Key Insights

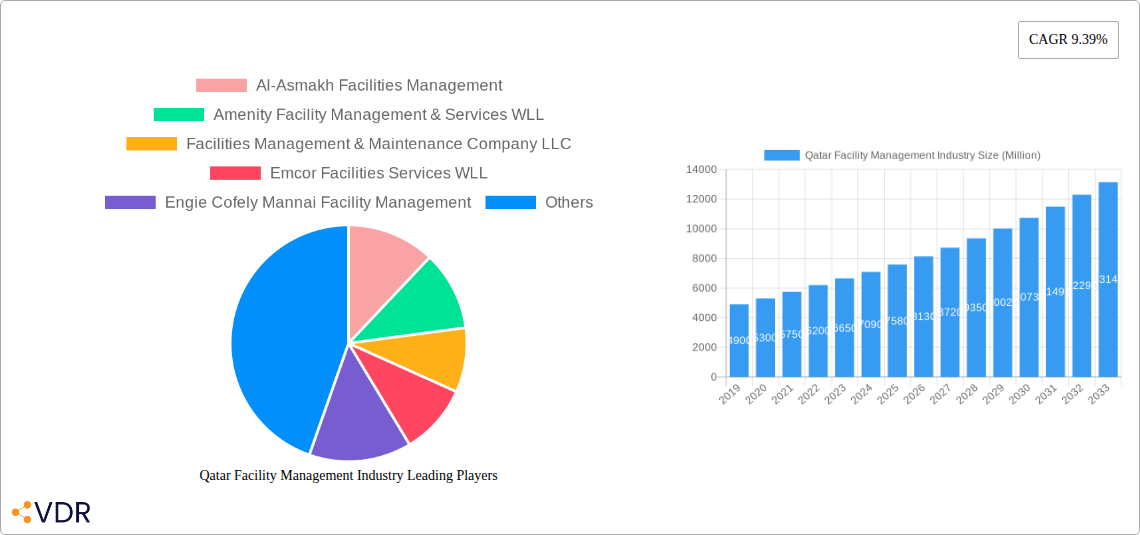

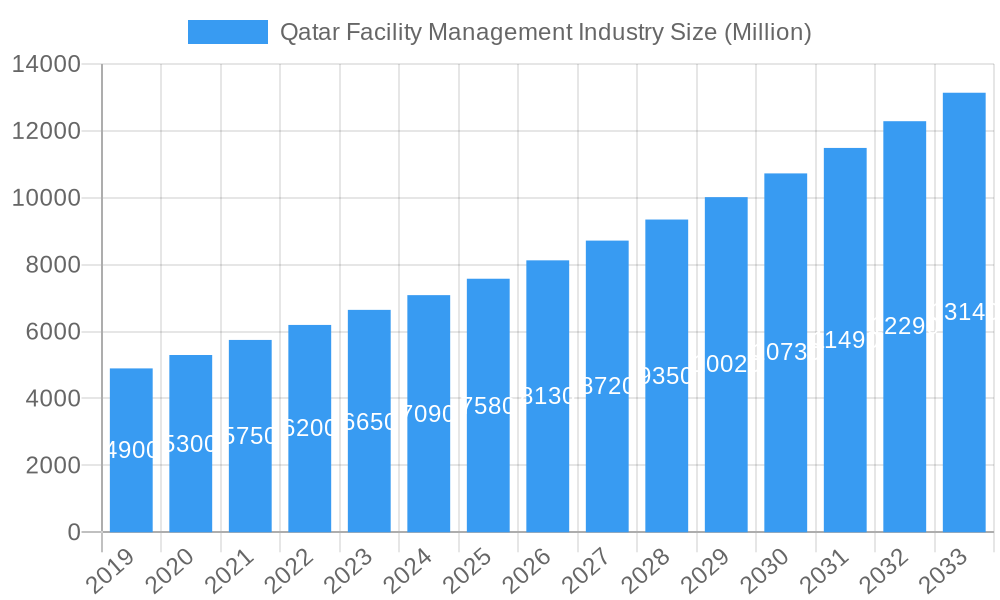

The Qatar Facility Management (FM) industry is poised for significant expansion, projected to reach a market size of approximately $7.58 million by 2025, growing at a robust Compound Annual Growth Rate (CAGR) of 9.39% through 2033. This dynamic growth is fueled by substantial investments in infrastructure development, particularly driven by the nation's vision for economic diversification and the hosting of major international events. The demand for comprehensive facility management services is escalating across commercial, institutional, and industrial sectors as organizations increasingly prioritize operational efficiency, cost optimization, and the creation of safe and sustainable working environments. The trend towards outsourcing facility management functions is a key driver, with businesses seeking specialized expertise and integrated solutions to manage complex building operations. This shift benefits both single and bundled FM service providers, as well as those offering integrated FM, indicating a maturing market that values holistic management approaches.

Qatar Facility Management Industry Market Size (In Billion)

The market segmentation reveals a strong demand for both Hard FM (technical services like maintenance and building systems) and Soft FM (non-technical services like cleaning and security). This dual demand underscores the comprehensive nature of modern facility management. Key players are actively expanding their service portfolios and geographical reach within Qatar to capture this growing market. While the market is robust, potential restraints might include the availability of skilled labor and the fluctuating costs of raw materials for maintenance. However, the strong government support for economic growth and the continuous influx of foreign investment are expected to outweigh these challenges, ensuring sustained growth and innovation in Qatar's facility management landscape. The increasing adoption of smart technologies and sustainable practices in facility management will further shape the industry's trajectory, making it an attractive sector for investment and development.

Qatar Facility Management Industry Company Market Share

Unlock the potential of Qatar's booming facility management sector with our in-depth industry report. This essential resource provides a critical overview of the market dynamics, growth trends, competitive landscape, and future outlook for facility management services in Qatar. Covering a study period from 2019 to 2033, with a base and estimated year of 2025, this report offers unparalleled insights for strategic decision-making. Delve into parent and child market segments, explore key industry developments, and understand the intricate web of players shaping this rapidly evolving sector.

Qatar Facility Management Industry Market Dynamics & Structure

The Qatar facility management industry is characterized by a moderately concentrated market, driven by significant government investment in infrastructure and the hosting of major international events. Technological innovation, particularly in areas like smart building management systems and AI-driven predictive maintenance, is a key differentiator. Regulatory frameworks are evolving to support sustainable and efficient facility operations, influencing service delivery models. While direct competitive product substitutes are limited, the increasing demand for specialized services creates niches for focused providers. End-user demographics are diverse, ranging from large-scale commercial and institutional clients to critical public infrastructure and burgeoning industrial sectors. Mergers and acquisitions (M&A) are becoming more prevalent as larger players seek to consolidate market share and expand service offerings.

- Market Concentration: A few key players hold a significant market share, but the fragmented nature of specialized services allows for niche providers to thrive.

- Technological Innovation: Adoption of IoT for real-time monitoring, energy management systems, and automated cleaning technologies are key drivers.

- Regulatory Frameworks: Growing emphasis on health, safety, and environmental compliance is shaping service standards and client expectations.

- Competitive Product Substitutes: While core FM services have few direct substitutes, digital transformation is creating new ways to deliver and manage facilities.

- End-User Demographics: Rapid urbanization and economic diversification are fueling demand across all end-user segments.

- M&A Trends: Consolidation is expected to increase as companies seek economies of scale and expanded capabilities, with an estimated 3-5 significant M&A deals anticipated within the forecast period.

Qatar Facility Management Industry Growth Trends & Insights

The Qatar facility management industry is poised for robust expansion, fueled by sustained economic development, significant infrastructure projects, and a growing awareness of the importance of integrated facility services. The market size is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 7.5% during the forecast period (2025-2033). Adoption rates for outsourced facility management are steadily increasing, driven by the desire for specialized expertise and cost optimization by businesses across all sectors. Technological disruptions, such as the integration of Building Information Modeling (BIM) for enhanced operational efficiency and the rise of sustainable facility management practices, are profoundly impacting service delivery. Consumer behavior shifts are evident, with a growing preference for holistic, tech-enabled, and eco-conscious facility solutions. The market penetration of advanced FM solutions is expected to rise from xx% in 2025 to xx% by 2033.

- Market Size Evolution: The total market size is projected to grow from an estimated $XXX Million in 2025 to $XXX Million by 2033.

- Adoption Rates: Outsourced FM services are expected to see a significant increase, driven by the growing complexity of modern facilities and the need for specialized skills.

- Technological Disruptions: AI-powered analytics for predictive maintenance and smart building technologies are transforming operational efficiency.

- Consumer Behavior Shifts: A heightened demand for green building certifications, energy efficiency, and occupant well-being is influencing service portfolios.

- CAGR: The industry is projected to grow at a CAGR of approximately 7.5% from 2025 to 2033.

- Market Penetration: Advanced FM solution penetration is estimated to grow from xx% to xx% over the forecast period.

Dominant Regions, Countries, or Segments in Qatar Facility Management Industry

Within the Qatar facility management industry, Outsourced Facility Management, particularly Integrated FM, stands out as a dominant segment driving market growth. This dominance is underpinned by the increasing complexity of large-scale projects and the strategic imperative for businesses to focus on core competencies, delegating facility operations to specialized providers. Commercial and Public/Infrastructure end-users are the primary beneficiaries and adopters of these integrated services. The surge in new commercial developments, mixed-use properties, and major public infrastructure projects, such as those associated with the World Cup legacy and ongoing urban expansion, necessitates comprehensive facility management solutions. Hard FM services, encompassing mechanical, electrical, and plumbing (MEP) maintenance, are crucial, but their integration with Soft FM services like cleaning, security, and catering under a single contract amplifies their market impact.

- Dominant Segment: Integrated Facility Management, offering a single point of accountability for a wide array of services.

- Key End Users: Commercial properties (offices, retail, hospitality) and Public/Infrastructure (airports, stadiums, transportation networks) are major demand drivers.

- Market Share: Integrated FM is estimated to capture xx% of the outsourced FM market by 2028.

- Growth Potential: Driven by large-scale construction projects and the need for operational efficiency in complex facilities.

- Hard FM Integration: Essential MEP services, when bundled, significantly enhance the value proposition of integrated FM contracts.

- Economic Policies: Government initiatives promoting foreign investment and business growth indirectly boost demand for high-quality facility management.

- Infrastructure Development: Ongoing and planned infrastructure projects are creating a sustained demand for ongoing FM services.

Qatar Facility Management Industry Product Landscape

The Qatar facility management industry's product landscape is evolving rapidly, with a strong emphasis on integrated technology solutions and sustainable practices. Innovations in Building Management Systems (BMS) and the adoption of IoT sensors are enabling predictive maintenance, optimizing energy consumption, and enhancing occupant comfort. AI-powered analytics are transforming operational efficiency, allowing for real-time data interpretation and proactive issue resolution. Unique selling propositions are increasingly tied to service customization, advanced reporting capabilities, and a proven track record in delivering energy-efficient and environmentally responsible facility management. Technological advancements are focused on creating smarter, safer, and more sustainable built environments, with a growing demand for green cleaning solutions and waste management technologies.

Key Drivers, Barriers & Challenges in Qatar Facility Management Industry

Key Drivers:

- Economic Diversification: Qatar's Vision 2030 initiative fuels infrastructure development and business expansion, creating sustained demand for FM services.

- Technological Advancements: Adoption of smart technologies, AI, and IoT for enhanced efficiency and predictive maintenance.

- Growing Real Estate Sector: Continuous development of commercial, residential, and hospitality properties.

- Focus on Sustainability: Increasing demand for eco-friendly and energy-efficient facility management solutions.

- Outsourcing Trend: Businesses increasingly opt for specialized FM providers to focus on core operations.

Barriers & Challenges:

- Skilled Labor Shortage: Difficulty in sourcing and retaining qualified FM professionals, impacting service quality and operational costs.

- Price Sensitivity: Clients, particularly in competitive sectors, may prioritize cost over comprehensive service offerings, leading to price wars.

- Regulatory Hurdles: Evolving regulations and compliance requirements can pose challenges for service providers.

- Supply Chain Disruptions: Potential for delays in procuring specialized equipment and materials, impacting project timelines.

- Intense Competition: A crowded market with both local and international players can lead to pressure on profit margins.

Emerging Opportunities in Qatar Facility Management Industry

Emerging opportunities in the Qatar facility management industry lie in the increasing demand for specialized services, particularly in the healthcare, education, and data center sectors. The development of smart cities and the growing emphasis on sustainable building practices are creating a significant need for green FM solutions, including energy management, waste reduction, and water conservation. Furthermore, the growth of the logistics and industrial sectors presents opportunities for integrated facility management tailored to specific operational needs. The rise of proptech (property technology) also opens avenues for innovative digital FM solutions, offering enhanced data analytics and remote management capabilities.

Growth Accelerators in the Qatar Facility Management Industry Industry

Several key catalysts are accelerating the growth of the Qatar facility management industry. Technological breakthroughs, such as the widespread adoption of AI for predictive maintenance and the integration of IoT for real-time building performance monitoring, are enhancing service efficiency and client value. Strategic partnerships between FM providers and technology companies are driving innovation and the development of bespoke solutions. Market expansion strategies, including diversification into niche service areas and geographical expansion within Qatar, are further fueling growth. The sustained government focus on infrastructure development and economic diversification provides a robust foundation for the industry's long-term expansion.

Key Players Shaping the Qatar Facility Management Industry Market

- Al-Asmakh Facilities Management

- Amenity Facility Management & Services WLL

- Facilities Management & Maintenance Company LLC

- Emcor Facilities Services WLL

- Engie Cofely Mannai Facility Management

- G4S QATAR SPC

- Al Faisal Holdings (MMG Qatar)

- Sodexo Qatar Services

- Como Facility Management Services

- EFS Facilities Services

Notable Milestones in Qatar Facility Management Industry Sector

- March 2022: EDGNEX, a subsidiary of Damac Group, operating in Qatar, partnered with JLL for its facility management needs as it pursues the first phase of its strategy to deliver data center facilities.

In-Depth Qatar Facility Management Industry Market Outlook

The Qatar facility management industry is set for sustained and significant growth, driven by a confluence of factors including robust economic diversification, ongoing infrastructure development, and a strong push towards sustainability. The increasing adoption of integrated FM services, coupled with technological advancements in smart building management and AI, will continue to be major growth accelerators. Emerging opportunities in specialized sectors like data centers and healthcare, alongside the growing demand for green FM solutions, offer substantial untapped market potential. Strategic partnerships and continued investment in skilled labor and innovative technologies will be crucial for companies to capitalize on the evolving landscape and secure a competitive advantage in this dynamic market.

Qatar Facility Management Industry Segmentation

-

1. Offering Type

- 1.1. Hard FM

- 1.2. Soft FM

-

2. Type

- 2.1. In-house Facility Management

-

2.2. Outsourced Facility Management

- 2.2.1. Single FM

- 2.2.2. Bundled FM

- 2.2.3. Integrated FM

-

3. End User

- 3.1. Commercial

- 3.2. Institutional

- 3.3. Public/Infrastructure

- 3.4. Industrial

- 3.5. Other End Users

Qatar Facility Management Industry Segmentation By Geography

- 1. Qatar

Qatar Facility Management Industry Regional Market Share

Geographic Coverage of Qatar Facility Management Industry

Qatar Facility Management Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.39% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Offering Type

- 5.1.1. Hard FM

- 5.1.2. Soft FM

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. In-house Facility Management

- 5.2.2. Outsourced Facility Management

- 5.2.2.1. Single FM

- 5.2.2.2. Bundled FM

- 5.2.2.3. Integrated FM

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Commercial

- 5.3.2. Institutional

- 5.3.3. Public/Infrastructure

- 5.3.4. Industrial

- 5.3.5. Other End Users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Qatar

- 5.1. Market Analysis, Insights and Forecast - by Offering Type

- 6. Qatar Facility Management Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Offering Type

- 6.1.1. Hard FM

- 6.1.2. Soft FM

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. In-house Facility Management

- 6.2.2. Outsourced Facility Management

- 6.2.2.1. Single FM

- 6.2.2.2. Bundled FM

- 6.2.2.3. Integrated FM

- 6.3. Market Analysis, Insights and Forecast - by End User

- 6.3.1. Commercial

- 6.3.2. Institutional

- 6.3.3. Public/Infrastructure

- 6.3.4. Industrial

- 6.3.5. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Offering Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Al-Asmakh Facilities Management

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Amenity Facility Management & Services WLL

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Facilities Management & Maintenance Company LLC

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Emcor Facilities Services WLL

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Engie Cofely Mannai Facility Management

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 G4S QATAR SPC

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Al Faisal Holdings (MMG Qatar)

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Sodexo Qatar Services

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Como Facility Management Services

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 EFS Facilities Services

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Al-Asmakh Facilities Management

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Qatar Facility Management Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Qatar Facility Management Industry Share (%) by Company 2025

List of Tables

- Table 1: Qatar Facility Management Industry Revenue Million Forecast, by Offering Type 2020 & 2033

- Table 2: Qatar Facility Management Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 3: Qatar Facility Management Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 4: Qatar Facility Management Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Qatar Facility Management Industry Revenue Million Forecast, by Offering Type 2020 & 2033

- Table 6: Qatar Facility Management Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 7: Qatar Facility Management Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 8: Qatar Facility Management Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Qatar Facility Management Industry?

The projected CAGR is approximately 9.39%.

2. Which companies are prominent players in the Qatar Facility Management Industry?

Key companies in the market include Al-Asmakh Facilities Management, Amenity Facility Management & Services WLL, Facilities Management & Maintenance Company LLC, Emcor Facilities Services WLL, Engie Cofely Mannai Facility Management, G4S QATAR SPC, Al Faisal Holdings (MMG Qatar), Sodexo Qatar Services, Como Facility Management Services, EFS Facilities Services.

3. What are the main segments of the Qatar Facility Management Industry?

The market segments include Offering Type, Type, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.65 Million as of 2022.

5. What are some drivers contributing to market growth?

Emergence of Qatar as One of the Key Investment Destinations in the GCC; Growing Emphasis on the Outsourcing of Non-core Operations; Increase in Market Concentration Due to the Entry of Global Firms with Diversified Service Portfolios.

6. What are the notable trends driving market growth?

Public/ Infrastructure Sector Accounts for Significant Growth.

7. Are there any restraints impacting market growth?

Regulatory & Legal Changes; Growing Presence of Global Firms Collaborating with Regional Entities Pose a Challenge for Local Firms.

8. Can you provide examples of recent developments in the market?

March 2022: EDGNEX, a subsidiary of Damac Group, operating in Qatar has partnered with JLL for its facility management needs as it pursues the first phase of its strategy to deliver data center facilities.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Qatar Facility Management Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Qatar Facility Management Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Qatar Facility Management Industry?

To stay informed about further developments, trends, and reports in the Qatar Facility Management Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence