Key Insights

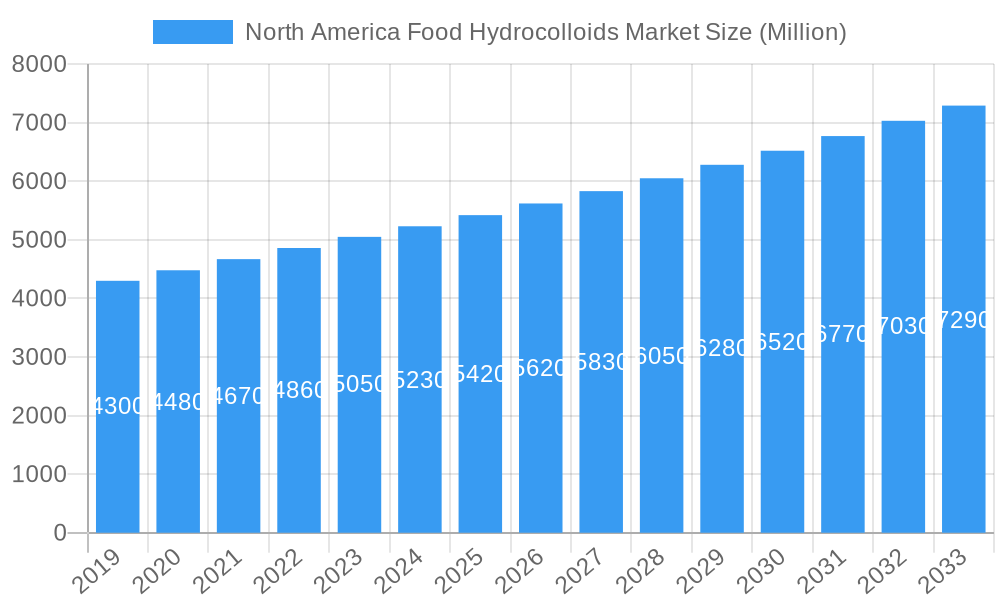

The North American Food Hydrocolloids Market is projected for substantial expansion, anticipated to reach $5,032 million by 2024, with a Compound Annual Growth Rate (CAGR) of 6.6% expected from 2024 to 2033. This growth is propelled by rising demand for convenient and processed foods, a strong consumer preference for clean-label ingredients, and advancements in food technology enhancing hydrocolloid applications. Key sectors like dairy, frozen products, bakery, and beverages will drive market growth by utilizing hydrocolloids for texture, stabilization, and shelf-life improvement. Emerging trends such as plant-based alternatives and the demand for reduced-sugar/fat products further increase the need for hydrocolloids to replicate traditional ingredient textures and structures.

North America Food Hydrocolloids Market Market Size (In Billion)

Challenges include raw material price fluctuations, evolving regulatory environments, and the emergence of alternative ingredients. Nevertheless, continuous new product development, focusing on sustainability and enhanced functionalities, is a significant industry trend. Major companies, including Cargill Incorporated and Archer Daniels Midland Company, are investing in R&D and strategic initiatives to broaden product offerings and market presence. The United States, Canada, and Mexico constitute a primary market due to a well-established food processing industry and high consumer expenditure. The wide array of applications, from confectionery to meat and seafood, highlights the indispensable role of hydrocolloids in contemporary food production.

North America Food Hydrocolloids Market Company Market Share

North America Food Hydrocolloids Market Report: Strategic Insights and Growth Forecast (2019-2033)

This comprehensive report offers an in-depth analysis of the North America Food Hydrocolloids Market, exploring its dynamics, growth trends, dominant segments, product landscape, and key influencing factors. Spanning the study period of 2019–2033, with a base year of 2025 and a forecast period of 2025–2033, this report provides actionable insights for stakeholders seeking to capitalize on this evolving market. We delve into the intricate interplay of market forces, technological advancements, and evolving consumer preferences that are shaping the future of food hydrocolloids across the United States, Canada, Mexico, and the rest of North America.

North America Food Hydrocolloids Market Market Dynamics & Structure

The North America Food Hydrocolloids Market is characterized by a moderate to high level of concentration, with key players like Cargill Incorporated, Ashland Global Holdings Inc, Archer Daniels Midland Company, J F Hydrocolloids Inc, Koninklijke DSM N V, DuPont, Behn Meyer Holding AG, and CP Kelco U S Inc holding significant market share. Technological innovation is a primary driver, with ongoing research focused on developing novel hydrocolloids with enhanced functionalities, improved stability, and cleaner labels. Regulatory frameworks, particularly those from the FDA in the United States and Health Canada, play a crucial role in defining product safety and permissible usage levels, influencing market access and product development strategies. The competitive landscape features a dynamic interplay of established players and emerging innovators, with a constant need to differentiate through product performance and cost-effectiveness. End-user demographics are increasingly influenced by growing health consciousness and demand for plant-based and clean-label ingredients, pushing manufacturers to reformulate products and explore sustainable sourcing. Mergers and acquisitions (M&A) remain a strategic tool for market consolidation, expanding product portfolios, and gaining access to new technologies or customer bases.

- Market Concentration: Moderately to highly concentrated, with a few key players dominating market share.

- Technological Innovation: Driven by the development of novel functionalities, improved stability, and clean-label solutions.

- Regulatory Influence: Strict adherence to FDA and Health Canada guidelines is paramount.

- Competitive Landscape: Characterized by both established giants and agile innovators.

- End-User Demographics: Shifting towards demand for healthier, plant-based, and clean-label ingredients.

- M&A Trends: Active M&A activity for market consolidation and portfolio expansion.

North America Food Hydrocolloids Market Growth Trends & Insights

The North America Food Hydrocolloids Market is poised for robust growth, projected to expand from an estimated $XX million in 2025 to reach $XX million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of XX% during the forecast period. This expansion is underpinned by several key trends, including the escalating demand for processed and convenience foods, where hydrocolloids are indispensable for texture modification, stabilization, and emulsification. The burgeoning health and wellness sector further fuels the market, as consumers increasingly seek products with natural ingredients, functional benefits, and improved nutritional profiles. Hydrocolloids derived from natural sources, such as pectin and guar gum, are witnessing heightened adoption rates, aligning with the clean-label movement. Technological disruptions, including advancements in extraction and modification techniques, are enabling the creation of hydrocolloids with tailored functionalities, catering to niche applications and premium product formulations. Consumer behavior shifts towards mindful eating and sustainable sourcing are compelling food manufacturers to prioritize ingredients with transparent supply chains and reduced environmental impact, further boosting the appeal of certain hydrocolloids. The penetration of hydrocolloids across diverse applications, from dairy and bakery to beverages and meat products, underscores their versatility and essential role in modern food production. The market is also influenced by the growing prevalence of chronic diseases, leading to a demand for low-sugar, low-fat, and gluten-free alternatives, where hydrocolloids act as crucial texturizers and stabilizers.

Dominant Regions, Countries, or Segments in North America Food Hydrocolloids Market

Within the North America Food Hydrocolloids Market, the United States stands out as the dominant region, accounting for the largest market share and exhibiting the highest growth potential. This dominance is attributed to several factors, including its large and sophisticated consumer base with a high disposable income, driving demand for a wide array of processed and specialty food products. The strong presence of major food manufacturers, coupled with a well-developed food processing industry, creates a significant demand pull for various hydrocolloids.

- United States: Leads market share due to a large consumer base, high disposable income, and advanced food processing industry.

- Key Drivers in the US:

- High consumption of dairy and frozen products, a major application segment.

- Robust bakery and confectionery industries requiring specific textural properties.

- Increasing demand for plant-based alternatives and clean-label ingredients.

- Significant R&D investment by leading hydrocolloid manufacturers.

- Favorable regulatory environment for food additives.

Among the Type segments, Xanthan Gum and Guar Gum are expected to witness substantial growth, driven by their extensive applications in gluten-free baking, sauces, dressings, and beverages. Their natural origin and cost-effectiveness make them highly sought after. Pectin is another key performer, particularly in the confectionery and dairy segments, owing to its gelling and stabilizing properties. Gelatin, while facing some scrutiny due to its animal origin, continues to hold a significant share in confectionery and dairy applications where its unique functionalities are difficult to replicate.

- Dominant Types: Xanthan Gum, Guar Gum, Pectin, and Gelatin are key growth drivers.

- Drivers for Dominant Types:

- Xanthan Gum & Guar Gum: Versatility in gluten-free products, sauces, and beverages; cost-effectiveness.

- Pectin: Essential for gelling in confectionery and stabilization in dairy products.

- Gelatin: Unique textural properties in confectionery and dairy, despite ethical considerations.

In terms of Application, Dairy and Frozen Products represent the largest segment, benefiting from the extensive use of hydrocolloids for texture, mouthfeel, and stability in products like ice cream, yogurt, and cheese. The Bakery segment follows closely, driven by the demand for improved dough handling, crumb structure, and shelf-life extension in bread and baked goods. The Beverages sector is also a significant contributor, utilizing hydrocolloids for viscosity control, suspension of pulp, and mouthfeel enhancement in juices, smoothies, and functional drinks.

- Dominant Applications: Dairy & Frozen Products, Bakery, and Beverages are key market segments.

- Drivers for Dominant Applications:

- Dairy & Frozen Products: Essential for texture, mouthfeel, and stability.

- Bakery: Improvement of dough, crumb structure, and shelf-life.

- Beverages: Viscosity control, pulp suspension, and mouthfeel enhancement.

North America Food Hydrocolloids Market Product Landscape

The North America Food Hydrocolloids Market product landscape is dynamic, marked by continuous innovation aimed at enhancing functionality, sustainability, and consumer appeal. Manufacturers are focusing on developing hydrocolloids with improved heat, acid, and shear stability, crucial for diverse processing conditions. Unique selling propositions include the development of plant-based alternatives to animal-derived hydrocolloids like gelatin, catering to vegetarian and vegan consumer bases. Technological advancements in encapsulation and modification are yielding hydrocolloids with tailored release properties and superior emulsifying capabilities. The trend towards clean labels is driving the demand for hydrocolloids derived from renewable and sustainable sources, with an emphasis on minimal processing.

Key Drivers, Barriers & Challenges in North America Food Hydrocolloids Market

Key Drivers: The North America Food Hydrocolloids Market is propelled by several significant factors. A primary driver is the continuously expanding processed food industry, where hydrocolloids are indispensable for achieving desired textures, stabilizing emulsions, and extending shelf life. The growing global population and urbanization further increase the demand for convenient and ready-to-eat food products, directly benefiting hydrocolloid consumption. The rising health consciousness among consumers has led to an increased demand for functional foods and beverages, which often incorporate hydrocolloids for texture and delivery of active ingredients. Furthermore, the trend towards plant-based diets is spurring innovation and demand for hydrocolloids derived from botanical sources. Technological advancements in extraction, purification, and modification of hydrocolloids are expanding their applicability and performance.

Barriers & Challenges: Despite its growth potential, the market faces several challenges. Fluctuations in the prices of raw materials, such as seaweed for carrageenan or plant-based sources for gums, can impact production costs and profit margins. Stringent regulatory requirements in different regions can create hurdles for product approval and market entry, demanding extensive testing and compliance. The availability of synthetic alternatives, though often less desirable from a clean-label perspective, can pose a competitive threat in certain applications. Consumer perception and potential health concerns associated with some hydrocolloids, even if unfounded, can lead to avoidance by manufacturers seeking to cater to consumer preferences. Supply chain disruptions, as seen in recent global events, can affect the availability and cost of raw materials, impacting production schedules and market stability.

Emerging Opportunities in North America Food Hydrocolloids Market

Emerging opportunities in the North America Food Hydrocolloids Market are primarily driven by evolving consumer preferences and technological advancements. The burgeoning demand for plant-based and vegan food products presents a significant avenue for hydrocolloids that can effectively mimic the functionality of animal-derived ingredients, such as gelatin. The clean-label movement continues to create opportunities for hydrocolloids derived from natural and sustainable sources, with transparent supply chains. Innovation in food technology, including the development of personalized nutrition and functional foods, will necessitate hydrocolloids with specific delivery and textural properties. Untapped markets within the convenience food sector, such as ready-to-drink nutritional shakes and meal replacements, offer considerable growth potential.

Growth Accelerators in the North America Food Hydrocolloids Market Industry

Several catalysts are accelerating the growth of the North America Food Hydrocolloids Market. Technological breakthroughs in modifying and refining existing hydrocolloids, leading to enhanced functionalities like improved gelling, thickening, and emulsifying capabilities, are pivotal. Strategic partnerships and collaborations between hydrocolloid manufacturers and food processing companies are fostering innovation and co-development of new applications. Market expansion strategies, including geographical diversification and penetration into emerging food categories, are also key growth accelerators. Investments in research and development to explore novel sources and sustainable production methods for hydrocolloids will further fuel long-term growth.

Key Players Shaping the North America Food Hydrocolloids Market Market

- Cargill Incorporated

- Ashland Global Holdings Inc

- Archer Daniels Midland Company

- J F Hydrocolloids Inc

- Koninklijke DSM N V

- DuPont

- Behn Meyer Holding AG

- CP Kelco U S Inc

Notable Milestones in North America Food Hydrocolloids Market Sector

- 2023: Launch of novel plant-based hydrocolloid blends by major manufacturers to cater to the growing vegan market.

- 2022: Significant investment in R&D for sustainable sourcing and production of seaweed-derived hydrocolloids.

- 2021: Increased M&A activity focused on acquiring companies with expertise in specialty hydrocolloids and clean-label ingredients.

- 2020: Enhanced focus on supply chain resilience and diversification of raw material sourcing due to global disruptions.

- 2019: Introduction of enhanced texture modification solutions for gluten-free bakery products.

In-Depth North America Food Hydrocolloids Market Market Outlook

The outlook for the North America Food Hydrocolloids Market remains highly promising, driven by persistent trends in food innovation and evolving consumer demands. Growth accelerators, including technological advancements in hydrocolloid functionality and sustainability, will continue to shape market dynamics. The strategic focus on developing clean-label, plant-based, and functional ingredients positions the market for sustained expansion. Opportunities lie in expanding applications within the burgeoning health and wellness sector, personalized nutrition, and the convenience food market. Collaboration and innovation will be critical for players to navigate regulatory landscapes and capitalize on emerging consumer preferences, ensuring a robust and dynamic future for this essential segment of the food industry.

North America Food Hydrocolloids Market Segmentation

-

1. Type

- 1.1. Gellan Gum

- 1.2. Carrageenan

- 1.3. Pectin

- 1.4. Xanthan Gum

- 1.5. Guar Gum

- 1.6. Gelatin

- 1.7. Others

-

2. Application

- 2.1. Dairy and Frozen Products

- 2.2. Bakery

- 2.3. Beverages

- 2.4. Confectionery

- 2.5. Meat and Seafood Products

- 2.6. Other Applications

-

3. Geography

-

3.1. North America

- 3.1.1. United States

- 3.1.2. Canada

- 3.1.3. Mexico

- 3.1.4. Rest of North America

-

3.1. North America

North America Food Hydrocolloids Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

- 1.4. Rest of North America

North America Food Hydrocolloids Market Regional Market Share

Geographic Coverage of North America Food Hydrocolloids Market

North America Food Hydrocolloids Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Demand for Low-Fat and Low-Calorie Food; Increasing Product Innovation

- 3.3. Market Restrains

- 3.3.1. ; Threat of New Entrants; Bargaining Power of Buyers/Consumers; Bargaining Power of Suppliers; Threat of Substitute Products; Degree Of Competition

- 3.4. Market Trends

- 3.4.1. Gellan Gum is the Largest Market Segment

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Food Hydrocolloids Market Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Gellan Gum

- 5.1.2. Carrageenan

- 5.1.3. Pectin

- 5.1.4. Xanthan Gum

- 5.1.5. Guar Gum

- 5.1.6. Gelatin

- 5.1.7. Others

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Dairy and Frozen Products

- 5.2.2. Bakery

- 5.2.3. Beverages

- 5.2.4. Confectionery

- 5.2.5. Meat and Seafood Products

- 5.2.6. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. North America

- 5.3.1.1. United States

- 5.3.1.2. Canada

- 5.3.1.3. Mexico

- 5.3.1.4. Rest of North America

- 5.3.1. North America

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 Cargill Incorporated

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Ashland Global Holdings Inc

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Archer Daniels Midland Company

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 J F Hydrocolloids Inc *List Not Exhaustive

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Koninklijke DSM N V

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 DuPont

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Behn Meyer Holding AG

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 CP Kelco U S Inc

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.1 Cargill Incorporated

List of Figures

- Figure 1: North America Food Hydrocolloids Market Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: North America Food Hydrocolloids Market Share (%) by Company 2025

List of Tables

- Table 1: North America Food Hydrocolloids Market Revenue million Forecast, by Type 2020 & 2033

- Table 2: North America Food Hydrocolloids Market Revenue million Forecast, by Application 2020 & 2033

- Table 3: North America Food Hydrocolloids Market Revenue million Forecast, by Geography 2020 & 2033

- Table 4: North America Food Hydrocolloids Market Revenue million Forecast, by Region 2020 & 2033

- Table 5: North America Food Hydrocolloids Market Revenue million Forecast, by Type 2020 & 2033

- Table 6: North America Food Hydrocolloids Market Revenue million Forecast, by Application 2020 & 2033

- Table 7: North America Food Hydrocolloids Market Revenue million Forecast, by Geography 2020 & 2033

- Table 8: North America Food Hydrocolloids Market Revenue million Forecast, by Country 2020 & 2033

- Table 9: United States North America Food Hydrocolloids Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Canada North America Food Hydrocolloids Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 11: Mexico North America Food Hydrocolloids Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 12: Rest of North America North America Food Hydrocolloids Market Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Food Hydrocolloids Market?

The projected CAGR is approximately 6.6%.

2. Which companies are prominent players in the North America Food Hydrocolloids Market?

Key companies in the market include Cargill Incorporated, Ashland Global Holdings Inc, Archer Daniels Midland Company, J F Hydrocolloids Inc *List Not Exhaustive, Koninklijke DSM N V, DuPont, Behn Meyer Holding AG, CP Kelco U S Inc.

3. What are the main segments of the North America Food Hydrocolloids Market?

The market segments include Type, Application, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 5032 million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Low-Fat and Low-Calorie Food; Increasing Product Innovation.

6. What are the notable trends driving market growth?

Gellan Gum is the Largest Market Segment.

7. Are there any restraints impacting market growth?

; Threat of New Entrants; Bargaining Power of Buyers/Consumers; Bargaining Power of Suppliers; Threat of Substitute Products; Degree Of Competition.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Food Hydrocolloids Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Food Hydrocolloids Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Food Hydrocolloids Market?

To stay informed about further developments, trends, and reports in the North America Food Hydrocolloids Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence