics market is characterized by moderate concentration, with a few major players holding significant market share. Technological innovation, driven by the demand for lighter, stronger, and more durable materials across various end-use sectors, is a key driver. Stringent regulatory frameworks regarding material safety and environmental impact influence market dynamics. The market faces competition from alternative materials like metal alloys and composites. The end-user demographics are diverse, spanning automotive, aerospace, electronics, and construction. M&A activity is significant, reflecting consolidation and expansion efforts within the industry.

- Market Concentration: xx% market share held by top 5 players in 2024.

- Technological Innovation: Focus on high-performance polymers with improved thermal stability, chemical resistance, and mechanical strength.

- Regulatory Framework: Compliance with RoHS, REACH, and other environmental regulations.

- Competitive Substitutes: Metals, composites, and bio-based plastics pose competitive pressure.

- M&A Trends: Significant increase in M&A activity in the past 5 years, driven by strategic acquisitions and portfolio expansion. xx M&A deals were recorded between 2019 and 2024.

United States Engineering Plastics Market Growth Trends & Insights

The United States engineering plastics market experienced steady growth from 2019 to 2024, with a CAGR of xx%. This growth is attributed to increasing demand from key end-use sectors, particularly automotive and electronics. Technological advancements, such as the development of high-performance polymers, are driving adoption rates. Consumer preferences for lightweight and fuel-efficient vehicles are boosting demand in the automotive sector. The market is witnessing disruptions due to the increasing adoption of sustainable and bio-based plastics. Market penetration of engineering plastics in specific applications continues to grow, fueled by cost-effectiveness and improved material properties. Future growth is anticipated to be driven by the increasing adoption of electric vehicles and renewable energy technologies. The projected CAGR for the forecast period (2025-2033) is xx%.

Dominant Regions, Countries, or Segments in United States Engineering Plastics Market

The automotive and electronics sectors are the dominant end-user industries, driving significant market growth. Among resin types, Polycarbonate (PC), Polybutylene Terephthalate (PBT), and Polyamide hold major market shares. The South and Midwest regions show strong growth potential, driven by the presence of major manufacturing hubs and industrial activities.

- Dominant End-User Industries: Automotive (xx%), Electrical & Electronics (xx%).

- Dominant Resin Types: Polycarbonate (PC) (xx%), Polybutylene Terephthalate (PBT) (xx%), Polyamide (xx%).

- Regional Growth Drivers: Strong industrial base and manufacturing activity in the South and Midwest regions.

- Growth Potential: Increased adoption of lightweight materials in automotive and aerospace.

United States Engineering Plastics Market Product Landscape

The market features a wide array of engineering plastics with diverse applications. Recent innovations focus on enhanced performance characteristics, such as improved heat resistance, chemical resistance, and mechanical strength. Unique selling propositions include superior durability, lightweight properties, and recyclability. Technological advancements incorporate nanomaterials and additive manufacturing techniques.

Key Drivers, Barriers & Challenges in United States Engineering Plastics Market

Key Drivers:

- Increasing demand from automotive and electronics sectors.

- Growing adoption of lightweight materials for fuel efficiency and improved performance.

- Technological advancements in polymer synthesis and processing.

Challenges:

- Fluctuations in raw material prices.

- Stringent environmental regulations and concerns about plastic waste.

- Competition from alternative materials and technologies. Estimated to cause a xx% reduction in market growth by 2030.

Emerging Opportunities in United States Engineering Plastics Market

- Growing demand for sustainable and bio-based plastics.

- Increased adoption of additive manufacturing (3D printing) for customized applications.

- Expansion into new high-growth sectors like renewable energy and medical devices.

Growth Accelerators in the United States Engineering Plastics Market Industry

Long-term growth will be fueled by technological breakthroughs leading to the development of even higher-performance materials. Strategic partnerships and collaborations between material suppliers and end-users will further accelerate innovation and market expansion. Expansion into new, high-growth markets, along with the growing adoption of circular economy principles, will drive significant market growth.

Key Players Shaping the United States Engineering Plastics Market Market

- Arkema

- Formosa Plastics Group

- Solvay

- Koch Industries Inc

- INEOS

- Celanese Corporation

- Indorama Ventures Public Company Limited

- Ascend Performance Materials

- BASF SE

- SABIC

- RTP Company

- DuPont

- Alfa S A B de C V

- Covestro AG

- The Chemours Company

Notable Milestones in United States Engineering Plastics Market Sector

- November 2022: Solvay and Orbia announced a partnership for PVDF production for battery materials, expanding North American capacity.

- November 2022: Celanese Corporation acquired DuPont's Mobility & Materials business, expanding its engineered thermoplastics portfolio.

- February 2023: Covestro AG launched Makrolon 3638 polycarbonate for healthcare and life sciences applications.

In-Depth United States Engineering Plastics Market Market Outlook

The future of the United States engineering plastics market looks promising, driven by continuous technological advancements, increasing demand from key sectors, and a growing focus on sustainability. Strategic partnerships, innovative product development, and expansion into new applications will create lucrative opportunities for market participants. The market is poised for substantial growth, driven by the accelerating adoption of lightweight materials in the automotive and aerospace industries, as well as the rise of sustainable and bio-based alternatives.

United States Engineering Plastics Market Segmentation

-

1. End User Industry

- 1.1. Aerospace

- 1.2. Automotive

- 1.3. Building and Construction

- 1.4. Electrical and Electronics

- 1.5. Industrial and Machinery

- 1.6. Packaging

- 1.7. Other End-user Industries

-

2. Resin Type

-

2.1. Fluoropolymer

-

2.1.1. By Sub Resin Type

- 2.1.1.1. Ethylenetetrafluoroethylene (ETFE)

- 2.1.1.2. Fluorinated Ethylene-propylene (FEP)

- 2.1.1.3. Polytetrafluoroethylene (PTFE)

- 2.1.1.4. Polyvinylfluoride (PVF)

- 2.1.1.5. Polyvinylidene Fluoride (PVDF)

- 2.1.1.6. Other Sub Resin Types

-

2.1.1. By Sub Resin Type

- 2.2. Liquid Crystal Polymer (LCP)

-

2.3. Polyamide (PA)

- 2.3.1. Aramid

- 2.3.2. Polyamide (PA) 6

- 2.3.3. Polyamide (PA) 66

- 2.3.4. Polyphthalamide

- 2.4. Polybutylene Terephthalate (PBT)

- 2.5. Polycarbonate (PC)

- 2.6. Polyether Ether Ketone (PEEK)

- 2.7. Polyethylene Terephthalate (PET)

- 2.8. Polyimide (PI)

- 2.9. Polymethyl Methacrylate (PMMA)

- 2.10. Polyoxymethylene (POM)

- 2.11. Styrene Copolymers (ABS and SAN)

-

2.1. Fluoropolymer

United States Engineering Plastics Market Segmentation By Geography

- 1. United States

United States Engineering Plastics Market Regional Market Share

Geographic Coverage of United States Engineering Plastics Market

United States Engineering Plastics Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.28% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rising Demand for Low-pressure Membrane Technologies; Other Drivers

- 3.3. Market Restrains

- 3.3.1. Poor Fouling Resistance of Nano porous Membranes; Other Restraints

- 3.4. Market Trends

- 3.4.1. OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. United States Engineering Plastics Market Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 5.1.1. Aerospace

- 5.1.2. Automotive

- 5.1.3. Building and Construction

- 5.1.4. Electrical and Electronics

- 5.1.5. Industrial and Machinery

- 5.1.6. Packaging

- 5.1.7. Other End-user Industries

- 5.2. Market Analysis, Insights and Forecast - by Resin Type

- 5.2.1. Fluoropolymer

- 5.2.1.1. By Sub Resin Type

- 5.2.1.1.1. Ethylenetetrafluoroethylene (ETFE)

- 5.2.1.1.2. Fluorinated Ethylene-propylene (FEP)

- 5.2.1.1.3. Polytetrafluoroethylene (PTFE)

- 5.2.1.1.4. Polyvinylfluoride (PVF)

- 5.2.1.1.5. Polyvinylidene Fluoride (PVDF)

- 5.2.1.1.6. Other Sub Resin Types

- 5.2.1.1. By Sub Resin Type

- 5.2.2. Liquid Crystal Polymer (LCP)

- 5.2.3. Polyamide (PA)

- 5.2.3.1. Aramid

- 5.2.3.2. Polyamide (PA) 6

- 5.2.3.3. Polyamide (PA) 66

- 5.2.3.4. Polyphthalamide

- 5.2.4. Polybutylene Terephthalate (PBT)

- 5.2.5. Polycarbonate (PC)

- 5.2.6. Polyether Ether Ketone (PEEK)

- 5.2.7. Polyethylene Terephthalate (PET)

- 5.2.8. Polyimide (PI)

- 5.2.9. Polymethyl Methacrylate (PMMA)

- 5.2.10. Polyoxymethylene (POM)

- 5.2.11. Styrene Copolymers (ABS and SAN)

- 5.2.1. Fluoropolymer

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United States

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 Arkema

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Formosa Plastics Group

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Solvay

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Koch Industries Inc

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 INEOS

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Celanese Corporation

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Indorama Ventures Public Company Limited

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Ascend Performance Materials

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 BASF SE

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 SABIC

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 RTP Company

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 DuPont

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.13 Alfa S A B de C V

- 6.2.13.1. Overview

- 6.2.13.2. Products

- 6.2.13.3. SWOT Analysis

- 6.2.13.4. Recent Developments

- 6.2.13.5. Financials (Based on Availability)

- 6.2.14 Covestro AG

- 6.2.14.1. Overview

- 6.2.14.2. Products

- 6.2.14.3. SWOT Analysis

- 6.2.14.4. Recent Developments

- 6.2.14.5. Financials (Based on Availability)

- 6.2.15 The Chemours Compan

- 6.2.15.1. Overview

- 6.2.15.2. Products

- 6.2.15.3. SWOT Analysis

- 6.2.15.4. Recent Developments

- 6.2.15.5. Financials (Based on Availability)

- 6.2.1 Arkema

List of Figures

- Figure 1: United States Engineering Plastics Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: United States Engineering Plastics Market Share (%) by Company 2025

List of Tables

- Table 1: United States Engineering Plastics Market Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 2: United States Engineering Plastics Market Volume K Tons Forecast, by End User Industry 2020 & 2033

- Table 3: United States Engineering Plastics Market Revenue billion Forecast, by Resin Type 2020 & 2033

- Table 4: United States Engineering Plastics Market Volume K Tons Forecast, by Resin Type 2020 & 2033

- Table 5: United States Engineering Plastics Market Revenue billion Forecast, by Region 2020 & 2033

- Table 6: United States Engineering Plastics Market Volume K Tons Forecast, by Region 2020 & 2033

- Table 7: United States Engineering Plastics Market Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 8: United States Engineering Plastics Market Volume K Tons Forecast, by End User Industry 2020 & 2033

- Table 9: United States Engineering Plastics Market Revenue billion Forecast, by Resin Type 2020 & 2033

- Table 10: United States Engineering Plastics Market Volume K Tons Forecast, by Resin Type 2020 & 2033

- Table 11: United States Engineering Plastics Market Revenue billion Forecast, by Country 2020 & 2033

- Table 12: United States Engineering Plastics Market Volume K Tons Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United States Engineering Plastics Market?

The projected CAGR is approximately 6.28%.

2. Which companies are prominent players in the United States Engineering Plastics Market?

Key companies in the market include Arkema, Formosa Plastics Group, Solvay, Koch Industries Inc, INEOS, Celanese Corporation, Indorama Ventures Public Company Limited, Ascend Performance Materials, BASF SE, SABIC, RTP Company, DuPont, Alfa S A B de C V, Covestro AG, The Chemours Compan.

3. What are the main segments of the United States Engineering Plastics Market?

The market segments include End User Industry, Resin Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 15.8 billion as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand for Low-pressure Membrane Technologies; Other Drivers.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Poor Fouling Resistance of Nano porous Membranes; Other Restraints.

8. Can you provide examples of recent developments in the market?

February 2023: Covestro AG introduced Makrolon 3638 polycarbonate for healthcare and life sciences applications such as drug delivery devices, wellness and wearable devices, and single-use containers for biopharmaceutical manufacturing.November 2022: Solvay and Orbia announced a framework agreement to form a partnership for the production of suspension-grade polyvinylidene fluoride (PVDF) for battery materials, resulting in the largest capacity in North America.November 2022: Celanese Corporation completed the acquisition of the Mobility & Materials (“M&M”) business of DuPont. This acquisition enhanced the company's product portfolio of engineered thermoplastics through the addition of well-recognized brands and intellectual properties of DuPont.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United States Engineering Plastics Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United States Engineering Plastics Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United States Engineering Plastics Market?

To stay informed about further developments, trends, and reports in the United States Engineering Plastics Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence