Key Insights

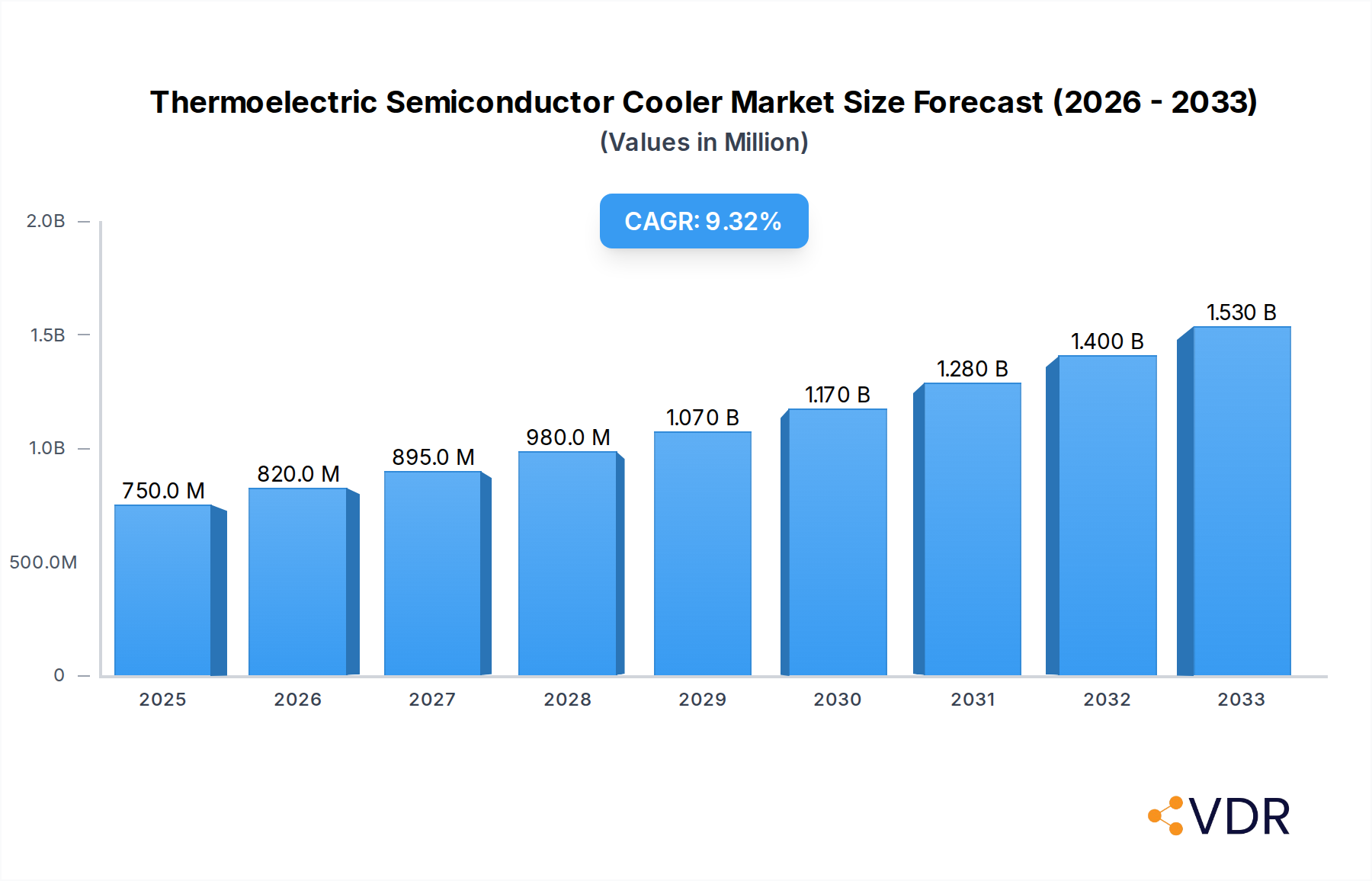

The global Thermoelectric Semiconductor Cooler market is poised for significant expansion, with an estimated market size of $580 million in 2020 and projected to reach substantial heights by 2033, driven by an impressive Compound Annual Growth Rate (CAGR) of 8.7%. This robust growth is fueled by the increasing demand for compact, reliable, and efficient cooling solutions across a multitude of high-growth sectors. Consumer electronics, in particular, is a primary driver, as the proliferation of sophisticated gadgets, from smartphones and laptops to gaming consoles and wearable devices, necessitates advanced thermal management to ensure optimal performance and longevity. The communication sector also plays a vital role, with the deployment of 5G infrastructure and the ever-increasing data processing demands in server farms requiring sophisticated cooling for critical components. Emerging applications in the medical field, such as portable diagnostic equipment and advanced life support systems, alongside the automotive industry's push towards electric vehicles and sophisticated in-cabin electronics, are further amplifying the market's trajectory. Aerospace and defense, known for their stringent requirements for reliable operation in extreme conditions, also contribute to steady demand.

Thermoelectric Semiconductor Cooler Market Size (In Million)

The market's expansion is further supported by key technological advancements and evolving industry trends. The development of more efficient thermoelectric materials and advanced manufacturing techniques is leading to smaller, lighter, and more power-efficient thermoelectric coolers (TECs). The increasing focus on energy efficiency and the reduction of greenhouse gas emissions across industries are also pushing for the adoption of TECs as an environmentally friendly alternative to traditional refrigeration systems in certain applications. While the market benefits from these strong drivers, it also faces certain restraints. The relatively higher initial cost compared to some conventional cooling methods can be a limiting factor in price-sensitive applications. Furthermore, the efficiency of TECs can be dependent on temperature differentials, which can impact their performance in certain extreme environmental conditions. Despite these challenges, the inherent advantages of TECs – their solid-state nature, lack of moving parts, long lifespan, and precise temperature control capabilities – position them favorably for continued market penetration and innovation.

Thermoelectric Semiconductor Cooler Company Market Share

Unlock critical insights into the global Thermoelectric Semiconductor Cooler market, a rapidly expanding sector vital for advanced cooling solutions. This in-depth report provides a holistic view of market dynamics, growth trajectories, regional dominance, product innovations, and future outlook, specifically designed for industry professionals seeking strategic advantage.

Thermoelectric Semiconductor Cooler Market Dynamics & Structure

The thermoelectric semiconductor cooler (TEC) market is characterized by a moderately concentrated structure, with a blend of established global players and emerging regional specialists. Technological innovation is the primary driver, fueled by the increasing demand for precise temperature control in sensitive applications. Regulatory frameworks, particularly concerning energy efficiency and environmental impact, are also shaping product development and market entry strategies. Competitive product substitutes, while present, often fall short of the precise, solid-state cooling capabilities offered by TECs, particularly in niche applications requiring high reliability and compact designs. End-user demographics are shifting, with a growing reliance on miniaturized and efficient cooling solutions across consumer electronics, medical devices, and automotive systems. Mergers and acquisitions (M&A) trends indicate a consolidation of expertise and market reach, with companies seeking to expand their product portfolios and geographical footprints. For instance, in the historical period (2019-2024), the market saw approximately $0.3 billion in M&A deal volumes, reflecting strategic acquisitions to bolster technological capabilities and market access. Innovation barriers include the inherent efficiency limitations of thermoelectric materials and the high cost of advanced semiconductor manufacturing, though ongoing research in novel materials and improved device architectures is actively addressing these.

- Market Concentration: Moderately concentrated, with key players holding significant shares in specific application segments.

- Technological Innovation Drivers: Miniaturization, energy efficiency improvements, higher cooling capacities, and integration with smart systems.

- Regulatory Frameworks: Increasing emphasis on energy efficiency standards and RoHS compliance.

- Competitive Product Substitutes: Traditional refrigeration, heat pipes, and advanced fan cooling solutions, though limited in precision and size.

- End-User Demographics: Growing demand from sectors requiring precise, compact, and reliable thermal management.

- M&A Trends: Strategic acquisitions to consolidate market share, acquire specialized technologies, and expand product offerings.

Thermoelectric Semiconductor Cooler Growth Trends & Insights

The global Thermoelectric Semiconductor Cooler market is poised for robust growth, driven by an insatiable demand for sophisticated thermal management solutions across a spectrum of industries. The market size, projected to reach $3.5 billion by 2025, is expected to witness a Compound Annual Growth Rate (CAGR) of 7.8% during the forecast period (2025-2033). This expansion is underpinned by escalating adoption rates in consumer electronics, where TECs are integral to cooling high-performance processors in laptops, gaming consoles, and smartphones, contributing an estimated $1.1 billion to the market in 2025. The communication sector, driven by the rollout of 5G infrastructure and advanced data centers, presents a significant growth avenue, with an estimated market contribution of $0.7 billion in 2025, as the need for reliable cooling of sensitive networking equipment intensifies. Medical applications, ranging from diagnostic imaging devices to portable blood analyzers, are experiencing a surge in demand for precise temperature control, estimated at $0.5 billion in 2025, highlighting the critical role of TECs in maintaining the efficacy and reliability of life-saving equipment.

Technological disruptions are playing a pivotal role, with advancements in thermoelectric materials science leading to enhanced Coefficient of Performance (COP) and higher cooling power densities. This innovation is enabling TECs to replace conventional cooling methods in increasingly diverse scenarios. Consumer behavior shifts are also influencing market dynamics; there is a growing preference for compact, silent, and energy-efficient devices, which TECs are uniquely positioned to deliver. For instance, the integration of TECs into portable refrigeration units and advanced personal climate control devices reflects this trend. The automotive industry's transition towards electric vehicles (EVs) and autonomous driving systems is creating a substantial market for TECs in battery thermal management, cabin cooling, and advanced sensor cooling, projected to reach $0.6 billion in 2025. The industrial segment, encompassing precision manufacturing, scientific instrumentation, and specialized cooling for lasers, continues to be a foundational market, estimated at $0.4 billion in 2025. The overall market penetration is deepening as awareness of TEC capabilities and their cost-effectiveness in specific applications grows, moving beyond niche markets to broader adoption.

Dominant Regions, Countries, or Segments in Thermoelectric Semiconductor Cooler

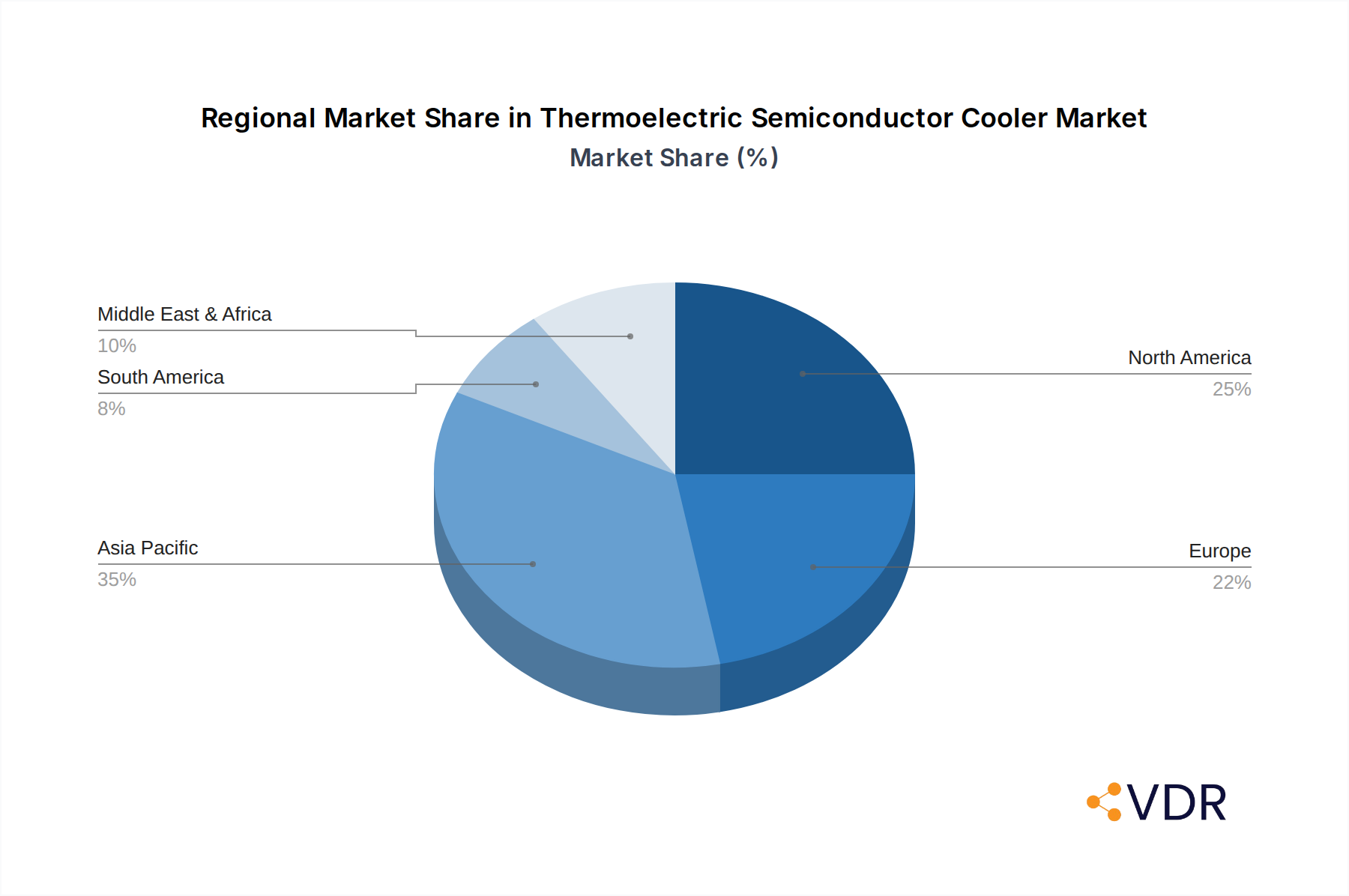

The Asia Pacific region stands out as the dominant force in the global Thermoelectric Semiconductor Cooler market, projecting to account for an estimated 45% of the total market share in 2025, valued at approximately $1.6 billion. This dominance is propelled by a confluence of factors, including its robust manufacturing ecosystem, rapid technological adoption, and significant investments in key application sectors. China, in particular, is a powerhouse, serving as a global hub for consumer electronics and communication equipment manufacturing, thereby driving substantial demand for TECs. Government initiatives supporting high-tech industries and research and development further bolster its position.

Within the Application segment, Consumer Electronics emerges as the leading driver of market growth. In 2025, this segment is projected to represent 30% of the total market, valued at $1.1 billion. The ever-increasing demand for more powerful and compact electronic devices, such as smartphones, laptops, gaming consoles, and smart home appliances, necessitates advanced and efficient cooling solutions, making TECs indispensable. The continuous push for miniaturization and enhanced performance in these devices directly fuels the demand for single-stage and multi-stage TECs.

The Single-stage Type TECs are expected to dominate the Type segment, holding an estimated 65% market share in 2025, valued at $2.3 billion. This preference is attributed to their widespread application in most consumer and industrial electronics where moderate cooling is sufficient and cost-effectiveness is paramount. Their simplicity, reliability, and lower price point make them the go-to solution for a vast array of applications.

- Dominant Region: Asia Pacific (estimated 45% market share, $1.6 billion in 2025)

- Key Driver: Strong manufacturing base in consumer electronics and communication.

- Key Driver: Significant government support for high-tech industries.

- Key Driver: Rapid adoption of advanced technologies.

- Market Share: China, South Korea, Japan leading growth.

- Leading Application Segment: Consumer Electronics (estimated 30% market share, $1.1 billion in 2025)

- Key Driver: Demand for miniaturized, high-performance electronic devices.

- Key Driver: Need for efficient cooling in smartphones, laptops, gaming consoles.

- Growth Potential: Continual innovation in portable and wearable technology.

- Dominant Type Segment: Single-stage Type (estimated 65% market share, $2.3 billion in 2025)

- Key Driver: Cost-effectiveness and suitability for moderate cooling requirements.

- Key Driver: Wide applicability across diverse industries.

- Growth Potential: Continued demand in established applications.

Thermoelectric Semiconductor Cooler Product Landscape

The product landscape of thermoelectric semiconductor coolers is characterized by continuous innovation focused on enhancing cooling efficiency, power density, and reliability. Companies are developing advanced TEC modules utilizing novel materials like bismuth telluride alloys and exploring new nanostructured materials to improve thermoelectric properties. Product offerings range from compact, single-stage modules for precise temperature stabilization of sensitive sensors and lasers to robust, multi-stage configurations capable of achieving sub-zero temperatures for specialized scientific instruments and medical equipment. Innovations include hermetically sealed modules for harsh environments, high-temperature TECs, and integrated thermal management solutions that combine TECs with heat sinks and fans for optimized performance. The unique selling proposition of TECs lies in their solid-state operation, absence of moving parts, precise temperature control capabilities, and scalability for various thermal loads.

Key Drivers, Barriers & Challenges in Thermoelectric Semiconductor Cooler

The Thermoelectric Semiconductor Cooler market is propelled by several key drivers. The relentless miniaturization trend across electronics necessitates compact cooling solutions that TECs uniquely provide. The growing demand for energy efficiency in all devices, from consumer gadgets to industrial equipment, favors TECs for their precise temperature control and lack of refrigerants. Advancements in material science are leading to higher performance TECs, expanding their application range. The burgeoning automotive sector, particularly electric vehicles requiring sophisticated battery thermal management, presents a significant growth catalyst.

- Key Drivers:

- Miniaturization of electronic devices.

- Increasing demand for energy efficiency and precise temperature control.

- Advancements in thermoelectric materials and manufacturing.

- Growth in automotive (EVs) and medical device sectors.

However, the market faces notable barriers and challenges. The inherent thermodynamic efficiency limitations of thermoelectric cooling, especially compared to traditional vapor-compression systems for large cooling loads, remain a challenge. High manufacturing costs for advanced TECs can limit their adoption in price-sensitive applications. Intense competition from alternative cooling technologies and the need for effective thermal interface materials to maximize TEC performance also pose hurdles. Supply chain vulnerabilities for critical raw materials can impact production and pricing.

- Barriers & Challenges:

- Thermodynamic efficiency limitations.

- High manufacturing costs for high-performance modules.

- Competition from established cooling technologies.

- Supply chain constraints for raw materials.

- Need for effective thermal interface management.

Emerging Opportunities in Thermoelectric Semiconductor Cooler

Emerging opportunities in the Thermoelectric Semiconductor Cooler industry lie in specialized niche applications and advancements in material science. The growing demand for portable and wearable medical devices, such as continuous glucose monitors and advanced diagnostic tools, presents a significant opportunity for miniaturized and highly reliable TECs. Furthermore, the expansion of the Internet of Things (IoT) ecosystem requires efficient cooling for a multitude of sensors and microprocessors, creating new avenues for TEC integration. The development of novel thermoelectric materials with enhanced efficiency and reduced cost, such as those based on skutterudites or half-Heusler alloys, could unlock broader market penetration into areas previously dominated by conventional cooling.

Growth Accelerators in the Thermoelectric Semiconductor Cooler Industry

Growth accelerators in the Thermoelectric Semiconductor Cooler industry are primarily driven by technological breakthroughs and strategic market expansion. The continuous innovation in thermoelectric materials, leading to higher Coefficient of Performance (COP) and greater cooling capacity, is a significant catalyst. Strategic partnerships between TEC manufacturers and end-product developers are crucial for co-designing optimized thermal solutions and accelerating adoption. Furthermore, the increasing focus on sustainability and the phasing out of refrigerants in conventional cooling systems are opening doors for TECs as an environmentally friendly alternative in various applications. The expansion into emerging markets and new application verticals, such as advanced electronics for space exploration and specialized cooling for quantum computing, will further fuel long-term growth.

Key Players Shaping the Thermoelectric Semiconductor Cooler Market

- Ferrotec

- KELK Ltd.(Komatsu)

- Coherent Corp (formerly II-VI Incorporated)

- Laird Thermal Systems

- Z-MAX

- KJLP

- Thermion Company

- Phononic

- Guangdong Fuxin Technology

- KYOCERA

- Thermonamic Electronics

- TE Technology

- Same Sky (formerly CUI Devices)

- Kryotherm Industries

- Crystal Ltd

- Merit Technology Group

- Wakefield Thermal

- Pelonis Technologies

- Zhejiang Wangu Semiconductor

- P&N Technology

- JiangXi Arctic Industrial

- Henan Hongchang Electronic

- Wei County Zhongtian Electron Stock Cooperative

- Beijing Xinyu Kaimeng Electronic Technology

- Beijing Huimao Refrigeration Equipment

- Hangzhou Aurin Cooling Device

Notable Milestones in Thermoelectric Semiconductor Cooler Sector

- 2019: Introduction of novel high-efficiency Peltier modules by major players, improving COP by 5%.

- 2020: Increased M&A activity, with consolidation aimed at technological integration and market reach, approximately $0.15 billion in disclosed deal value.

- 2021: Significant advancements in solid-state cooling for 5G base stations, boosting demand in the communication sector.

- 2022: Growing adoption of TECs in electric vehicle battery thermal management systems, signaling a major market shift.

- 2023: Development of low-profile, high-power-density TECs for consumer electronics, enabling thinner and more powerful devices.

- 2024: Increased investment in R&D for next-generation thermoelectric materials, promising substantial efficiency gains in the coming years.

In-Depth Thermoelectric Semiconductor Cooler Market Outlook

The outlook for the Thermoelectric Semiconductor Cooler market is exceptionally positive, characterized by sustained growth driven by technological innovation and expanding application horizons. Growth accelerators, including advancements in material science leading to more efficient and cost-effective TECs, will continue to propel market penetration. Strategic partnerships between manufacturers and end-users will facilitate the development of tailored thermal solutions, further embedding TECs into diverse product lines. The increasing global emphasis on energy efficiency and the environmental benefits of solid-state cooling are poised to displace less sustainable cooling technologies. Emerging opportunities in advanced medical devices, IoT, and specialized industrial applications will create new revenue streams. The market is set to witness a significant evolution, with TECs becoming an indispensable component in a wide array of high-performance and energy-conscious products.

Thermoelectric Semiconductor Cooler Segmentation

-

1. Application

- 1.1. Consumer Electronics

- 1.2. Communication

- 1.3. Medical

- 1.4. Automotive

- 1.5. Industrial

- 1.6. Aerospace Defense

- 1.7. Others

-

2. Type

- 2.1. Single-stage Type

- 2.2. Multi-stage Type

Thermoelectric Semiconductor Cooler Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Thermoelectric Semiconductor Cooler Regional Market Share

Geographic Coverage of Thermoelectric Semiconductor Cooler

Thermoelectric Semiconductor Cooler REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Thermoelectric Semiconductor Cooler Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Consumer Electronics

- 5.1.2. Communication

- 5.1.3. Medical

- 5.1.4. Automotive

- 5.1.5. Industrial

- 5.1.6. Aerospace Defense

- 5.1.7. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Single-stage Type

- 5.2.2. Multi-stage Type

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Thermoelectric Semiconductor Cooler Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Consumer Electronics

- 6.1.2. Communication

- 6.1.3. Medical

- 6.1.4. Automotive

- 6.1.5. Industrial

- 6.1.6. Aerospace Defense

- 6.1.7. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Single-stage Type

- 6.2.2. Multi-stage Type

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Thermoelectric Semiconductor Cooler Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Consumer Electronics

- 7.1.2. Communication

- 7.1.3. Medical

- 7.1.4. Automotive

- 7.1.5. Industrial

- 7.1.6. Aerospace Defense

- 7.1.7. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Single-stage Type

- 7.2.2. Multi-stage Type

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Thermoelectric Semiconductor Cooler Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Consumer Electronics

- 8.1.2. Communication

- 8.1.3. Medical

- 8.1.4. Automotive

- 8.1.5. Industrial

- 8.1.6. Aerospace Defense

- 8.1.7. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Single-stage Type

- 8.2.2. Multi-stage Type

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Thermoelectric Semiconductor Cooler Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Consumer Electronics

- 9.1.2. Communication

- 9.1.3. Medical

- 9.1.4. Automotive

- 9.1.5. Industrial

- 9.1.6. Aerospace Defense

- 9.1.7. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Single-stage Type

- 9.2.2. Multi-stage Type

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Thermoelectric Semiconductor Cooler Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Consumer Electronics

- 10.1.2. Communication

- 10.1.3. Medical

- 10.1.4. Automotive

- 10.1.5. Industrial

- 10.1.6. Aerospace Defense

- 10.1.7. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Single-stage Type

- 10.2.2. Multi-stage Type

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Ferrotec

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 KELK Ltd.(Komatsu)

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Coherent Corp (formerly II-VI Incorporated)

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Laird Thermal Systems

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Z-MAX

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 KJLP

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Thermion Company

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Phononic

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Guangdong Fuxin Technology

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 KYOCERA

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Thermonamic Electronics

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 TE Technology

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Same Sky (formerly CUI Devices)

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Kryotherm Industries

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Crystal Ltd

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Merit Technology Group

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Wakefield Thermal

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Pelonis Technologies

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Zhejiang Wangu Semiconductor

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 P&N Technology

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 JiangXi Arctic Industrial

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 Henan Hongchang Electronic

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 Wei County Zhongtian Electron Stock Cooperative

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 Beijing Xinyu Kaimeng Electronic Technology

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.25 Beijing Huimao Refrigeration Equipment

- 11.2.25.1. Overview

- 11.2.25.2. Products

- 11.2.25.3. SWOT Analysis

- 11.2.25.4. Recent Developments

- 11.2.25.5. Financials (Based on Availability)

- 11.2.26 Hangzhou Aurin Cooling Device

- 11.2.26.1. Overview

- 11.2.26.2. Products

- 11.2.26.3. SWOT Analysis

- 11.2.26.4. Recent Developments

- 11.2.26.5. Financials (Based on Availability)

- 11.2.1 Ferrotec

List of Figures

- Figure 1: Global Thermoelectric Semiconductor Cooler Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Thermoelectric Semiconductor Cooler Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Thermoelectric Semiconductor Cooler Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Thermoelectric Semiconductor Cooler Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Thermoelectric Semiconductor Cooler Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Thermoelectric Semiconductor Cooler Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Thermoelectric Semiconductor Cooler Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Thermoelectric Semiconductor Cooler Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Thermoelectric Semiconductor Cooler Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Thermoelectric Semiconductor Cooler Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Thermoelectric Semiconductor Cooler Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Thermoelectric Semiconductor Cooler Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Thermoelectric Semiconductor Cooler Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Thermoelectric Semiconductor Cooler Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Thermoelectric Semiconductor Cooler Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Thermoelectric Semiconductor Cooler Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Thermoelectric Semiconductor Cooler Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Thermoelectric Semiconductor Cooler Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Thermoelectric Semiconductor Cooler Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Thermoelectric Semiconductor Cooler Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Thermoelectric Semiconductor Cooler Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Thermoelectric Semiconductor Cooler Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Thermoelectric Semiconductor Cooler Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Thermoelectric Semiconductor Cooler Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Thermoelectric Semiconductor Cooler Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Thermoelectric Semiconductor Cooler Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Thermoelectric Semiconductor Cooler Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Thermoelectric Semiconductor Cooler Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Thermoelectric Semiconductor Cooler Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Thermoelectric Semiconductor Cooler Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Thermoelectric Semiconductor Cooler Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Thermoelectric Semiconductor Cooler Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Thermoelectric Semiconductor Cooler Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Thermoelectric Semiconductor Cooler Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Thermoelectric Semiconductor Cooler Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Thermoelectric Semiconductor Cooler Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Thermoelectric Semiconductor Cooler Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Thermoelectric Semiconductor Cooler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Thermoelectric Semiconductor Cooler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Thermoelectric Semiconductor Cooler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Thermoelectric Semiconductor Cooler Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Thermoelectric Semiconductor Cooler Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Thermoelectric Semiconductor Cooler Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Thermoelectric Semiconductor Cooler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Thermoelectric Semiconductor Cooler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Thermoelectric Semiconductor Cooler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Thermoelectric Semiconductor Cooler Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Thermoelectric Semiconductor Cooler Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Thermoelectric Semiconductor Cooler Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Thermoelectric Semiconductor Cooler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Thermoelectric Semiconductor Cooler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Thermoelectric Semiconductor Cooler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Thermoelectric Semiconductor Cooler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Thermoelectric Semiconductor Cooler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Thermoelectric Semiconductor Cooler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Thermoelectric Semiconductor Cooler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Thermoelectric Semiconductor Cooler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Thermoelectric Semiconductor Cooler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Thermoelectric Semiconductor Cooler Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Thermoelectric Semiconductor Cooler Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Thermoelectric Semiconductor Cooler Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Thermoelectric Semiconductor Cooler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Thermoelectric Semiconductor Cooler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Thermoelectric Semiconductor Cooler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Thermoelectric Semiconductor Cooler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Thermoelectric Semiconductor Cooler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Thermoelectric Semiconductor Cooler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Thermoelectric Semiconductor Cooler Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Thermoelectric Semiconductor Cooler Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Thermoelectric Semiconductor Cooler Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Thermoelectric Semiconductor Cooler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Thermoelectric Semiconductor Cooler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Thermoelectric Semiconductor Cooler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Thermoelectric Semiconductor Cooler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Thermoelectric Semiconductor Cooler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Thermoelectric Semiconductor Cooler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Thermoelectric Semiconductor Cooler Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Thermoelectric Semiconductor Cooler?

The projected CAGR is approximately 8.7%.

2. Which companies are prominent players in the Thermoelectric Semiconductor Cooler?

Key companies in the market include Ferrotec, KELK Ltd.(Komatsu), Coherent Corp (formerly II-VI Incorporated), Laird Thermal Systems, Z-MAX, KJLP, Thermion Company, Phononic, Guangdong Fuxin Technology, KYOCERA, Thermonamic Electronics, TE Technology, Same Sky (formerly CUI Devices), Kryotherm Industries, Crystal Ltd, Merit Technology Group, Wakefield Thermal, Pelonis Technologies, Zhejiang Wangu Semiconductor, P&N Technology, JiangXi Arctic Industrial, Henan Hongchang Electronic, Wei County Zhongtian Electron Stock Cooperative, Beijing Xinyu Kaimeng Electronic Technology, Beijing Huimao Refrigeration Equipment, Hangzhou Aurin Cooling Device.

3. What are the main segments of the Thermoelectric Semiconductor Cooler?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Thermoelectric Semiconductor Cooler," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Thermoelectric Semiconductor Cooler report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Thermoelectric Semiconductor Cooler?

To stay informed about further developments, trends, and reports in the Thermoelectric Semiconductor Cooler, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence