Key Insights

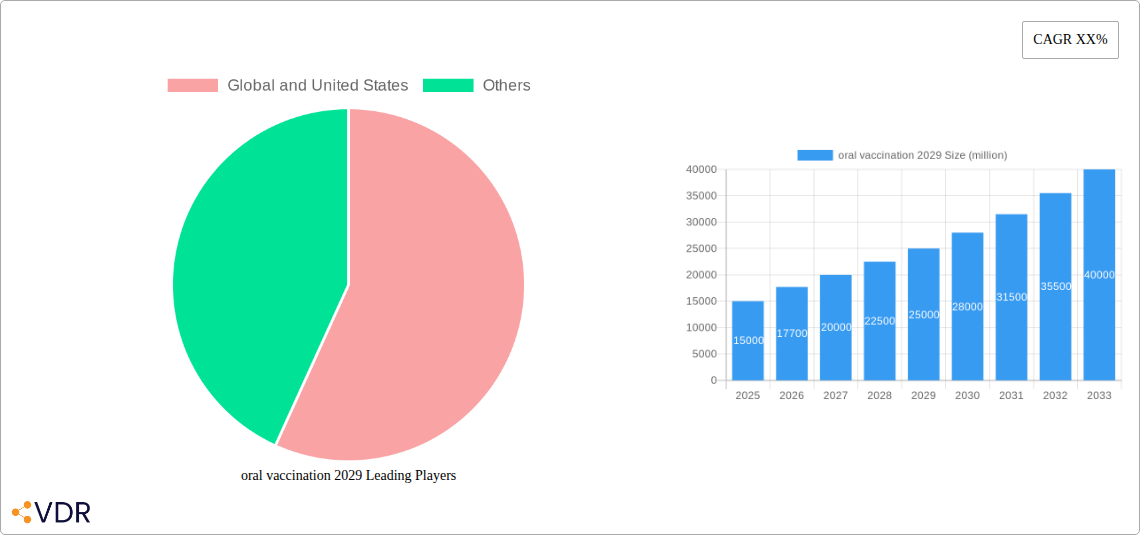

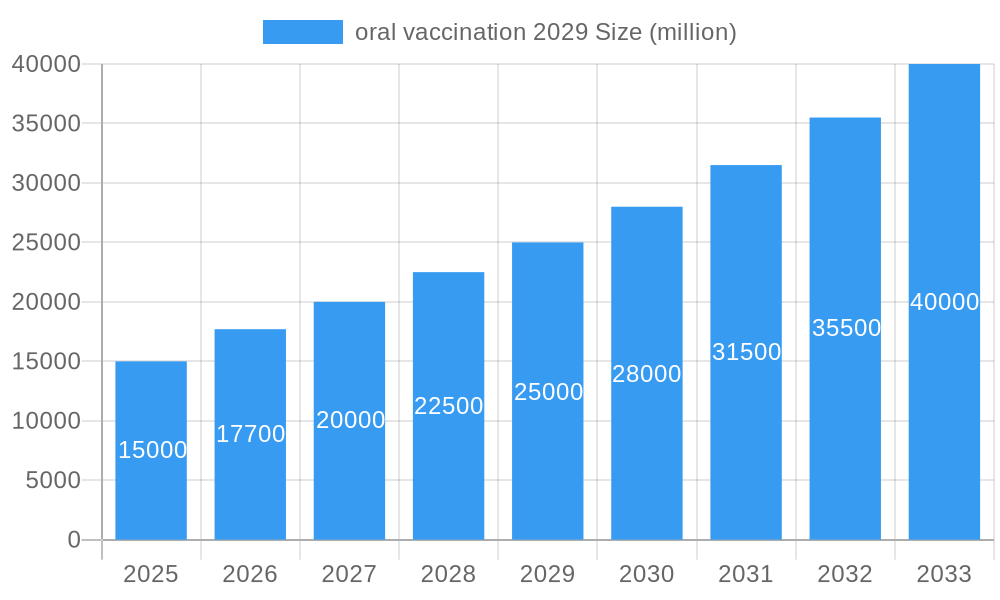

The global oral vaccination market is projected to reach $4.24 billion by 2029, growing at a CAGR of 9.53% from a base year of 2025. This expansion is driven by the rising incidence of infectious diseases, increased demand for convenient, needle-free vaccination, and advancements in vaccine development. Oral vaccines offer advantages like simplified administration, reduced needle-stick injuries, improved patient compliance, and enhanced mucosal immunity, driving their adoption in pediatric and adult populations. Global emphasis on public health preparedness and the development of novel oral vaccine candidates for emerging threats will further propel market growth.

oral vaccination 2029 Market Size (In Billion)

Key trends shaping the market include sustained investment in R&D for oral vaccine stability and efficacy. Nanotechnology and novel adjuvant systems are crucial for overcoming oral delivery challenges, such as gastrointestinal degradation and immunogenicity. Geographically, the Asia Pacific region is a significant growth driver due to its large population, increasing healthcare spending, and rising vaccination awareness. While opportunities are abundant, lengthy regulatory approval processes and extensive clinical trial requirements may temper growth in certain segments. Nonetheless, the demand for safer, more accessible, and patient-friendly immunization strategies ensures a dynamic future for the oral vaccination market.

oral vaccination 2029 Company Market Share

Report Overview:

This comprehensive report analyzes the global oral vaccination market through 2029, providing insights into its dynamics, growth, and future potential. Covering the period from 2019 to 2033, with a base and forecast year of 2025, this study examines oral vaccine development, technology, and delivery systems. It identifies key drivers, challenges, and opportunities, highlighting the impact of vaccine advancements, preventive healthcare, and public health initiatives.

This analysis, tailored for industry professionals, researchers, investors, and policymakers, provides quantitative data in billion units and qualitative assessments. It serves as an essential guide to understanding the oral vaccination market size, market share, and factors influencing oral vaccine adoption rates.

Oral Vaccination Market Dynamics & Structure

The global oral vaccination market in 2029 is characterized by a dynamic interplay of technological innovation, evolving regulatory landscapes, and shifting end-user demographics. Market concentration remains moderate, with a few key players holding significant shares, but innovation remains a crucial differentiator. The primary driver of technological innovation is the pursuit of more convenient and accessible vaccination methods, reducing the need for injections and overcoming needle phobia, thereby improving vaccine uptake. Robust regulatory frameworks, particularly from agencies like the FDA and EMA, are essential for ensuring the safety and efficacy of new oral vaccines, though they can also present hurdles to rapid development. Competitive product substitutes, including traditional injectable vaccines and other preventative healthcare measures, exert continuous pressure, necessitating clear demonstration of oral vaccine advantages in terms of efficacy, safety, and patient compliance.

- Market Concentration: Moderate, with a growing number of innovative biotechs entering the space.

- Technological Innovation Drivers: Enhanced vaccine stability, improved antigen delivery mechanisms, and advancements in formulation science are key.

- Regulatory Frameworks: Stringent yet supportive, focusing on rigorous clinical trials and post-market surveillance.

- Competitive Product Substitutes: Injectable vaccines, other preventative measures; differentiation is crucial.

- End-User Demographics: Growing demand from pediatric populations, individuals with needle phobia, and in resource-limited settings.

- M&A Trends: Strategic acquisitions and partnerships are increasing as larger pharmaceutical companies seek to bolster their pipelines in this promising segment.

Oral Vaccination Market Growth Trends & Insights

The oral vaccination market is poised for substantial growth, driven by a confluence of factors that are reshaping the global healthcare landscape. The market size evolution is projected to be robust, fueled by an increasing understanding of the benefits and a growing pipeline of oral vaccine candidates for various infectious diseases. Adoption rates are steadily climbing as clinical trials demonstrate comparable or superior efficacy to injectable counterparts, coupled with significantly enhanced patient convenience. Technological disruptions are at the forefront of this expansion, with breakthroughs in oral vaccine platforms such as enteric-coated capsules, nanoparticles, and mucoadhesive systems enabling effective antigen delivery and immune stimulation in the gastrointestinal tract. These advancements are crucial for overcoming the challenges of oral administration, including enzymatic degradation and poor bioavailability.

Consumer behavior shifts are profoundly impacting the market. There is a noticeable preference for less invasive health interventions, particularly among parents for their children and for routine adult immunizations. This inclination towards needle-free vaccination is a powerful catalyst, driving demand for oral alternatives. Furthermore, the ongoing global focus on pandemic preparedness and the need for rapid, scalable vaccine deployment strategies highlight the strategic advantage of oral vaccines, which can potentially simplify distribution and administration in public health emergencies. The oral vaccine market forecast indicates a consistent upward trajectory, with a projected compound annual growth rate (CAGR) of XX% from 2025 to 2033. Market penetration for specific indications is expected to increase significantly as approved oral vaccines become widely available.

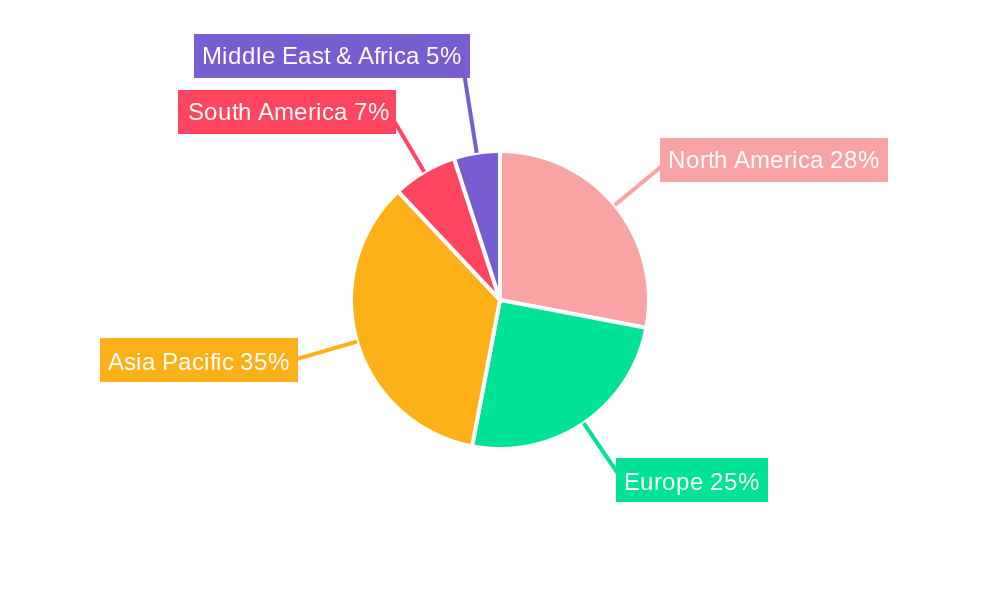

Dominant Regions, Countries, or Segments in Oral Vaccination 2029

The oral vaccination market in 2029 is experiencing dominant growth driven by specific regions, countries, and application segments. North America, particularly the United States, is a leading force due to its advanced healthcare infrastructure, high research and development investment, and strong regulatory support for novel vaccine technologies. The strong presence of major pharmaceutical companies and a robust market for innovative healthcare solutions further solidify its position.

From an Application perspective, the pediatric oral vaccine segment is a primary growth driver. The inherent challenges and anxieties associated with childhood immunizations, particularly needle phobia, make oral vaccines a highly sought-after alternative. This translates into significant market share and high growth potential for oral vaccines targeting common childhood diseases like rotavirus, polio, and potentially future vaccines for respiratory syncytial virus (RSV) and other prevalent pediatric infections.

The Types of oral vaccines contributing to market dominance include live-attenuated vaccines and subunit vaccines, which have shown particular promise for oral delivery. These types offer a favorable balance of immunogenicity and safety profiles suitable for oral administration. The ongoing advancements in mRNA and viral vector technologies are also expected to create new opportunities for oral delivery systems.

- Key Drivers in North America:

- High R&D expenditure and strong investment in biotechnology.

- Supportive regulatory pathways for novel vaccine approvals.

- Significant market demand for patient-friendly healthcare solutions.

- Established healthcare infrastructure for widespread vaccine distribution.

- Dominant Application Segment: Pediatric Oral Vaccines

- Addresses significant unmet needs in childhood immunization.

- Reduces vaccine hesitancy and improves compliance.

- High potential for future indications.

- Key Types Driving Growth:

- Live-attenuated oral vaccines for well-established efficacy.

- Subunit oral vaccines offering enhanced safety.

- Emerging platforms like mRNA and viral vectors adapted for oral delivery.

Oral Vaccination Market 2029 Product Landscape

The oral vaccination market in 2029 is witnessing a wave of product innovations focused on enhancing stability, efficacy, and patient compliance. Novel formulations utilizing enteric coatings, microencapsulation, and mucoadhesive polymers are key to protecting antigens from degradation in the gastrointestinal tract and promoting targeted immune responses. These advancements are enabling the development of oral vaccines for a wider range of infectious diseases, moving beyond historically challenging targets. Unique selling propositions include the elimination of needle-related pain and anxiety, simplified administration, and reduced healthcare professional burden. Technological advancements in antigen engineering and adjuvant development are further bolstering the immunogenicity of oral vaccine candidates, bringing them closer to widespread clinical adoption.

Key Drivers, Barriers & Challenges in Oral Vaccination 2029

The oral vaccination market in 2029 is propelled by several key drivers. The fundamental driver is the pursuit of improved vaccine accessibility and patient compliance, directly addressing needle phobia and reducing the burden on healthcare systems. Technological advancements in oral vaccine delivery systems, such as nano-encapsulation and enteric coatings, are overcoming previous biological hurdles. Furthermore, the growing demand for pandemic preparedness and routine preventative healthcare solutions is creating a fertile ground for innovative vaccine formats.

However, significant barriers and challenges persist. The primary challenge lies in achieving comparable immunogenicity and durability of immune response to traditional injectable vaccines, requiring substantial R&D investment. Regulatory hurdles, while necessary for safety, can lead to lengthy approval processes. Supply chain complexities for novel formulations and the cost of developing and manufacturing these advanced oral vaccines also present substantial obstacles. Competitive pressures from established injectable vaccine markets and the need for extensive public education campaigns to foster trust and acceptance are also critical factors.

Emerging Opportunities in Oral Vaccination 2029

Emerging opportunities in the oral vaccination market for 2029 are vast and diverse. A significant untapped market lies in developing countries where the logistics of cold chain management for injectable vaccines are challenging; oral vaccines offer a potential solution for widespread immunization campaigns. Innovative applications for chronic disease prevention and therapeutic vaccines are also gaining traction. Evolving consumer preferences for convenient and less invasive healthcare interventions continue to drive demand for novel oral formulations. Furthermore, the potential for self-administration and home-based vaccination programs presents a transformative opportunity, especially for routine immunizations and in managing public health crises.

Growth Accelerators in the Oral Vaccination 2029 Industry

Several catalysts are accelerating the growth of the oral vaccination industry. Technological breakthroughs in platform technologies, particularly in oral vaccine formulation and antigen stabilization, are crucial. Strategic partnerships between academic research institutions and large pharmaceutical companies are expediting the translation of promising research into viable products. Furthermore, expanding market access through global health initiatives and government-backed vaccination programs are key market expansion strategies. The development of oral vaccines for emerging infectious diseases and the adaptation of existing vaccine technologies for oral delivery are also significant growth accelerators.

Key Players Shaping the Oral Vaccination 2029 Market

- Pfizer Inc.

- Moderna, Inc.

- Sanofi S.A.

- GlaxoSmithKline plc

- AstraZeneca PLC

- Merck & Co., Inc.

- Johnson & Johnson

- CureVac AG

- Vaxart, Inc.

- Bharat Biotech International Limited

- Sinovac Biotech Ltd.

Notable Milestones in Oral Vaccination 2029 Sector

- 2021/08: Approval of a novel oral rotavirus vaccine in a key emerging market, demonstrating high efficacy and ease of administration.

- 2022/03: Successful completion of Phase III clinical trials for an oral polio vaccine booster, showing non-inferiority to existing injectable formulations.

- 2022/11: Significant funding secured by a biotech startup for the development of an oral mRNA vaccine platform.

- 2023/05: Collaboration announced between a major pharmaceutical company and a leading academic institution to explore oral vaccine delivery for influenza.

- 2023/10: Positive preclinical data published for an oral vaccine targeting a common respiratory pathogen.

- 2024/02: Regulatory agency grants fast-track designation for an oral vaccine candidate for a neglected tropical disease.

- 2024/07: A breakthrough in encapsulation technology promises enhanced oral vaccine stability and bioavailability.

In-Depth Oral Vaccination 2029 Market Outlook

The oral vaccination market is set for a period of significant expansion and transformation. Growth accelerators such as advancements in mRNA and subunit vaccine technologies, coupled with improved oral delivery systems, will drive innovation and expand the therapeutic applications of oral vaccines. Strategic partnerships and increasing investment in R&D by major pharmaceutical players will further fuel this growth. The market is ripe with opportunities for companies that can effectively navigate regulatory pathways and demonstrate the superior patient convenience and logistical advantages of their oral vaccine products, particularly in pediatric and global health settings.

oral vaccination 2029 Segmentation

- 1. Application

- 2. Types

oral vaccination 2029 Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

oral vaccination 2029 Regional Market Share

Geographic Coverage of oral vaccination 2029

oral vaccination 2029 REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.53% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global oral vaccination 2029 Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America oral vaccination 2029 Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America oral vaccination 2029 Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe oral vaccination 2029 Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa oral vaccination 2029 Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific oral vaccination 2029 Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1. Global and United States

List of Figures

- Figure 1: Global oral vaccination 2029 Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global oral vaccination 2029 Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America oral vaccination 2029 Revenue (billion), by Application 2025 & 2033

- Figure 4: North America oral vaccination 2029 Volume (K), by Application 2025 & 2033

- Figure 5: North America oral vaccination 2029 Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America oral vaccination 2029 Volume Share (%), by Application 2025 & 2033

- Figure 7: North America oral vaccination 2029 Revenue (billion), by Types 2025 & 2033

- Figure 8: North America oral vaccination 2029 Volume (K), by Types 2025 & 2033

- Figure 9: North America oral vaccination 2029 Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America oral vaccination 2029 Volume Share (%), by Types 2025 & 2033

- Figure 11: North America oral vaccination 2029 Revenue (billion), by Country 2025 & 2033

- Figure 12: North America oral vaccination 2029 Volume (K), by Country 2025 & 2033

- Figure 13: North America oral vaccination 2029 Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America oral vaccination 2029 Volume Share (%), by Country 2025 & 2033

- Figure 15: South America oral vaccination 2029 Revenue (billion), by Application 2025 & 2033

- Figure 16: South America oral vaccination 2029 Volume (K), by Application 2025 & 2033

- Figure 17: South America oral vaccination 2029 Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America oral vaccination 2029 Volume Share (%), by Application 2025 & 2033

- Figure 19: South America oral vaccination 2029 Revenue (billion), by Types 2025 & 2033

- Figure 20: South America oral vaccination 2029 Volume (K), by Types 2025 & 2033

- Figure 21: South America oral vaccination 2029 Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America oral vaccination 2029 Volume Share (%), by Types 2025 & 2033

- Figure 23: South America oral vaccination 2029 Revenue (billion), by Country 2025 & 2033

- Figure 24: South America oral vaccination 2029 Volume (K), by Country 2025 & 2033

- Figure 25: South America oral vaccination 2029 Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America oral vaccination 2029 Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe oral vaccination 2029 Revenue (billion), by Application 2025 & 2033

- Figure 28: Europe oral vaccination 2029 Volume (K), by Application 2025 & 2033

- Figure 29: Europe oral vaccination 2029 Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe oral vaccination 2029 Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe oral vaccination 2029 Revenue (billion), by Types 2025 & 2033

- Figure 32: Europe oral vaccination 2029 Volume (K), by Types 2025 & 2033

- Figure 33: Europe oral vaccination 2029 Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe oral vaccination 2029 Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe oral vaccination 2029 Revenue (billion), by Country 2025 & 2033

- Figure 36: Europe oral vaccination 2029 Volume (K), by Country 2025 & 2033

- Figure 37: Europe oral vaccination 2029 Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe oral vaccination 2029 Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa oral vaccination 2029 Revenue (billion), by Application 2025 & 2033

- Figure 40: Middle East & Africa oral vaccination 2029 Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa oral vaccination 2029 Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa oral vaccination 2029 Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa oral vaccination 2029 Revenue (billion), by Types 2025 & 2033

- Figure 44: Middle East & Africa oral vaccination 2029 Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa oral vaccination 2029 Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa oral vaccination 2029 Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa oral vaccination 2029 Revenue (billion), by Country 2025 & 2033

- Figure 48: Middle East & Africa oral vaccination 2029 Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa oral vaccination 2029 Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa oral vaccination 2029 Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific oral vaccination 2029 Revenue (billion), by Application 2025 & 2033

- Figure 52: Asia Pacific oral vaccination 2029 Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific oral vaccination 2029 Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific oral vaccination 2029 Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific oral vaccination 2029 Revenue (billion), by Types 2025 & 2033

- Figure 56: Asia Pacific oral vaccination 2029 Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific oral vaccination 2029 Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific oral vaccination 2029 Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific oral vaccination 2029 Revenue (billion), by Country 2025 & 2033

- Figure 60: Asia Pacific oral vaccination 2029 Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific oral vaccination 2029 Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific oral vaccination 2029 Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global oral vaccination 2029 Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global oral vaccination 2029 Volume K Forecast, by Application 2020 & 2033

- Table 3: Global oral vaccination 2029 Revenue billion Forecast, by Types 2020 & 2033

- Table 4: Global oral vaccination 2029 Volume K Forecast, by Types 2020 & 2033

- Table 5: Global oral vaccination 2029 Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global oral vaccination 2029 Volume K Forecast, by Region 2020 & 2033

- Table 7: Global oral vaccination 2029 Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Global oral vaccination 2029 Volume K Forecast, by Application 2020 & 2033

- Table 9: Global oral vaccination 2029 Revenue billion Forecast, by Types 2020 & 2033

- Table 10: Global oral vaccination 2029 Volume K Forecast, by Types 2020 & 2033

- Table 11: Global oral vaccination 2029 Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global oral vaccination 2029 Volume K Forecast, by Country 2020 & 2033

- Table 13: United States oral vaccination 2029 Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United States oral vaccination 2029 Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada oral vaccination 2029 Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada oral vaccination 2029 Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico oral vaccination 2029 Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Mexico oral vaccination 2029 Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global oral vaccination 2029 Revenue billion Forecast, by Application 2020 & 2033

- Table 20: Global oral vaccination 2029 Volume K Forecast, by Application 2020 & 2033

- Table 21: Global oral vaccination 2029 Revenue billion Forecast, by Types 2020 & 2033

- Table 22: Global oral vaccination 2029 Volume K Forecast, by Types 2020 & 2033

- Table 23: Global oral vaccination 2029 Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global oral vaccination 2029 Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil oral vaccination 2029 Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Brazil oral vaccination 2029 Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina oral vaccination 2029 Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Argentina oral vaccination 2029 Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America oral vaccination 2029 Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America oral vaccination 2029 Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global oral vaccination 2029 Revenue billion Forecast, by Application 2020 & 2033

- Table 32: Global oral vaccination 2029 Volume K Forecast, by Application 2020 & 2033

- Table 33: Global oral vaccination 2029 Revenue billion Forecast, by Types 2020 & 2033

- Table 34: Global oral vaccination 2029 Volume K Forecast, by Types 2020 & 2033

- Table 35: Global oral vaccination 2029 Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global oral vaccination 2029 Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom oral vaccination 2029 Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom oral vaccination 2029 Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany oral vaccination 2029 Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Germany oral vaccination 2029 Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France oral vaccination 2029 Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: France oral vaccination 2029 Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy oral vaccination 2029 Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Italy oral vaccination 2029 Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain oral vaccination 2029 Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Spain oral vaccination 2029 Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia oral vaccination 2029 Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Russia oral vaccination 2029 Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux oral vaccination 2029 Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Benelux oral vaccination 2029 Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics oral vaccination 2029 Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Nordics oral vaccination 2029 Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe oral vaccination 2029 Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe oral vaccination 2029 Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global oral vaccination 2029 Revenue billion Forecast, by Application 2020 & 2033

- Table 56: Global oral vaccination 2029 Volume K Forecast, by Application 2020 & 2033

- Table 57: Global oral vaccination 2029 Revenue billion Forecast, by Types 2020 & 2033

- Table 58: Global oral vaccination 2029 Volume K Forecast, by Types 2020 & 2033

- Table 59: Global oral vaccination 2029 Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global oral vaccination 2029 Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey oral vaccination 2029 Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Turkey oral vaccination 2029 Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel oral vaccination 2029 Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Israel oral vaccination 2029 Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC oral vaccination 2029 Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: GCC oral vaccination 2029 Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa oral vaccination 2029 Revenue (billion) Forecast, by Application 2020 & 2033

- Table 68: North Africa oral vaccination 2029 Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa oral vaccination 2029 Revenue (billion) Forecast, by Application 2020 & 2033

- Table 70: South Africa oral vaccination 2029 Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa oral vaccination 2029 Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa oral vaccination 2029 Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global oral vaccination 2029 Revenue billion Forecast, by Application 2020 & 2033

- Table 74: Global oral vaccination 2029 Volume K Forecast, by Application 2020 & 2033

- Table 75: Global oral vaccination 2029 Revenue billion Forecast, by Types 2020 & 2033

- Table 76: Global oral vaccination 2029 Volume K Forecast, by Types 2020 & 2033

- Table 77: Global oral vaccination 2029 Revenue billion Forecast, by Country 2020 & 2033

- Table 78: Global oral vaccination 2029 Volume K Forecast, by Country 2020 & 2033

- Table 79: China oral vaccination 2029 Revenue (billion) Forecast, by Application 2020 & 2033

- Table 80: China oral vaccination 2029 Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India oral vaccination 2029 Revenue (billion) Forecast, by Application 2020 & 2033

- Table 82: India oral vaccination 2029 Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan oral vaccination 2029 Revenue (billion) Forecast, by Application 2020 & 2033

- Table 84: Japan oral vaccination 2029 Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea oral vaccination 2029 Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: South Korea oral vaccination 2029 Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN oral vaccination 2029 Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: ASEAN oral vaccination 2029 Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania oral vaccination 2029 Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: Oceania oral vaccination 2029 Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific oral vaccination 2029 Revenue (billion) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific oral vaccination 2029 Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the oral vaccination 2029?

The projected CAGR is approximately 9.53%.

2. Which companies are prominent players in the oral vaccination 2029?

Key companies in the market include Global and United States.

3. What are the main segments of the oral vaccination 2029?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 4.24 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4350.00, USD 6525.00, and USD 8700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "oral vaccination 2029," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the oral vaccination 2029 report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the oral vaccination 2029?

To stay informed about further developments, trends, and reports in the oral vaccination 2029, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence