Key Insights

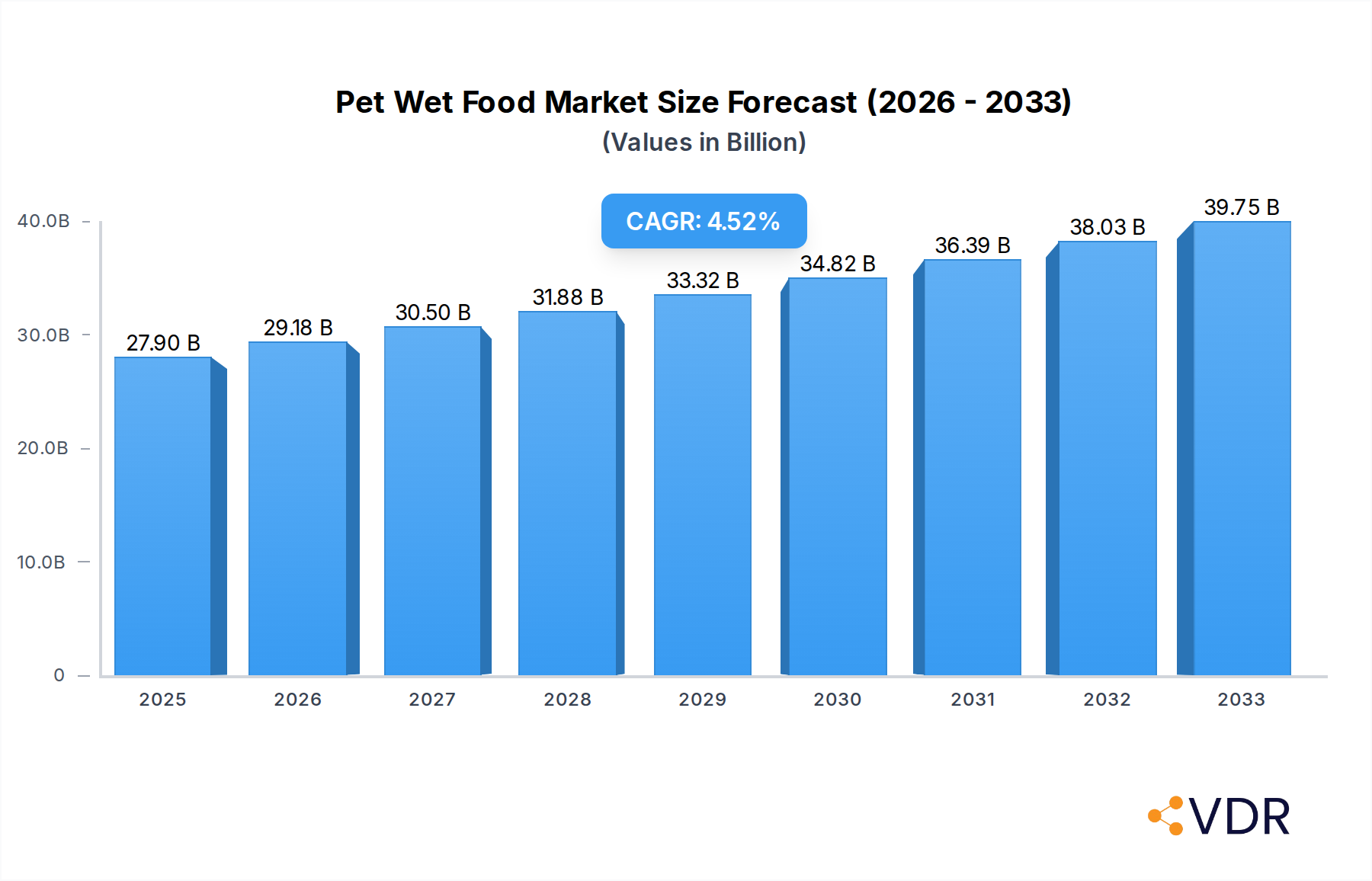

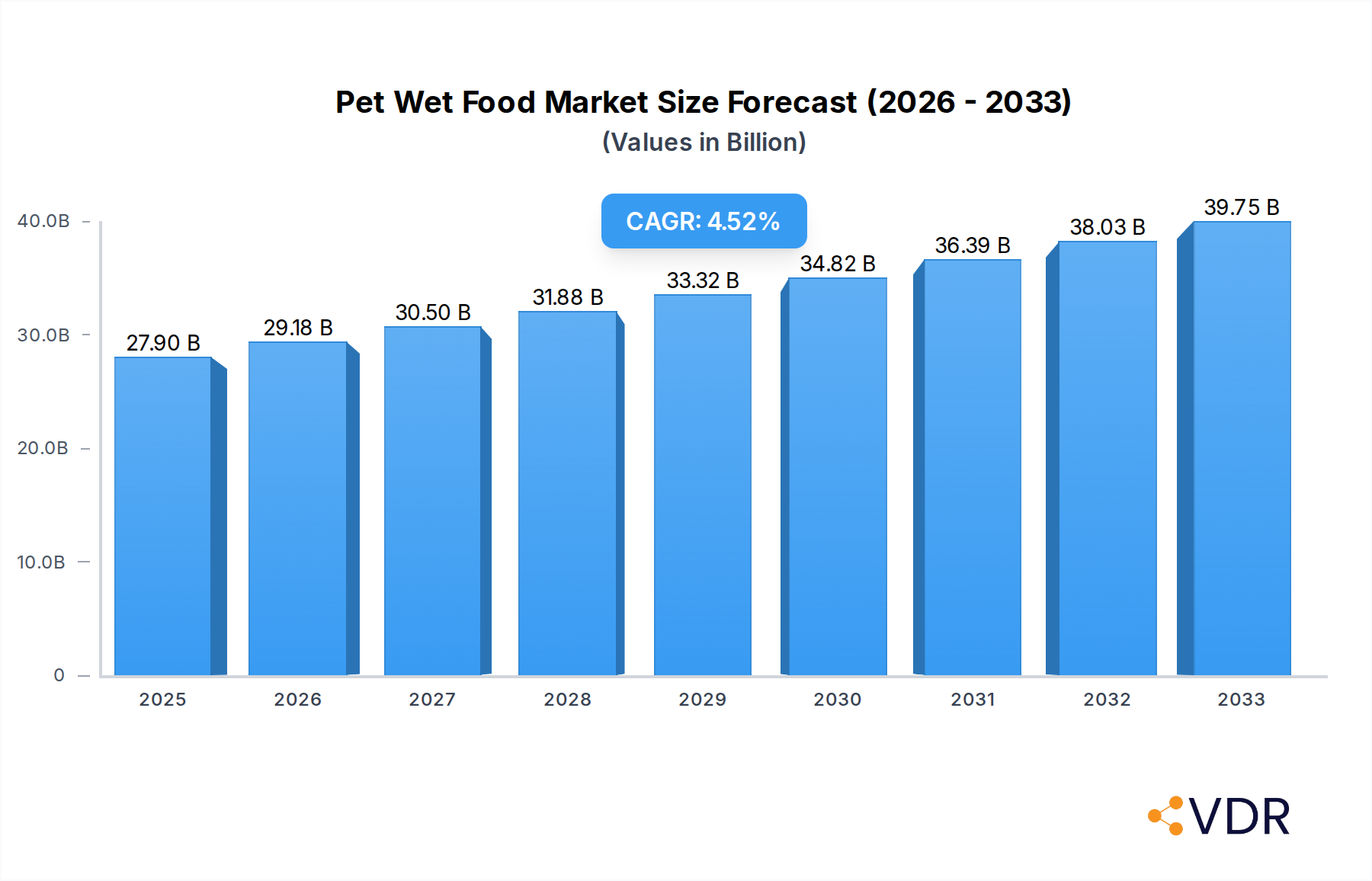

The global Pet Wet Food market is poised for robust growth, projected to reach a substantial $27.9 billion in 2025, expanding at a CAGR of 4.58% through 2033. This upward trajectory is primarily fueled by an increasing humanization of pets, where owners increasingly view their animal companions as integral family members, demanding higher quality and more specialized nutrition. This sentiment translates into a growing preference for wet food due to its palatability, moisture content, and perceived health benefits, especially for pets with specific dietary needs or older animals. The market is witnessing strong demand across both the Pet Dog and Pet Cat segments, with innovation in product formulations, flavor varieties, and grain-free or limited-ingredient options further stimulating consumer interest. Leading companies such as Mars, Nestle Purina, and Colgate-Palmolive are actively investing in research and development to cater to evolving consumer preferences and capitalize on this expanding market.

Pet Wet Food Market Size (In Billion)

Key drivers propelling the Pet Wet Food market include the rising disposable incomes globally, enabling pet owners to allocate more resources to premium pet food. Furthermore, the surge in pet adoption rates, particularly in emerging economies, presents a significant growth opportunity. The trend towards subscription services and e-commerce platforms for pet food has also made these products more accessible and convenient for consumers. While the market exhibits strong growth, potential restraints might include fluctuating raw material costs, which could impact pricing strategies. Additionally, growing consumer awareness regarding the environmental impact of pet food production and packaging could necessitate a shift towards more sustainable practices. Nevertheless, the overarching trend of premiumization and the unwavering emotional bond between owners and their pets are expected to sustain the positive market momentum for the foreseeable future.

Pet Wet Food Company Market Share

Here is a compelling, SEO-optimized report description for the Pet Wet Food market, designed to attract industry professionals and maximize search engine visibility.

Pet Wet Food Market Dynamics & Structure

The global Pet Wet Food market exhibits a moderate to highly concentrated structure, driven by the significant presence of multinational corporations and strong regional players. Technological innovation plays a crucial role, with advancements in palatability enhancers, nutritional formulations, and sustainable packaging shaping product development. Regulatory frameworks, including food safety standards and labeling requirements, are critical for market entry and sustained operations. Competitive product substitutes, such as dry kibble and raw food diets, present a constant challenge, pushing manufacturers to differentiate through premium offerings and specialized formulations. End-user demographics, characterized by increasing pet humanization and rising disposable incomes, are a primary driver of demand. Mergers and acquisitions (M&A) activity remains a key strategic lever for market consolidation and expansion.

- Market Concentration: Dominated by a few key players, but with a growing number of niche manufacturers.

- Technological Innovation: Focus on advanced nutrient delivery, improved palatability, and shelf-life extension.

- Regulatory Frameworks: Stringent food safety regulations and evolving labeling standards for pet food.

- Competitive Product Substitutes: Dry food, raw diets, and homemade pet food options influencing consumer choices.

- End-User Demographics: Rising pet ownership, humanization trends, and increased spending on premium pet products.

- M&A Trends: Strategic acquisitions to gain market share, expand product portfolios, and access new geographies.

Pet Wet Food Growth Trends & Insights

The Pet Wet Food market is poised for robust expansion, driven by a confluence of evolving consumer attitudes towards pet care and significant product innovation. The market size is projected to witness substantial growth, fueled by increasing pet ownership globally and the ongoing trend of pet humanization, where pets are increasingly viewed as integral family members. This sentiment translates into a higher willingness among pet owners to invest in premium and specialized pet food options, with wet food often perceived as more palatable and closer to a natural diet. Adoption rates for wet pet food are steadily climbing, particularly in emerging economies where disposable incomes are rising, and awareness of advanced pet nutrition is growing.

Technological disruptions are continuously reshaping the market. Innovations in ingredient sourcing, such as the increased use of sustainably sourced proteins and novel functional ingredients like prebiotics and probiotics, are enhancing the nutritional profile and perceived health benefits of wet pet food. Advanced processing techniques are also contributing to improved texture, flavor, and preservation, further appealing to both pets and their owners. Furthermore, the development of specialized wet food formulations catering to specific life stages, breed needs, and health conditions (e.g., weight management, sensitive stomachs, dental health) is a significant growth driver.

Consumer behavior shifts are also playing a pivotal role. Pet owners are becoming more informed and discerning, actively seeking out brands that offer transparency in ingredients, ethical sourcing, and scientifically backed nutritional claims. The convenience factor associated with wet food, particularly single-serving pouches and cans, appeals to busy pet owners. The rise of e-commerce and subscription services has further democratized access to a wider variety of wet pet food options, making it easier for consumers to discover and repurchase their preferred brands. The historical period (2019–2024) has laid the groundwork for this sustained growth, with the base year of 2025 expected to see an estimated market value of $XX billion, projecting a compound annual growth rate (CAGR) of XX% through the forecast period of 2025–2033. This upward trajectory is underpinned by a market penetration that is expected to increase significantly as more consumers recognize the benefits of high-quality wet food for their pets' overall well-being.

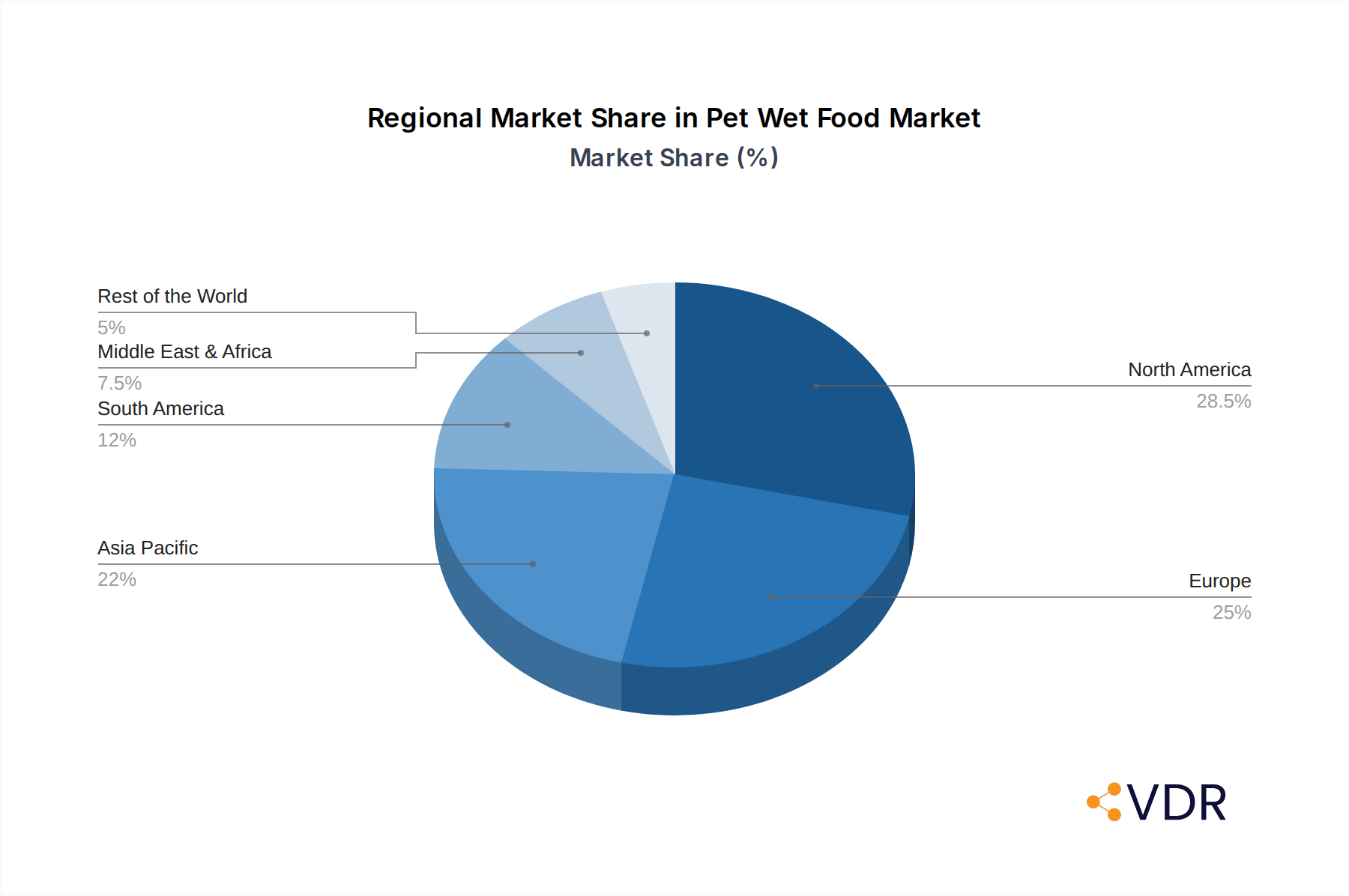

Dominant Regions, Countries, or Segments in Pet Wet Food

The global Pet Wet Food market’s dominance is significantly influenced by the Pet Cat application segment, which consistently outpaces other applications due to several compelling factors. The inherent dietary preferences and perceived nutritional needs of cats, coupled with the increasing number of cat owners worldwide, make this segment a cornerstone of market growth. Cats are often more discerning eaters than dogs, and the high palatability and moisture content of wet food align perfectly with their preferences, leading to higher consumption rates.

The 200-400g type segment within pet wet food is also experiencing exceptional growth, reflecting a sweet spot in terms of convenience, portion control, and value for money for both cat and dog owners. These package sizes are ideal for single-pet households and for pet owners seeking to provide fresh meals without excessive leftovers, thereby reducing waste and maintaining freshness. This size also offers a balance between affordability and a substantial serving, making it a popular choice across various socioeconomic demographics.

North America continues to be a dominant region, driven by its mature pet care market, high pet ownership rates, and a deeply ingrained culture of pet humanization. The economic prosperity in countries like the United States and Canada translates into higher disposable incomes, allowing consumers to allocate significant budgets towards premium pet food, including wet varieties. The well-established retail infrastructure, encompassing both brick-and-mortar pet specialty stores and robust e-commerce platforms, facilitates widespread availability and accessibility of a diverse range of pet wet food products.

- Application Dominance (Pet Cat):

- Higher palatability and moisture content favored by feline dietary preferences.

- Increasing global cat population and rising adoption rates.

- Perceived as closer to a natural diet, aligning with cat owner concerns.

- Type Dominance (200-400g):

- Ideal for portion control and managing freshness, reducing food waste.

- Offers a balance of value and convenience for single and multi-pet households.

- Appeals to a broad spectrum of consumers seeking practical solutions.

- Regional Dominance (North America):

- Mature pet market with high pet ownership and humanization trends.

- Strong economic indicators supporting premium pet product spending.

- Extensive retail and e-commerce distribution networks.

- High consumer awareness of pet nutrition and health benefits.

Pet Wet Food Product Landscape

The Pet Wet Food product landscape is characterized by an accelerating wave of innovation aimed at meeting the sophisticated demands of modern pet owners. Manufacturers are increasingly focusing on developing formulations that mimic natural diets, incorporating high-quality proteins, such as poultry, fish, and novel meat sources, as well as a variety of vegetables and fruits. This trend is driven by a desire to provide complete and balanced nutrition while enhancing palatability. Product applications span a wide range, from everyday staples to specialized diets targeting specific health concerns like sensitive digestion, weight management, and age-related needs. Performance metrics are gauged by superior nutrient bioavailability, enhanced digestibility, and positive feedback on taste and texture from pets. Unique selling propositions often revolve around grain-free options, limited ingredient diets, and the inclusion of functional ingredients like antioxidants, omega fatty acids, and prebiotics/probiotics to support overall pet wellness and longevity. Technological advancements in processing and packaging are also critical, ensuring extended shelf life and maintaining the nutritional integrity of the product.

Key Drivers, Barriers & Challenges in Pet Wet Food

The Pet Wet Food market is propelled by several key drivers. The burgeoning trend of pet humanization, where pets are considered family members, is a primary impetus, leading owners to seek premium, human-grade ingredients and specialized nutrition. The increasing global pet population, particularly in emerging economies, provides a vast untapped consumer base. Technological advancements in food processing and formulation contribute to improved palatability, digestibility, and the incorporation of functional ingredients that offer health benefits, thereby enhancing product appeal.

However, the market faces significant barriers and challenges. The higher cost of production for wet food compared to dry kibble can make it less accessible for budget-conscious consumers, especially in price-sensitive regions. Stringent regulatory requirements for food safety and labeling can pose compliance hurdles for manufacturers. The availability and cost of high-quality raw ingredients can fluctuate, impacting supply chains and profit margins. Furthermore, the competitive landscape is intense, with established global players and numerous smaller brands vying for market share, necessitating continuous innovation and effective marketing strategies.

Emerging Opportunities in Pet Wet Food

Emerging opportunities in the Pet Wet Food sector lie in catering to niche markets and evolving consumer preferences. The demand for sustainably sourced and ethically produced pet food is on the rise, presenting an opportunity for brands that prioritize these values. Innovations in plant-based and insect-based protein sources offer novel avenues for sustainable and hypoallergenic wet food formulations. Personalized nutrition, leveraging advanced diagnostics and tailored ingredient blends, represents a significant future growth area. Furthermore, the expansion of direct-to-consumer (DTC) models and subscription services allows for greater customer engagement and data collection, enabling the development of highly customized product offerings.

Growth Accelerators in the Pet Wet Food Industry

Several catalysts are accelerating long-term growth in the Pet Wet Food industry. Technological breakthroughs in extrusion and aseptic processing are enabling the creation of more diverse textures and longer shelf lives, making wet food more versatile and appealing. Strategic partnerships between pet food manufacturers and veterinary clinics or pet nutritionists can enhance product credibility and drive adoption through professional recommendations. Market expansion strategies targeting underserved demographics and geographical regions, particularly in Asia and Latin America, offer substantial growth potential. The development of innovative packaging solutions that enhance convenience, reduce environmental impact, and preserve freshness also acts as a significant growth accelerator.

Key Players Shaping the Pet Wet Food Market

- Mars

- Nestle Purina

- Mogiana Alimentos

- Colgate-Palmolive

- Total Alimentos

- Nutriara Alimentos

- Heristo

- Diamond Pet Foods

- Empresas Iansa

- Unicharm

Notable Milestones in Pet Wet Food Sector

- 2019: Increased focus on grain-free and limited ingredient diets as consumer awareness of pet allergies grew.

- 2020: Surge in e-commerce sales of pet food, including wet varieties, driven by pandemic-related lockdowns and convenience.

- 2021: Introduction of innovative functional ingredients like CBD and adaptogens aimed at supporting pet wellness.

- 2022: Greater emphasis on sustainable packaging solutions and transparent ingredient sourcing by major manufacturers.

- 2023: Expansion of specialized diet offerings for specific life stages and health conditions, including senior pets and pets with kidney issues.

- 2024: Growing interest in plant-based and alternative protein sources in pet food formulations.

In-Depth Pet Wet Food Market Outlook

The Pet Wet Food market outlook remains exceptionally positive, with growth accelerators such as sustainable ingredient sourcing, personalized nutrition plans, and the expansion into emerging markets poised to drive significant expansion. The continued evolution of pet humanization trends ensures sustained demand for premium, health-conscious options. Technological advancements in processing and packaging will further enhance product offerings and consumer convenience. Strategic collaborations and a focus on direct-to-consumer channels will foster deeper brand loyalty and market penetration. The future of the Pet Wet Food market is characterized by innovation, specialization, and a steadfast commitment to pet well-being.

Pet Wet Food Segmentation

-

1. Application

- 1.1. Pet Dog

- 1.2. Pet Cat

- 1.3. Others

-

2. Types

- 2.1. 80-200g

- 2.2. 200-400g

- 2.3. 400-600g

- 2.4. Others

Pet Wet Food Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Pet Wet Food Regional Market Share

Geographic Coverage of Pet Wet Food

Pet Wet Food REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.58% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Pet Wet Food Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Pet Dog

- 5.1.2. Pet Cat

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. 80-200g

- 5.2.2. 200-400g

- 5.2.3. 400-600g

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Pet Wet Food Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Pet Dog

- 6.1.2. Pet Cat

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. 80-200g

- 6.2.2. 200-400g

- 6.2.3. 400-600g

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Pet Wet Food Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Pet Dog

- 7.1.2. Pet Cat

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. 80-200g

- 7.2.2. 200-400g

- 7.2.3. 400-600g

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Pet Wet Food Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Pet Dog

- 8.1.2. Pet Cat

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. 80-200g

- 8.2.2. 200-400g

- 8.2.3. 400-600g

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Pet Wet Food Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Pet Dog

- 9.1.2. Pet Cat

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. 80-200g

- 9.2.2. 200-400g

- 9.2.3. 400-600g

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Pet Wet Food Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Pet Dog

- 10.1.2. Pet Cat

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. 80-200g

- 10.2.2. 200-400g

- 10.2.3. 400-600g

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Mars

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Nestle Purina

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Mogiana Alimentos

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Colgate-Palmolive

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Total Alimentos

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Nutriara Alimentos

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Heristo

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Diamond pet foods

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Empresas Iansa

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Unicharm

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Mars

List of Figures

- Figure 1: Global Pet Wet Food Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Pet Wet Food Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Pet Wet Food Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Pet Wet Food Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Pet Wet Food Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Pet Wet Food Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Pet Wet Food Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Pet Wet Food Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Pet Wet Food Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Pet Wet Food Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Pet Wet Food Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Pet Wet Food Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Pet Wet Food Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Pet Wet Food Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Pet Wet Food Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Pet Wet Food Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Pet Wet Food Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Pet Wet Food Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Pet Wet Food Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Pet Wet Food Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Pet Wet Food Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Pet Wet Food Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Pet Wet Food Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Pet Wet Food Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Pet Wet Food Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Pet Wet Food Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Pet Wet Food Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Pet Wet Food Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Pet Wet Food Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Pet Wet Food Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Pet Wet Food Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Pet Wet Food Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Pet Wet Food Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Pet Wet Food Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Pet Wet Food Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Pet Wet Food Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Pet Wet Food Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Pet Wet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Pet Wet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Pet Wet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Pet Wet Food Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Pet Wet Food Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Pet Wet Food Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Pet Wet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Pet Wet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Pet Wet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Pet Wet Food Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Pet Wet Food Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Pet Wet Food Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Pet Wet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Pet Wet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Pet Wet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Pet Wet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Pet Wet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Pet Wet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Pet Wet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Pet Wet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Pet Wet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Pet Wet Food Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Pet Wet Food Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Pet Wet Food Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Pet Wet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Pet Wet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Pet Wet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Pet Wet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Pet Wet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Pet Wet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Pet Wet Food Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Pet Wet Food Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Pet Wet Food Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Pet Wet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Pet Wet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Pet Wet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Pet Wet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Pet Wet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Pet Wet Food Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Pet Wet Food Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Pet Wet Food?

The projected CAGR is approximately 4.58%.

2. Which companies are prominent players in the Pet Wet Food?

Key companies in the market include Mars, Nestle Purina, Mogiana Alimentos, Colgate-Palmolive, Total Alimentos, Nutriara Alimentos, Heristo, Diamond pet foods, Empresas Iansa, Unicharm.

3. What are the main segments of the Pet Wet Food?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Pet Wet Food," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Pet Wet Food report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Pet Wet Food?

To stay informed about further developments, trends, and reports in the Pet Wet Food, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence