Key Insights

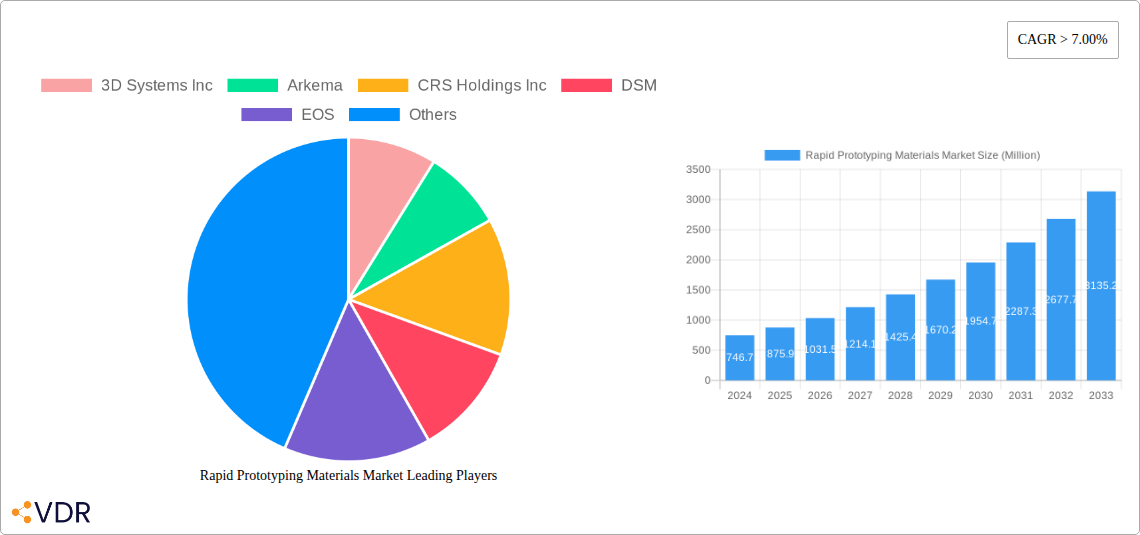

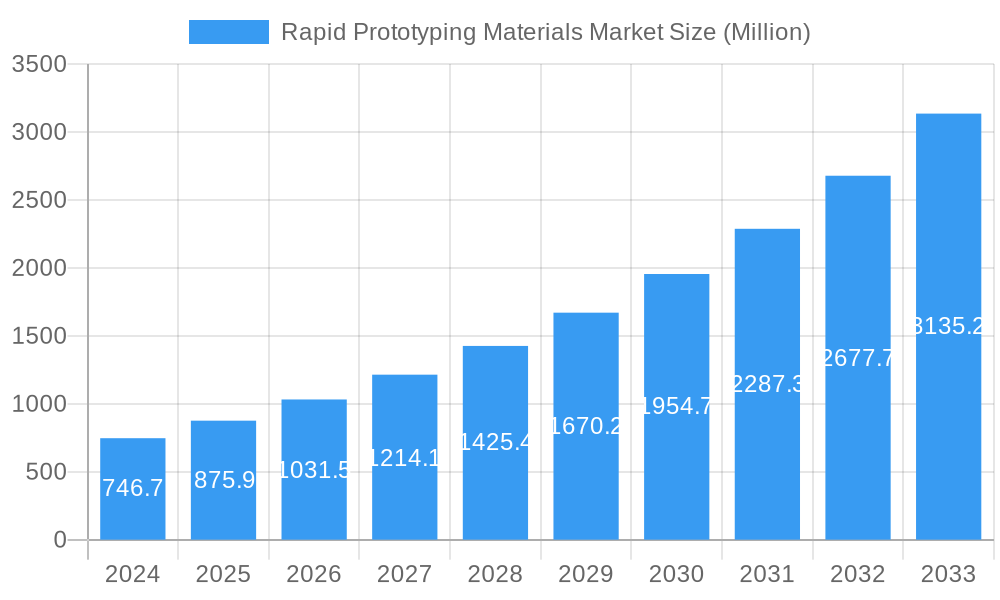

The global Rapid Prototyping Materials Market is poised for significant expansion, projected to reach USD 746.7 million in 2024 and grow at a robust CAGR of 18.1% through 2033. This substantial growth is fueled by the increasing adoption of additive manufacturing across diverse industries, driven by the demand for faster product development cycles, cost-effectiveness, and enhanced design flexibility. Key sectors like automotive and aerospace are leading the charge, leveraging rapid prototyping to create intricate components and validate designs with unprecedented speed. The medical industry is also a strong contributor, utilizing advanced materials for patient-specific implants and surgical guides. Furthermore, the burgeoning electronics sector is increasingly relying on rapid prototyping for circuit board development and custom device casings. The market is characterized by a dynamic interplay of material innovation, with advancements in ceramics, metals, and advanced plastics offering tailored solutions for specific application needs.

Rapid Prototyping Materials Market Market Size (In Million)

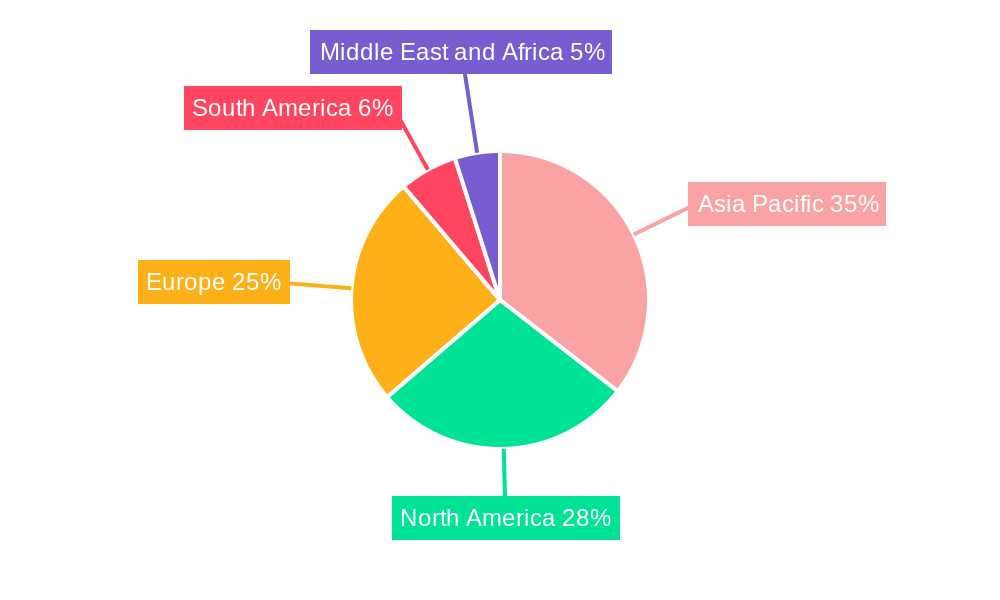

The rapid prototyping materials market is a vibrant landscape characterized by continuous innovation and strategic collaborations among key players such as 3D Systems Inc., EOS, and General Electric. The market's trajectory is further shaped by emerging trends like the development of sustainable and bio-compatible prototyping materials, catering to a growing environmental consciousness and specialized medical applications. While the market presents immense opportunities, certain restraints, such as the initial high cost of advanced prototyping equipment and the need for specialized expertise in material selection and process optimization, may present localized challenges. However, the overarching benefits of accelerated innovation, reduced lead times, and the ability to produce complex geometries are powerful drivers that are expected to overcome these hurdles. Regional dynamics highlight Asia Pacific's dominant position, driven by rapid industrialization and a strong manufacturing base, followed closely by North America and Europe, both with established advanced manufacturing ecosystems.

Rapid Prototyping Materials Market Company Market Share

Here's a compelling, SEO-optimized report description for the Rapid Prototyping Materials Market, incorporating your specific requirements:

Rapid Prototyping Materials Market: Comprehensive 2024-2033 Analysis & Forecast

Unlock critical insights into the Rapid Prototyping Materials Market, a dynamic sector experiencing explosive growth driven by advanced manufacturing and on-demand production. This in-depth report, spanning the Historical Period (2019-2024) and extending to the Forecast Period (2025-2033) with a Base Year and Estimated Year of 2025, provides an indispensable resource for stakeholders seeking to navigate this evolving landscape. Discover the latest trends, key drivers, and emerging opportunities within 3D printing materials, additive manufacturing consumables, and advanced prototyping solutions.

This report meticulously analyzes the Rapid Prototyping Materials Market across key segments, including Plastics, Metals and Alloys, Ceramics, and Other Types. We dissect its influence on critical End-user Industries such as Automotive, Aerospace and Defense, Medical, Electronics, Construction, and others. With a keen focus on market share, CAGR, and market penetration, this research equips you with the data-driven intelligence necessary for strategic decision-making. Explore the competitive intelligence surrounding key players like 3D Systems Inc, Arkema, CRS Holdings Inc, DSM, EOS, GENERAL ELECTRIC, Höganäs AB, Oxford Performance Materials, Renishaw plc, and Sandvik AB. Dive into the parent and child market dynamics and understand the intricate web of innovation, regulation, and demand shaping the future of rapid prototyping.

Rapid Prototyping Materials Market Market Dynamics & Structure

The Rapid Prototyping Materials Market exhibits a moderately concentrated structure, characterized by the presence of both established global players and agile niche innovators. Technological innovation is the primary engine, with ongoing advancements in material science leading to the development of enhanced 3D printing filaments, resins, powders, and pastes offering superior mechanical properties, thermal resistance, and biocompatibility. Regulatory frameworks, particularly in the Medical and Aerospace and Defense sectors, are increasingly stringent, driving demand for certified and traceable materials, thereby creating barriers for new entrants without robust quality control systems. Competitive product substitutes, while present in the form of traditional manufacturing methods, are rapidly losing ground to the speed, cost-efficiency, and design freedom offered by additive manufacturing. End-user demographics are shifting towards a greater adoption of rapid prototyping for both functional prototyping and end-use part production, particularly within the Automotive and Electronics industries. Merger and acquisition (M&A) trends are noticeable, with larger chemical companies acquiring specialized material providers to expand their additive manufacturing portfolios, signaling consolidation and strategic expansion. The market share of the top 5 players is estimated to be around 45-55%, with significant ongoing M&A deal volumes aimed at acquiring innovative technologies and expanding market reach. Innovation barriers include the high cost of R&D for novel materials and the need for extensive testing and certification processes.

- Market Concentration: Moderately concentrated, with a blend of large conglomerates and specialized firms.

- Technological Innovation Drivers: Development of high-performance, multi-functional materials; advancements in material formulation for specific additive manufacturing processes.

- Regulatory Frameworks: Increasing stringency in sectors like healthcare and aerospace, influencing material selection and certification requirements.

- Competitive Product Substitutes: Traditional manufacturing methods are being challenged by the speed and flexibility of rapid prototyping.

- End-user Demographics: Growing demand for rapid prototyping in functional applications and end-use part production.

- M&A Trends: Strategic acquisitions by larger entities to enhance additive manufacturing capabilities and product offerings.

- Estimated Top 5 Player Market Share: 45-55%.

Rapid Prototyping Materials Market Growth Trends & Insights

The Rapid Prototyping Materials Market is poised for robust expansion, driven by a confluence of accelerating technological advancements and a fundamental shift in manufacturing paradigms. The market size, which was valued at approximately $12,500 million units in the base year of 2025, is projected to witness a Compound Annual Growth Rate (CAGR) of 18.5% through the forecast period of 2025-2033. This substantial growth is fueled by increasing adoption rates across a wider spectrum of industries, moving beyond traditional R&D applications to encompass serial production and mass customization. Technological disruptions, such as the development of multi-material printing capabilities and the integration of artificial intelligence in material design, are significantly enhancing the utility and application range of rapid prototyping. Consumer behavior is also evolving, with a growing demand for personalized products and faster product development cycles, directly benefiting the agile nature of additive manufacturing. The market penetration of advanced prototyping solutions is expected to surge, particularly in emerging economies as infrastructure and awareness surrounding these technologies improve. This evolution signifies a move towards a more decentralized and on-demand manufacturing ecosystem. The increasing accessibility of industrial-grade 3D printers and a wider variety of high-performance 3D printing materials further democratize the technology, enabling small and medium-sized enterprises (SMEs) to innovate and compete. The cost-effectiveness of producing complex geometries and reducing tooling expenses also contributes to the accelerated adoption. Furthermore, the push for sustainability in manufacturing is driving interest in materials that can be recycled or produced with a lower environmental footprint, aligning with the principles of additive manufacturing. The overall market trajectory indicates a sustained period of high growth, driven by continuous innovation and expanding industrial applications.

- Market Size (2025): $12,500 million units

- Projected CAGR (2025-2033): 18.5%

- Key Growth Drivers: Increasing adoption in serial production, advancements in material science, demand for mass customization, evolving consumer preferences.

- Technological Disruptions: Multi-material printing, AI-driven material design, improved printer capabilities.

- Market Penetration: Expected surge, especially in developing regions.

- Cost-Effectiveness: Reduced tooling costs and ability to produce complex geometries.

- Sustainability Focus: Growing demand for eco-friendly and recyclable 3D printing materials.

Dominant Regions, Countries, or Segments in Rapid Prototyping Materials Market

North America, spearheaded by the United States, is currently the most dominant region in the Rapid Prototyping Materials Market, driven by its advanced industrial base, strong R&D investment, and a high concentration of leading companies in sectors like Aerospace and Defense and Medical. The region's robust ecosystem of universities, research institutions, and private companies fosters a continuous stream of innovation in 3D printing materials and processes. The Automotive industry in North America is also a significant driver, with major car manufacturers leveraging rapid prototyping for everything from concept validation to the production of customized parts. The strong economic policies and substantial government funding for advanced manufacturing initiatives further bolster its leadership position.

Within the Material Type segment, Plastics currently hold the largest market share, estimated at over 50% of the total market value in 2025. This dominance is attributed to the versatility, cost-effectiveness, and wide range of available 3D printing plastics, including ABS, PLA, PETG, and high-performance engineering plastics like PEEK. These materials are extensively used across various End-user Industries for their lightweight properties, design flexibility, and suitability for both functional prototypes and end-use parts.

In terms of End-user Industry, the Aerospace and Defense sector commands a significant share, estimated at around 25% in 2025. This is due to the stringent requirements for lightweight, high-strength components, the need for rapid iteration in design and testing of complex aerospace parts, and the growing adoption of additive manufacturing for producing critical flight components. The Medical sector, accounting for an estimated 20% market share in 2025, is another major growth engine, propelled by the demand for custom implants, prosthetics, surgical guides, and patient-specific anatomical models.

- Dominant Region: North America (primarily the United States).

- Key Drivers: Strong industrial base, high R&D investment, leading companies in Aerospace & Defense and Medical.

- Market Share (Regional): Estimated to hold over 35% of the global market in 2025.

- Dominant Material Type: Plastics.

- Key Drivers: Versatility, cost-effectiveness, wide range of available materials (ABS, PLA, PETG, PEEK), extensive applications.

- Market Share (Material Type): Over 50% in 2025.

- Dominant End-user Industry: Aerospace and Defense.

- Key Drivers: Demand for lightweight, high-strength components; rapid iteration in design; use for critical flight parts.

- Market Share (End-user Industry): Approximately 25% in 2025.

- Significant End-user Industry: Medical.

- Key Drivers: Custom implants, prosthetics, surgical guides, patient-specific models.

- Market Share (End-user Industry): Approximately 20% in 2025.

Rapid Prototyping Materials Market Product Landscape

The Rapid Prototyping Materials Market product landscape is characterized by continuous innovation, offering a diverse range of materials engineered for specific additive manufacturing processes and applications. Innovations focus on enhancing mechanical properties such as tensile strength, impact resistance, and flexibility, as well as thermal stability and chemical resistance. Applications span from creating highly detailed visual prototypes and functional test parts to producing end-use components for demanding industries. Unique selling propositions often lie in the material's ability to mimic traditional manufacturing materials, its biocompatibility for medical devices, or its extreme durability for aerospace applications. Technological advancements include the development of advanced composite filaments reinforced with carbon fiber or glass fiber, high-temperature resistant polymers, and specialized metal alloys optimized for laser powder bed fusion and binder jetting.

Key Drivers, Barriers & Challenges in Rapid Prototyping Materials Market

Key Drivers: The Rapid Prototyping Materials Market is propelled by several key factors. Technological innovation, particularly in the development of novel 3D printing materials with enhanced performance characteristics, is a primary driver. The growing demand for mass customization and on-demand manufacturing across industries like Automotive and Medical fuels adoption. Increasing cost-effectiveness of additive manufacturing processes and the reduced lead times for product development also significantly contribute to market growth. Furthermore, supportive government initiatives promoting advanced manufacturing further accelerate market expansion.

Barriers & Challenges: Despite its robust growth, the market faces certain barriers. High initial investment costs for industrial-grade 3D printers and specialized materials can be a restraint for smaller enterprises. The need for extensive material testing, certification, and standardization, especially in highly regulated industries like Aerospace and Defense, can slow down adoption. Supply chain complexities for certain advanced 3D printing materials and the limited availability of skilled personnel to operate and maintain these technologies also present challenges. Competitive pressures from established manufacturing methods, although diminishing, still exist.

- Key Drivers:

- Technological advancements in material science.

- Demand for mass customization and on-demand production.

- Cost-effectiveness and reduced lead times in product development.

- Supportive government policies for advanced manufacturing.

- Barriers & Challenges:

- High initial investment costs for equipment and materials.

- Stringent certification and standardization requirements.

- Supply chain complexities for specialized materials.

- Limited availability of skilled workforce.

- Continued competition from traditional manufacturing methods.

Emerging Opportunities in Rapid Prototyping Materials Market

Emerging opportunities within the Rapid Prototyping Materials Market are substantial and diverse. The increasing demand for sustainable and recyclable 3D printing materials presents a significant avenue for growth. Innovations in biomaterials for advanced medical applications, including tissue engineering and drug delivery systems, are rapidly expanding. The development of functional 3D printing materials that incorporate electronic or sensing capabilities opens up new frontiers in the Electronics industry for creating integrated circuits and smart devices. Furthermore, the growing trend of decentralized manufacturing and the rise of micro-factories create opportunities for localized production of highly customized parts, reducing logistics costs and lead times. The integration of AI and machine learning in material discovery and optimization is also poised to unlock new material possibilities.

Growth Accelerators in the Rapid Prototyping Materials Market Industry

Several factors act as significant growth accelerators for the Rapid Prototyping Materials Market. Continued breakthroughs in material science, leading to the creation of materials with superior mechanical, thermal, and chemical properties, are a primary catalyst. Strategic partnerships between material manufacturers, printer OEMs, and end-users are fostering co-development and market penetration. The expanding applications of rapid prototyping in high-growth sectors like personalized medicine, electric vehicles, and advanced aerospace components are driving demand. Market expansion strategies, including the development of localized supply chains and tailored material solutions for specific regional needs, are also contributing to sustained growth. The increasing investment by venture capital and private equity firms in additive manufacturing startups further fuels innovation and market expansion.

Key Players Shaping the Rapid Prototyping Materials Market Market

- 3D Systems Inc

- Arkema

- CRS Holdings Inc

- DSM

- EOS

- GENERAL ELECTRIC

- Höganäs AB

- Oxford Performance Materials

- Renishaw plc

- Sandvik AB

Notable Milestones in Rapid Prototyping Materials Market Sector

- 2023: Introduction of high-temperature resistant polymer filaments, enabling functional prototyping for demanding automotive applications.

- 2023: Launch of advanced metal powders optimized for binder jetting, improving cost-efficiency and scalability for metal additive manufacturing.

- 2024: Significant advancements in biocompatible resins for medical 3D printing, facilitating the production of intricate surgical instruments and implants.

- 2024: Development of composite materials with enhanced strength-to-weight ratios for aerospace applications, opening new avenues for part lightweighting.

- 2025: Release of new software platforms enabling AI-driven optimization of 3D printing materials for specific design requirements.

- 2025: Expansion of ceramic material offerings, broadening applications in tooling, heat exchangers, and other industrial components.

In-Depth Rapid Prototyping Materials Market Market Outlook

The outlook for the Rapid Prototyping Materials Market remains exceptionally strong, fueled by ongoing technological advancements and expanding industrial adoption. Key growth accelerators include the continuous development of high-performance and sustainable materials, robust strategic partnerships across the value chain, and the increasing penetration of additive manufacturing in high-value sectors. The market is expected to witness further innovation in functional materials, such as those with embedded electronics or self-healing properties. Market expansion will be driven by the growing demand for personalized products and the shift towards decentralized, on-demand manufacturing models. Strategic opportunities lie in catering to emerging applications in areas like sustainable packaging, advanced robotics, and next-generation electronics. The ongoing evolution of 3D printing materials is fundamental to unlocking the full potential of additive manufacturing, promising a future of unprecedented design freedom, rapid innovation, and efficient production.

Rapid Prototyping Materials Market Segmentation

-

1. Material Type

- 1.1. Ceramics

- 1.2. Metals and Alloys

- 1.3. Plastics

- 1.4. Other Types

-

2. End-user Industry

- 2.1. Automotive

- 2.2. Aerospace and Defense

- 2.3. Medical

- 2.4. Electronics

- 2.5. Construction

- 2.6. Other End-user Industries

Rapid Prototyping Materials Market Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. France

- 3.4. Italy

- 3.5. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. South Africa

- 5.3. Rest of Middle East and Africa

Rapid Prototyping Materials Market Regional Market Share

Geographic Coverage of Rapid Prototyping Materials Market

Rapid Prototyping Materials Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 18.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 5.1.1. Ceramics

- 5.1.2. Metals and Alloys

- 5.1.3. Plastics

- 5.1.4. Other Types

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Automotive

- 5.2.2. Aerospace and Defense

- 5.2.3. Medical

- 5.2.4. Electronics

- 5.2.5. Construction

- 5.2.6. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.3.2. North America

- 5.3.3. Europe

- 5.3.4. South America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 6. Global Rapid Prototyping Materials Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 6.1.1. Ceramics

- 6.1.2. Metals and Alloys

- 6.1.3. Plastics

- 6.1.4. Other Types

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Automotive

- 6.2.2. Aerospace and Defense

- 6.2.3. Medical

- 6.2.4. Electronics

- 6.2.5. Construction

- 6.2.6. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 7. Asia Pacific Rapid Prototyping Materials Market Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 7.1.1. Ceramics

- 7.1.2. Metals and Alloys

- 7.1.3. Plastics

- 7.1.4. Other Types

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Automotive

- 7.2.2. Aerospace and Defense

- 7.2.3. Medical

- 7.2.4. Electronics

- 7.2.5. Construction

- 7.2.6. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 8. North America Rapid Prototyping Materials Market Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 8.1.1. Ceramics

- 8.1.2. Metals and Alloys

- 8.1.3. Plastics

- 8.1.4. Other Types

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Automotive

- 8.2.2. Aerospace and Defense

- 8.2.3. Medical

- 8.2.4. Electronics

- 8.2.5. Construction

- 8.2.6. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 9. Europe Rapid Prototyping Materials Market Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 9.1.1. Ceramics

- 9.1.2. Metals and Alloys

- 9.1.3. Plastics

- 9.1.4. Other Types

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Automotive

- 9.2.2. Aerospace and Defense

- 9.2.3. Medical

- 9.2.4. Electronics

- 9.2.5. Construction

- 9.2.6. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 10. South America Rapid Prototyping Materials Market Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Material Type

- 10.1.1. Ceramics

- 10.1.2. Metals and Alloys

- 10.1.3. Plastics

- 10.1.4. Other Types

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. Automotive

- 10.2.2. Aerospace and Defense

- 10.2.3. Medical

- 10.2.4. Electronics

- 10.2.5. Construction

- 10.2.6. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Material Type

- 11. Middle East and Africa Rapid Prototyping Materials Market Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Material Type

- 11.1.1. Ceramics

- 11.1.2. Metals and Alloys

- 11.1.3. Plastics

- 11.1.4. Other Types

- 11.2. Market Analysis, Insights and Forecast - by End-user Industry

- 11.2.1. Automotive

- 11.2.2. Aerospace and Defense

- 11.2.3. Medical

- 11.2.4. Electronics

- 11.2.5. Construction

- 11.2.6. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Material Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 3D Systems Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Arkema

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 CRS Holdings Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 DSM

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 EOS

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 GENERAL ELECTRIC

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Höganäs AB

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Oxford Performance Materials

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Renishaw plc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Sandvik AB*List Not Exhaustive

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 3D Systems Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Rapid Prototyping Materials Market Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: Asia Pacific Rapid Prototyping Materials Market Revenue (million), by Material Type 2025 & 2033

- Figure 3: Asia Pacific Rapid Prototyping Materials Market Revenue Share (%), by Material Type 2025 & 2033

- Figure 4: Asia Pacific Rapid Prototyping Materials Market Revenue (million), by End-user Industry 2025 & 2033

- Figure 5: Asia Pacific Rapid Prototyping Materials Market Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 6: Asia Pacific Rapid Prototyping Materials Market Revenue (million), by Country 2025 & 2033

- Figure 7: Asia Pacific Rapid Prototyping Materials Market Revenue Share (%), by Country 2025 & 2033

- Figure 8: North America Rapid Prototyping Materials Market Revenue (million), by Material Type 2025 & 2033

- Figure 9: North America Rapid Prototyping Materials Market Revenue Share (%), by Material Type 2025 & 2033

- Figure 10: North America Rapid Prototyping Materials Market Revenue (million), by End-user Industry 2025 & 2033

- Figure 11: North America Rapid Prototyping Materials Market Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 12: North America Rapid Prototyping Materials Market Revenue (million), by Country 2025 & 2033

- Figure 13: North America Rapid Prototyping Materials Market Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Rapid Prototyping Materials Market Revenue (million), by Material Type 2025 & 2033

- Figure 15: Europe Rapid Prototyping Materials Market Revenue Share (%), by Material Type 2025 & 2033

- Figure 16: Europe Rapid Prototyping Materials Market Revenue (million), by End-user Industry 2025 & 2033

- Figure 17: Europe Rapid Prototyping Materials Market Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 18: Europe Rapid Prototyping Materials Market Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Rapid Prototyping Materials Market Revenue Share (%), by Country 2025 & 2033

- Figure 20: South America Rapid Prototyping Materials Market Revenue (million), by Material Type 2025 & 2033

- Figure 21: South America Rapid Prototyping Materials Market Revenue Share (%), by Material Type 2025 & 2033

- Figure 22: South America Rapid Prototyping Materials Market Revenue (million), by End-user Industry 2025 & 2033

- Figure 23: South America Rapid Prototyping Materials Market Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: South America Rapid Prototyping Materials Market Revenue (million), by Country 2025 & 2033

- Figure 25: South America Rapid Prototyping Materials Market Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Rapid Prototyping Materials Market Revenue (million), by Material Type 2025 & 2033

- Figure 27: Middle East and Africa Rapid Prototyping Materials Market Revenue Share (%), by Material Type 2025 & 2033

- Figure 28: Middle East and Africa Rapid Prototyping Materials Market Revenue (million), by End-user Industry 2025 & 2033

- Figure 29: Middle East and Africa Rapid Prototyping Materials Market Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 30: Middle East and Africa Rapid Prototyping Materials Market Revenue (million), by Country 2025 & 2033

- Figure 31: Middle East and Africa Rapid Prototyping Materials Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Rapid Prototyping Materials Market Revenue million Forecast, by Material Type 2020 & 2033

- Table 2: Global Rapid Prototyping Materials Market Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 3: Global Rapid Prototyping Materials Market Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Rapid Prototyping Materials Market Revenue million Forecast, by Material Type 2020 & 2033

- Table 5: Global Rapid Prototyping Materials Market Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 6: Global Rapid Prototyping Materials Market Revenue million Forecast, by Country 2020 & 2033

- Table 7: China Rapid Prototyping Materials Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: India Rapid Prototyping Materials Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Japan Rapid Prototyping Materials Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: South Korea Rapid Prototyping Materials Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 11: Rest of Asia Pacific Rapid Prototyping Materials Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 12: Global Rapid Prototyping Materials Market Revenue million Forecast, by Material Type 2020 & 2033

- Table 13: Global Rapid Prototyping Materials Market Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 14: Global Rapid Prototyping Materials Market Revenue million Forecast, by Country 2020 & 2033

- Table 15: United States Rapid Prototyping Materials Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Canada Rapid Prototyping Materials Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 17: Mexico Rapid Prototyping Materials Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 18: Global Rapid Prototyping Materials Market Revenue million Forecast, by Material Type 2020 & 2033

- Table 19: Global Rapid Prototyping Materials Market Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 20: Global Rapid Prototyping Materials Market Revenue million Forecast, by Country 2020 & 2033

- Table 21: Germany Rapid Prototyping Materials Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: United Kingdom Rapid Prototyping Materials Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: France Rapid Prototyping Materials Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Italy Rapid Prototyping Materials Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Rest of Europe Rapid Prototyping Materials Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Global Rapid Prototyping Materials Market Revenue million Forecast, by Material Type 2020 & 2033

- Table 27: Global Rapid Prototyping Materials Market Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 28: Global Rapid Prototyping Materials Market Revenue million Forecast, by Country 2020 & 2033

- Table 29: Brazil Rapid Prototyping Materials Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 30: Argentina Rapid Prototyping Materials Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 31: Rest of South America Rapid Prototyping Materials Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Global Rapid Prototyping Materials Market Revenue million Forecast, by Material Type 2020 & 2033

- Table 33: Global Rapid Prototyping Materials Market Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 34: Global Rapid Prototyping Materials Market Revenue million Forecast, by Country 2020 & 2033

- Table 35: Saudi Arabia Rapid Prototyping Materials Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: South Africa Rapid Prototyping Materials Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Rest of Middle East and Africa Rapid Prototyping Materials Market Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Rapid Prototyping Materials Market?

The projected CAGR is approximately 18.8%.

2. Which companies are prominent players in the Rapid Prototyping Materials Market?

Key companies in the market include 3D Systems Inc, Arkema, CRS Holdings Inc, DSM, EOS, GENERAL ELECTRIC, Höganäs AB, Oxford Performance Materials, Renishaw plc, Sandvik AB*List Not Exhaustive.

3. What are the main segments of the Rapid Prototyping Materials Market?

The market segments include Material Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 1250.08 million as of 2022.

5. What are some drivers contributing to market growth?

; Increasing Applications for the Medical Industry; Growing Demand from the Manufacturing Sector.

6. What are the notable trends driving market growth?

Growing Demand from the Manufacturing Sector.

7. Are there any restraints impacting market growth?

; Increasing Applications for the Medical Industry; Growing Demand from the Manufacturing Sector.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Rapid Prototyping Materials Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Rapid Prototyping Materials Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Rapid Prototyping Materials Market?

To stay informed about further developments, trends, and reports in the Rapid Prototyping Materials Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence