Key Insights

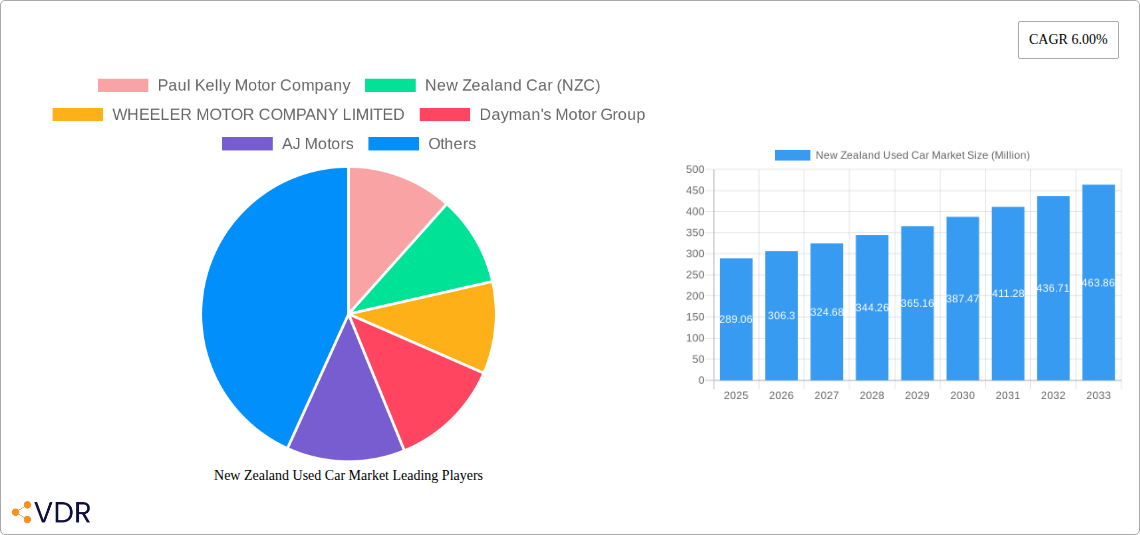

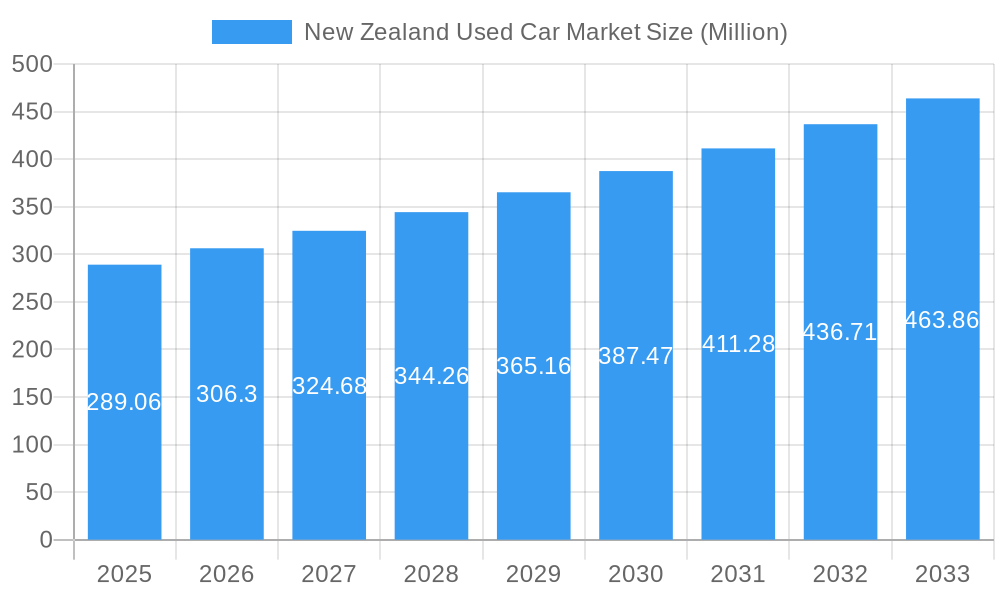

The New Zealand used car market is poised for significant growth, projected to reach a market size of approximately USD 289.06 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of 6.00% anticipated through 2033. This expansion is fueled by several key drivers, including the increasing affordability of pre-owned vehicles compared to new models, a sustained demand for personal mobility solutions, and a growing consumer awareness of the environmental benefits associated with purchasing used cars, thereby reducing the manufacturing footprint of new vehicles. Furthermore, ongoing advancements in vehicle inspection and reconditioning technologies are enhancing consumer confidence in the quality and reliability of used cars. The market's dynamism is also shaped by evolving consumer preferences, with a noticeable trend towards Sport Utility Vehicles (SUVs) and Multi-Purpose Vehicles (MUVs) owing to their versatility and suitability for diverse lifestyles and family needs. Electric Vehicles (EVs) are also emerging as a significant segment, driven by governmental incentives and a rising environmental consciousness.

New Zealand Used Car Market Market Size (In Million)

Despite this positive outlook, certain restraints could temper growth, such as potential fluctuations in currency exchange rates impacting import costs and the availability of new car inventory, which can indirectly influence the used car market. Regulatory changes concerning vehicle emissions and safety standards could also necessitate further investment in reconditioning for older models. The market is characterized by a competitive landscape with both organized dealerships offering certified pre-owned vehicles and unorganized players catering to budget-conscious buyers. Key players like Turners Automotive Group, Morrison Motor Group, and AutoTrader are actively shaping the market through innovative sales strategies, digital platforms, and a focus on customer experience. The prevalence of gasoline and diesel vehicles continues to dominate, but the accelerating adoption of electric and alternative fuel vehicles signals a significant future shift, presenting both opportunities and challenges for market participants in New Zealand.

New Zealand Used Car Market Company Market Share

New Zealand Used Car Market Report Description: Trends, Growth, and Key Players 2019-2033

This comprehensive report offers an in-depth analysis of the New Zealand Used Car Market, providing critical insights into its dynamics, growth trajectory, and competitive landscape. Covering a study period from 2019 to 2033, with a base and estimated year of 2025, this report is an indispensable resource for automotive manufacturers, dealerships, financial institutions, and market strategists seeking to capitalize on the burgeoning opportunities within this sector. We delve into market concentration, technological advancements, regulatory shifts, and evolving consumer preferences, delivering actionable intelligence for informed decision-making. This report examines the parent and child market segments with granular detail, ensuring a complete understanding of market drivers and future potential.

New Zealand Used Car Market Market Dynamics & Structure

The New Zealand Used Car Market is characterized by a dynamic interplay of factors influencing its structure and growth. Market concentration varies across different vendor types, with an increasing presence of organized players like Turners Automotive Group and AutoTrader alongside a significant unorganized sector. Technological innovation is a key driver, particularly with the growing interest in Electric Vehicles (EVs) and Alternative Fuel Vehicles, pushing demand for newer used models. Regulatory frameworks, such as the Clean Car Fee/Rebate scheme introduced in May 2023, are actively shaping the market by incentivizing lower-emission vehicles. Competitive product substitutes are abundant, ranging from budget-friendly hatchbacks to premium SUVs, catering to a diverse range of consumer needs and financial capabilities. End-user demographics are shifting, with a growing younger demographic seeking affordable and environmentally conscious transportation options. Mergers and acquisitions (M&A) activity, while not extensively detailed in public records, are anticipated to play a role in consolidating market share among larger entities.

- Market Concentration: Dual structure with organized players gaining traction and a persistent unorganized segment.

- Technological Innovation Drivers: Increasing demand for EVs and hybrid technologies influencing trade-in values and availability.

- Regulatory Frameworks: Government initiatives like the Clean Car Fee/Rebate scheme directly impact import and sales dynamics.

- Competitive Product Substitutes: A wide spectrum of vehicle types and price points ensures diverse consumer choice.

- End-User Demographics: Younger buyers and environmentally conscious consumers are influencing purchasing patterns.

- M&A Trends: Potential for consolidation as established players seek to expand their footprint.

New Zealand Used Car Market Growth Trends & Insights

The New Zealand Used Car Market is projected for robust growth, driven by a confluence of economic, technological, and societal factors. The market size is expected to witness a significant upward trend from the historical period of 2019-2024 through the forecast period of 2025-2033. Adoption rates for various vehicle types, particularly Sport Utility Vehicles (SUVs) and increasingly, Electric Vehicles (EVs), are accelerating. Technological disruptions, including advancements in battery technology and the integration of smart features in vehicles, are influencing consumer preferences and the resale value of used cars. Consumer behavior shifts are evident, with a growing emphasis on value for money, environmental sustainability, and online purchasing convenience. The market is expected to exhibit a Compound Annual Growth Rate (CAGR) of approximately xx% over the forecast period. Market penetration for used EVs is anticipated to rise, driven by government incentives and a broadening range of affordable models entering the used market.

The increasing demand for personal mobility, coupled with the sustained appeal of pre-owned vehicles as a cost-effective alternative to new car purchases, underpins the market’s expansion. Economic stability and consumer confidence are crucial factors influencing discretionary spending on vehicles. Furthermore, the availability of diverse financing options for used cars contributes to increased accessibility for a wider segment of the population. The competitive pricing strategies adopted by dealerships and private sellers alike ensure that the market remains attractive to budget-conscious buyers. The transition towards cleaner transportation is also a significant catalyst, with consumers increasingly seeking used vehicles that align with environmental concerns, thereby boosting the demand for hybrids and EVs.

Technological advancements are not only impacting the types of vehicles available but also the way they are bought and sold. Online marketplaces and digital sales platforms have revolutionized the car buying experience, offering greater transparency, convenience, and a wider selection. This shift towards digital channels is expected to continue, influencing traditional dealership models and opening up new avenues for market growth. The evolution of automotive technology, including enhanced safety features and improved fuel efficiency in older models, also contributes to the sustained demand for used cars. As new car prices continue to fluctuate, the value proposition of purchasing a well-maintained used vehicle becomes even more compelling for consumers.

Dominant Regions, Countries, or Segments in New Zealand Used Car Market

The New Zealand Used Car Market exhibits dominance across several key segments, with Sport Utility Vehicles (SUVs) emerging as a leading vehicle type driving significant growth. The inherent versatility, larger cabin space, and higher driving position of SUVs appeal to a broad demographic, from families to individuals seeking a more capable vehicle for diverse terrains and lifestyles. This segment's dominance is further amplified by evolving consumer preferences for comfort and practicality.

- Vehicle Type Dominance: Sport Utility Vehicles (SUVs) consistently lead the market due to their perceived practicality, spaciousness, and suitability for various terrains.

- Vendor Type Dynamics: Organized vendor types, including prominent dealerships and online platforms, are increasingly capturing market share by offering greater transparency, warranties, and financing options.

- Fuel Type Trends: Gasoline-powered vehicles remain dominant due to widespread availability and established infrastructure, however, Diesel and Electric, Alternative Fuel Vehicles are experiencing rapid growth fueled by environmental consciousness and government incentives.

The organized vendor segment, exemplified by players like Turners Automotive Group and AutoTrader, is increasingly influencing market growth. These entities provide a structured purchasing experience, often including pre-sale inspections, warranties, and streamlined financing, thereby building consumer trust and confidence. This organized approach is particularly attractive to buyers seeking peace of mind and a predictable transaction.

Geographically, while specific regional data is not presented, major urban centers like Auckland, Wellington, and Christchurch are expected to represent the largest markets due to higher population densities and greater economic activity. These regions typically have a higher concentration of dealerships and a more diverse range of available used vehicles.

The shift in fuel types is a crucial growth driver. While gasoline vehicles continue to form the bulk of the market, the increasing adoption of Electric Vehicles (EVs) and Alternative Fuel Vehicles, spurred by the government's Clean Car initiatives and growing environmental awareness, is creating a significant sub-market. This growing demand for cleaner vehicles is influencing trade-in values and the availability of newer used models with lower emissions. The market share for EVs in the used car segment is projected to expand considerably in the coming years.

New Zealand Used Car Market Product Landscape

The product landscape of the New Zealand Used Car Market is diverse, reflecting a wide array of vehicle types and ages. Dominant categories include practical hatchbacks, comfortable sedans, versatile SUVs, and family-oriented Multi-Purpose Vehicles (MUVs). Recent product innovations in the new car market, such as advanced safety features, improved fuel efficiency, and the integration of digital connectivity, are gradually trickling down into the used car inventory. This means that even pre-owned vehicles are offering increasingly sophisticated technologies and performance metrics, making them attractive to discerning buyers. The unique selling propositions of used cars often lie in their affordability compared to new models, coupled with a well-established track record.

Key Drivers, Barriers & Challenges in New Zealand Used Car Market

Key Drivers: The New Zealand Used Car Market is propelled by several key drivers. The primary force is the inherent affordability and value proposition of pre-owned vehicles, offering a cost-effective alternative to new car purchases. Evolving consumer preferences towards SUVs and fuel-efficient vehicles are also significant, influencing demand for specific models. Government initiatives, such as the Clean Car Fee/Rebate scheme, play a crucial role in stimulating demand for lower-emission used cars. Economic stability and consumer confidence contribute to increased discretionary spending on vehicles. Furthermore, the growing availability of online platforms enhances accessibility and transparency in the purchasing process.

Barriers & Challenges: Despite strong growth drivers, the market faces several barriers and challenges. Supply chain disruptions, though easing, can still impact the availability of desirable used vehicles, particularly those with newer technology. Regulatory hurdles and evolving emissions standards can create complexities for imports and sales. Competitive pressures from dealerships, private sellers, and increasingly, online retailers, can lead to price wars and margin erosion. Consumer concerns regarding vehicle condition, maintenance history, and potential hidden defects remain a significant barrier, necessitating robust inspection and warranty services. The upfront cost of newer used EVs, despite potential running cost savings, can still be a barrier for some buyers.

Emerging Opportunities in New Zealand Used Car Market

Emerging opportunities in the New Zealand Used Car Market are centered around the growing demand for sustainable transportation solutions. The expansion of the used Electric Vehicle (EV) market presents a significant untapped potential, driven by government incentives and increasing consumer environmental consciousness. The development of specialized online platforms that offer enhanced vehicle inspection reports and transparent history documentation can build greater consumer trust and capture market share from traditional dealers. Furthermore, the increasing interest in vehicle subscription services and flexible ownership models could create new avenues for the used car market, particularly for younger demographics.

Growth Accelerators in the New Zealand Used Car Market Industry

Several catalysts are accelerating long-term growth in the New Zealand Used Car Market industry. Technological breakthroughs in battery longevity and charging infrastructure are making used EVs a more viable and attractive option. Strategic partnerships between established automotive groups, such as the August 2023 collaboration between Andrew Simms Group and BYD Co. Ltd., are enhancing brand value and introducing new models that will eventually feed into the used car market. Market expansion strategies by online platforms, focusing on user experience and trust-building mechanisms, are broadening the reach of used car sales. The continued evolution of the Clean Car Fee/Rebate scheme is likely to incentivize the import and sale of cleaner used vehicles, further driving market growth.

Key Players Shaping the New Zealand Used Car Market Market

- Paul Kelly Motor Company

- New Zealand Car (NZC)

- WHEELER MOTOR COMPANY LIMITED

- Dayman's Motor Group

- AJ Motors

- Andrew Simms Group

- Turners Automotive Group

- AutoTrader

- Autoport

- Morrison Motor Group

Notable Milestones in New Zealand Used Car Market Sector

- August 2023: Andrew Simms Group, a leading dealer group, collaborated with BYD Co. Ltd., enhancing their brand value across New Zealand and influencing future used car inventory.

- May 2023: The New Zealand Government implemented the Clean Car Fee/Rebate scheme, designed to reduce vehicle emissions from imported used cars and subsequently impacting market demand and pricing dynamics.

In-Depth New Zealand Used Car Market Market Outlook

The outlook for the New Zealand Used Car Market remains exceptionally strong, underpinned by sustained demand for affordable and practical transportation. Growth accelerators such as government incentives for cleaner vehicles and the increasing availability of used electric cars are poised to significantly expand market reach. Strategic opportunities lie in leveraging digital platforms to enhance consumer trust and accessibility, and in forging partnerships that bring newer, more technologically advanced vehicles into the used car ecosystem. As consumer preferences continue to evolve towards sustainability and value, the used car market is well-positioned to meet these demands, promising continued growth and innovation in the coming years.

New Zealand Used Car Market Segmentation

-

1. Vehicle Type

- 1.1. Hatchback

- 1.2. Sedan

- 1.3. Sport Utility Vehicles (SUVs)

- 1.4. Multi-Purpose Vehicles (MUVs)

-

2. Vendor Type

- 2.1. Organized

- 2.2. Unorganized

-

3. Fuel Type

- 3.1. Gasoline

- 3.2. Diesel

- 3.3. Electric

- 3.4. Alternative Fuel Vehicles

New Zealand Used Car Market Segmentation By Geography

- 1. New Zealand

New Zealand Used Car Market Regional Market Share

Geographic Coverage of New Zealand Used Car Market

New Zealand Used Car Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.00% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Hatchback

- 5.1.2. Sedan

- 5.1.3. Sport Utility Vehicles (SUVs)

- 5.1.4. Multi-Purpose Vehicles (MUVs)

- 5.2. Market Analysis, Insights and Forecast - by Vendor Type

- 5.2.1. Organized

- 5.2.2. Unorganized

- 5.3. Market Analysis, Insights and Forecast - by Fuel Type

- 5.3.1. Gasoline

- 5.3.2. Diesel

- 5.3.3. Electric

- 5.3.4. Alternative Fuel Vehicles

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. New Zealand

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. New Zealand Used Car Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.1.1. Hatchback

- 6.1.2. Sedan

- 6.1.3. Sport Utility Vehicles (SUVs)

- 6.1.4. Multi-Purpose Vehicles (MUVs)

- 6.2. Market Analysis, Insights and Forecast - by Vendor Type

- 6.2.1. Organized

- 6.2.2. Unorganized

- 6.3. Market Analysis, Insights and Forecast - by Fuel Type

- 6.3.1. Gasoline

- 6.3.2. Diesel

- 6.3.3. Electric

- 6.3.4. Alternative Fuel Vehicles

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Paul Kelly Motor Company

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 New Zealand Car (NZC)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 WHEELER MOTOR COMPANY LIMITED

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Dayman's Motor Group

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 AJ Motors

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Andrew Simms Grou

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Turners Automotive Group

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 AutoTrader

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Autoport

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Morrison Motor Group

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Paul Kelly Motor Company

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: New Zealand Used Car Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: New Zealand Used Car Market Share (%) by Company 2025

List of Tables

- Table 1: New Zealand Used Car Market Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 2: New Zealand Used Car Market Revenue Million Forecast, by Vendor Type 2020 & 2033

- Table 3: New Zealand Used Car Market Revenue Million Forecast, by Fuel Type 2020 & 2033

- Table 4: New Zealand Used Car Market Revenue Million Forecast, by Region 2020 & 2033

- Table 5: New Zealand Used Car Market Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 6: New Zealand Used Car Market Revenue Million Forecast, by Vendor Type 2020 & 2033

- Table 7: New Zealand Used Car Market Revenue Million Forecast, by Fuel Type 2020 & 2033

- Table 8: New Zealand Used Car Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the New Zealand Used Car Market?

The projected CAGR is approximately 6.00%.

2. Which companies are prominent players in the New Zealand Used Car Market?

Key companies in the market include Paul Kelly Motor Company, New Zealand Car (NZC), WHEELER MOTOR COMPANY LIMITED, Dayman's Motor Group, AJ Motors, Andrew Simms Grou, Turners Automotive Group, AutoTrader, Autoport, Morrison Motor Group.

3. What are the main segments of the New Zealand Used Car Market?

The market segments include Vehicle Type, Vendor Type, Fuel Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 289.06 Million as of 2022.

5. What are some drivers contributing to market growth?

Online Sales Channel Witnessed Significant Market Growth.

6. What are the notable trends driving market growth?

Hatchback Cars witnessing major growth.

7. Are there any restraints impacting market growth?

Trust And Transparency In Used Car Remained A Key Challenge For Consumers.

8. Can you provide examples of recent developments in the market?

August 2023: Andrew Simms, one of the leading dealer groups in New Zealand, collaborated with BYD Co. Ltd. Through this collaboration, the Andrew Simms Group enhanced their brand value across the country.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "New Zealand Used Car Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the New Zealand Used Car Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the New Zealand Used Car Market?

To stay informed about further developments, trends, and reports in the New Zealand Used Car Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence