Key Insights

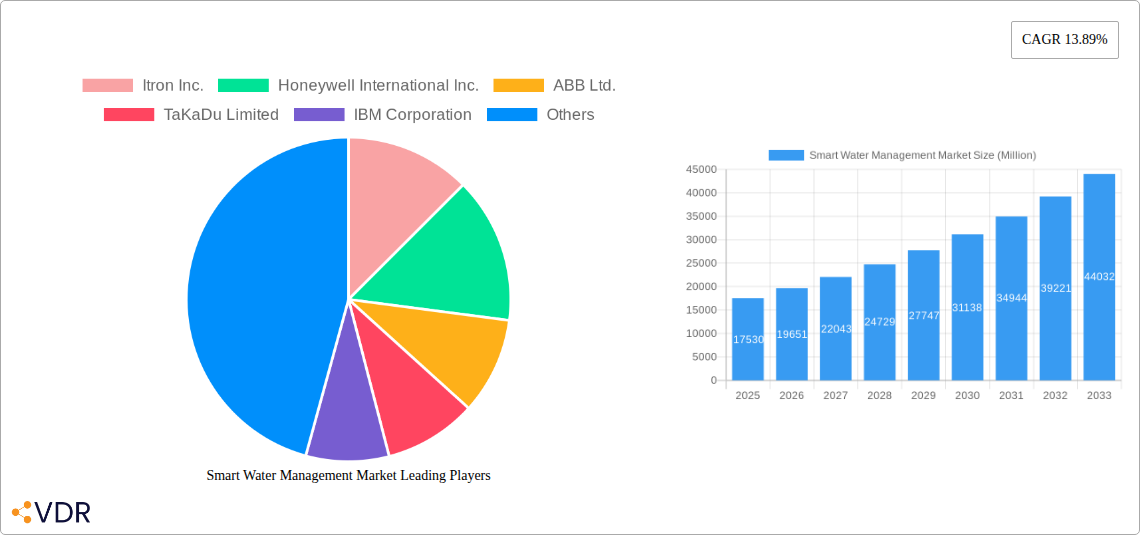

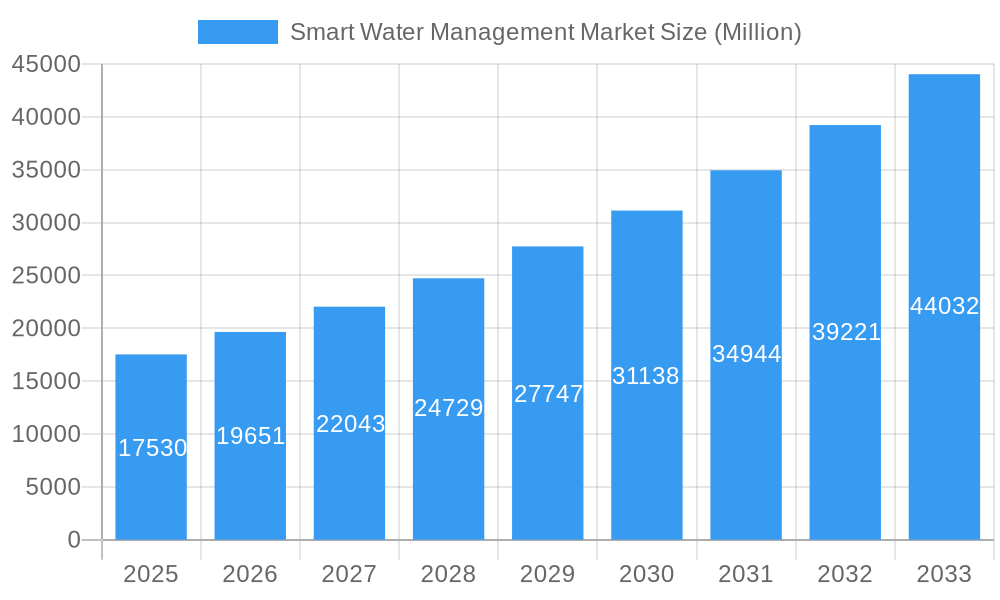

The global Smart Water Management market is poised for significant expansion, projected to reach a substantial $17.53 billion by 2025. This impressive growth is driven by an increasing awareness of water scarcity, the escalating need for efficient water distribution, and the imperative to reduce operational costs for water utilities. Advanced technologies like IoT sensors, AI-powered analytics, and SCADA systems are revolutionizing how water resources are monitored, managed, and conserved. The market's robust CAGR of 12.1% from 2025 to 2033 underscores its dynamic nature, fueled by government initiatives promoting sustainable water practices and the growing adoption of smart city infrastructure. Key solution segments such as Asset Management and Distribution Network Monitoring are vital in optimizing water infrastructure, while Meter Data Management (MDM) offers crucial insights into consumption patterns.

Smart Water Management Market Market Size (In Billion)

Further bolstering this growth trajectory are the burgeoning services sector, encompassing managed and professional services, which enable utilities to effectively implement and leverage smart water solutions. The widespread demand spans across residential, commercial, and industrial end-users, all seeking to improve water efficiency and reduce leakage. Emerging trends like real-time data analytics for predictive maintenance and proactive leak detection are setting new benchmarks for operational excellence. While significant opportunities exist, challenges such as high initial investment costs and the need for robust cybersecurity measures for networked systems require strategic attention. North America and Europe are currently leading in adoption, but the Asia Pacific region is rapidly emerging as a key growth market due to rapid urbanization and increasing water stress.

Smart Water Management Market Company Market Share

Smart Water Management Market: Unlocking Efficiency and Sustainability in a Water-Scarce World (2019–2033)

This comprehensive report offers an in-depth analysis of the global Smart Water Management market, projecting significant growth driven by increasing water scarcity, aging infrastructure, and the imperative for enhanced operational efficiency. Covering the historical period from 2019 to 2024 and a forecast period extending to 2033, with a base year of 2025, this report provides actionable insights for stakeholders seeking to navigate this dynamic sector. Explore detailed segment analysis, regional dominance, product innovations, key players, and emerging opportunities within this critical market.

Smart Water Management Market Dynamics & Structure

The Smart Water Management market is characterized by a moderate to high concentration, with key players actively engaged in strategic partnerships, acquisitions, and continuous technological innovation. The increasing demand for resource conservation and the growing regulatory pressure to reduce water loss are primary technological innovation drivers. Competitive product substitutes are emerging, but the integrated nature of smart water solutions, encompassing asset management, distribution network monitoring, SCADA, MDM, and advanced analytics, creates a strong barrier to entry. End-user demographics are diversifying, with significant growth expected from industrial and commercial sectors alongside the residential segment. Mergers and acquisitions are a prominent trend, as larger players seek to consolidate their market position and acquire specialized technologies. For instance, recent M&A activities are estimated to have a cumulative deal volume of $X.X billion in the historical period, reflecting the industry's consolidation phase.

- Market Concentration: Dominated by a few large players but with a growing number of specialized solution providers.

- Technological Innovation Drivers: Water scarcity, climate change, aging infrastructure, smart city initiatives, energy efficiency mandates.

- Regulatory Frameworks: Stringent water conservation policies, environmental regulations, smart grid integration mandates.

- Competitive Product Substitutes: Traditional water management systems, manual monitoring, standalone sensor technologies.

- End-User Demographics: Growing adoption across residential, commercial (healthcare, education, hospitality), and industrial (manufacturing, energy, mining) sectors.

- M&A Trends: Strategic acquisitions to enhance technological capabilities, expand product portfolios, and gain market share.

Smart Water Management Market Growth Trends & Insights

The global Smart Water Management market is poised for substantial expansion, driven by a confluence of factors including escalating global water demand, increasing investments in smart city infrastructure, and the urgent need to optimize water resource allocation. The market is projected to witness a robust Compound Annual Growth Rate (CAGR) of XX.X% during the forecast period, reaching an estimated market size of $XXX.X billion by 2033. This growth trajectory is fueled by the widespread adoption of advanced technologies such as IoT sensors, AI-powered analytics, and cloud-based platforms, which are revolutionizing water distribution, leak detection, and overall network efficiency. Consumer behavior is shifting towards greater awareness of water conservation, leading to increased demand for smart metering solutions and personalized water usage insights. Technological disruptions, including the integration of digital twins for predictive maintenance and the deployment of advanced meter data management (MDM) systems, are critical in driving market penetration. The market penetration is expected to rise from XX% in 2025 to XX% by 2033.

- Market Size Evolution: Significant growth from an estimated $XX.X billion in 2025 to $XXX.X billion by 2033.

- Adoption Rates: Increasing adoption of smart meters, real-time monitoring systems, and data analytics platforms across utilities and industries.

- Technological Disruptions: AI and ML for predictive analytics, IoT for real-time data collection, blockchain for secure data management.

- Consumer Behavior Shifts: Growing consumer awareness of water conservation, demand for transparent billing and usage data.

- CAGR: Projected at XX.X% during the forecast period (2025–2033).

- Market Penetration: Expected to increase from XX% in 2025 to XX% by 2033.

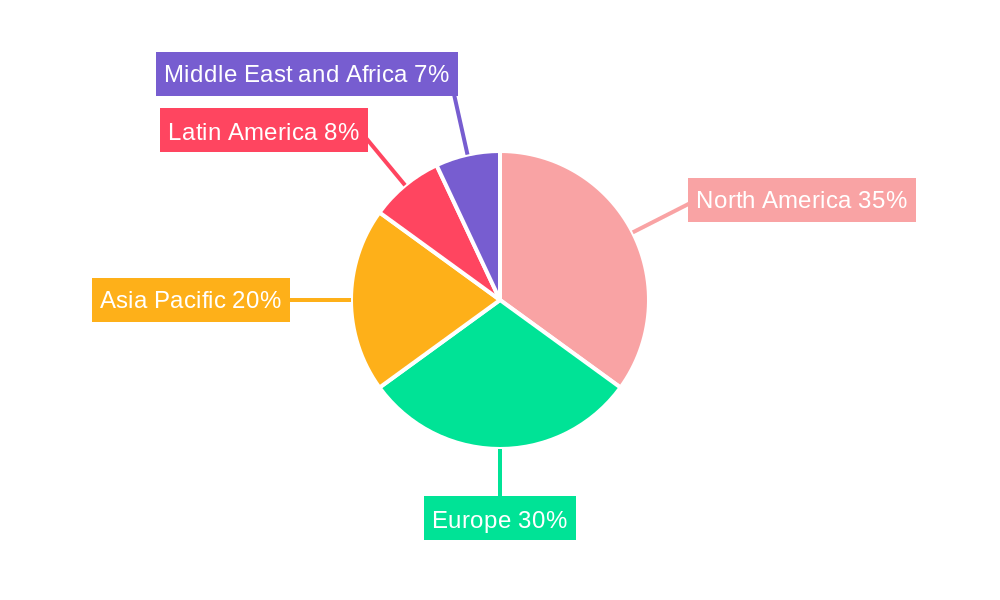

Dominant Regions, Countries, or Segments in Smart Water Management Market

North America is emerging as a dominant region in the Smart Water Management market, propelled by its advanced technological infrastructure, robust government initiatives supporting smart city development, and a proactive approach to water resource management. The United States, in particular, accounts for a significant market share due to substantial investments in upgrading aging water infrastructure and the widespread adoption of smart metering technologies by major utility providers. Furthermore, stringent environmental regulations and a high level of public awareness regarding water conservation contribute to the region's leadership.

Dominant Region: North America, driven by the United States.

- Key Drivers: Aging infrastructure replacement programs, smart city initiatives, strong regulatory framework, high consumer adoption of smart technologies, significant utility investments.

- Market Share (Estimated): North America is projected to hold approximately XX% of the global market share in 2025.

- Growth Potential: Continued strong growth fueled by ongoing infrastructure upgrades and the expansion of smart water solutions into new applications.

Dominant Segment (Type): Distribution Network Monitoring and Meter Data Management (MDM) are leading the solution segments.

- Distribution Network Monitoring: Crucial for real-time leak detection, pressure management, and operational efficiency, reducing non-revenue water.

- Meter Data Management (MDM): Essential for accurate billing, consumption analysis, and empowering consumers with usage insights, driving demand for smart meters.

- Market Share (Estimated): These segments combined are estimated to account for over XX% of the solutions market.

Dominant Segment (End User): The Industrial segment is a significant driver of adoption.

- Industrial Sector: High water consumption and stringent operational requirements necessitate efficient water management for cost savings, regulatory compliance, and sustainability goals. This includes manufacturing, energy, and mining industries.

- Market Share (Estimated): The Industrial segment is expected to contribute approximately XX% to the overall market revenue.

Smart Water Management Market Product Landscape

The Smart Water Management market is defined by continuous product innovation, with a focus on enhancing data accuracy, real-time monitoring capabilities, and predictive analytics. Key product innovations include the development of advanced IoT sensors for granular data collection, sophisticated AI-powered algorithms for anomaly detection and demand forecasting, and integrated platforms that offer end-to-end water management solutions. Unique selling propositions revolve around reducing non-revenue water, optimizing energy consumption in water treatment, and improving the overall resilience of water networks. Technological advancements are leading to more compact, robust, and energy-efficient devices, enabling broader deployment across diverse water systems.

Key Drivers, Barriers & Challenges in Smart Water Management Market

Key Drivers:

- Increasing Water Scarcity: Global population growth and climate change are intensifying the need for efficient water management.

- Aging Infrastructure: Deteriorating water networks lead to significant water loss and contamination risks, necessitating smart upgrades.

- Smart City Initiatives: Governments worldwide are investing in smart technologies to enhance urban infrastructure, including water systems.

- Technological Advancements: IoT, AI, and Big Data analytics enable real-time monitoring, leak detection, and predictive maintenance.

- Regulatory Pressure: Strict environmental regulations and water conservation policies drive the adoption of smart solutions.

Barriers & Challenges:

- High Upfront Costs: Initial investment in smart water management systems can be substantial for utilities.

- Regulatory Hurdles: Complex approval processes and evolving standards can slow down deployment.

- Cybersecurity Concerns: Protecting sensitive water network data from cyber threats is a critical challenge.

- Integration Complexity: Integrating new smart technologies with existing legacy systems can be technically challenging.

- Skilled Workforce Shortage: A lack of trained personnel to operate and maintain advanced smart water systems.

Emerging Opportunities in Smart Water Management Market

Emerging opportunities lie in the development of predictive maintenance solutions powered by AI for water infrastructure, the expansion of smart water management into agricultural applications for precision irrigation, and the integration of smart water systems with other smart city utilities for a holistic approach to resource management. The growing focus on water reuse and recycling technologies presents a significant untapped market. Furthermore, the increasing demand for personalized water usage insights among consumers is creating opportunities for innovative mobile applications and data-driven engagement platforms.

Growth Accelerators in the Smart Water Management Market Industry

Long-term growth in the Smart Water Management industry is being accelerated by groundbreaking technological breakthroughs in sensor technology, leading to more precise and cost-effective data collection. Strategic partnerships between technology providers, utilities, and government bodies are fostering wider adoption and the development of integrated solutions. Market expansion strategies are focusing on developing economies with rapidly urbanizing populations and growing water infrastructure needs. The increasing emphasis on sustainability and circular economy principles is further catalyzing investments in advanced water management solutions.

Key Players Shaping the Smart Water Management Market Market

- Itron Inc.

- Honeywell International Inc.

- ABB Ltd.

- TaKaDu Limited

- IBM Corporation

- Schneider Electric SE (+AVEVA)

- Esri Geographic Information System Company

- Arad Group

- Hitachi Ltd.

- Siemens AG

- Sebata Holdings Limited

- SUEZ Group

- i2O Water Ltd.

- Huawei Technologies Co. Ltd.

- Sensus Inc (Xylem Inc )

Notable Milestones in Smart Water Management Market Sector

- December 2022: The Asian Development Bank (ADB) announced the approval of a USD 20 million financing package to enhance access to drinking water and irrigation services and strengthen climate resilience in Bhutan. This highlights a growing trend of international financial institutions supporting smart water infrastructure development in emerging economies.

- March 2022: Ecopetrol SA, Accenture, and Amazon Web Services (AWS) announced the launch of a first-of-its-kind water intelligence and management solution to help advance sustainability and operational efficiencies for energy companies. This collaboration signifies the growing intersection of smart water management with other industrial sectors, emphasizing data-driven efficiency and sustainability.

- February 2022: ABB introduced the ABB Ability Smart Solution for Wastewater. This digital solution solves wastewater treatment plant operators' challenges in achieving the lowest energy consumption and the highest operational requirements. The innovative solution comprises two main pillars, advanced process control (APC) and digital twin and simulation technology to forecast future operational needs. This product launch underscores the increasing focus on smart solutions for wastewater treatment, emphasizing energy efficiency and predictive capabilities.

In-Depth Smart Water Management Market Market Outlook

The future outlook for the Smart Water Management market is exceptionally strong, driven by sustained investment in smart infrastructure, the critical need for water resource optimization, and ongoing technological advancements. Growth accelerators such as the increasing adoption of AI for predictive analytics, the development of advanced leak detection technologies, and the expansion of smart water solutions into underserved markets will continue to propel market expansion. Strategic opportunities abound for companies that can offer integrated, end-to-end solutions that address the complex challenges of water management, from source to tap and back again. The market is set to transform how we manage and utilize this vital resource, ensuring greater efficiency, sustainability, and resilience for generations to come.

Smart Water Management Market Segmentation

-

1. Type

-

1.1. Solution

- 1.1.1. Asset Management

- 1.1.2. Distribution Network Monitoring

- 1.1.3. Supervisory Control and Data Acquisition (SCADA)

- 1.1.4. Meter Data Management (MDM)

- 1.1.5. Analytics

- 1.1.6. Other Solutions

- 1.2. Services - Managed/Professional

-

1.1. Solution

-

2. End User

- 2.1. Residential

- 2.2. Commercial

- 2.3. Industrial

Smart Water Management Market Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Smart Water Management Market Regional Market Share

Geographic Coverage of Smart Water Management Market

Smart Water Management Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Solution

- 5.1.1.1. Asset Management

- 5.1.1.2. Distribution Network Monitoring

- 5.1.1.3. Supervisory Control and Data Acquisition (SCADA)

- 5.1.1.4. Meter Data Management (MDM)

- 5.1.1.5. Analytics

- 5.1.1.6. Other Solutions

- 5.1.2. Services - Managed/Professional

- 5.1.1. Solution

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Residential

- 5.2.2. Commercial

- 5.2.3. Industrial

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Smart Water Management Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Solution

- 6.1.1.1. Asset Management

- 6.1.1.2. Distribution Network Monitoring

- 6.1.1.3. Supervisory Control and Data Acquisition (SCADA)

- 6.1.1.4. Meter Data Management (MDM)

- 6.1.1.5. Analytics

- 6.1.1.6. Other Solutions

- 6.1.2. Services - Managed/Professional

- 6.1.1. Solution

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Residential

- 6.2.2. Commercial

- 6.2.3. Industrial

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Smart Water Management Market Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Solution

- 7.1.1.1. Asset Management

- 7.1.1.2. Distribution Network Monitoring

- 7.1.1.3. Supervisory Control and Data Acquisition (SCADA)

- 7.1.1.4. Meter Data Management (MDM)

- 7.1.1.5. Analytics

- 7.1.1.6. Other Solutions

- 7.1.2. Services - Managed/Professional

- 7.1.1. Solution

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. Residential

- 7.2.2. Commercial

- 7.2.3. Industrial

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Smart Water Management Market Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Solution

- 8.1.1.1. Asset Management

- 8.1.1.2. Distribution Network Monitoring

- 8.1.1.3. Supervisory Control and Data Acquisition (SCADA)

- 8.1.1.4. Meter Data Management (MDM)

- 8.1.1.5. Analytics

- 8.1.1.6. Other Solutions

- 8.1.2. Services - Managed/Professional

- 8.1.1. Solution

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. Residential

- 8.2.2. Commercial

- 8.2.3. Industrial

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific Smart Water Management Market Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Solution

- 9.1.1.1. Asset Management

- 9.1.1.2. Distribution Network Monitoring

- 9.1.1.3. Supervisory Control and Data Acquisition (SCADA)

- 9.1.1.4. Meter Data Management (MDM)

- 9.1.1.5. Analytics

- 9.1.1.6. Other Solutions

- 9.1.2. Services - Managed/Professional

- 9.1.1. Solution

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. Residential

- 9.2.2. Commercial

- 9.2.3. Industrial

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Latin America Smart Water Management Market Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Solution

- 10.1.1.1. Asset Management

- 10.1.1.2. Distribution Network Monitoring

- 10.1.1.3. Supervisory Control and Data Acquisition (SCADA)

- 10.1.1.4. Meter Data Management (MDM)

- 10.1.1.5. Analytics

- 10.1.1.6. Other Solutions

- 10.1.2. Services - Managed/Professional

- 10.1.1. Solution

- 10.2. Market Analysis, Insights and Forecast - by End User

- 10.2.1. Residential

- 10.2.2. Commercial

- 10.2.3. Industrial

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Middle East and Africa Smart Water Management Market Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Solution

- 11.1.1.1. Asset Management

- 11.1.1.2. Distribution Network Monitoring

- 11.1.1.3. Supervisory Control and Data Acquisition (SCADA)

- 11.1.1.4. Meter Data Management (MDM)

- 11.1.1.5. Analytics

- 11.1.1.6. Other Solutions

- 11.1.2. Services - Managed/Professional

- 11.1.1. Solution

- 11.2. Market Analysis, Insights and Forecast - by End User

- 11.2.1. Residential

- 11.2.2. Commercial

- 11.2.3. Industrial

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Itron Inc.

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Honeywell International Inc.

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 ABB Ltd.

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 TaKaDu Limited

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 IBM Corporation

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Schneider Electric SE (+AVEVA)

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Esri Geographic Information System Company

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Arad Group

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Hitachi Ltd.

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Siemens AG

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Sebata Holdings Limited

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 SUEZ Group

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 i2O Water Ltd.

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Huawei Technologies Co. Ltd.

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Sensus Inc (Xylem Inc )

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 Itron Inc.

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Smart Water Management Market Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Smart Water Management Market Revenue (billion), by Type 2025 & 2033

- Figure 3: North America Smart Water Management Market Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Smart Water Management Market Revenue (billion), by End User 2025 & 2033

- Figure 5: North America Smart Water Management Market Revenue Share (%), by End User 2025 & 2033

- Figure 6: North America Smart Water Management Market Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Smart Water Management Market Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Smart Water Management Market Revenue (billion), by Type 2025 & 2033

- Figure 9: Europe Smart Water Management Market Revenue Share (%), by Type 2025 & 2033

- Figure 10: Europe Smart Water Management Market Revenue (billion), by End User 2025 & 2033

- Figure 11: Europe Smart Water Management Market Revenue Share (%), by End User 2025 & 2033

- Figure 12: Europe Smart Water Management Market Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Smart Water Management Market Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Smart Water Management Market Revenue (billion), by Type 2025 & 2033

- Figure 15: Asia Pacific Smart Water Management Market Revenue Share (%), by Type 2025 & 2033

- Figure 16: Asia Pacific Smart Water Management Market Revenue (billion), by End User 2025 & 2033

- Figure 17: Asia Pacific Smart Water Management Market Revenue Share (%), by End User 2025 & 2033

- Figure 18: Asia Pacific Smart Water Management Market Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific Smart Water Management Market Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America Smart Water Management Market Revenue (billion), by Type 2025 & 2033

- Figure 21: Latin America Smart Water Management Market Revenue Share (%), by Type 2025 & 2033

- Figure 22: Latin America Smart Water Management Market Revenue (billion), by End User 2025 & 2033

- Figure 23: Latin America Smart Water Management Market Revenue Share (%), by End User 2025 & 2033

- Figure 24: Latin America Smart Water Management Market Revenue (billion), by Country 2025 & 2033

- Figure 25: Latin America Smart Water Management Market Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Smart Water Management Market Revenue (billion), by Type 2025 & 2033

- Figure 27: Middle East and Africa Smart Water Management Market Revenue Share (%), by Type 2025 & 2033

- Figure 28: Middle East and Africa Smart Water Management Market Revenue (billion), by End User 2025 & 2033

- Figure 29: Middle East and Africa Smart Water Management Market Revenue Share (%), by End User 2025 & 2033

- Figure 30: Middle East and Africa Smart Water Management Market Revenue (billion), by Country 2025 & 2033

- Figure 31: Middle East and Africa Smart Water Management Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Smart Water Management Market Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global Smart Water Management Market Revenue billion Forecast, by End User 2020 & 2033

- Table 3: Global Smart Water Management Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Smart Water Management Market Revenue billion Forecast, by Type 2020 & 2033

- Table 5: Global Smart Water Management Market Revenue billion Forecast, by End User 2020 & 2033

- Table 6: Global Smart Water Management Market Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Smart Water Management Market Revenue billion Forecast, by Type 2020 & 2033

- Table 8: Global Smart Water Management Market Revenue billion Forecast, by End User 2020 & 2033

- Table 9: Global Smart Water Management Market Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Global Smart Water Management Market Revenue billion Forecast, by Type 2020 & 2033

- Table 11: Global Smart Water Management Market Revenue billion Forecast, by End User 2020 & 2033

- Table 12: Global Smart Water Management Market Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global Smart Water Management Market Revenue billion Forecast, by Type 2020 & 2033

- Table 14: Global Smart Water Management Market Revenue billion Forecast, by End User 2020 & 2033

- Table 15: Global Smart Water Management Market Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global Smart Water Management Market Revenue billion Forecast, by Type 2020 & 2033

- Table 17: Global Smart Water Management Market Revenue billion Forecast, by End User 2020 & 2033

- Table 18: Global Smart Water Management Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Smart Water Management Market?

The projected CAGR is approximately 11.8%.

2. Which companies are prominent players in the Smart Water Management Market?

Key companies in the market include Itron Inc., Honeywell International Inc., ABB Ltd., TaKaDu Limited, IBM Corporation, Schneider Electric SE (+AVEVA), Esri Geographic Information System Company, Arad Group, Hitachi Ltd., Siemens AG, Sebata Holdings Limited, SUEZ Group, i2O Water Ltd., Huawei Technologies Co. Ltd., Sensus Inc (Xylem Inc ).

3. What are the main segments of the Smart Water Management Market?

The market segments include Type, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 20.5 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Need to Manage the Increasing Global Demand for Water; Increasing Demand to Reduce Non-revenue Water (NRW) Losses.

6. What are the notable trends driving market growth?

Growing Need for Water Management to Drive the Market.

7. Are there any restraints impacting market growth?

Lack of Capital Investments to Install Infrastructure.

8. Can you provide examples of recent developments in the market?

December 2022: The Asian Development Bank (ADB) announced the approval of a USD 20 million financing package to enhance access to drinking water and irrigation services and strengthen climate resilience in Bhutan.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Smart Water Management Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Smart Water Management Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Smart Water Management Market?

To stay informed about further developments, trends, and reports in the Smart Water Management Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence