Key Insights

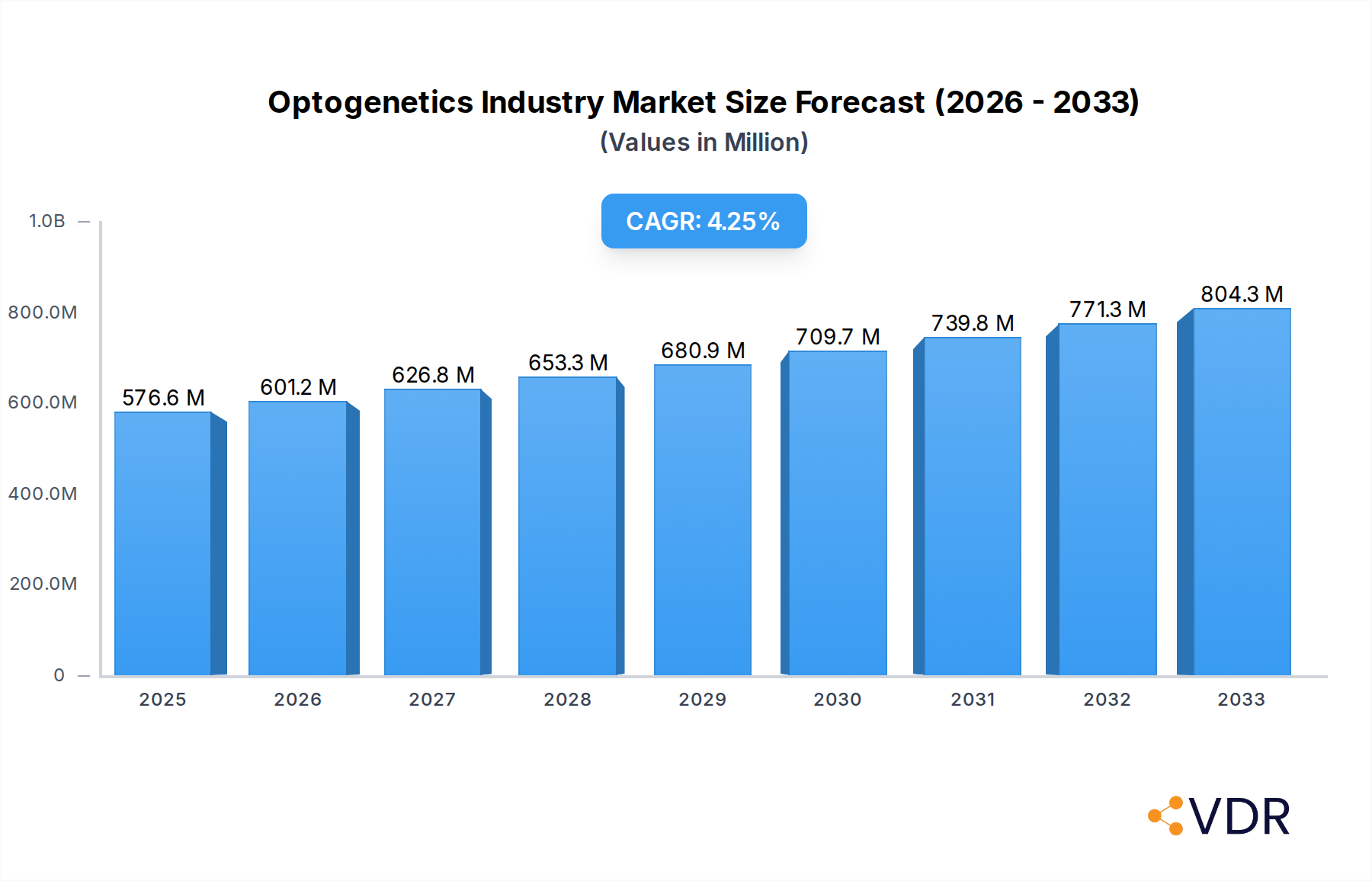

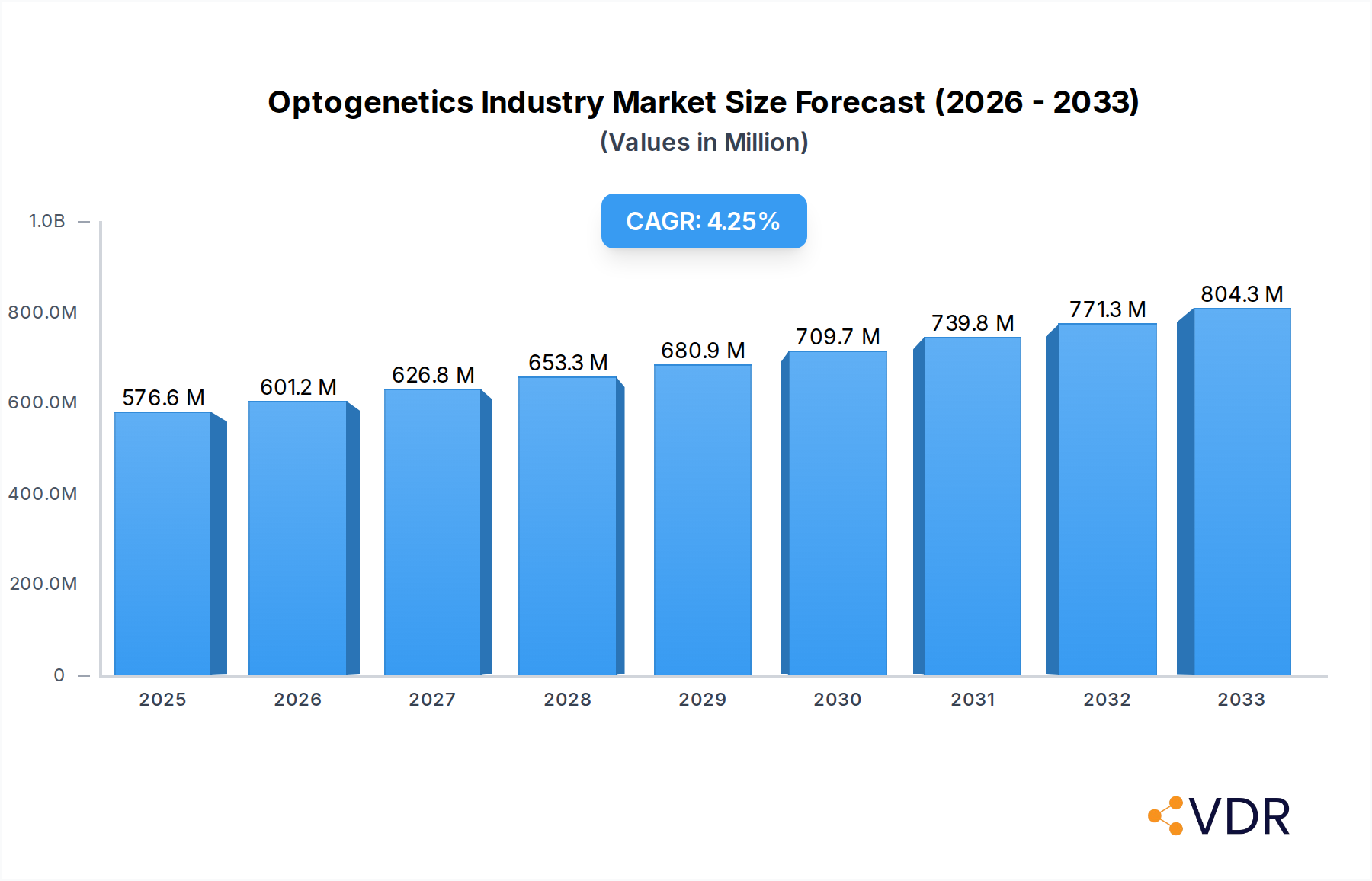

The global Optogenetics market is poised for significant expansion, projected to reach $576.57 million by 2025. This growth is fueled by the rapid advancements in neuroscience research, enabling precise control over neural circuits and offering novel therapeutic avenues. The market is expected to witness a Compound Annual Growth Rate (CAGR) of 4.29% during the forecast period of 2025-2033, indicating a steady and robust upward trajectory. Key drivers include the increasing demand for sophisticated tools for understanding brain function, the development of gene therapy techniques for treating neurological and visual disorders, and the growing investment in research and development by both academic institutions and pharmaceutical companies. The application of optogenetics in behavioral tracking and the exploration of its potential in retinal disease treatment are also contributing to this market momentum.

Optogenetics Industry Market Size (In Million)

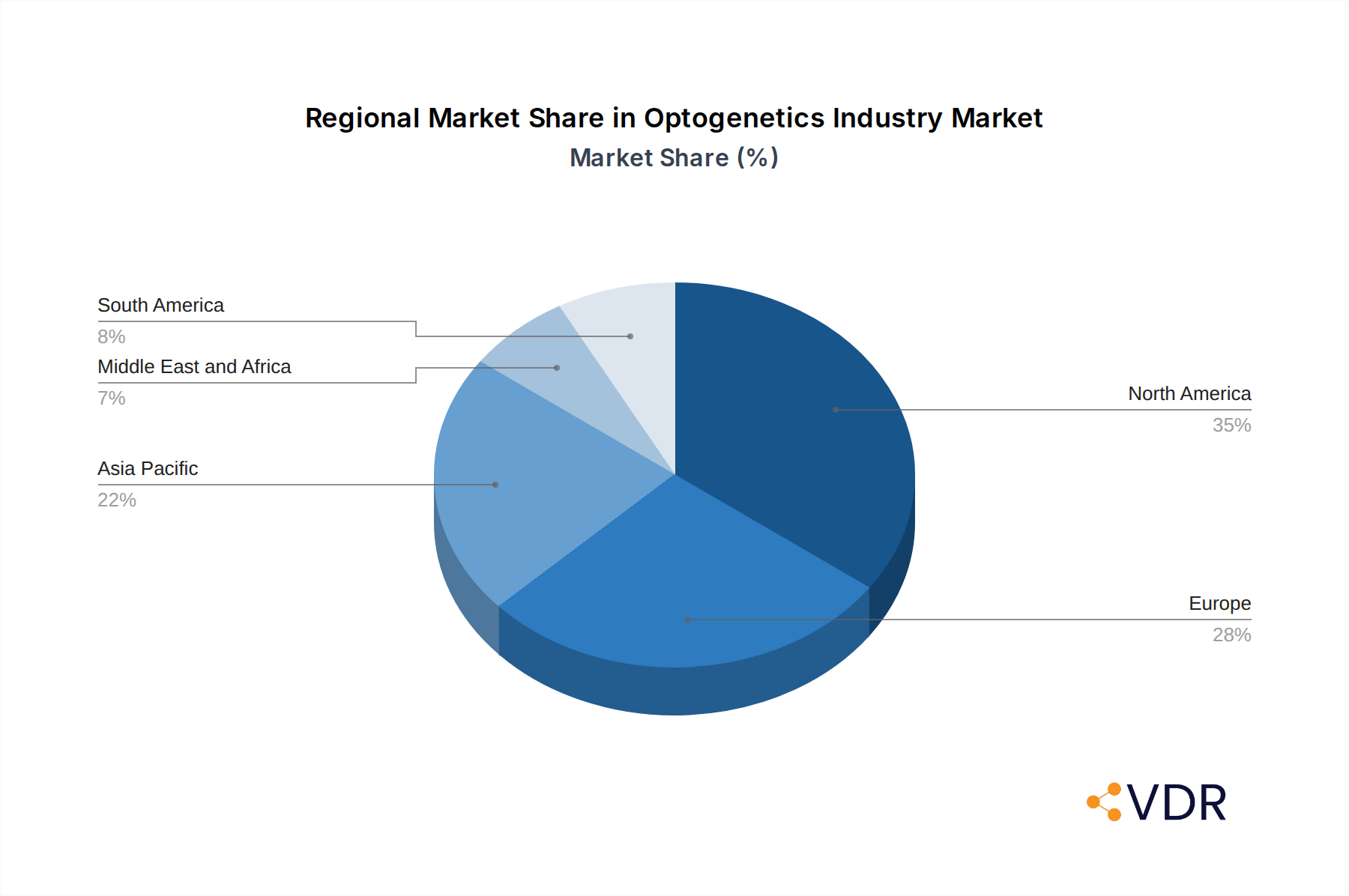

The market's segmentation highlights a dynamic landscape. In terms of light equipment, both Laser and Light-emitting Diode (LED) technologies are integral, with ongoing innovation enhancing their precision and applicability. The actuator segment, featuring Channelrhodopsin, Halorhodopsin, and Archaerhodopsin, is critical for light-induced neural activity modulation. Furthermore, the development of advanced sensors like Calcium, Chloride (Clomeleon), and Membrane-gated (Mermaid) sensors is expanding the scope of optogenetic investigations. Geographically, North America is anticipated to lead the market due to substantial R&D funding and a strong presence of leading research institutions. However, Asia Pacific is expected to exhibit the fastest growth, driven by increasing investments and a burgeoning research ecosystem. While the market presents immense opportunities, challenges such as the high cost of specialized equipment and the need for skilled personnel may pose moderate restraints.

Optogenetics Industry Company Market Share

This comprehensive report delves into the burgeoning optogenetics market, offering an in-depth analysis of its dynamics, growth trends, and future potential. Harnessing advanced light-based technologies, optogenetics is revolutionizing our understanding of neural circuits and paving the way for groundbreaking therapeutic interventions. This report forecasts significant growth, driven by increasing research investments and the development of novel applications.

Optogenetics Industry Market Dynamics & Structure

The optogenetics industry is characterized by a dynamic and evolving market structure, driven by rapid technological advancements and a growing understanding of neurological disorders. Market concentration is moderate, with several key players vying for dominance, particularly in the Light Equipment and Actuator segments. Technological innovation is the primary driver, fueled by continuous research into more precise and efficient light delivery systems and genetic tools. Neuroscience research remains the dominant application, but significant growth is anticipated in Retinal Disease Treatment and Behavioral Tracking. Regulatory frameworks are still developing, with a focus on ensuring the safety and efficacy of optogenetic therapies. Competitive product substitutes are limited due to the unique nature of optogenetics, but advancements in other neuromodulation techniques could present indirect competition. End-user demographics are primarily academic and research institutions, with a growing segment of pharmaceutical and biotechnology companies exploring therapeutic applications. Mergers and acquisitions (M&A) trends are expected to increase as larger companies seek to acquire specialized optogenetics technologies and expertise. In 2024, the market saw an estimated xx M&A deals, with an average deal value of $xx Million. Barriers to innovation include the high cost of specialized equipment and the complexity of genetic engineering.

- Market Concentration: Moderate, with increasing consolidation expected.

- Technological Innovation Drivers: Development of novel opsins, advanced light sources, and miniaturized delivery systems.

- Regulatory Frameworks: Emerging, focusing on safety, efficacy, and ethical considerations.

- Competitive Product Substitutes: Indirect competition from other neuromodulation techniques.

- End-User Demographics: Academic/research institutions, pharmaceutical & biotechnology companies.

- M&A Trends: Anticipated increase in deal volume and value.

- Innovation Barriers: High cost of equipment, genetic engineering complexity.

Optogenetics Industry Growth Trends & Insights

The global optogenetics market is poised for robust expansion, exhibiting a significant Compound Annual Growth Rate (CAGR) of approximately 15.8% from 2025 to 2033. This growth is underpinned by increasing global healthcare expenditures and a heightened focus on understanding complex neurological conditions like Parkinson's disease, epilepsy, and Alzheimer's disease. The market size is projected to reach an estimated $7,234.5 Million in 2025, growing from $3,500.0 Million in 2019. Adoption rates are steadily increasing as researchers become more familiar with optogenetic tools and their potential. Technological disruptions are continually emerging, with advancements in deep brain stimulation technologies and the development of wireless optogenetic systems significantly enhancing research capabilities and therapeutic potential. Consumer behavior shifts are observed, with a growing demand for personalized medicine and less invasive treatment options, areas where optogenetics holds immense promise. The increasing integration of artificial intelligence (AI) in analyzing optogenetic data is also contributing to faster research insights and therapeutic development. Furthermore, the growing pipeline of optogenetic therapies in clinical trials, particularly for rare genetic eye diseases, is a major indicator of future market penetration. The market penetration of optogenetics in neuroscience research is estimated to be around 45% in 2025, with significant room for growth. The successful translation of preclinical research into clinical applications will be a key determinant of future market share expansion. The expanding applications in animal research for drug discovery and development also represent a substantial growth avenue.

Dominant Regions, Countries, or Segments in Optogenetics Industry

North America currently dominates the global optogenetics market, driven by its strong research infrastructure, substantial government funding for scientific research, and the presence of leading academic institutions and biotechnology companies. The United States, in particular, is a powerhouse, with a significant share of global optogenetics research output and commercialization activities. This dominance is further solidified by substantial investments in neuroscience research and development, coupled with favorable regulatory environments for novel therapeutic development.

- North America: Leading region due to robust research ecosystem, funding, and industry presence.

- Key Drivers: Government funding for neuroscience research, presence of top-tier universities and biotech firms, advanced technological adoption.

- Market Share: Estimated at 40% in 2025.

- Growth Potential: High, driven by ongoing innovation and clinical trial advancements.

The Light Equipment segment, specifically Laser technology, is a primary growth driver within the market. Lasers offer the precision and wavelength control essential for activating specific neuronal populations, making them indispensable for sophisticated optogenetic experiments.

- Dominant Segment: Light Equipment (Laser): Crucial for precise neuronal activation.

- Key Drivers: Need for high-resolution spatial and temporal control of neural activity.

- Market Share: Estimated at 35% of the Light Equipment segment.

- Growth Potential: Strong, driven by advancements in laser miniaturization and efficiency.

In terms of applications, Neuroscience remains the most dominant segment, accounting for over 60% of the market share. This is attributed to the extensive use of optogenetics in unraveling complex brain functions, understanding neurological disorders, and developing novel therapeutic strategies.

- Dominant Application: Neuroscience: Foundation of optogenetics research.

- Key Drivers: Unraveling brain function, understanding neurological diseases, developing novel therapeutic targets.

- Market Share: Estimated at 65% of the total Applications segment.

- Growth Potential: Sustained high growth due to continued research demand.

Retinal Disease Treatment is an emerging and rapidly growing application segment, with significant potential for commercialization. Advancements in optogenetic therapies for conditions like retinitis pigmentosa are nearing clinical success, attracting substantial investment and driving market expansion.

- Emerging Application: Retinal Disease Treatment: High therapeutic potential and nearing clinical success.

- Key Drivers: Unmet medical needs in vision restoration, promising clinical trial results.

- Market Share: Projected CAGR of 20% from 2025-2033.

- Growth Potential: Very High, with significant commercialization prospects.

Optogenetics Industry Product Landscape

The optogenetics product landscape is characterized by rapid innovation, focusing on enhancing precision, versatility, and ease of use. Key product developments include advanced laser systems offering unparalleled temporal and spatial resolution for targeted neuronal activation, and novel opsins engineered for specific cellular responses and improved photosensitivity. Actuators like channelrhodopsins and halorhodopsins are continuously being refined for greater specificity and reduced photodamage. Sensor technologies, such as calcium and membrane-gated sensors, are evolving to provide real-time monitoring of neural activity with higher sensitivity and faster kinetics. The development of integrated systems, combining light delivery, genetic tools, and sophisticated data acquisition, is a significant trend, offering researchers comprehensive solutions for complex experiments.

Key Drivers, Barriers & Challenges in Optogenetics Industry

Key Drivers:

- Technological Advancements: Continuous innovation in light sources, genetic tools, and delivery systems.

- Growing Neuroscience Research: Increased investment in understanding brain function and neurological disorders.

- Therapeutic Potential: Promising applications in treating blindness, Parkinson's, and other neurological conditions.

- Government Funding: Support from research grants and initiatives for cutting-edge science.

Barriers & Challenges:

- High Cost of Equipment: Specialized lasers and genetic engineering tools are expensive.

- Technical Expertise Required: Implementing optogenetics demands specialized knowledge and skills.

- Regulatory Hurdles: Navigating the approval process for therapeutic applications can be lengthy.

- Ethical Considerations: Discussions surrounding germline gene editing and the long-term implications of neuromodulation.

- Supply Chain Issues: Ensuring consistent availability of specialized reagents and components. The global supply chain for rare earth elements used in some laser components experienced disruptions in 2023, impacting production by an estimated 5%.

Emerging Opportunities in Optogenetics Industry

Emerging opportunities in the optogenetics industry lie in expanding therapeutic applications beyond current research focus areas. The development of non-invasive optogenetic techniques, such as using near-infrared light for deeper tissue penetration, presents a significant avenue for growth. Furthermore, the integration of optogenetics with other advanced technologies like artificial intelligence and machine learning for personalized treatment strategies and diagnostics holds immense potential. The exploration of optogenetics in treating psychiatric disorders, such as depression and anxiety, is also a rapidly developing area. The untapped market for optogenetic tools in veterinary medicine for research purposes also presents a niche but growing opportunity.

Growth Accelerators in the Optogenetics Industry Industry

Several key catalysts are accelerating the growth of the optogenetics industry. Technological breakthroughs, such as the development of more efficient and less phototoxic opsins, are expanding the applicability and safety profile of optogenetic interventions. Strategic partnerships between academic institutions and commercial entities are crucial for translating research findings into viable products and therapies. Market expansion strategies, including the development of user-friendly, integrated optogenetic systems, are making these advanced tools more accessible to a broader research community. The increasing number of clinical trials demonstrating positive outcomes in treating specific conditions is also a major growth accelerator, attracting further investment and driving market demand.

Key Players Shaping the Optogenetics Industry Market

- Coherent Inc

- Gensight Biologics

- Thorlabs Inc

- Judges Scientific PLC (Scientifica)

- Laserglow Technologies

- Shanghai Laser & Optics Century Co Ltd

- Hubner Group (Cobolt Inc )

- Bruker Corporation

- Noldus Information Technology

Notable Milestones in Optogenetics Industry Sector

- February 2023: GenSight Biologics announced the 1 Year safety data and efficacy signals from the PIONEER phase I/II clinical trial of GS030, an optogenetic treatment candidate for retinitis pigmentosa.

- June 2022: Bruker Corporation launched the NeuraLight 3D Ultra module to support advanced neuroscience and optogenetics research applications on Bruker's Ultima multiphoton microscopes.

In-Depth Optogenetics Industry Market Outlook

The future outlook for the optogenetics industry is exceptionally promising, driven by its transformative potential in neuroscience and medicine. Growth accelerators, including ongoing breakthroughs in opsin engineering and light delivery technologies, will continue to expand the toolkit for researchers and clinicians. Strategic partnerships between innovators and pharmaceutical giants will be instrumental in translating the vast research potential into tangible therapeutic solutions, particularly in areas like vision restoration and neurodegenerative disease management. The increasing demand for personalized and targeted treatments will further fuel market expansion. The global market is projected to witness sustained double-digit growth throughout the forecast period, with significant opportunities in emerging economies adopting advanced research methodologies.

Optogenetics Industry Segmentation

-

1. Light Equipment

- 1.1. Laser

- 1.2. Light-emitting Diode (LED)

-

2. Actuator

- 2.1. Channelrhodopsin

- 2.2. Halorhodopsin

- 2.3. Archaerhodopsin

-

3. Sensor

- 3.1. Calcium

- 3.2. Chloride (Clomeleon)

- 3.3. Membrane-gated (Mermaid)

- 3.4. Other Sensors

-

4. Application

- 4.1. Neuroscience

- 4.2. Behavioral Tracking

- 4.3. Retinal Disease Treatment

- 4.4. Other Applications

Optogenetics Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Optogenetics Industry Regional Market Share

Geographic Coverage of Optogenetics Industry

Optogenetics Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.29% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Light Equipment

- 5.1.1. Laser

- 5.1.2. Light-emitting Diode (LED)

- 5.2. Market Analysis, Insights and Forecast - by Actuator

- 5.2.1. Channelrhodopsin

- 5.2.2. Halorhodopsin

- 5.2.3. Archaerhodopsin

- 5.3. Market Analysis, Insights and Forecast - by Sensor

- 5.3.1. Calcium

- 5.3.2. Chloride (Clomeleon)

- 5.3.3. Membrane-gated (Mermaid)

- 5.3.4. Other Sensors

- 5.4. Market Analysis, Insights and Forecast - by Application

- 5.4.1. Neuroscience

- 5.4.2. Behavioral Tracking

- 5.4.3. Retinal Disease Treatment

- 5.4.4. Other Applications

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. Europe

- 5.5.3. Asia Pacific

- 5.5.4. Middle East and Africa

- 5.5.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Light Equipment

- 6. Global Optogenetics Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Light Equipment

- 6.1.1. Laser

- 6.1.2. Light-emitting Diode (LED)

- 6.2. Market Analysis, Insights and Forecast - by Actuator

- 6.2.1. Channelrhodopsin

- 6.2.2. Halorhodopsin

- 6.2.3. Archaerhodopsin

- 6.3. Market Analysis, Insights and Forecast - by Sensor

- 6.3.1. Calcium

- 6.3.2. Chloride (Clomeleon)

- 6.3.3. Membrane-gated (Mermaid)

- 6.3.4. Other Sensors

- 6.4. Market Analysis, Insights and Forecast - by Application

- 6.4.1. Neuroscience

- 6.4.2. Behavioral Tracking

- 6.4.3. Retinal Disease Treatment

- 6.4.4. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Light Equipment

- 7. North America Optogenetics Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Light Equipment

- 7.1.1. Laser

- 7.1.2. Light-emitting Diode (LED)

- 7.2. Market Analysis, Insights and Forecast - by Actuator

- 7.2.1. Channelrhodopsin

- 7.2.2. Halorhodopsin

- 7.2.3. Archaerhodopsin

- 7.3. Market Analysis, Insights and Forecast - by Sensor

- 7.3.1. Calcium

- 7.3.2. Chloride (Clomeleon)

- 7.3.3. Membrane-gated (Mermaid)

- 7.3.4. Other Sensors

- 7.4. Market Analysis, Insights and Forecast - by Application

- 7.4.1. Neuroscience

- 7.4.2. Behavioral Tracking

- 7.4.3. Retinal Disease Treatment

- 7.4.4. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Light Equipment

- 8. Europe Optogenetics Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Light Equipment

- 8.1.1. Laser

- 8.1.2. Light-emitting Diode (LED)

- 8.2. Market Analysis, Insights and Forecast - by Actuator

- 8.2.1. Channelrhodopsin

- 8.2.2. Halorhodopsin

- 8.2.3. Archaerhodopsin

- 8.3. Market Analysis, Insights and Forecast - by Sensor

- 8.3.1. Calcium

- 8.3.2. Chloride (Clomeleon)

- 8.3.3. Membrane-gated (Mermaid)

- 8.3.4. Other Sensors

- 8.4. Market Analysis, Insights and Forecast - by Application

- 8.4.1. Neuroscience

- 8.4.2. Behavioral Tracking

- 8.4.3. Retinal Disease Treatment

- 8.4.4. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Light Equipment

- 9. Asia Pacific Optogenetics Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Light Equipment

- 9.1.1. Laser

- 9.1.2. Light-emitting Diode (LED)

- 9.2. Market Analysis, Insights and Forecast - by Actuator

- 9.2.1. Channelrhodopsin

- 9.2.2. Halorhodopsin

- 9.2.3. Archaerhodopsin

- 9.3. Market Analysis, Insights and Forecast - by Sensor

- 9.3.1. Calcium

- 9.3.2. Chloride (Clomeleon)

- 9.3.3. Membrane-gated (Mermaid)

- 9.3.4. Other Sensors

- 9.4. Market Analysis, Insights and Forecast - by Application

- 9.4.1. Neuroscience

- 9.4.2. Behavioral Tracking

- 9.4.3. Retinal Disease Treatment

- 9.4.4. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Light Equipment

- 10. Middle East and Africa Optogenetics Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Light Equipment

- 10.1.1. Laser

- 10.1.2. Light-emitting Diode (LED)

- 10.2. Market Analysis, Insights and Forecast - by Actuator

- 10.2.1. Channelrhodopsin

- 10.2.2. Halorhodopsin

- 10.2.3. Archaerhodopsin

- 10.3. Market Analysis, Insights and Forecast - by Sensor

- 10.3.1. Calcium

- 10.3.2. Chloride (Clomeleon)

- 10.3.3. Membrane-gated (Mermaid)

- 10.3.4. Other Sensors

- 10.4. Market Analysis, Insights and Forecast - by Application

- 10.4.1. Neuroscience

- 10.4.2. Behavioral Tracking

- 10.4.3. Retinal Disease Treatment

- 10.4.4. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Light Equipment

- 11. South America Optogenetics Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Light Equipment

- 11.1.1. Laser

- 11.1.2. Light-emitting Diode (LED)

- 11.2. Market Analysis, Insights and Forecast - by Actuator

- 11.2.1. Channelrhodopsin

- 11.2.2. Halorhodopsin

- 11.2.3. Archaerhodopsin

- 11.3. Market Analysis, Insights and Forecast - by Sensor

- 11.3.1. Calcium

- 11.3.2. Chloride (Clomeleon)

- 11.3.3. Membrane-gated (Mermaid)

- 11.3.4. Other Sensors

- 11.4. Market Analysis, Insights and Forecast - by Application

- 11.4.1. Neuroscience

- 11.4.2. Behavioral Tracking

- 11.4.3. Retinal Disease Treatment

- 11.4.4. Other Applications

- 11.1. Market Analysis, Insights and Forecast - by Light Equipment

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Coherent Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Gensight Biologics

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Thorlabs Inc *List Not Exhaustive

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Judges Scientific PLC (Scientifica)

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Laserglow Technologies

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Shanghai Laser & Optics Century Co Ltd

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Hubner Group (Cobolt Inc )

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Bruker Corporation

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Noldus Information Technology

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.1 Coherent Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Optogenetics Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Optogenetics Industry Revenue (Million), by Light Equipment 2025 & 2033

- Figure 3: North America Optogenetics Industry Revenue Share (%), by Light Equipment 2025 & 2033

- Figure 4: North America Optogenetics Industry Revenue (Million), by Actuator 2025 & 2033

- Figure 5: North America Optogenetics Industry Revenue Share (%), by Actuator 2025 & 2033

- Figure 6: North America Optogenetics Industry Revenue (Million), by Sensor 2025 & 2033

- Figure 7: North America Optogenetics Industry Revenue Share (%), by Sensor 2025 & 2033

- Figure 8: North America Optogenetics Industry Revenue (Million), by Application 2025 & 2033

- Figure 9: North America Optogenetics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 10: North America Optogenetics Industry Revenue (Million), by Country 2025 & 2033

- Figure 11: North America Optogenetics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 12: Europe Optogenetics Industry Revenue (Million), by Light Equipment 2025 & 2033

- Figure 13: Europe Optogenetics Industry Revenue Share (%), by Light Equipment 2025 & 2033

- Figure 14: Europe Optogenetics Industry Revenue (Million), by Actuator 2025 & 2033

- Figure 15: Europe Optogenetics Industry Revenue Share (%), by Actuator 2025 & 2033

- Figure 16: Europe Optogenetics Industry Revenue (Million), by Sensor 2025 & 2033

- Figure 17: Europe Optogenetics Industry Revenue Share (%), by Sensor 2025 & 2033

- Figure 18: Europe Optogenetics Industry Revenue (Million), by Application 2025 & 2033

- Figure 19: Europe Optogenetics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 20: Europe Optogenetics Industry Revenue (Million), by Country 2025 & 2033

- Figure 21: Europe Optogenetics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Asia Pacific Optogenetics Industry Revenue (Million), by Light Equipment 2025 & 2033

- Figure 23: Asia Pacific Optogenetics Industry Revenue Share (%), by Light Equipment 2025 & 2033

- Figure 24: Asia Pacific Optogenetics Industry Revenue (Million), by Actuator 2025 & 2033

- Figure 25: Asia Pacific Optogenetics Industry Revenue Share (%), by Actuator 2025 & 2033

- Figure 26: Asia Pacific Optogenetics Industry Revenue (Million), by Sensor 2025 & 2033

- Figure 27: Asia Pacific Optogenetics Industry Revenue Share (%), by Sensor 2025 & 2033

- Figure 28: Asia Pacific Optogenetics Industry Revenue (Million), by Application 2025 & 2033

- Figure 29: Asia Pacific Optogenetics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Asia Pacific Optogenetics Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Asia Pacific Optogenetics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: Middle East and Africa Optogenetics Industry Revenue (Million), by Light Equipment 2025 & 2033

- Figure 33: Middle East and Africa Optogenetics Industry Revenue Share (%), by Light Equipment 2025 & 2033

- Figure 34: Middle East and Africa Optogenetics Industry Revenue (Million), by Actuator 2025 & 2033

- Figure 35: Middle East and Africa Optogenetics Industry Revenue Share (%), by Actuator 2025 & 2033

- Figure 36: Middle East and Africa Optogenetics Industry Revenue (Million), by Sensor 2025 & 2033

- Figure 37: Middle East and Africa Optogenetics Industry Revenue Share (%), by Sensor 2025 & 2033

- Figure 38: Middle East and Africa Optogenetics Industry Revenue (Million), by Application 2025 & 2033

- Figure 39: Middle East and Africa Optogenetics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 40: Middle East and Africa Optogenetics Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Middle East and Africa Optogenetics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: South America Optogenetics Industry Revenue (Million), by Light Equipment 2025 & 2033

- Figure 43: South America Optogenetics Industry Revenue Share (%), by Light Equipment 2025 & 2033

- Figure 44: South America Optogenetics Industry Revenue (Million), by Actuator 2025 & 2033

- Figure 45: South America Optogenetics Industry Revenue Share (%), by Actuator 2025 & 2033

- Figure 46: South America Optogenetics Industry Revenue (Million), by Sensor 2025 & 2033

- Figure 47: South America Optogenetics Industry Revenue Share (%), by Sensor 2025 & 2033

- Figure 48: South America Optogenetics Industry Revenue (Million), by Application 2025 & 2033

- Figure 49: South America Optogenetics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 50: South America Optogenetics Industry Revenue (Million), by Country 2025 & 2033

- Figure 51: South America Optogenetics Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Optogenetics Industry Revenue Million Forecast, by Light Equipment 2020 & 2033

- Table 2: Global Optogenetics Industry Revenue Million Forecast, by Actuator 2020 & 2033

- Table 3: Global Optogenetics Industry Revenue Million Forecast, by Sensor 2020 & 2033

- Table 4: Global Optogenetics Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 5: Global Optogenetics Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global Optogenetics Industry Revenue Million Forecast, by Light Equipment 2020 & 2033

- Table 7: Global Optogenetics Industry Revenue Million Forecast, by Actuator 2020 & 2033

- Table 8: Global Optogenetics Industry Revenue Million Forecast, by Sensor 2020 & 2033

- Table 9: Global Optogenetics Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 10: Global Optogenetics Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 11: United States Optogenetics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Canada Optogenetics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Mexico Optogenetics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Global Optogenetics Industry Revenue Million Forecast, by Light Equipment 2020 & 2033

- Table 15: Global Optogenetics Industry Revenue Million Forecast, by Actuator 2020 & 2033

- Table 16: Global Optogenetics Industry Revenue Million Forecast, by Sensor 2020 & 2033

- Table 17: Global Optogenetics Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 18: Global Optogenetics Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 19: Germany Optogenetics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: United Kingdom Optogenetics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: France Optogenetics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Italy Optogenetics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Spain Optogenetics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Rest of Europe Optogenetics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Global Optogenetics Industry Revenue Million Forecast, by Light Equipment 2020 & 2033

- Table 26: Global Optogenetics Industry Revenue Million Forecast, by Actuator 2020 & 2033

- Table 27: Global Optogenetics Industry Revenue Million Forecast, by Sensor 2020 & 2033

- Table 28: Global Optogenetics Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 29: Global Optogenetics Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 30: China Optogenetics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: Japan Optogenetics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: India Optogenetics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: Australia Optogenetics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: South Korea Optogenetics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: Rest of Asia Pacific Optogenetics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Global Optogenetics Industry Revenue Million Forecast, by Light Equipment 2020 & 2033

- Table 37: Global Optogenetics Industry Revenue Million Forecast, by Actuator 2020 & 2033

- Table 38: Global Optogenetics Industry Revenue Million Forecast, by Sensor 2020 & 2033

- Table 39: Global Optogenetics Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 40: Global Optogenetics Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 41: GCC Optogenetics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: South Africa Optogenetics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 43: Rest of Middle East and Africa Optogenetics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: Global Optogenetics Industry Revenue Million Forecast, by Light Equipment 2020 & 2033

- Table 45: Global Optogenetics Industry Revenue Million Forecast, by Actuator 2020 & 2033

- Table 46: Global Optogenetics Industry Revenue Million Forecast, by Sensor 2020 & 2033

- Table 47: Global Optogenetics Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 48: Global Optogenetics Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 49: Brazil Optogenetics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 50: Argentina Optogenetics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 51: Rest of South America Optogenetics Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Optogenetics Industry?

The projected CAGR is approximately 4.29%.

2. Which companies are prominent players in the Optogenetics Industry?

Key companies in the market include Coherent Inc, Gensight Biologics, Thorlabs Inc *List Not Exhaustive, Judges Scientific PLC (Scientifica), Laserglow Technologies, Shanghai Laser & Optics Century Co Ltd, Hubner Group (Cobolt Inc ), Bruker Corporation, Noldus Information Technology.

3. What are the main segments of the Optogenetics Industry?

The market segments include Light Equipment, Actuator, Sensor, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 576.57 Million as of 2022.

5. What are some drivers contributing to market growth?

Potential Diagnostic Tool in the Field of Neurosciences; Rapid Growth of Advanced Technology; Increasing Use of Multimodal Imaging.

6. What are the notable trends driving market growth?

Light-emitting Diode (LED) Segment is Expected to Hold a Significant Share in the Optogenetics Market.

7. Are there any restraints impacting market growth?

High Cost of Technology; Lack of Awareness.

8. Can you provide examples of recent developments in the market?

In February 2023, GenSight Biologics announced the 1 Year safety data and efficacy signals from the PIONEER phase I/II clinical trial of GS030, an optogenetic treatment candidate for retinitis pigmentosa.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Optogenetics Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Optogenetics Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Optogenetics Industry?

To stay informed about further developments, trends, and reports in the Optogenetics Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence