Key Insights

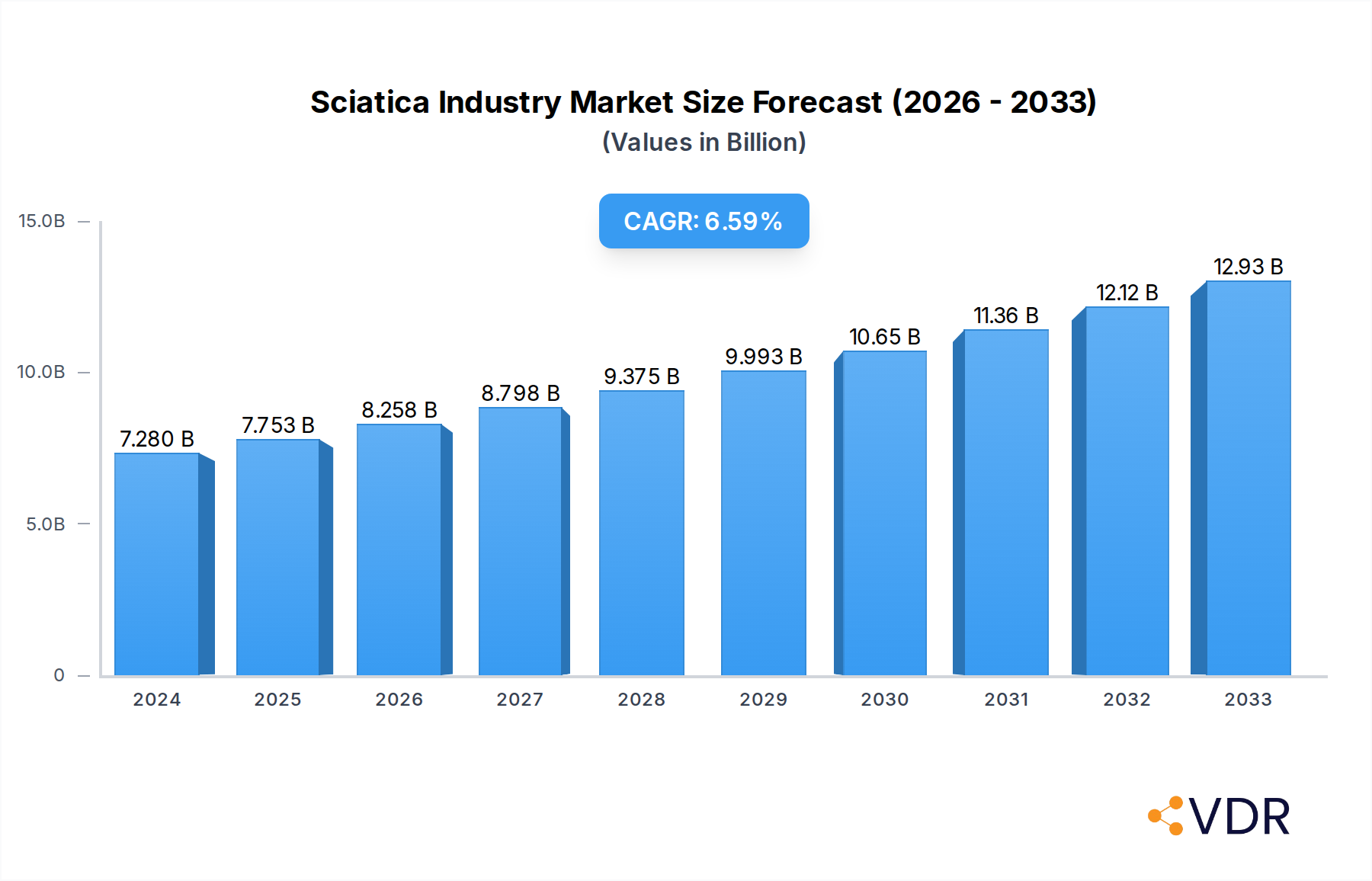

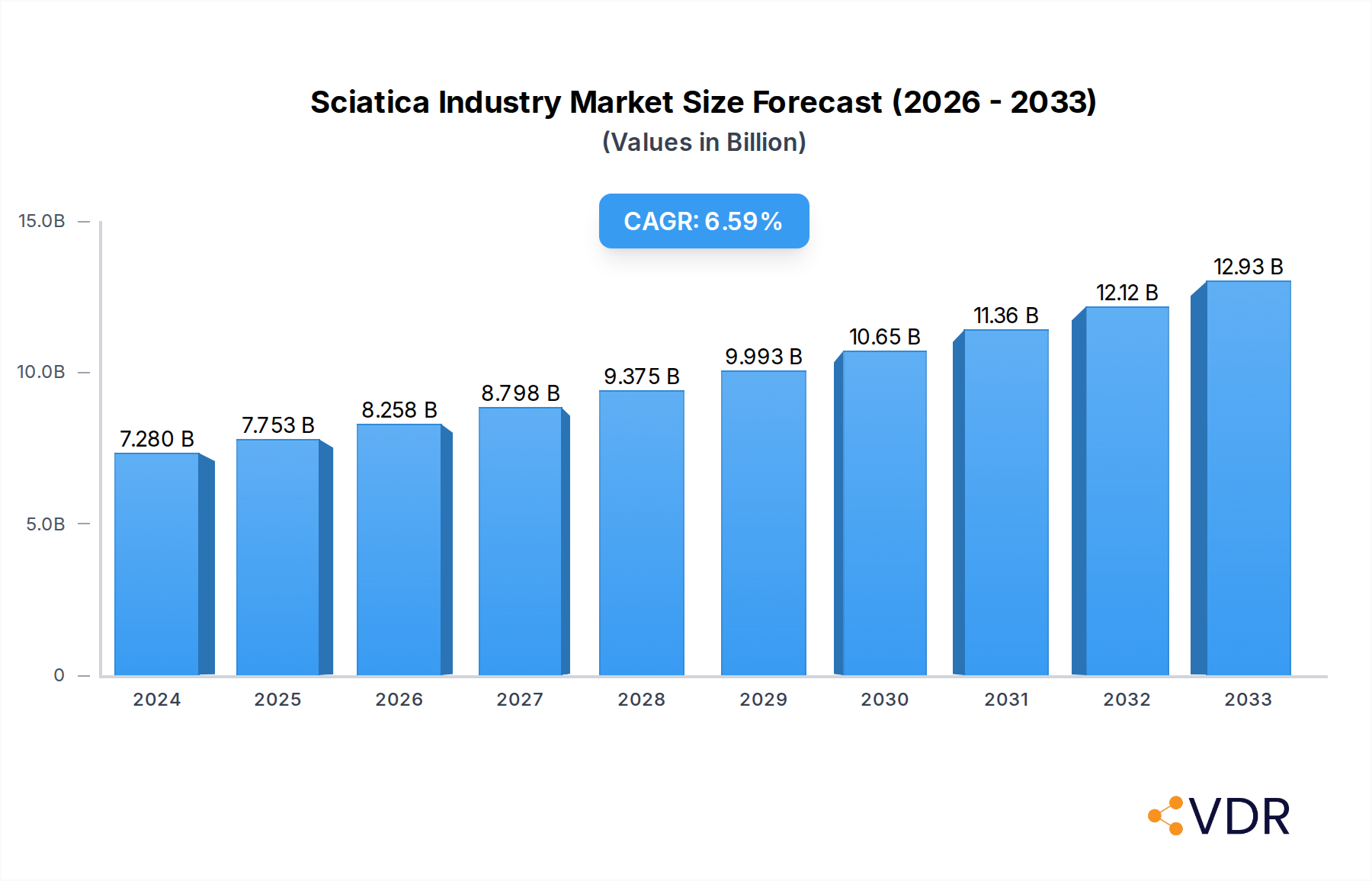

The global sciatica market is poised for significant expansion, projected to reach USD 7.28 billion in 2024 and grow at a robust CAGR of 6.5% through 2033. This growth is propelled by an increasing prevalence of sedentary lifestyles, aging populations, and a rising incidence of lower back pain, all contributing to a higher demand for effective sciatica treatments. Key market drivers include advancements in pharmacological therapies, such as the development of more targeted NSAIDs and novel pain management solutions, alongside growing awareness and early diagnosis of the condition. The market's segmentation highlights a strong focus on both acute and chronic sciatica management, with pharmacological interventions forming the backbone of treatment strategies. This includes established treatments like NSAIDs and steroids, as well as emerging antidepressant and painkiller formulations designed to offer comprehensive relief and improve patient quality of life.

Sciatica Industry Market Size (In Billion)

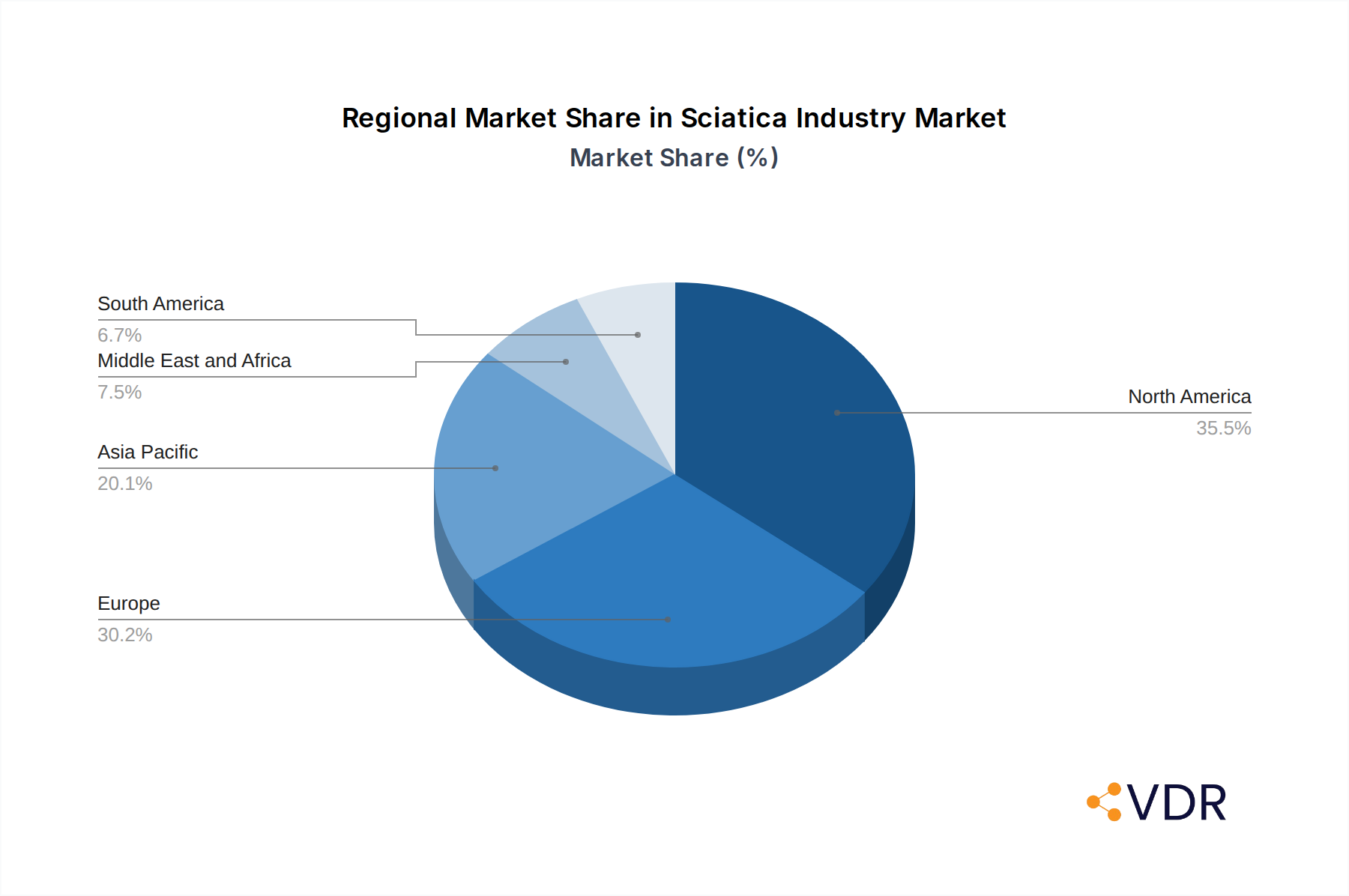

The competitive landscape features a mix of established pharmaceutical giants and innovative biotechnology firms, including Scilex Holding, Eliem Therapeutics, and SpineThera, who are actively engaged in research and development of new therapeutic options. Geographical trends indicate North America and Europe as dominant regions, driven by advanced healthcare infrastructure and high healthcare expenditure. However, the Asia Pacific region is expected to witness the fastest growth due to a burgeoning patient pool and improving healthcare access. Restraints, such as the potential side effects of long-term medication use and the high cost of some advanced treatments, are being addressed through the development of safer and more cost-effective alternatives. The increasing focus on minimally invasive procedures and personalized treatment plans will further shape the market's trajectory, ensuring continued innovation and accessibility for a growing number of patients.

Sciatica Industry Company Market Share

This comprehensive report provides an in-depth analysis of the global Sciatica industry, covering market dynamics, growth trends, regional dominance, product landscape, key players, and future opportunities. With a study period from 2019 to 2033, and a base year of 2025, this report offers critical insights for industry professionals seeking to understand the evolution of sciatica treatment and management. The market is segmented by type (Acute Sciatica, Chronic Sciatica, Other Types) and pharmacological therapies (NSAIDs, Steroids, Antidepressants, Painkillers, Other Pharmacological Therapies). We project the global sciatica market to reach USD 25.5 billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of 6.2% during the forecast period.

Sciatica Industry Market Dynamics & Structure

The Sciatica industry is characterized by a moderately concentrated market, driven by significant technological innovation in drug development and minimally invasive treatment procedures. Regulatory frameworks, particularly stringent FDA and EMA approvals, significantly influence market entry and product lifecycles. Competitive product substitutes, including physical therapy and surgical interventions, exert pressure on pharmacological solutions. End-user demographics are shifting, with an aging global population and increased prevalence of sedentary lifestyles contributing to higher incidences of sciatica. Merger and acquisition (M&A) trends indicate a strategic consolidation among key players aiming to broaden their product portfolios and geographical reach. For instance, recent M&A activities in the pain management sector are indirectly impacting the sciatica market.

- Market Concentration: Dominated by a few key pharmaceutical giants and specialized biotechnology firms, with increasing fragmentation due to new entrants focusing on novel therapies.

- Technological Innovation Drivers: Advancements in targeted drug delivery systems, regenerative medicine, and non-opioid pain management solutions are paramount.

- Regulatory Frameworks: Strict clinical trial requirements and post-market surveillance for pain therapeutics shape product development and market access.

- Competitive Product Substitutes: Non-pharmacological treatments like physiotherapy, chiropractic care, and surgical interventions represent significant competition.

- End-User Demographics: Growing prevalence due to aging populations, obesity, and increased screen time.

- M&A Trends: Strategic acquisitions by larger pharmaceutical companies to acquire innovative pain management pipelines and synergistic technologies.

Sciatica Industry Growth Trends & Insights

The Sciatica industry is poised for substantial growth, driven by an increasing global prevalence of lower back pain and radiculopathy, conditions that commonly manifest as sciatica. Market size evolution is directly correlated with the aging demographic and the rising incidence of lifestyle-related ailments such as obesity and degenerative disc diseases. Adoption rates for advanced pharmacological treatments are steadily increasing, propelled by the demand for more effective and targeted pain relief. Technological disruptions, including the development of novel drug delivery systems and the exploration of biologic therapies, are reshaping the treatment landscape. Consumer behavior shifts are evident, with patients actively seeking less invasive and more sustainable pain management options, moving away from a reliance on opioid painkillers.

The market is expected to grow from an estimated USD 13.8 billion in 2025 to USD 25.5 billion by 2033. This expansion is underpinned by a projected CAGR of 6.2% during the forecast period (2025-2033). The market penetration of novel therapies, particularly those with improved efficacy and reduced side effects, is a key growth indicator. For example, the recent positive Phase III trial results for SP-102 (SEMDEXA) by Scilex Holding, demonstrating sustained pain relief for up to 12 weeks, signify a potential paradigm shift. The FDA's Fast Track designation for SP-102 further underscores the industry's commitment to addressing unmet needs in sciatica treatment. The prevalence of chronic sciatica, accounting for an estimated 70% of the market, continues to be a significant driver, demanding long-term management solutions. The demand for non-steroidal anti-inflammatory drugs (NSAIDs) and steroids remains high, forming a substantial portion of the current market revenue, estimated at USD 5.2 billion and USD 3.1 billion respectively in 2025.

Dominant Regions, Countries, or Segments in Sciatica Industry

North America currently dominates the Sciatica industry, driven by a robust healthcare infrastructure, high disposable incomes, and a high prevalence of chronic pain conditions. The United States, in particular, is a leading market due to advanced research and development capabilities, significant healthcare expenditure, and a strong regulatory environment that fosters innovation. The dominant segment within the industry is Chronic Sciatica, accounting for an estimated 70% of the total market value in 2025, valued at USD 9.66 billion. This dominance is attributed to the persistent nature of chronic pain, necessitating long-term treatment strategies and a continuous demand for effective therapies.

Among pharmacological therapies, Non-steroidal Anti-inflammatory Drugs (NSAIDs) represent the largest segment, estimated at USD 5.2 billion in 2025. Their widespread availability, affordability, and established efficacy in managing mild to moderate pain contribute to their market leadership. However, the growth potential for Steroids, estimated at USD 3.1 billion in 2025, is significant, especially with advancements in localized delivery methods for targeted pain relief and reduced systemic side effects. The "Other Pharmacological Therapies" segment, encompassing newer drug classes and emerging treatments, is expected to witness the highest CAGR, driven by ongoing research and development.

- Dominant Region: North America (particularly the United States)

- Drivers: High healthcare spending, advanced R&D, strong regulatory support, and high prevalence of lifestyle-related chronic conditions.

- Dominant Segment (Type): Chronic Sciatica

- Market Share (2025): Approximately 70%

- Drivers: Long-term treatment needs, persistent pain, and increasing incidence due to aging populations and lifestyle factors.

- Dominant Segment (Therapy): Non-steroidal Anti-inflammatory Drugs (NSAIDs)

- Market Share (2025): Approximately 37.7%

- Drivers: Accessibility, affordability, established efficacy for moderate pain, and broad prescription rates.

- High Growth Potential Segment (Therapy): Steroids (due to targeted delivery innovations)

- Market Share (2025): Approximately 22.5%

- Drivers: Improved localized administration techniques, enhanced efficacy in reducing inflammation, and growing preference for non-opioid alternatives.

Sciatica Industry Product Landscape

The sciatica industry's product landscape is evolving with a focus on enhanced efficacy, reduced side effects, and improved patient compliance. Innovations in drug delivery systems, such as long-acting injectable formulations and targeted topical applications, are gaining prominence. For instance, Scilex Holding's SP-102 (SEMDEXA), an injectable dexamethasone sodium phosphate viscous gel, represents a significant advancement in localized, non-opioid pain management, demonstrating sustained pain relief in clinical trials. The performance metrics are increasingly gauged by the duration and intensity of pain reduction, alongside the incidence of adverse events. Unique selling propositions now center on novel mechanisms of action that target inflammatory pathways more precisely, offering superior therapeutic outcomes compared to traditional pain management options.

Key Drivers, Barriers & Challenges in Sciatica Industry

Key Drivers: The primary forces propelling the Sciatica industry include a rising global prevalence of chronic pain conditions, particularly among aging populations and those with sedentary lifestyles. Technological advancements in pharmaceutical research and development, leading to more effective and targeted therapies, are significant drivers. The increasing demand for non-opioid pain management solutions, spurred by the opioid crisis, also fuels innovation and market growth. Favorable regulatory pathways, like the FDA's Fast Track designation, accelerate the approval and market entry of promising treatments.

Key Barriers & Challenges: Despite robust growth, the industry faces several challenges. Stringent and lengthy regulatory approval processes can hinder the market entry of new drugs. High research and development costs associated with novel drug discovery and clinical trials pose a significant financial barrier. The availability of established generic pain medications and the cost-sensitivity of healthcare systems can limit the adoption of premium-priced innovative therapies. Furthermore, the development of effective long-term treatments for chronic sciatica remains an ongoing challenge, alongside managing patient expectations and adherence to complex treatment regimens. Supply chain disruptions and geopolitical factors can also impact raw material availability and manufacturing costs.

Emerging Opportunities in Sciatica Industry

Emerging opportunities within the Sciatica industry are primarily centered on the development of novel, non-opioid therapeutic agents with improved efficacy and safety profiles. The growing interest in regenerative medicine and biologic therapies for nerve repair and inflammation reduction presents a significant untapped market. Personalized medicine approaches, tailoring treatments based on individual genetic predispositions and pain mechanisms, are also an area of immense potential. Furthermore, the expansion of telehealth and remote patient monitoring services offers new avenues for managing chronic sciatica patients, improving access to care and treatment adherence, especially in underserved regions. The global expansion into emerging markets with increasing healthcare awareness and spending also presents a substantial growth avenue.

Growth Accelerators in the Sciatica Industry Industry

Several key catalysts are accelerating long-term growth in the Sciatica industry. Technological breakthroughs in understanding the neurobiology of pain are paving the way for the development of highly targeted therapies. Strategic partnerships between pharmaceutical giants and innovative biotechnology firms are crucial for leveraging specialized expertise and accelerating pipeline development. Market expansion strategies, including penetration into emerging economies and the development of patient-centric delivery models, are vital for sustained growth. The increasing focus on value-based healthcare and outcomes research is also encouraging the development of therapies that demonstrate clear clinical and economic benefits, further accelerating adoption and market expansion.

Key Players Shaping the Sciatica Industry Market

- Scilex Holding

- Eliem Therapeutics

- Vita Sciences

- Kolon Life Science

- SpineThera

- Aurobindo Pharma

- Seikagaku Corporation

- Sorrento Therapeutics

- Sinfonia Biotherapeutics

Notable Milestones in Sciatica Industry Sector

- March 2022: Scilex Holding Company, a majority-owned subsidiary of Sorrento Therapeutics, Inc., announced the final results for SP-102 (SEMDEXA) efficacy and safety from its pivotal Phase III clinical trial program for Sciatica pain management. SP-102 (SEMDEXA) demonstrated pain relief that continued through 12 weeks.

- December 2021: The United States Food and Drug Administration (FDA) granted Fast Track designation to SP-102 (injectable dexamethasone sodium phosphate viscous gel) for the treatment of lumbosacral radicular pain or sciatica.

In-Depth Sciatica Industry Market Outlook

The future outlook for the Sciatica industry is exceptionally promising, driven by a confluence of factors that will significantly accelerate market growth. The ongoing shift away from opioid analgesics towards safer, more effective alternatives will continue to fuel demand for innovative non-opioid therapies. Advances in drug formulation and delivery systems, enabling precise targeting of inflamed tissues and sustained pain relief, will be key differentiators. The increasing global burden of chronic pain, compounded by an aging population and lifestyle-related health issues, ensures a sustained and growing patient pool. Strategic collaborations and investments in R&D, particularly in areas like regenerative medicine and novel molecular targets, are expected to yield groundbreaking treatments. The expanding healthcare infrastructure in emerging economies also presents significant untapped potential for market penetration.

Sciatica Industry Segmentation

-

1. Type

- 1.1. Acute Sciatica

- 1.2. Chronic Sciatica

- 1.3. Other Types

-

2. Pharmacological Therapies

- 2.1. Non-steroidal Anti-inflammatory Drug (NSAIDs)

- 2.2. Steroids

- 2.3. Antidepressants

- 2.4. Painkillers

- 2.5. Other Pharmacological Therapies

Sciatica Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Sciatica Industry Regional Market Share

Geographic Coverage of Sciatica Industry

Sciatica Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Acute Sciatica

- 5.1.2. Chronic Sciatica

- 5.1.3. Other Types

- 5.2. Market Analysis, Insights and Forecast - by Pharmacological Therapies

- 5.2.1. Non-steroidal Anti-inflammatory Drug (NSAIDs)

- 5.2.2. Steroids

- 5.2.3. Antidepressants

- 5.2.4. Painkillers

- 5.2.5. Other Pharmacological Therapies

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Sciatica Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Acute Sciatica

- 6.1.2. Chronic Sciatica

- 6.1.3. Other Types

- 6.2. Market Analysis, Insights and Forecast - by Pharmacological Therapies

- 6.2.1. Non-steroidal Anti-inflammatory Drug (NSAIDs)

- 6.2.2. Steroids

- 6.2.3. Antidepressants

- 6.2.4. Painkillers

- 6.2.5. Other Pharmacological Therapies

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Sciatica Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Acute Sciatica

- 7.1.2. Chronic Sciatica

- 7.1.3. Other Types

- 7.2. Market Analysis, Insights and Forecast - by Pharmacological Therapies

- 7.2.1. Non-steroidal Anti-inflammatory Drug (NSAIDs)

- 7.2.2. Steroids

- 7.2.3. Antidepressants

- 7.2.4. Painkillers

- 7.2.5. Other Pharmacological Therapies

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Sciatica Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Acute Sciatica

- 8.1.2. Chronic Sciatica

- 8.1.3. Other Types

- 8.2. Market Analysis, Insights and Forecast - by Pharmacological Therapies

- 8.2.1. Non-steroidal Anti-inflammatory Drug (NSAIDs)

- 8.2.2. Steroids

- 8.2.3. Antidepressants

- 8.2.4. Painkillers

- 8.2.5. Other Pharmacological Therapies

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific Sciatica Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Acute Sciatica

- 9.1.2. Chronic Sciatica

- 9.1.3. Other Types

- 9.2. Market Analysis, Insights and Forecast - by Pharmacological Therapies

- 9.2.1. Non-steroidal Anti-inflammatory Drug (NSAIDs)

- 9.2.2. Steroids

- 9.2.3. Antidepressants

- 9.2.4. Painkillers

- 9.2.5. Other Pharmacological Therapies

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Middle East and Africa Sciatica Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Acute Sciatica

- 10.1.2. Chronic Sciatica

- 10.1.3. Other Types

- 10.2. Market Analysis, Insights and Forecast - by Pharmacological Therapies

- 10.2.1. Non-steroidal Anti-inflammatory Drug (NSAIDs)

- 10.2.2. Steroids

- 10.2.3. Antidepressants

- 10.2.4. Painkillers

- 10.2.5. Other Pharmacological Therapies

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. South America Sciatica Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Acute Sciatica

- 11.1.2. Chronic Sciatica

- 11.1.3. Other Types

- 11.2. Market Analysis, Insights and Forecast - by Pharmacological Therapies

- 11.2.1. Non-steroidal Anti-inflammatory Drug (NSAIDs)

- 11.2.2. Steroids

- 11.2.3. Antidepressants

- 11.2.4. Painkillers

- 11.2.5. Other Pharmacological Therapies

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Scilex Holding

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Eliem Therapeutics

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Vita Sciences

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Kolon life Science

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 SpineThera

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Aurobindo Pharma

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Seikagaku Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Sorrento Therapeutics

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Sinfonia Biotherapeutics

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.1 Scilex Holding

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Sciatica Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Sciatica Industry Revenue (billion), by Type 2025 & 2033

- Figure 3: North America Sciatica Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Sciatica Industry Revenue (billion), by Pharmacological Therapies 2025 & 2033

- Figure 5: North America Sciatica Industry Revenue Share (%), by Pharmacological Therapies 2025 & 2033

- Figure 6: North America Sciatica Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Sciatica Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Sciatica Industry Revenue (billion), by Type 2025 & 2033

- Figure 9: Europe Sciatica Industry Revenue Share (%), by Type 2025 & 2033

- Figure 10: Europe Sciatica Industry Revenue (billion), by Pharmacological Therapies 2025 & 2033

- Figure 11: Europe Sciatica Industry Revenue Share (%), by Pharmacological Therapies 2025 & 2033

- Figure 12: Europe Sciatica Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Sciatica Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Sciatica Industry Revenue (billion), by Type 2025 & 2033

- Figure 15: Asia Pacific Sciatica Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Asia Pacific Sciatica Industry Revenue (billion), by Pharmacological Therapies 2025 & 2033

- Figure 17: Asia Pacific Sciatica Industry Revenue Share (%), by Pharmacological Therapies 2025 & 2033

- Figure 18: Asia Pacific Sciatica Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific Sciatica Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East and Africa Sciatica Industry Revenue (billion), by Type 2025 & 2033

- Figure 21: Middle East and Africa Sciatica Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: Middle East and Africa Sciatica Industry Revenue (billion), by Pharmacological Therapies 2025 & 2033

- Figure 23: Middle East and Africa Sciatica Industry Revenue Share (%), by Pharmacological Therapies 2025 & 2033

- Figure 24: Middle East and Africa Sciatica Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East and Africa Sciatica Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Sciatica Industry Revenue (billion), by Type 2025 & 2033

- Figure 27: South America Sciatica Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: South America Sciatica Industry Revenue (billion), by Pharmacological Therapies 2025 & 2033

- Figure 29: South America Sciatica Industry Revenue Share (%), by Pharmacological Therapies 2025 & 2033

- Figure 30: South America Sciatica Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: South America Sciatica Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Sciatica Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global Sciatica Industry Revenue billion Forecast, by Pharmacological Therapies 2020 & 2033

- Table 3: Global Sciatica Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Sciatica Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 5: Global Sciatica Industry Revenue billion Forecast, by Pharmacological Therapies 2020 & 2033

- Table 6: Global Sciatica Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Sciatica Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Sciatica Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Sciatica Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Sciatica Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 11: Global Sciatica Industry Revenue billion Forecast, by Pharmacological Therapies 2020 & 2033

- Table 12: Global Sciatica Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Germany Sciatica Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United Kingdom Sciatica Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: France Sciatica Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Italy Sciatica Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Spain Sciatica Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Rest of Europe Sciatica Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Global Sciatica Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 20: Global Sciatica Industry Revenue billion Forecast, by Pharmacological Therapies 2020 & 2033

- Table 21: Global Sciatica Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 22: China Sciatica Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Japan Sciatica Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: India Sciatica Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Australia Sciatica Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: South Korea Sciatica Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Asia Pacific Sciatica Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Sciatica Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 29: Global Sciatica Industry Revenue billion Forecast, by Pharmacological Therapies 2020 & 2033

- Table 30: Global Sciatica Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 31: GCC Sciatica Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: South Africa Sciatica Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: Rest of Middle East and Africa Sciatica Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Global Sciatica Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 35: Global Sciatica Industry Revenue billion Forecast, by Pharmacological Therapies 2020 & 2033

- Table 36: Global Sciatica Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 37: Brazil Sciatica Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Argentina Sciatica Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: Rest of South America Sciatica Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Sciatica Industry?

The projected CAGR is approximately 6.5%.

2. Which companies are prominent players in the Sciatica Industry?

Key companies in the market include Scilex Holding, Eliem Therapeutics, Vita Sciences, Kolon life Science, SpineThera, Aurobindo Pharma, Seikagaku Corporation, Sorrento Therapeutics, Sinfonia Biotherapeutics.

3. What are the main segments of the Sciatica Industry?

The market segments include Type, Pharmacological Therapies.

4. Can you provide details about the market size?

The market size is estimated to be USD 7.28 billion as of 2022.

5. What are some drivers contributing to market growth?

Increased Public Awareness and High Survival Rate of Sciatica; Risk Factors and Increasing Elderly Population.

6. What are the notable trends driving market growth?

The Non-Steroidal Anti Inflammatory Drug Segment is Expected to Witness a Strong Growth.

7. Are there any restraints impacting market growth?

No Single or Definitive Diagnostic Criteria Available; Several Off-Label Drugs and Physical Therapy In Market.

8. Can you provide examples of recent developments in the market?

In March 2022, Scilex Holding Company, a majority-owned subsidiary of Sorrento Therapeutics, Inc., announced the final results for SP-102 (SEMDEXA) efficacy and safety from its pivotal Phase III clinical trial program for Sciatica pain management. SP-102 (SEMDEXA) demonstrated pain relief that continued through 12 weeks.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Sciatica Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Sciatica Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Sciatica Industry?

To stay informed about further developments, trends, and reports in the Sciatica Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence