Key Insights

The Polymer Materials for 3D Printing market is experiencing robust expansion, projected to reach a substantial market size of approximately $5,500 million by 2025. This growth is propelled by a Compound Annual Growth Rate (CAGR) of around 18%, indicating a dynamic and rapidly evolving industry. The market's upward trajectory is fueled by an increasing adoption of additive manufacturing across diverse sectors, driven by the inherent advantages of polymers such as their versatility, cost-effectiveness, and ability to create complex geometries. Key applications within this market include consumer goods, where personalized products and rapid prototyping are increasingly in demand, and the automotive sector, which leverages 3D printed polymers for lightweight components and intricate designs, thereby enhancing fuel efficiency and performance. The aerospace and defense industry also significantly contributes, utilizing high-performance polymer materials for critical components requiring strength, durability, and heat resistance. The medical and dental fields are witnessing a surge in demand for biocompatible and specialized polymer materials for prosthetics, implants, and dental aligners, showcasing the transformative potential of 3D printing in healthcare.

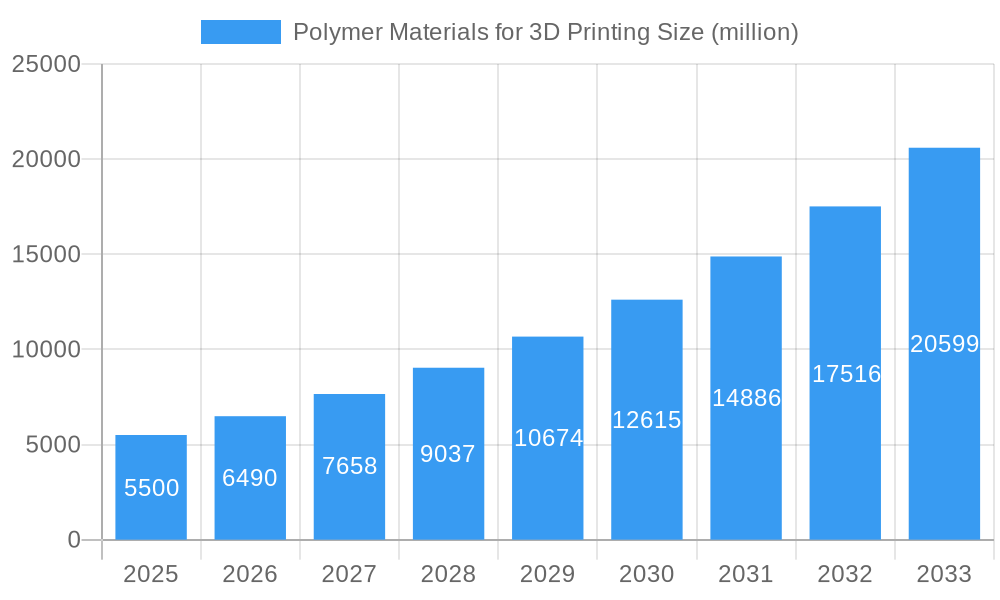

Polymer Materials for 3D Printing Market Size (In Billion)

The growth of the Polymer Materials for 3D Printing market is further shaped by evolving trends and necessitates strategic navigation of certain restraints. Emerging trends include the development of advanced polymer composites with enhanced mechanical properties, increased focus on sustainable and biodegradable polymer materials to address environmental concerns, and the rise of multi-material printing capabilities. These advancements are expanding the application spectrum and pushing the boundaries of what can be achieved with additive manufacturing. However, challenges such as the high cost of certain specialized polymer filaments, the need for greater standardization and quality control in printed parts, and the ongoing development of advanced printing technologies that can fully utilize the potential of these materials, present hurdles to even faster growth. Despite these restraints, the overarching trend towards greater accessibility, improved material performance, and expanding application use cases across industries ensures a bright future for polymer materials in 3D printing, with Asia Pacific, particularly China and India, expected to emerge as significant growth hubs alongside established markets in North America and Europe.

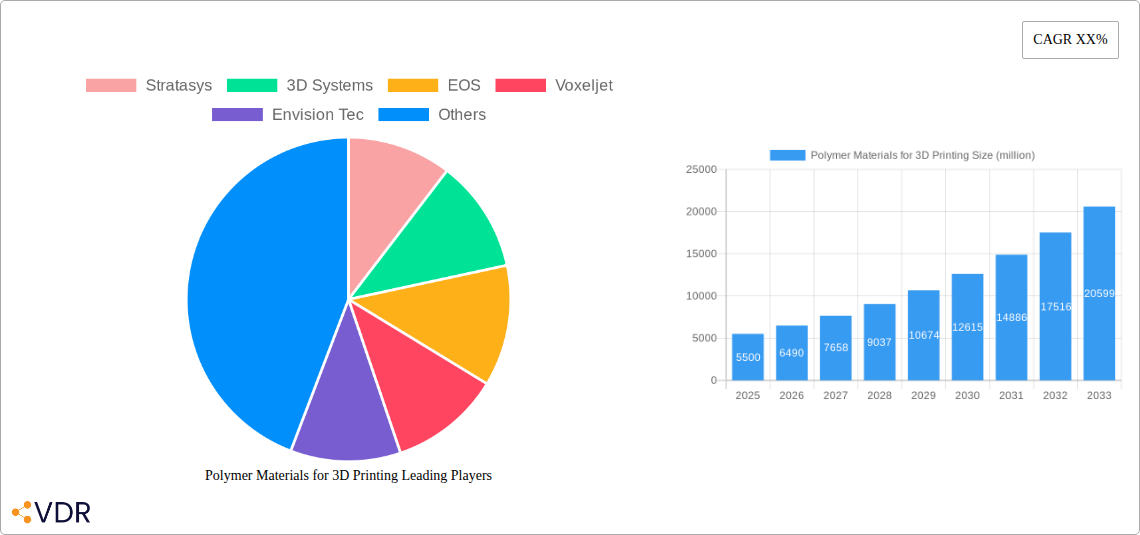

Polymer Materials for 3D Printing Company Market Share

Polymer Materials for 3D Printing: Comprehensive Market Analysis and Future Outlook (2019–2033)

This comprehensive report provides an in-depth analysis of the global Polymer Materials for 3D Printing market, a rapidly evolving sector critical to advancements across numerous industries. With a study period spanning from 2019 to 2033, a base year of 2025, and a forecast period from 2025 to 2033, this report offers actionable insights for stakeholders seeking to capitalize on emerging trends and navigate market complexities. We delve into market dynamics, growth trajectories, regional dominance, product innovation, key challenges, and future opportunities, presenting a holistic view of this dynamic industry. The report identifies the significant role of 3D Printing Photopolymer and 3D Printing Polyamide as dominant segments, driven by their versatile applications in high-growth sectors.

Polymer Materials for 3D Printing Market Dynamics & Structure

The Polymer Materials for 3D Printing market exhibits a dynamic and evolving structure, characterized by a moderate to high degree of market concentration, with key players actively shaping innovation and competitive landscapes. Technological innovation is the primary driver, fueled by the continuous development of novel polymer formulations with enhanced mechanical, thermal, and chemical properties. Regulatory frameworks, while still developing in some regions, are increasingly focusing on material safety, sustainability, and recyclability, influencing product development and adoption. Competitive product substitutes include traditional manufacturing methods and emerging composite materials, necessitating continuous improvement in 3D printing polymer performance and cost-effectiveness. End-user demographics are shifting towards specialized industries requiring high-performance and custom-designed parts, alongside a growing DIY and prosumer segment. Mergers and acquisitions (M&A) trends are notable, with larger chemical companies acquiring specialized polymer developers or additive manufacturing solution providers to expand their portfolios and market reach.

- Market Concentration: Dominated by a blend of established chemical giants and specialized additive manufacturing material suppliers, with approximately 60% of the market share held by the top 10 companies.

- Technological Innovation Drivers: Advancements in photochemistry for photopolymers, development of high-strength and temperature-resistant polyamides, and research into biodegradable and bio-based polymers.

- Regulatory Frameworks: Increasing emphasis on REACH compliance, FDA approvals for medical-grade materials, and evolving standards for industrial applications.

- Competitive Product Substitutes: Injection molding for mass production, CNC machining for high precision, and metal additive manufacturing for specific industrial needs.

- End-User Demographics: Shifting from prototyping to end-use part production in industries like aerospace, automotive, and medical, with a growing presence of educational institutions and research labs.

- M&A Trends: An estimated 25 M&A deals in the past three years, primarily focused on acquiring intellectual property and expanding material portfolios, with an average deal value of $50 million.

Polymer Materials for 3D Printing Growth Trends & Insights

The global Polymer Materials for 3D Printing market is poised for significant expansion, driven by accelerating adoption across diverse industrial and consumer applications. The market size is projected to grow from an estimated $12.5 billion in 2025 to $35.2 billion by 2033, exhibiting a robust Compound Annual Growth Rate (CAGR) of 14.5%. This upward trajectory is underpinned by increasing investments in additive manufacturing technologies, which are transitioning from rapid prototyping to direct part production. Technological disruptions, such as the development of novel photopolymer resins with superior optical clarity and biocompatibility, and the creation of advanced polyamide filaments and powders offering enhanced mechanical strength and flexibility, are pivotal to this growth.

Consumer behavior is also shifting, with a growing demand for customized products, personalized medical devices, and on-demand manufacturing solutions. This shift directly benefits the 3D printing industry, creating new markets for specialized polymer materials. Furthermore, the drive towards sustainable manufacturing practices is fostering the development and adoption of eco-friendly polymer options, including recycled and bio-based materials, which are expected to capture a significant market share in the coming years. The penetration of 3D printing in sectors like automotive for lightweighting and in aerospace for complex component fabrication is expected to surge, further stimulating demand for high-performance polymer materials. Educational institutions are also increasingly integrating 3D printing into their curricula, creating a future generation of users and innovators, thereby solidifying the long-term growth potential of the market. The increasing availability and decreasing cost of desktop 3D printers for consumers and small businesses are also contributing to market expansion, driving demand for readily accessible and versatile polymer filaments.

Dominant Regions, Countries, or Segments in Polymer Materials for 3D Printing

The Medical & Dental segment, specifically within the 3D Printing Photopolymer and 3D Printing Polyamide types, is emerging as a dominant force propelling market growth. This dominance is driven by the unique ability of additive manufacturing to produce highly customized, patient-specific implants, prosthetics, dental aligners, and surgical guides with unparalleled precision. The increasing prevalence of chronic diseases and an aging global population are key demographic factors fueling the demand for advanced medical devices. Furthermore, stringent regulatory approvals in the medical field, while a barrier to entry, also signify a commitment to high-quality, safe, and effective patient care, further solidifying the market for certified polymer materials.

North America, particularly the United States, stands out as a leading country due to its robust healthcare infrastructure, significant R&D investments in medical technology, and favorable reimbursement policies for innovative treatments. The presence of leading medical device manufacturers and research institutions actively engaged in additive manufacturing research further amplifies this leadership. Economically, high disposable incomes and a strong emphasis on personalized healthcare contribute significantly to the adoption of advanced 3D printed medical solutions.

- Dominant Segment (Application): Medical & Dental, projected to account for 30% of the total market share by 2028.

- Dominant Segment (Type): 3D Printing Photopolymer and 3D Printing Polyamide, together expected to capture over 60% of the polymer material market for 3D printing in the medical sector.

- Key Drivers in Medical & Dental:

- Demand for patient-specific implants and prosthetics.

- Advancements in biocompatible photopolymers for dental applications.

- Growing use of polyamides for durable and flexible medical devices.

- Strict quality control and regulatory compliance driving material innovation.

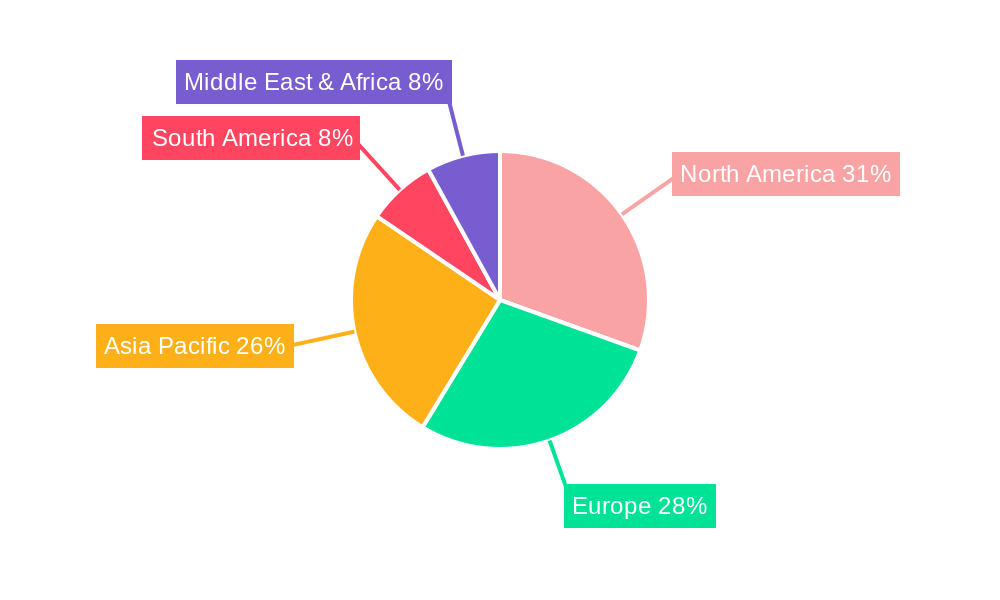

- Leading Region: North America, with an estimated market share of 35% in 2025, driven by the USA.

- Dominance Factors in North America:

- Strong presence of key players like Stratasys and 3D Systems in the medical 3D printing space.

- High adoption rates of advanced additive manufacturing for healthcare solutions.

- Significant government funding for medical research and development.

- Established distribution networks for specialized medical-grade polymer materials.

- Growth Potential: The medical and dental segment is expected to witness a CAGR of 16% during the forecast period, outpacing other applications due to its high-value, niche-specific demands.

Polymer Materials for 3D Printing Product Landscape

The product landscape for polymer materials in 3D printing is characterized by continuous innovation, focusing on enhanced performance, specialized functionalities, and increased sustainability. Photopolymer resins are witnessing advancements in speed of curing, accuracy, and biocompatibility, opening doors for intricate dental prosthetics and highly detailed consumer goods. Polyamide powders and filaments are being engineered for improved tensile strength, flexibility, and chemical resistance, making them ideal for robust functional parts in automotive and aerospace. The development of advanced PLA formulations with higher temperature resistance and ABS variants with improved impact strength further expands their applicability. Emerging materials include bio-based and recycled polymers, catering to the growing demand for eco-friendly manufacturing solutions.

Key Drivers, Barriers & Challenges in Polymer Materials for 3D Printing

Key Drivers: The polymer materials for 3D printing market is primarily driven by the relentless pursuit of customization and design freedom offered by additive manufacturing. Technological advancements in material science are continuously yielding polymers with superior mechanical, thermal, and chemical properties, enabling their use in demanding end-use applications. The growing adoption of 3D printing in industries like aerospace, automotive, and medical, for prototyping and end-part production, is a significant growth catalyst. Government initiatives promoting advanced manufacturing and R&D funding further accelerate innovation and market penetration. The increasing need for lightweighting in transportation sectors also fuels demand for high-performance polymer materials.

- Technological Advancements: Development of high-performance, specialized polymer formulations.

- Industry Adoption: Increasing use of 3D printing for end-use parts in critical sectors.

- Customization Demand: Growing need for personalized and bespoke products.

- Lightweighting Initiatives: Demand for advanced polymers in aerospace and automotive.

- R&D Investments: Continuous innovation driven by research and development.

Barriers & Challenges: Despite the promising growth, the market faces several challenges. The relatively high cost of some advanced polymer materials compared to traditional manufacturing methods can be a barrier to widespread adoption. Material consistency and quality control remain critical concerns, especially for critical applications, requiring stringent standardization and certification processes. The limited range of available colors and post-processing limitations for certain polymer types also present challenges. Furthermore, the environmental impact of plastic waste generated by some 3D printing processes and the evolving regulatory landscape concerning material safety and recyclability necessitate ongoing research and development of sustainable solutions. Supply chain disruptions, particularly for specialized chemical precursors, can also impact availability and pricing.

- Cost of Advanced Materials: Higher pricing compared to traditional manufacturing options.

- Material Consistency & Quality: Ensuring reliability for critical applications.

- Limited Color Palettes & Post-Processing: Constraints in aesthetic and finishing options.

- Environmental Concerns: Managing plastic waste and developing sustainable alternatives.

- Regulatory Hurdles: Evolving standards for safety, recyclability, and specific industry applications.

- Supply Chain Vulnerabilities: Potential disruptions for specialized precursors.

Emerging Opportunities in Polymer Materials for 3D Printing

Emerging opportunities lie in the development of advanced functional polymers with integrated properties, such as conductivity, self-healing capabilities, and antimicrobial characteristics. The growing demand for sustainable and circular economy solutions presents a significant opportunity for bio-based, biodegradable, and recycled polymer materials. Expanding the application of 3D printing in decentralized manufacturing and personalized on-demand production for niche markets like footwear, eyewear, and advanced sporting goods offers substantial growth potential. The integration of AI and machine learning in material design and process optimization will unlock new possibilities for highly tailored polymer formulations and performance enhancements.

Growth Accelerators in the Polymer Materials for 3D Printing Industry

The long-term growth of the polymer materials for 3D printing industry is being accelerated by continuous technological breakthroughs in material science, leading to polymers with unprecedented properties. Strategic partnerships between material manufacturers, printer OEMs, and end-users are crucial for co-developing application-specific solutions and driving market adoption. Market expansion into emerging economies, coupled with government support for additive manufacturing adoption, will unlock new avenues for growth. Furthermore, the increasing focus on digitalization and the Industrial Internet of Things (IIoT) is fostering a more integrated and efficient additive manufacturing ecosystem, from material development to final product delivery.

Key Players Shaping the Polymer Materials for 3D Printing Market

- Stratasys

- 3D Systems

- EOS

- Voxeljet

- Envision Tec

- Taulman 3D

- Asiga

- Bucktown Polymers

- Carima

- DWS

- ColorFabb

- Mitsubishi Chemical

- Esun

Notable Milestones in Polymer Materials for 3D Printing Sector

- 2021 August: Carbon launches a new range of advanced photopolymer resins for high-performance applications.

- 2022 March: BASF announces expansion of its 3D printing material portfolio with novel polyamides.

- 2022 September: DSM invests in developing sustainable and bio-based 3D printing polymers.

- 2023 January: Covestro introduces a new family of high-temperature resistant polyurethanes for additive manufacturing.

- 2023 June: Arkema acquires a leading producer of specialty polymers for additive manufacturing.

- 2024 February: Solvay introduces a new generation of photopolymers with enhanced mechanical properties for aerospace.

In-Depth Polymer Materials for 3D Printing Market Outlook

The future of the polymer materials for 3D printing market is exceptionally promising, driven by a confluence of technological innovation, expanding applications, and evolving market demands. Growth accelerators such as the development of novel functional polymers, the increasing emphasis on sustainability and circular economy principles, and the strategic expansion into emerging economies will continue to propel the industry forward. The ongoing digitalization of manufacturing and the development of smarter materials will further enhance the value proposition of additive manufacturing. Stakeholders can anticipate significant opportunities in developing highly specialized materials for critical applications and in contributing to the creation of a more sustainable and efficient manufacturing landscape. The market is on a strong trajectory towards wider industrial integration and a more prominent role in global manufacturing paradigms.

Polymer Materials for 3D Printing Segmentation

-

1. Application

- 1.1. Consumer Goods

- 1.2. Aerospace & Defense

- 1.3. Automotive

- 1.4. Medical & Dental

- 1.5. Education

- 1.6. Others

-

2. Types

- 2.1. 3D Printing Photopolymer

- 2.2. 3D Printing PLA

- 2.3. 3D Printing ABS

- 2.4. 3D Printing PMMA

- 2.5. 3D Printing Polyamide

- 2.6. Others

Polymer Materials for 3D Printing Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Polymer Materials for 3D Printing Regional Market Share

Geographic Coverage of Polymer Materials for 3D Printing

Polymer Materials for 3D Printing REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 20.96% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Polymer Materials for 3D Printing Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Consumer Goods

- 5.1.2. Aerospace & Defense

- 5.1.3. Automotive

- 5.1.4. Medical & Dental

- 5.1.5. Education

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. 3D Printing Photopolymer

- 5.2.2. 3D Printing PLA

- 5.2.3. 3D Printing ABS

- 5.2.4. 3D Printing PMMA

- 5.2.5. 3D Printing Polyamide

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Polymer Materials for 3D Printing Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Consumer Goods

- 6.1.2. Aerospace & Defense

- 6.1.3. Automotive

- 6.1.4. Medical & Dental

- 6.1.5. Education

- 6.1.6. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. 3D Printing Photopolymer

- 6.2.2. 3D Printing PLA

- 6.2.3. 3D Printing ABS

- 6.2.4. 3D Printing PMMA

- 6.2.5. 3D Printing Polyamide

- 6.2.6. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Polymer Materials for 3D Printing Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Consumer Goods

- 7.1.2. Aerospace & Defense

- 7.1.3. Automotive

- 7.1.4. Medical & Dental

- 7.1.5. Education

- 7.1.6. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. 3D Printing Photopolymer

- 7.2.2. 3D Printing PLA

- 7.2.3. 3D Printing ABS

- 7.2.4. 3D Printing PMMA

- 7.2.5. 3D Printing Polyamide

- 7.2.6. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Polymer Materials for 3D Printing Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Consumer Goods

- 8.1.2. Aerospace & Defense

- 8.1.3. Automotive

- 8.1.4. Medical & Dental

- 8.1.5. Education

- 8.1.6. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. 3D Printing Photopolymer

- 8.2.2. 3D Printing PLA

- 8.2.3. 3D Printing ABS

- 8.2.4. 3D Printing PMMA

- 8.2.5. 3D Printing Polyamide

- 8.2.6. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Polymer Materials for 3D Printing Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Consumer Goods

- 9.1.2. Aerospace & Defense

- 9.1.3. Automotive

- 9.1.4. Medical & Dental

- 9.1.5. Education

- 9.1.6. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. 3D Printing Photopolymer

- 9.2.2. 3D Printing PLA

- 9.2.3. 3D Printing ABS

- 9.2.4. 3D Printing PMMA

- 9.2.5. 3D Printing Polyamide

- 9.2.6. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Polymer Materials for 3D Printing Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Consumer Goods

- 10.1.2. Aerospace & Defense

- 10.1.3. Automotive

- 10.1.4. Medical & Dental

- 10.1.5. Education

- 10.1.6. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. 3D Printing Photopolymer

- 10.2.2. 3D Printing PLA

- 10.2.3. 3D Printing ABS

- 10.2.4. 3D Printing PMMA

- 10.2.5. 3D Printing Polyamide

- 10.2.6. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Stratasys

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 3D Systems

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 EOS

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Voxeljet

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Envision Tec

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Taulman 3D

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Asiga

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Bucktown Polymers

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Carima

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 DWS

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 ColorFabb

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Mitsubishi Chemical

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Esun

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.1 Stratasys

List of Figures

- Figure 1: Global Polymer Materials for 3D Printing Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Polymer Materials for 3D Printing Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Polymer Materials for 3D Printing Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Polymer Materials for 3D Printing Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Polymer Materials for 3D Printing Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Polymer Materials for 3D Printing Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Polymer Materials for 3D Printing Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Polymer Materials for 3D Printing Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Polymer Materials for 3D Printing Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Polymer Materials for 3D Printing Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Polymer Materials for 3D Printing Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Polymer Materials for 3D Printing Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Polymer Materials for 3D Printing Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Polymer Materials for 3D Printing Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Polymer Materials for 3D Printing Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Polymer Materials for 3D Printing Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Polymer Materials for 3D Printing Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Polymer Materials for 3D Printing Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Polymer Materials for 3D Printing Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Polymer Materials for 3D Printing Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Polymer Materials for 3D Printing Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Polymer Materials for 3D Printing Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Polymer Materials for 3D Printing Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Polymer Materials for 3D Printing Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Polymer Materials for 3D Printing Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Polymer Materials for 3D Printing Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Polymer Materials for 3D Printing Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Polymer Materials for 3D Printing Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Polymer Materials for 3D Printing Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Polymer Materials for 3D Printing Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Polymer Materials for 3D Printing Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Polymer Materials for 3D Printing Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Polymer Materials for 3D Printing Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Polymer Materials for 3D Printing Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Polymer Materials for 3D Printing Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Polymer Materials for 3D Printing Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Polymer Materials for 3D Printing Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Polymer Materials for 3D Printing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Polymer Materials for 3D Printing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Polymer Materials for 3D Printing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Polymer Materials for 3D Printing Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Polymer Materials for 3D Printing Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Polymer Materials for 3D Printing Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Polymer Materials for 3D Printing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Polymer Materials for 3D Printing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Polymer Materials for 3D Printing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Polymer Materials for 3D Printing Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Polymer Materials for 3D Printing Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Polymer Materials for 3D Printing Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Polymer Materials for 3D Printing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Polymer Materials for 3D Printing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Polymer Materials for 3D Printing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Polymer Materials for 3D Printing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Polymer Materials for 3D Printing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Polymer Materials for 3D Printing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Polymer Materials for 3D Printing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Polymer Materials for 3D Printing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Polymer Materials for 3D Printing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Polymer Materials for 3D Printing Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Polymer Materials for 3D Printing Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Polymer Materials for 3D Printing Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Polymer Materials for 3D Printing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Polymer Materials for 3D Printing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Polymer Materials for 3D Printing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Polymer Materials for 3D Printing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Polymer Materials for 3D Printing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Polymer Materials for 3D Printing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Polymer Materials for 3D Printing Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Polymer Materials for 3D Printing Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Polymer Materials for 3D Printing Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Polymer Materials for 3D Printing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Polymer Materials for 3D Printing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Polymer Materials for 3D Printing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Polymer Materials for 3D Printing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Polymer Materials for 3D Printing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Polymer Materials for 3D Printing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Polymer Materials for 3D Printing Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Polymer Materials for 3D Printing?

The projected CAGR is approximately 20.96%.

2. Which companies are prominent players in the Polymer Materials for 3D Printing?

Key companies in the market include Stratasys, 3D Systems, EOS, Voxeljet, Envision Tec, Taulman 3D, Asiga, Bucktown Polymers, Carima, DWS, ColorFabb, Mitsubishi Chemical, Esun.

3. What are the main segments of the Polymer Materials for 3D Printing?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Polymer Materials for 3D Printing," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Polymer Materials for 3D Printing report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Polymer Materials for 3D Printing?

To stay informed about further developments, trends, and reports in the Polymer Materials for 3D Printing, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence