Key Insights

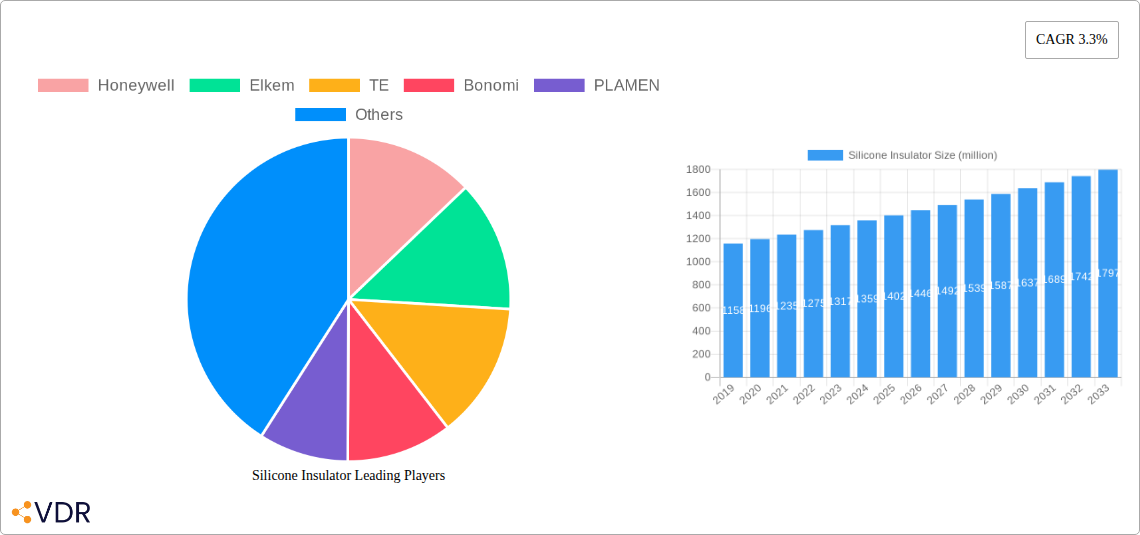

The global silicone insulator market is projected to reach a substantial valuation of $1466 million, driven by a steady Compound Annual Growth Rate (CAGR) of 3.3% from 2019 to 2033. This sustained growth underscores the increasing demand for advanced insulation solutions across various industries. The primary drivers fueling this expansion are the superior dielectric properties, excellent resistance to environmental factors like moisture and UV radiation, and enhanced durability offered by silicone insulators compared to traditional materials. These advantages make them indispensable for high-voltage applications in power transmission and distribution, contributing significantly to grid reliability and efficiency. Furthermore, the ongoing global push for renewable energy, particularly solar and wind power, which often utilize advanced power electronics and require robust insulation, is a significant growth catalyst. The inherent flexibility and lighter weight of silicone insulators also facilitate easier installation and maintenance, further appealing to project developers and utilities.

The market is poised for continued development, with innovations focusing on enhanced performance characteristics such as improved arc resistance, higher mechanical strength, and extended service life. Emerging trends indicate a growing adoption of silicone insulators in railway electrification, electric vehicles, and specialized industrial equipment where safety and reliability are paramount. While the market is robust, certain restraints exist, including the initial cost compared to conventional materials and the availability of alternative insulation technologies. However, the long-term cost benefits derived from reduced maintenance and longer lifespan are increasingly outweighing these initial considerations. Key players like Honeywell, Elkem, and TE are actively investing in research and development to introduce next-generation silicone insulator products, solidifying their market positions and addressing evolving industry needs. The market's segmentation by application and type, alongside strategic regional expansions, will shape its future trajectory.

This in-depth report provides a definitive analysis of the global Silicone Insulator market, offering critical insights into its dynamics, growth trajectory, and future potential. Spanning the study period of 2019–2033, with a base year of 2025 and an estimated year also of 2025, this report leverages advanced analytical methodologies to deliver actionable intelligence for industry stakeholders. We delve into parent and child market segments, providing granular details on applications, types, and key industry developments to offer a holistic view of this rapidly evolving sector.

Silicone Insulator Market Dynamics & Structure

The global silicone insulator market exhibits a moderate concentration, with key players like Honeywell, Elkem, and TE dominating significant market shares. Technological innovation is primarily driven by the demand for high-performance, durable, and weather-resistant insulators for critical electrical infrastructure. Regulatory frameworks, particularly those focused on grid modernization and renewable energy integration, are shaping product development and adoption. Competitive product substitutes, such as porcelain and glass insulators, are being increasingly challenged by the superior dielectric properties, flexibility, and lighter weight of silicone materials, especially in demanding environments. End-user demographics are shifting towards utilities and power transmission companies prioritizing long-term asset reliability and reduced maintenance costs. Mergers and acquisitions (M&A) activity has been present, though not at an extreme level, with strategic consolidations aimed at expanding product portfolios and geographical reach.

- Market Concentration: Moderate, with leading players holding substantial market shares.

- Technological Innovation Drivers: Enhanced dielectric strength, UV resistance, hydrophobicity, and mechanical resilience.

- Regulatory Frameworks: Grid modernization initiatives, renewable energy mandates, and safety standards.

- Competitive Product Substitutes: Porcelain and glass insulators facing pressure from silicone's performance advantages.

- End-User Demographics: Utilities, transmission & distribution companies, renewable energy developers.

- M&A Trends: Strategic acquisitions for portfolio enhancement and market access.

Silicone Insulator Growth Trends & Insights

The silicone insulator market is projected for robust growth, fueled by escalating demand for reliable and resilient electrical infrastructure globally. The market size is expected to evolve significantly from its historical base, driven by continuous technological advancements and the increasing adoption of silicone insulators across various critical applications. Leading the charge are advancements in material science that enhance the performance of silicone insulators, making them lighter, more durable, and better equipped to withstand extreme environmental conditions. This includes improved resistance to UV radiation, pollution, and moisture, which are crucial for extending the lifespan of power grids and reducing maintenance needs.

The adoption rates of silicone insulators are steadily increasing, particularly in regions undergoing significant grid modernization and expansion projects. These projects are often driven by the need to integrate renewable energy sources, which require robust and flexible insulation solutions. The inherent advantages of silicone, such as its excellent electrical insulation properties, high mechanical strength, and resistance to aging, make it a preferred choice over traditional materials like porcelain and glass. This preference is further amplified by the growing emphasis on reducing operational costs and minimizing downtime for critical electrical infrastructure.

Technological disruptions in the manufacturing processes of silicone insulators are also contributing to market expansion. Innovations in molding techniques and material formulations are leading to more cost-effective production, making silicone insulators more competitive. Furthermore, the development of specialized silicone compounds tailored for specific applications, such as high-voltage direct current (HVDC) transmission lines and offshore wind farms, is opening up new market avenues.

Consumer behavior shifts are also playing a pivotal role. Utilities and grid operators are increasingly prioritizing long-term value and performance over initial cost. The lower total cost of ownership associated with silicone insulators, due to their extended service life and reduced maintenance requirements, is a key factor influencing purchasing decisions. Moreover, the growing awareness of the environmental benefits, such as reduced material usage and longer product lifespans, is further aligning consumer preferences with silicone-based solutions.

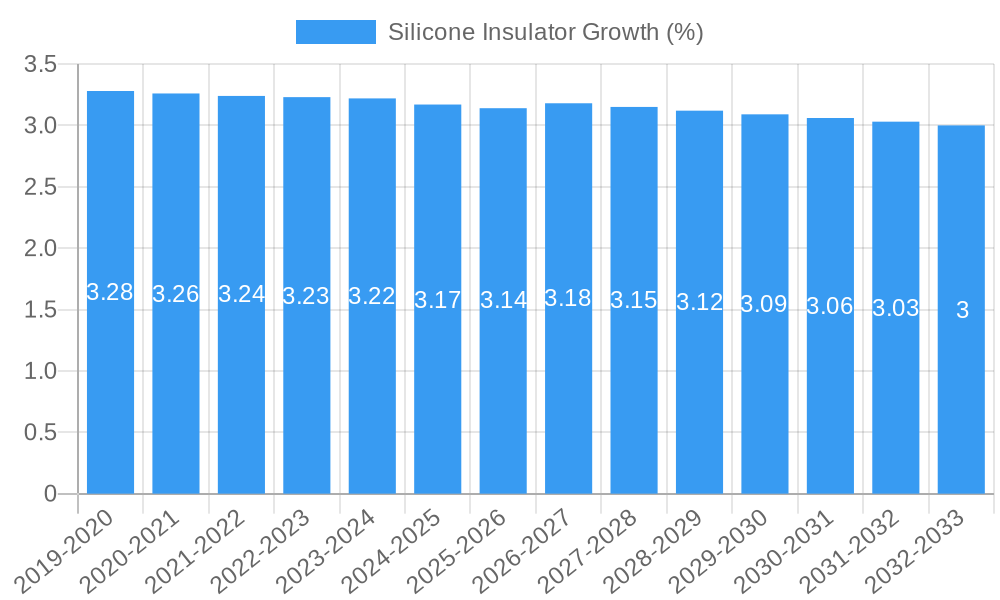

The market is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 6.5% during the forecast period of 2025–2033. This sustained growth trajectory underscores the critical role silicone insulators are set to play in shaping the future of global power transmission and distribution networks. The market penetration of silicone insulators is expected to rise substantially, displacing older technologies and becoming the standard for new installations and upgrades across diverse geographical regions.

Dominant Regions, Countries, or Segments in Silicone Insulator

The Application segment of High-Voltage Transmission Lines is identified as the dominant driver of growth within the global silicone insulator market. This dominance is propelled by several interconnected factors, including massive investments in power grid expansion and modernization worldwide, the increasing demand for efficient and reliable long-distance power transmission, and the inherent advantages of silicone insulators in these demanding applications.

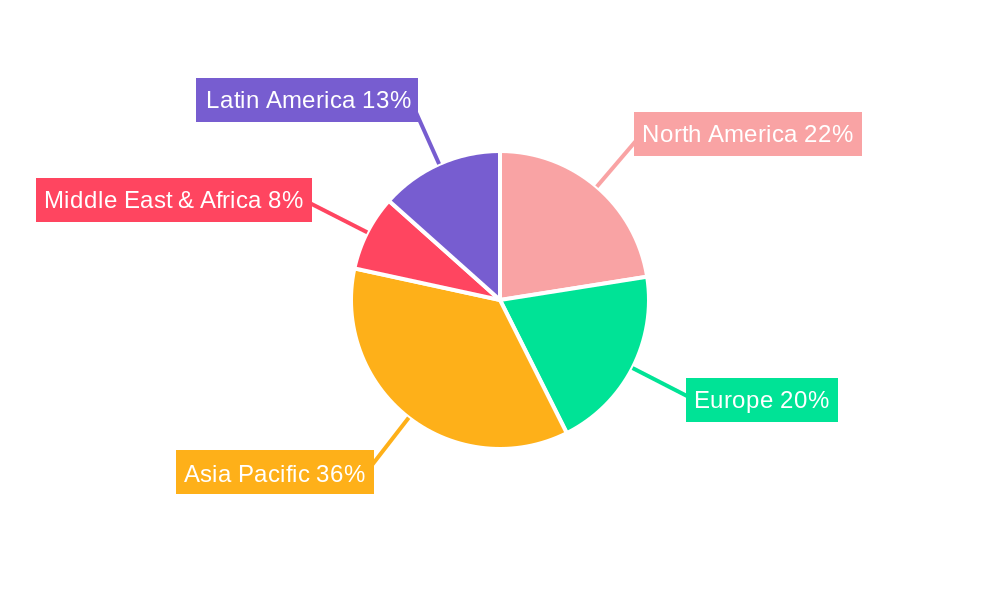

In terms of Region, Asia-Pacific stands out as the most significant and fastest-growing market for silicone insulators. This leadership is attributed to a confluence of powerful economic policies, substantial infrastructure development, and a burgeoning energy demand across countries like China, India, and Southeast Asian nations. These regions are actively investing in upgrading and expanding their electrical grids to meet the needs of their rapidly industrializing economies and growing populations. The push towards renewable energy integration, particularly solar and wind power, further amplifies the demand for advanced insulation solutions like silicone, which perform exceptionally well in variable weather conditions and across vast geographical expanses.

Within the Application segment, High-Voltage Transmission Lines represent the largest market share. The increasing need for efficient power transfer over long distances necessitates the use of highly reliable and durable insulators that can withstand extreme environmental stresses, such as pollution, humidity, and temperature fluctuations. Silicone insulators, with their superior hydrophobic properties, excellent arc resistance, and lightweight construction, offer significant advantages over traditional porcelain or glass insulators in these critical applications. They contribute to reduced line losses and enhanced grid stability, making them the preferred choice for utility companies worldwide.

The Type segment of Suspension Insulators also plays a crucial role in the market's growth, particularly within the high-voltage transmission line application. These insulators are extensively used in overhead power lines to support and isolate conductors from the supporting structures. Their design flexibility and ability to be strung in long chains provide excellent insulation for very high voltage systems.

Key drivers contributing to this regional and segmental dominance include:

- Economic Policies: Government initiatives promoting industrial growth, urbanization, and electrification in regions like Asia-Pacific.

- Infrastructure Development: Large-scale investments in building new power transmission networks and upgrading existing ones.

- Renewable Energy Integration: The growing adoption of renewable energy sources necessitates robust and adaptable insulation for grid connection.

- Technological Advancement: Continuous improvements in silicone material science leading to enhanced performance and cost-effectiveness.

- Environmental Regulations: Stricter regulations promoting the use of more durable and environmentally friendly insulation materials.

- Demand for Grid Reliability: Increasing emphasis on ensuring uninterrupted power supply, especially in critical sectors.

The market share within these dominant segments is estimated to be around 35% for High-Voltage Transmission Lines and approximately 40% for the Asia-Pacific region, with significant growth potential of over 7% CAGR projected for both. The continued expansion of power grids and the relentless pursuit of greater grid reliability are expected to solidify the dominance of these segments and regions in the foreseeable future.

Silicone Insulator Product Landscape

The silicone insulator product landscape is characterized by ongoing innovation focused on enhancing performance, durability, and application versatility. Key advancements include the development of composite insulators with improved dielectric strength, enhanced UV resistance, and superior hydrophobic properties, ensuring excellent performance even in heavily polluted environments. Applications span across various high-voltage transmission lines, substations, and railway electrification systems. Performance metrics such as improved creepage distance, higher mechanical strength, and reduced weight compared to traditional insulators are key selling propositions. Technological advancements are also enabling more cost-effective manufacturing processes, making these high-performance insulators more accessible. Unique selling propositions include their excellent resistance to aging and weathering, leading to extended service life and reduced maintenance costs for power infrastructure.

Key Drivers, Barriers & Challenges in Silicone Insulator

Key Drivers: The silicone insulator market is propelled by the global drive for grid modernization and expansion, particularly to accommodate the increasing integration of renewable energy sources. The superior dielectric properties, lightweight nature, and exceptional weather resistance of silicone insulators make them ideal for high-voltage applications and demanding environmental conditions. Furthermore, the long-term cost savings through reduced maintenance and extended lifespan are significant economic drivers. Technological advancements in material science are continuously improving performance, while supportive government policies promoting electrification and clean energy are fostering market growth.

Barriers & Challenges: Despite the positive growth trajectory, the silicone insulator market faces several challenges. The initial cost of silicone insulators can be higher than traditional porcelain or glass alternatives, which can be a barrier for price-sensitive markets. Supply chain disruptions and volatility in raw material prices, particularly for silicone rubber, can impact production costs and availability. Stringent and evolving regulatory standards across different regions can pose compliance challenges. Moreover, established trust and familiarity with conventional insulator materials can create inertia among some end-users, leading to a slower adoption rate in certain segments.

Emerging Opportunities in Silicone Insulator

Emerging opportunities in the silicone insulator sector lie in the expansion of renewable energy infrastructure, including large-scale solar farms and offshore wind projects, which require specialized and robust insulation solutions. The increasing adoption of electric vehicles (EVs) and the associated charging infrastructure also presents a growing market for medium-voltage insulators. Furthermore, smart grid technologies and the demand for enhanced grid resilience in the face of extreme weather events are creating opportunities for advanced silicone insulator designs with integrated monitoring capabilities. Untapped markets in developing economies with rapidly growing power demands also represent significant potential.

Growth Accelerators in the Silicone Insulator Industry

Several catalysts are accelerating the growth of the silicone insulator industry. The continuous pursuit of higher voltage levels in power transmission necessitates insulators with superior performance characteristics, which silicone materials excel at providing. Strategic partnerships between silicone manufacturers and utility companies facilitate product development and pilot projects, driving market acceptance. Furthermore, ongoing research and development into novel silicone compounds and composite structures are leading to lighter, stronger, and more cost-effective insulators, expanding their applicability and market reach. The increasing global focus on sustainability and the circular economy is also indirectly benefiting silicone insulators due to their longer lifespan and potential for recyclability.

Key Players Shaping the Silicone Insulator Market

- Honeywell

- Elkem

- TE

- Bonomi

- PLAMEN

- Hubbell

- Poinsa

- DECCAN ENTERPRISES PRIVATE LIMITED

- NGK-LOCKE

- Compaq

- Yamuna Power & Infrastructure Ltd

- K-LINE INSULATORS

Notable Milestones in Silicone Insulator Sector

- 2019: Significant advancements in hydrophobic recovery coatings for silicone insulators, improving performance in polluted environments.

- 2020: Increased adoption of composite silicone insulators for HVDC transmission lines, demonstrating enhanced efficiency.

- 2021: Strategic partnerships formed to develop next-generation silicone materials with higher mechanical strength and temperature resistance.

- 2022: Growing demand for silicone insulators in offshore wind farm applications due to their superior corrosion resistance.

- 2023: Launch of innovative silicone insulator designs with integrated sensors for real-time condition monitoring.

- 2024: Further consolidation within the market as companies seek to expand their product portfolios and global presence.

In-Depth Silicone Insulator Market Outlook

- 2019: Significant advancements in hydrophobic recovery coatings for silicone insulators, improving performance in polluted environments.

- 2020: Increased adoption of composite silicone insulators for HVDC transmission lines, demonstrating enhanced efficiency.

- 2021: Strategic partnerships formed to develop next-generation silicone materials with higher mechanical strength and temperature resistance.

- 2022: Growing demand for silicone insulators in offshore wind farm applications due to their superior corrosion resistance.

- 2023: Launch of innovative silicone insulator designs with integrated sensors for real-time condition monitoring.

- 2024: Further consolidation within the market as companies seek to expand their product portfolios and global presence.

In-Depth Silicone Insulator Market Outlook

The future outlook for the silicone insulator market is exceptionally promising, driven by a confluence of sustained global energy demand, the accelerating transition to renewable energy, and ongoing technological innovation. Growth accelerators such as the development of higher voltage-rated insulators and the increasing integration of smart grid technologies will continue to fuel market expansion. Strategic collaborations between manufacturers and end-users will play a crucial role in tailoring solutions for specific challenges. The inherent advantages of silicone insulators in terms of performance, durability, and reduced lifecycle costs position them to capture a larger share of the global insulation market, especially in critical infrastructure upgrades and new installations worldwide. The market is poised for significant value creation and innovation in the coming years.

Silicone Insulator Segmentation

-

1. Application

- 1.1. undefined

-

2. Type

- 2.1. undefined

Silicone Insulator Segmentation By Geography

- 1. undefined

- 2. undefined

- 3. undefined

- 4. undefined

- 5. undefined

Silicone Insulator REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 3.3% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Silicone Insulator Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1.

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1.

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1.

- 5.3.2.

- 5.3.3.

- 5.3.4.

- 5.3.5.

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. undefined Silicone Insulator Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1.

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1.

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. undefined Silicone Insulator Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1.

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1.

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. undefined Silicone Insulator Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1.

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1.

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. undefined Silicone Insulator Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1.

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1.

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. undefined Silicone Insulator Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1.

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1.

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Honeywell

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Elkem

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 TE

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Bonomi

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 PLAMEN

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Hubbell

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Poinsa

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 DECCAN ENTERPRISES PRIVATE LIMITED

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 NGK-LOCKE

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Compaq

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Yamuna Power & Infrastructure Ltd

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 K-LINE INSULATORS

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 Honeywell

List of Figures

- Figure 1: Global Silicone Insulator Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: Global Silicone Insulator Volume Breakdown (K, %) by Region 2024 & 2032

- Figure 3: undefined Silicone Insulator Revenue (million), by Application 2024 & 2032

- Figure 4: undefined Silicone Insulator Volume (K), by Application 2024 & 2032

- Figure 5: undefined Silicone Insulator Revenue Share (%), by Application 2024 & 2032

- Figure 6: undefined Silicone Insulator Volume Share (%), by Application 2024 & 2032

- Figure 7: undefined Silicone Insulator Revenue (million), by Type 2024 & 2032

- Figure 8: undefined Silicone Insulator Volume (K), by Type 2024 & 2032

- Figure 9: undefined Silicone Insulator Revenue Share (%), by Type 2024 & 2032

- Figure 10: undefined Silicone Insulator Volume Share (%), by Type 2024 & 2032

- Figure 11: undefined Silicone Insulator Revenue (million), by Country 2024 & 2032

- Figure 12: undefined Silicone Insulator Volume (K), by Country 2024 & 2032

- Figure 13: undefined Silicone Insulator Revenue Share (%), by Country 2024 & 2032

- Figure 14: undefined Silicone Insulator Volume Share (%), by Country 2024 & 2032

- Figure 15: undefined Silicone Insulator Revenue (million), by Application 2024 & 2032

- Figure 16: undefined Silicone Insulator Volume (K), by Application 2024 & 2032

- Figure 17: undefined Silicone Insulator Revenue Share (%), by Application 2024 & 2032

- Figure 18: undefined Silicone Insulator Volume Share (%), by Application 2024 & 2032

- Figure 19: undefined Silicone Insulator Revenue (million), by Type 2024 & 2032

- Figure 20: undefined Silicone Insulator Volume (K), by Type 2024 & 2032

- Figure 21: undefined Silicone Insulator Revenue Share (%), by Type 2024 & 2032

- Figure 22: undefined Silicone Insulator Volume Share (%), by Type 2024 & 2032

- Figure 23: undefined Silicone Insulator Revenue (million), by Country 2024 & 2032

- Figure 24: undefined Silicone Insulator Volume (K), by Country 2024 & 2032

- Figure 25: undefined Silicone Insulator Revenue Share (%), by Country 2024 & 2032

- Figure 26: undefined Silicone Insulator Volume Share (%), by Country 2024 & 2032

- Figure 27: undefined Silicone Insulator Revenue (million), by Application 2024 & 2032

- Figure 28: undefined Silicone Insulator Volume (K), by Application 2024 & 2032

- Figure 29: undefined Silicone Insulator Revenue Share (%), by Application 2024 & 2032

- Figure 30: undefined Silicone Insulator Volume Share (%), by Application 2024 & 2032

- Figure 31: undefined Silicone Insulator Revenue (million), by Type 2024 & 2032

- Figure 32: undefined Silicone Insulator Volume (K), by Type 2024 & 2032

- Figure 33: undefined Silicone Insulator Revenue Share (%), by Type 2024 & 2032

- Figure 34: undefined Silicone Insulator Volume Share (%), by Type 2024 & 2032

- Figure 35: undefined Silicone Insulator Revenue (million), by Country 2024 & 2032

- Figure 36: undefined Silicone Insulator Volume (K), by Country 2024 & 2032

- Figure 37: undefined Silicone Insulator Revenue Share (%), by Country 2024 & 2032

- Figure 38: undefined Silicone Insulator Volume Share (%), by Country 2024 & 2032

- Figure 39: undefined Silicone Insulator Revenue (million), by Application 2024 & 2032

- Figure 40: undefined Silicone Insulator Volume (K), by Application 2024 & 2032

- Figure 41: undefined Silicone Insulator Revenue Share (%), by Application 2024 & 2032

- Figure 42: undefined Silicone Insulator Volume Share (%), by Application 2024 & 2032

- Figure 43: undefined Silicone Insulator Revenue (million), by Type 2024 & 2032

- Figure 44: undefined Silicone Insulator Volume (K), by Type 2024 & 2032

- Figure 45: undefined Silicone Insulator Revenue Share (%), by Type 2024 & 2032

- Figure 46: undefined Silicone Insulator Volume Share (%), by Type 2024 & 2032

- Figure 47: undefined Silicone Insulator Revenue (million), by Country 2024 & 2032

- Figure 48: undefined Silicone Insulator Volume (K), by Country 2024 & 2032

- Figure 49: undefined Silicone Insulator Revenue Share (%), by Country 2024 & 2032

- Figure 50: undefined Silicone Insulator Volume Share (%), by Country 2024 & 2032

- Figure 51: undefined Silicone Insulator Revenue (million), by Application 2024 & 2032

- Figure 52: undefined Silicone Insulator Volume (K), by Application 2024 & 2032

- Figure 53: undefined Silicone Insulator Revenue Share (%), by Application 2024 & 2032

- Figure 54: undefined Silicone Insulator Volume Share (%), by Application 2024 & 2032

- Figure 55: undefined Silicone Insulator Revenue (million), by Type 2024 & 2032

- Figure 56: undefined Silicone Insulator Volume (K), by Type 2024 & 2032

- Figure 57: undefined Silicone Insulator Revenue Share (%), by Type 2024 & 2032

- Figure 58: undefined Silicone Insulator Volume Share (%), by Type 2024 & 2032

- Figure 59: undefined Silicone Insulator Revenue (million), by Country 2024 & 2032

- Figure 60: undefined Silicone Insulator Volume (K), by Country 2024 & 2032

- Figure 61: undefined Silicone Insulator Revenue Share (%), by Country 2024 & 2032

- Figure 62: undefined Silicone Insulator Volume Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Silicone Insulator Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Silicone Insulator Volume K Forecast, by Region 2019 & 2032

- Table 3: Global Silicone Insulator Revenue million Forecast, by Application 2019 & 2032

- Table 4: Global Silicone Insulator Volume K Forecast, by Application 2019 & 2032

- Table 5: Global Silicone Insulator Revenue million Forecast, by Type 2019 & 2032

- Table 6: Global Silicone Insulator Volume K Forecast, by Type 2019 & 2032

- Table 7: Global Silicone Insulator Revenue million Forecast, by Region 2019 & 2032

- Table 8: Global Silicone Insulator Volume K Forecast, by Region 2019 & 2032

- Table 9: Global Silicone Insulator Revenue million Forecast, by Application 2019 & 2032

- Table 10: Global Silicone Insulator Volume K Forecast, by Application 2019 & 2032

- Table 11: Global Silicone Insulator Revenue million Forecast, by Type 2019 & 2032

- Table 12: Global Silicone Insulator Volume K Forecast, by Type 2019 & 2032

- Table 13: Global Silicone Insulator Revenue million Forecast, by Country 2019 & 2032

- Table 14: Global Silicone Insulator Volume K Forecast, by Country 2019 & 2032

- Table 15: Global Silicone Insulator Revenue million Forecast, by Application 2019 & 2032

- Table 16: Global Silicone Insulator Volume K Forecast, by Application 2019 & 2032

- Table 17: Global Silicone Insulator Revenue million Forecast, by Type 2019 & 2032

- Table 18: Global Silicone Insulator Volume K Forecast, by Type 2019 & 2032

- Table 19: Global Silicone Insulator Revenue million Forecast, by Country 2019 & 2032

- Table 20: Global Silicone Insulator Volume K Forecast, by Country 2019 & 2032

- Table 21: Global Silicone Insulator Revenue million Forecast, by Application 2019 & 2032

- Table 22: Global Silicone Insulator Volume K Forecast, by Application 2019 & 2032

- Table 23: Global Silicone Insulator Revenue million Forecast, by Type 2019 & 2032

- Table 24: Global Silicone Insulator Volume K Forecast, by Type 2019 & 2032

- Table 25: Global Silicone Insulator Revenue million Forecast, by Country 2019 & 2032

- Table 26: Global Silicone Insulator Volume K Forecast, by Country 2019 & 2032

- Table 27: Global Silicone Insulator Revenue million Forecast, by Application 2019 & 2032

- Table 28: Global Silicone Insulator Volume K Forecast, by Application 2019 & 2032

- Table 29: Global Silicone Insulator Revenue million Forecast, by Type 2019 & 2032

- Table 30: Global Silicone Insulator Volume K Forecast, by Type 2019 & 2032

- Table 31: Global Silicone Insulator Revenue million Forecast, by Country 2019 & 2032

- Table 32: Global Silicone Insulator Volume K Forecast, by Country 2019 & 2032

- Table 33: Global Silicone Insulator Revenue million Forecast, by Application 2019 & 2032

- Table 34: Global Silicone Insulator Volume K Forecast, by Application 2019 & 2032

- Table 35: Global Silicone Insulator Revenue million Forecast, by Type 2019 & 2032

- Table 36: Global Silicone Insulator Volume K Forecast, by Type 2019 & 2032

- Table 37: Global Silicone Insulator Revenue million Forecast, by Country 2019 & 2032

- Table 38: Global Silicone Insulator Volume K Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Silicone Insulator?

The projected CAGR is approximately 3.3%.

2. Which companies are prominent players in the Silicone Insulator?

Key companies in the market include Honeywell, Elkem, TE, Bonomi, PLAMEN, Hubbell, Poinsa, DECCAN ENTERPRISES PRIVATE LIMITED, NGK-LOCKE, Compaq, Yamuna Power & Infrastructure Ltd, K-LINE INSULATORS.

3. What are the main segments of the Silicone Insulator?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 1466 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Silicone Insulator," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Silicone Insulator report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Silicone Insulator?

To stay informed about further developments, trends, and reports in the Silicone Insulator, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence