Key Insights

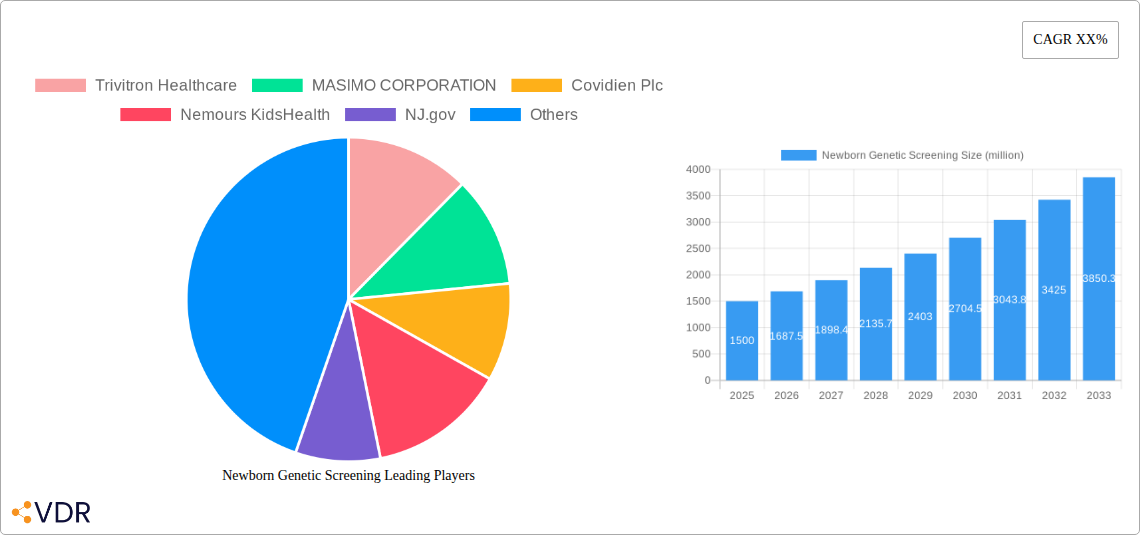

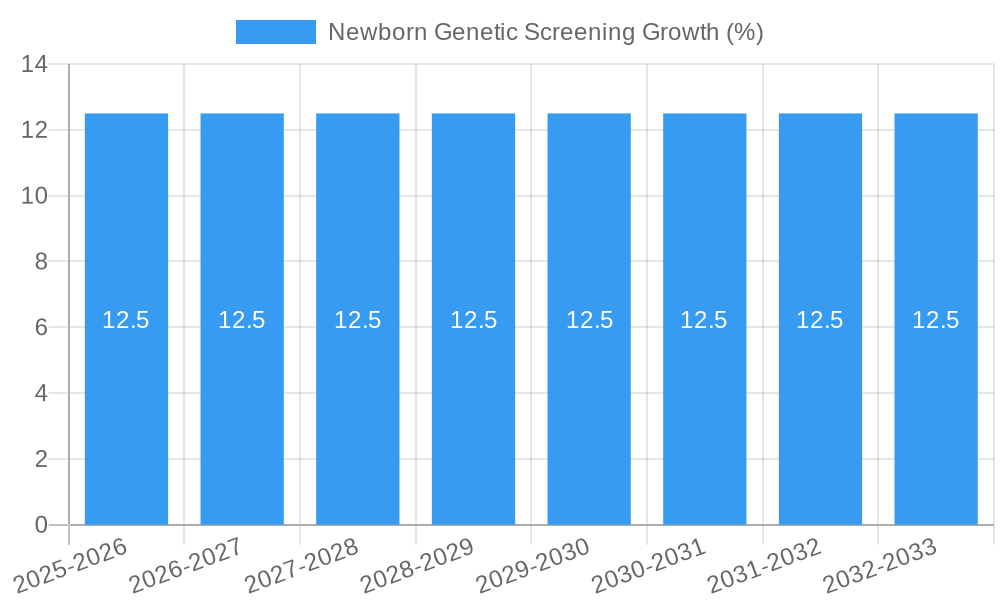

The global Newborn Genetic Screening market is poised for significant expansion, projected to reach a substantial market size of USD 1,500 million by 2025. This growth is propelled by an estimated Compound Annual Growth Rate (CAGR) of 12.5% during the forecast period of 2025-2033. A key driver behind this robust expansion is the increasing awareness among parents and healthcare providers regarding the critical importance of early detection and intervention for genetic disorders. Advances in genetic sequencing technologies, coupled with the development of more accurate and less invasive screening methods like dry blood spot tests, are further fueling market adoption. The growing prevalence of various genetic conditions in newborns globally also necessitates enhanced screening programs, thereby creating sustained demand. Furthermore, supportive government initiatives and rising healthcare expenditure in developing economies are contributing to the expanding reach and accessibility of these vital screening services.

The market's dynamic landscape is shaped by evolving trends and the strategic focus of key industry players. The growing emphasis on personalized medicine and preventative healthcare is a significant trend, driving the demand for comprehensive genetic screening panels that can identify a wider spectrum of disorders. Innovations in point-of-care testing (POCT) are also gaining traction, promising faster results and improved accessibility, particularly in remote or underserved areas. However, certain restraints, such as the high cost of advanced genetic testing equipment and the need for specialized personnel for accurate interpretation of results, may pose challenges to market penetration in some regions. Nevertheless, the overwhelming benefits of early diagnosis in preventing long-term complications and improving patient outcomes are expected to outweigh these limitations, ensuring a positive trajectory for the Newborn Genetic Screening market. Leading companies like Trivitron Healthcare, MASIMO CORPORATION, and PERKINELMER are actively investing in research and development to offer more sophisticated and cost-effective solutions, further stimulating market growth and innovation.

Newborn Genetic Screening Market Dynamics & Structure

The global Newborn Genetic Screening market is characterized by a dynamic and evolving landscape, driven by significant technological advancements and an increasing awareness of early disease detection. Market concentration is moderately fragmented, with key players like Trivitron Healthcare, MASIMO CORPORATION, Covidien Plc, Agilent Technologies, Ge Healthcare, PERKINELMER, Natus Medical Incorporated, Waters, Bio-Rad Laboratories, and Ab Sciex LLC actively engaged in research and development, and strategic acquisitions. Technological innovation is a primary driver, with the continuous refinement of genetic sequencing technologies, such as next-generation sequencing (NGS) and advanced diagnostic assays, enabling broader and more accurate screening panels. Regulatory frameworks, established by bodies like NJ.gov, are crucial in defining screening protocols, ensuring data privacy, and mandating the inclusion of specific conditions, thereby shaping market accessibility and growth. Competitive product substitutes are minimal in the core screening arena, as the focus is on definitive diagnostic tools rather than alternatives. End-user demographics, encompassing parents seeking optimal health for their children and healthcare providers focused on preventative care, exert a growing influence. Mergers and acquisition (M&A) trends indicate a strategic consolidation, with companies aiming to expand their product portfolios, geographic reach, and technological capabilities.

- Market Concentration: Moderately fragmented, with significant presence of established players and emerging innovators.

- Technological Innovation: Driven by advancements in NGS, microarrays, and automated laboratory systems.

- Regulatory Frameworks: Essential for standardizing protocols, ensuring accuracy, and driving adoption.

- Competitive Landscape: Characterized by a focus on innovation and integrated solutions rather than direct substitutes for core screening.

- End-User Demographics: Parents prioritizing early intervention and healthcare systems emphasizing public health initiatives.

- M&A Trends: Strategic acquisitions aimed at portfolio enhancement, technology integration, and market consolidation.

Newborn Genetic Screening Growth Trends & Insights

The global Newborn Genetic Screening market is projected to witness robust expansion, fueled by a confluence of escalating healthcare investments, increasing parental awareness regarding genetic disorders, and governmental initiatives promoting universal screening. The market size is anticipated to surge from an estimated $X,XXX million in the base year of 2025 to $X,XXX million by the end of the forecast period in 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately X.X% over the study period of 2019–2033. Adoption rates for newborn genetic screening are steadily climbing, driven by the availability of more comprehensive and cost-effective testing methods. Technological disruptions, particularly the widespread integration of next-generation sequencing (NGS) platforms, have revolutionized the scope of detectable genetic conditions, moving beyond traditional panels to include a wider array of rare diseases and metabolic disorders. This advancement not only enhances diagnostic accuracy but also opens new avenues for early intervention and management, significantly improving patient outcomes. Consumer behavior shifts are also playing a pivotal role; parents are increasingly proactive in seeking genetic information for their offspring, driven by a desire for informed reproductive choices and a commitment to long-term child health. The availability of direct-to-consumer genetic testing, while not a substitute for clinical newborn screening, has contributed to a broader societal understanding and acceptance of genetic diagnostics. Furthermore, the increasing prevalence of chronic and genetic diseases globally necessitates early detection, making newborn genetic screening a critical component of pediatric healthcare. The healthcare infrastructure in developing regions is also witnessing improvements, enabling wider access to these life-saving technologies. The expanding reimbursement policies by insurance providers and government health programs are further accelerating market penetration. The development of advanced bioinformatics tools for data analysis and interpretation is also crucial, making the vast amount of genetic data generated more actionable for clinicians and researchers. The collaborative efforts between research institutions and commercial entities are continuously pushing the boundaries of what can be screened, leading to the discovery of new genetic markers for diseases and the refinement of existing screening protocols.

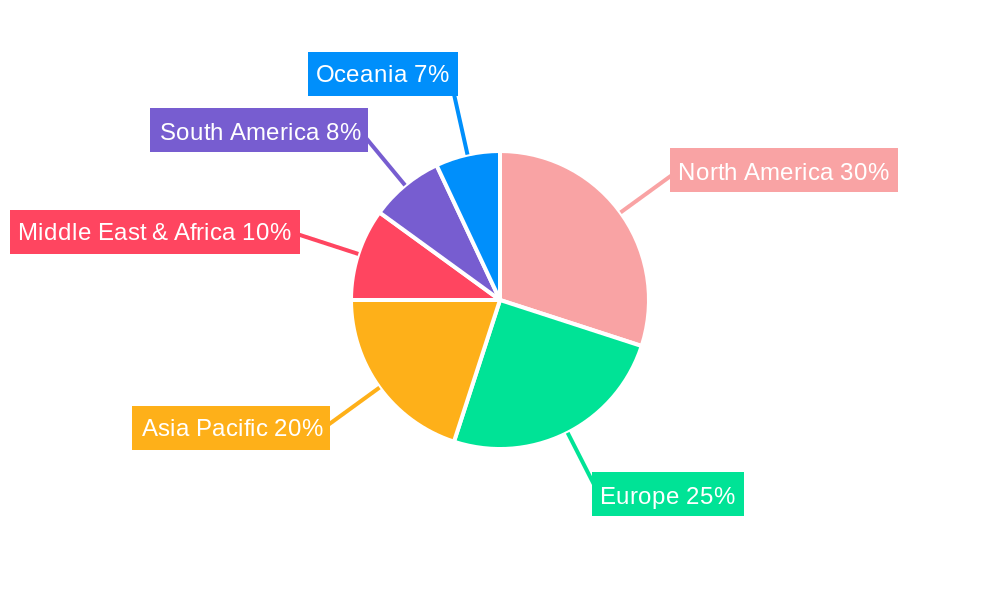

Dominant Regions, Countries, or Segments in Newborn Genetic Screening

The Clinical Laboratories segment, within the Application category, is emerging as the dominant force driving growth in the global Newborn Genetic Screening market. This dominance is attributed to several key factors that underscore the critical role these facilities play in the entire screening continuum, from sample processing to data analysis and reporting. Clinical laboratories, including those operated by Nemours KidsHealth and specialized diagnostic centers, are at the forefront of adopting and implementing advanced genetic testing technologies. Their infrastructure is designed to handle high volumes of samples efficiently and accurately, ensuring timely results for newborns. The increasing adoption of Dry Blood Spot Tests, a key type within the market, further solidifies the importance of clinical laboratories, as these samples are typically collected and then transported to these specialized labs for analysis using sophisticated instrumentation from companies like Agilent Technologies and PERKINELMER.

The market share held by clinical laboratories is substantial and projected to continue its upward trajectory. These laboratories are equipped with state-of-the-art sequencing equipment and bioinformatics capabilities, enabling them to perform a comprehensive range of genetic tests, including the screening for Critical Congenital Heart Defects (CCHD) and a growing number of inherited metabolic disorders. The regulatory compliance and accreditation requirements for clinical laboratories, often overseen by bodies similar to NJ.gov, ensure the highest standards of quality and reliability, making them the trusted partners for healthcare providers.

Furthermore, the growth potential of this segment is amplified by the expanding scope of newborn screening panels. As more genetic conditions become identifiable and clinically actionable, the demand for sophisticated laboratory services increases. The ability of clinical laboratories to integrate new screening targets into their existing workflows, often facilitated by partnerships with technology providers like MASIMO CORPORATION and Ge Healthcare, is a significant growth accelerator. The economic policies in many developed and developing nations are increasingly prioritizing public health initiatives, which include robust newborn screening programs. This leads to increased funding for laboratory infrastructure and personnel, further bolstering the dominance of clinical laboratories. The concentration of expertise within these labs, coupled with their ability to manage complex data interpretation, makes them indispensable in the newborn genetic screening ecosystem. Their role extends beyond simple testing to providing crucial diagnostic support and facilitating follow-up care for affected infants.

Newborn Genetic Screening Product Landscape

The Newborn Genetic Screening product landscape is defined by innovation and increasing comprehensiveness. Dry blood spot tests remain the gold standard for sample collection due to their ease of use and stability, facilitating widespread accessibility. Technological advancements have led to the development of highly sensitive and specific assays for a growing number of genetic disorders, including various metabolic conditions and CCHD. Companies are focusing on developing integrated platforms that combine sample preparation, amplification, detection, and data analysis, streamlining workflows for clinical laboratories. These innovations offer improved turnaround times and enhanced diagnostic accuracy, directly benefiting newborns by enabling earlier intervention and better health outcomes.

Key Drivers, Barriers & Challenges in Newborn Genetic Screening

Key Drivers: The primary forces propelling the Newborn Genetic Screening market include advancements in genomic technologies, leading to more comprehensive and accurate testing. Increasing government mandates and public health initiatives promoting universal screening are significant accelerators. Growing parental awareness and demand for early disease detection, coupled with expanding insurance coverage and reimbursement policies for genetic tests, are also critical drivers.

Key Barriers & Challenges: Despite the positive outlook, the market faces several challenges. High initial investment costs for advanced genetic sequencing equipment and infrastructure can be a barrier, particularly for smaller healthcare facilities. Stringent regulatory approval processes for new screening tests and technologies can lead to delays in market entry. Ethical considerations surrounding incidental findings and data privacy, as well as the need for skilled personnel for data interpretation and genetic counseling, pose significant hurdles. Supply chain disruptions for essential reagents and consumables can also impact operational efficiency.

Emerging Opportunities in Newborn Genetic Screening

Emerging opportunities in the Newborn Genetic Screening sector lie in the expansion of screening panels to include a wider array of rare genetic diseases and carrier screening for parents. The integration of artificial intelligence (AI) and machine learning for enhanced data analysis and predictive diagnostics presents a significant avenue for growth. Development of point-of-care diagnostic solutions, particularly in resource-limited settings, could dramatically increase screening accessibility. Furthermore, the growing emphasis on personalized medicine and pharmacogenomics offers potential for tailored treatment strategies based on newborn genetic profiles.

Growth Accelerators in the Newborn Genetic Screening Industry

Growth accelerators in the Newborn Genetic Screening industry are primarily driven by continuous technological breakthroughs in gene sequencing and molecular diagnostics, making tests more affordable and accessible. Strategic partnerships between diagnostic companies, research institutions, and healthcare providers are fostering innovation and expanding the reach of screening programs. The increasing global emphasis on preventative healthcare and the successful implementation of national newborn screening policies are significant market expansion strategies. Furthermore, the development of novel therapeutic interventions for previously untreatable genetic disorders is creating a stronger impetus for early diagnosis through newborn screening.

Key Players Shaping the Newborn Genetic Screening Market

- Trivitron Healthcare

- MASIMO CORPORATION

- Covidien Plc

- Nemours KidsHealth

- NJ.gov

- Agilent Technologies

- Ge Healthcare

- PERKINELMER

- Natus Medical Incorporated

- Waters

- Bio-Rad Laboratories

- Ab Sciex LLC

Notable Milestones in Newborn Genetic Screening Sector

- 2019: Expanded adoption of Whole Exome Sequencing (WES) for diagnosing rare pediatric conditions.

- 2020: Increased focus on CCHD screening programs, leading to wider implementation of pulse oximetry.

- 2021: Advancements in dried blood spot technology for improved DNA preservation and analysis.

- 2022: Growing integration of bioinformatics tools for efficient data interpretation in newborn screening.

- 2023: Emergence of expanded newborn screening panels covering a broader range of metabolic and genetic disorders.

- 2024: Increased investment in research for novel genetic markers and diagnostic technologies for early disease detection.

In-Depth Newborn Genetic Screening Market Outlook

The future of the Newborn Genetic Screening market is exceptionally promising, propelled by ongoing technological innovations and a global shift towards proactive healthcare. Growth accelerators such as the continuous refinement of next-generation sequencing, the development of more sophisticated bioinformatics platforms for data interpretation, and expanding government mandates for broader screening will continue to fuel market expansion. Strategic collaborations between key industry players and research institutions will unlock new diagnostic capabilities and therapeutic avenues. The increasing global burden of genetic diseases and the growing awareness among parents regarding the benefits of early intervention are creating a sustained demand for comprehensive screening solutions. The market is poised for significant growth, offering substantial opportunities for companies to enhance child health outcomes worldwide.

Newborn Genetic Screening Segmentation

-

1. Application

- 1.1. Clinical Laboratories

- 1.2. Hospitals

-

2. Types

- 2.1. Dry blood spot tests

- 2.2. Hearing screening tests

- 2.3. CCHD screening tests

Newborn Genetic Screening Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Newborn Genetic Screening REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Newborn Genetic Screening Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Clinical Laboratories

- 5.1.2. Hospitals

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Dry blood spot tests

- 5.2.2. Hearing screening tests

- 5.2.3. CCHD screening tests

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Newborn Genetic Screening Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Clinical Laboratories

- 6.1.2. Hospitals

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Dry blood spot tests

- 6.2.2. Hearing screening tests

- 6.2.3. CCHD screening tests

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Newborn Genetic Screening Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Clinical Laboratories

- 7.1.2. Hospitals

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Dry blood spot tests

- 7.2.2. Hearing screening tests

- 7.2.3. CCHD screening tests

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Newborn Genetic Screening Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Clinical Laboratories

- 8.1.2. Hospitals

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Dry blood spot tests

- 8.2.2. Hearing screening tests

- 8.2.3. CCHD screening tests

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Newborn Genetic Screening Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Clinical Laboratories

- 9.1.2. Hospitals

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Dry blood spot tests

- 9.2.2. Hearing screening tests

- 9.2.3. CCHD screening tests

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Newborn Genetic Screening Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Clinical Laboratories

- 10.1.2. Hospitals

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Dry blood spot tests

- 10.2.2. Hearing screening tests

- 10.2.3. CCHD screening tests

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Trivitron Healthcare

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 MASIMO CORPORATION

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Covidien Plc

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Nemours KidsHealth

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 NJ.gov

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Agilent Technologies

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Ge Healthcare

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 PERKINELMER

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Natus Medical Incorporated

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Waters

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Bio-Rad Laboratories

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Ab Sciex LLC

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 Trivitron Healthcare

List of Figures

- Figure 1: Global Newborn Genetic Screening Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Newborn Genetic Screening Revenue (million), by Application 2024 & 2032

- Figure 3: North America Newborn Genetic Screening Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Newborn Genetic Screening Revenue (million), by Types 2024 & 2032

- Figure 5: North America Newborn Genetic Screening Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Newborn Genetic Screening Revenue (million), by Country 2024 & 2032

- Figure 7: North America Newborn Genetic Screening Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Newborn Genetic Screening Revenue (million), by Application 2024 & 2032

- Figure 9: South America Newborn Genetic Screening Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Newborn Genetic Screening Revenue (million), by Types 2024 & 2032

- Figure 11: South America Newborn Genetic Screening Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Newborn Genetic Screening Revenue (million), by Country 2024 & 2032

- Figure 13: South America Newborn Genetic Screening Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Newborn Genetic Screening Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Newborn Genetic Screening Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Newborn Genetic Screening Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Newborn Genetic Screening Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Newborn Genetic Screening Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Newborn Genetic Screening Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Newborn Genetic Screening Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Newborn Genetic Screening Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Newborn Genetic Screening Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Newborn Genetic Screening Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Newborn Genetic Screening Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Newborn Genetic Screening Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Newborn Genetic Screening Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Newborn Genetic Screening Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Newborn Genetic Screening Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Newborn Genetic Screening Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Newborn Genetic Screening Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Newborn Genetic Screening Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Newborn Genetic Screening Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Newborn Genetic Screening Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Newborn Genetic Screening Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Newborn Genetic Screening Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Newborn Genetic Screening Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Newborn Genetic Screening Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Newborn Genetic Screening Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Newborn Genetic Screening Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Newborn Genetic Screening Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Newborn Genetic Screening Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Newborn Genetic Screening Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Newborn Genetic Screening Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Newborn Genetic Screening Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Newborn Genetic Screening Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Newborn Genetic Screening Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Newborn Genetic Screening Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Newborn Genetic Screening Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Newborn Genetic Screening Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Newborn Genetic Screening Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Newborn Genetic Screening Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Newborn Genetic Screening Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Newborn Genetic Screening Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Newborn Genetic Screening Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Newborn Genetic Screening Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Newborn Genetic Screening Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Newborn Genetic Screening Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Newborn Genetic Screening Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Newborn Genetic Screening Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Newborn Genetic Screening Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Newborn Genetic Screening Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Newborn Genetic Screening Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Newborn Genetic Screening Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Newborn Genetic Screening Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Newborn Genetic Screening Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Newborn Genetic Screening Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Newborn Genetic Screening Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Newborn Genetic Screening Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Newborn Genetic Screening Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Newborn Genetic Screening Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Newborn Genetic Screening Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Newborn Genetic Screening Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Newborn Genetic Screening Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Newborn Genetic Screening Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Newborn Genetic Screening Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Newborn Genetic Screening Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Newborn Genetic Screening Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Newborn Genetic Screening Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Newborn Genetic Screening?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Newborn Genetic Screening?

Key companies in the market include Trivitron Healthcare, MASIMO CORPORATION, Covidien Plc, Nemours KidsHealth, NJ.gov, Agilent Technologies, Ge Healthcare, PERKINELMER, Natus Medical Incorporated, Waters, Bio-Rad Laboratories, Ab Sciex LLC.

3. What are the main segments of the Newborn Genetic Screening?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Newborn Genetic Screening," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Newborn Genetic Screening report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Newborn Genetic Screening?

To stay informed about further developments, trends, and reports in the Newborn Genetic Screening, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence