Key Insights

The global Model-Based Manufacturing Technologies market is poised for significant expansion, projected to reach an estimated market size of \$4,523 million by 2025. This robust growth is underpinned by an impressive Compound Annual Growth Rate (CAGR) of 18.3% throughout the forecast period of 2025-2033. This remarkable upward trajectory is fueled by several key drivers. Foremost among these is the increasing demand for enhanced product quality and reduced time-to-market across various industries. Model-based approaches streamline design, simulation, and manufacturing processes, minimizing errors and rework, which is crucial in today's competitive landscape. Furthermore, the widespread adoption of Industry 4.0 principles and the Internet of Things (IoT) are creating a fertile ground for model-based solutions, enabling seamless integration of digital and physical manufacturing environments. The inherent benefits of improved collaboration, better data traceability, and advanced simulation capabilities are compelling organizations to invest heavily in these technologies.

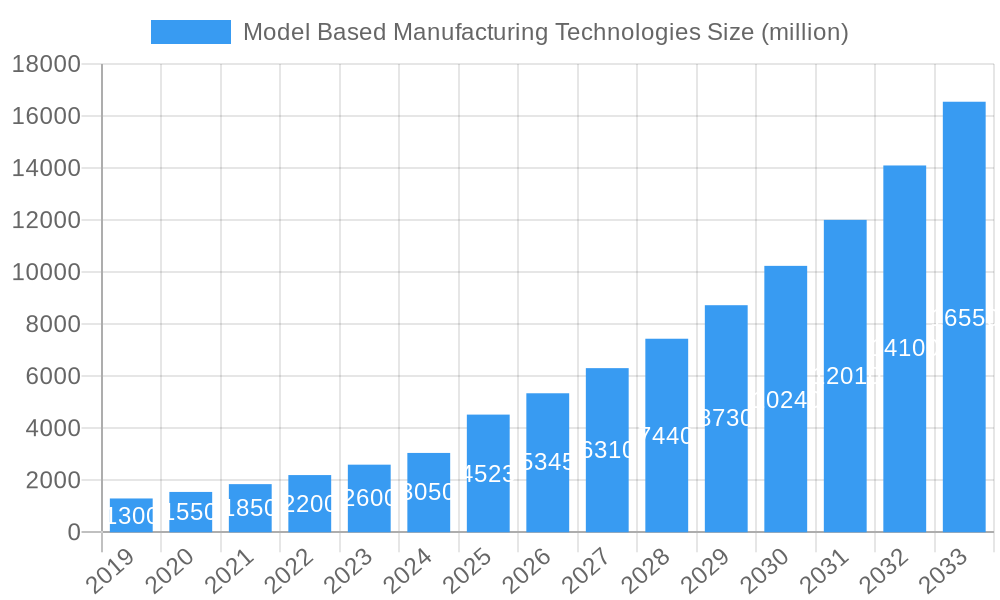

Model Based Manufacturing Technologies Market Size (In Billion)

The market segmentation reveals a diverse application landscape, with the Automotive, Electronics and Semiconductor, and Aerospace and Defence sectors leading in adoption due to their complex product development cycles and stringent quality requirements. These industries leverage model-based technologies for sophisticated design validation, virtual prototyping, and intricate process simulation. The rise of cloud-based solutions is also a significant trend, offering greater scalability, accessibility, and cost-effectiveness compared to traditional on-premises deployments. While the market is vibrant, certain restraints may influence its pace, such as the initial investment costs associated with implementing new systems and the need for skilled workforce development to effectively utilize these advanced tools. However, the overwhelming advantages in efficiency, innovation, and competitive edge are expected to outweigh these challenges, driving sustained growth across the globe.

Model Based Manufacturing Technologies Company Market Share

Report Description: Model-Based Manufacturing Technologies Market Analysis 2019-2033

Unlock the future of intelligent production with our comprehensive report on Model-Based Manufacturing Technologies. This in-depth analysis, spanning the historical period of 2019-2024 and extending through a robust forecast to 2033, provides critical insights into the evolving landscape of digital thread adoption, digital twin integration, and advanced simulation techniques in modern manufacturing. Designed for industry leaders, technology providers, and strategic planners, this report offers a definitive roadmap for navigating the complexities and capitalizing on the immense opportunities within this high-growth sector. Discover the key market dynamics, growth trajectories, regional dominance, product innovations, and the strategic imperatives shaping the global Model-Based Manufacturing Technologies market, with a particular focus on the parent market of Digital Manufacturing Solutions and the child market of Model-Based Systems Engineering.

Model Based Manufacturing Technologies Market Dynamics & Structure

The Model-Based Manufacturing Technologies market is characterized by a dynamic interplay of rapid technological advancement, increasing adoption across diverse industries, and a concentrated yet evolving competitive landscape. Leading players like Siemens, PTC, Dassault Systèmes, Autodesk, and SAP are at the forefront, driving innovation through integrated software suites and platform solutions. Market concentration is moderate, with these giants holding significant shares, but innovation barriers remain due to the complexity of implementation and the need for specialized expertise. Key technological innovation drivers include the rise of Artificial Intelligence (AI) and Machine Learning (ML) for predictive maintenance and process optimization, the widespread adoption of the Internet of Things (IoT) for real-time data acquisition, and advancements in augmented reality (AR) and virtual reality (VR) for enhanced design and training. Regulatory frameworks, particularly those focused on cybersecurity and data privacy, are becoming increasingly stringent, influencing technology development and deployment strategies. Competitive product substitutes, while present in the form of traditional CAD/CAM solutions, are rapidly being outpaced by the comprehensive, integrated approach offered by model-based technologies. End-user demographics are shifting towards a more tech-savvy workforce demanding efficient, data-driven production environments. Mergers and acquisitions (M&A) trends are active, as larger players seek to consolidate their offerings and acquire specialized capabilities, fueling market consolidation and strategic partnerships. For instance, the acquisition of Capvidia by Siemens underscores the drive for enhanced digital twin capabilities.

- Market Concentration: Moderate to High among key enterprise software providers.

- Technological Innovation Drivers: AI/ML for optimization, IoT for data, AR/VR for immersion.

- Regulatory Frameworks: Emphasis on cybersecurity, data integrity, and interoperability standards.

- Competitive Product Substitutes: Traditional CAD/CAM, but losing ground to integrated solutions.

- End-User Demographics: Demand for digital skills and data-driven decision-making.

- M&A Trends: Strategic acquisitions for platform expansion and niche technology integration.

Model Based Manufacturing Technologies Growth Trends & Insights

The Model-Based Manufacturing Technologies market is experiencing robust growth, projected to expand significantly from its estimated base year value of $15,500 million in 2025. This expansion is driven by a compelling convergence of factors, including the escalating need for enhanced operational efficiency, the imperative to reduce product development cycles, and the increasing demand for customized and complex products. The adoption rate of model-based approaches is accelerating across all major industry verticals, signifying a paradigm shift from traditional linear manufacturing processes to integrated, digital-first methodologies. Technological disruptions are constantly reshaping the market, with advancements in digital twins, simulation software, and cloud-based platforms becoming central to competitive advantage. Consumer behavior shifts are also playing a crucial role; end-users, particularly in the automotive and electronics sectors, expect higher quality, greater personalization, and faster delivery, all of which are facilitated by model-based manufacturing. The market penetration of these technologies is steadily increasing, as organizations recognize the tangible ROI in terms of reduced waste, improved quality control, and optimized resource allocation. The projected Compound Annual Growth Rate (CAGR) of 15.2% from 2025 to 2033 highlights the sustained and significant upward trajectory of this market. This growth is further amplified by the continuous development of more sophisticated simulation tools, enabling virtual prototyping and testing at an unprecedented scale. The increasing emphasis on sustainability and circular economy principles is also driving the adoption of model-based technologies, which enable better lifecycle management and material optimization. The integration of AI and ML algorithms into model-based platforms is further unlocking new possibilities for predictive analytics and autonomous decision-making on the shop floor, leading to further efficiency gains. The growing complexity of product designs, especially in sectors like aerospace and defense and medical devices, necessitates a model-based approach for managing intricate dependencies and ensuring compliance.

The market size is expected to grow from an estimated $15,500 million in 2025 to over $45,000 million by 2033, reflecting an impressive expansion driven by widespread adoption and technological advancements. This growth is underpinned by the increasing realization of the benefits of a unified digital thread, connecting design, simulation, manufacturing, and service throughout the product lifecycle. The adoption of cloud-based solutions is a key trend, offering scalability, flexibility, and accessibility for small and medium-sized enterprises (SMEs) as well as large corporations. This shift away from solely on-premises solutions is democratizing access to advanced manufacturing technologies. The continuous evolution of simulation capabilities, allowing for highly accurate predictions of product performance and manufacturing processes, is another significant growth catalyst. Companies are investing heavily in these tools to de-risk development and accelerate time-to-market. Furthermore, the increasing interconnectivity of manufacturing systems through IoT is feeding rich data into model-based platforms, enabling more sophisticated analysis and optimization. The demand for highly customized products, particularly in consumer electronics and medical devices, is pushing manufacturers to adopt agile and responsive production methods, where model-based approaches are indispensable. The escalating complexity of global supply chains also necessitates robust digital tools for end-to-end visibility and control, a domain where model-based manufacturing excels. The market is also seeing a rise in the adoption of digital twins, enabling real-time monitoring, performance analysis, and predictive maintenance of physical assets, thus enhancing operational efficiency and reducing downtime. The educational sector and research institutions are also playing a vital role by fostering a skilled workforce adept at utilizing these advanced technologies, ensuring a continuous supply of talent to drive future growth.

Dominant Regions, Countries, or Segments in Model Based Manufacturing Technologies

The Automotive segment is poised to be a dominant force in the Model-Based Manufacturing Technologies market, exhibiting substantial growth and influencing market trends through 2033. This dominance stems from the sector's inherent complexity, stringent regulatory requirements, and the relentless pursuit of innovation in areas like electric vehicles (EVs), autonomous driving, and advanced driver-assistance systems (ADAS). The need for sophisticated simulations to test vehicle performance, safety, and aerodynamic efficiency, coupled with the intricate nature of automotive supply chains, makes model-based approaches indispensable. Countries like Germany, the United States, China, and Japan, with their established automotive manufacturing bases and significant R&D investments, are leading this adoption. The Electronics and Semiconductor segment is another critical growth driver, fueled by the rapid pace of technological advancement and the miniaturization of components. The demand for precision engineering, complex integrated circuits, and the need for rapid prototyping in this sector directly benefits from model-based design and manufacturing. North America, particularly the US, and East Asian nations such as South Korea, Taiwan, and China, are at the forefront of this segment.

The Aerospace and Defence segment, while perhaps a more mature adopter, continues to be a significant contributor, driven by the need for extreme precision, rigorous safety standards, and the development of advanced aircraft and defense systems. The complexity of these projects necessitates extensive simulation, digital twin implementation for aircraft lifecycle management, and robust collaboration across global supply chains. Countries with strong aerospace industries, including the United States, France, the United Kingdom, and Russia, are key players.

The Medical device industry is also witnessing accelerated adoption due to the increasing demand for personalized implants, complex surgical instruments, and the critical need for regulatory compliance and patient safety. Model-based systems engineering and simulation are vital for designing and validating these intricate devices.

In terms of technology types, Cloud-Based solutions are rapidly gaining traction across all segments, offering scalability, cost-effectiveness, and enhanced collaboration capabilities, particularly for dispersed teams and SMEs. While On-premises solutions remain relevant for highly sensitive data or specific legacy systems, the trend is undeniably shifting towards the flexibility and accessibility of cloud environments.

- Dominant Application Segment: Automotive, driven by EV, ADAS, and autonomous technology development.

- Key Regional Hubs: North America (USA), Europe (Germany, France), and Asia-Pacific (China, Japan, South Korea).

- Growth Accelerators in Automotive: Electric powertrains, connectivity, autonomous systems, lightweight materials.

- Growth Accelerators in Electronics: Miniaturization, advanced packaging, AI-enabled devices, IoT integration.

- Growth Accelerators in Aerospace & Defence: Next-generation aircraft, hypersonic technology, cybersecurity solutions, space exploration.

- Growth Accelerators in Medical: Personalized medicine, advanced prosthetics, robotic surgery, diagnostic equipment.

- Technological Trend: Dominance of Cloud-Based solutions for flexibility and scalability.

Model Based Manufacturing Technologies Product Landscape

The product landscape of Model-Based Manufacturing Technologies is characterized by sophisticated, integrated software solutions designed to create and manage digital representations of physical products and processes. These offerings encompass powerful Computer-Aided Design (CAD), Computer-Aided Manufacturing (CAM), Computer-Aided Engineering (CAE) for simulation and analysis, and Product Lifecycle Management (PLM) systems. Key advancements include the seamless integration of these components, enabling a true digital thread from conceptualization to post-production. Companies like Siemens (Teamcenter, NX), PTC (Windchill, Creo), and Dassault Systèmes (3DEXPERIENCE Platform) are at the forefront, offering comprehensive platforms that facilitate collaborative design, virtual testing, and optimized manufacturing workflows. The performance metrics are increasingly focused on reducing design iterations, accelerating time-to-market, improving product quality, and enabling predictive maintenance through advanced simulation and digital twin technologies. Unique selling propositions often revolve around the platform's ability to handle complex multi-domain engineering challenges and its scalability to accommodate evolving business needs.

Key Drivers, Barriers & Challenges in Model Based Manufacturing Technologies

Key Drivers: The primary forces propelling the Model-Based Manufacturing Technologies market include the escalating demand for operational efficiency and cost reduction, the critical need to accelerate product development cycles in highly competitive industries, and the growing complexity of modern products requiring sophisticated design and simulation capabilities. Technological advancements in AI, IoT, and cloud computing are also significant drivers, enabling more intelligent and connected manufacturing ecosystems. Furthermore, government initiatives promoting digital transformation and Industry 4.0 are fostering wider adoption.

Barriers & Challenges: Despite strong growth, the market faces several barriers. The significant upfront investment required for implementing model-based solutions, coupled with the need for extensive employee training and change management, presents a considerable hurdle. Integration complexities with legacy systems and a lack of standardization across different platforms can also impede seamless adoption. Cybersecurity concerns and data privacy issues are paramount, especially with the increasing reliance on cloud-based solutions. Supply chain disruptions and the global shortage of skilled professionals capable of leveraging these advanced technologies also pose significant challenges to widespread implementation and growth.

Emerging Opportunities in Model Based Manufacturing Technologies

Emerging opportunities in the Model-Based Manufacturing Technologies sector lie in the expanding application of digital twins for real-time monitoring and predictive maintenance across a wider array of industries, including energy and utilities. The integration of advanced AI and machine learning algorithms within these platforms is creating opportunities for autonomous manufacturing processes and hyper-personalized product customization. Furthermore, the growing focus on sustainable manufacturing practices opens avenues for model-based technologies to optimize resource utilization, reduce waste, and facilitate circular economy principles. The development of accessible, cloud-based solutions tailored for SMEs represents a significant untapped market, democratizing access to advanced digital manufacturing capabilities.

Growth Accelerators in the Model Based Manufacturing Technologies Industry

Several catalysts are accelerating the long-term growth of the Model-Based Manufacturing Technologies industry. The continuous technological breakthroughs in areas like generative design, simulation fidelity, and augmented reality are expanding the capabilities and applicability of these solutions. Strategic partnerships between software providers, hardware manufacturers, and system integrators are fostering more comprehensive and cohesive offerings, simplifying adoption for end-users. Market expansion strategies, including targeting emerging economies and specific niche applications, are also driving growth. The increasing emphasis on digital transformation mandates from governments worldwide, coupled with significant R&D investments by leading companies, are creating a fertile ground for sustained expansion and innovation.

Key Players Shaping the Model Based Manufacturing Technologies Market

- Siemens

- PTC

- Dassault Systèmes

- Autodesk

- SAP

- Altair

- Ansys

- NXP

- Capvidia

- Anark

- MathWorks

- dSPACE

- ETAS

- Zuken

Notable Milestones in Model Based Manufacturing Technologies Sector

- 2019: Siemens launches Teamcenter X, a cloud-based PLM solution, accelerating SaaS adoption.

- 2020: PTC acquires Arena Solutions, strengthening its cloud-based PLM and supply chain management offerings.

- 2021: Dassault Systèmes expands its 3DEXPERIENCE platform with enhanced simulation and AI capabilities.

- 2022: Autodesk introduces new generative design tools for advanced manufacturing, boosting innovation.

- 2023: Ansys enhances its digital twin capabilities with advanced real-time simulation for complex systems.

- 2023: NXP Semiconductors announces collaborations to advance model-based development for automotive electronics.

- 2024: Altair expands its simulation portfolio with acquisitions focused on AI-driven design optimization.

- 2024: MathWorks introduces new toolboxes for embedded systems development and model-based control.

In-Depth Model Based Manufacturing Technologies Market Outlook

The future outlook for the Model-Based Manufacturing Technologies market is exceptionally promising, driven by sustained innovation and increasing adoption across a wide spectrum of industries. Growth accelerators such as the ubiquitous integration of AI for intelligent automation, the expansion of digital twin applications beyond product lifecycle management into operational intelligence, and the ongoing push towards hyper-personalized manufacturing will continue to fuel demand. The increasing focus on sustainable production and the circular economy will further necessitate the adoption of model-based approaches for optimizing resource efficiency and material usage. Strategic partnerships and the development of more accessible, cloud-native solutions are expected to broaden market reach, particularly to SMEs, unlocking significant untapped potential and solidifying the indispensable role of these technologies in the future of manufacturing.

Model Based Manufacturing Technologies Segmentation

-

1. Application

- 1.1. Automotive

- 1.2. Electronics and Semiconductor

- 1.3. Aerospace and Defence

- 1.4. Medical

- 1.5. Industrial

- 1.6. Others

-

2. Types

- 2.1. On-premises

- 2.2. Cloud Based

Model Based Manufacturing Technologies Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Model Based Manufacturing Technologies Regional Market Share

Geographic Coverage of Model Based Manufacturing Technologies

Model Based Manufacturing Technologies REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 21.17% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Model Based Manufacturing Technologies Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Automotive

- 5.1.2. Electronics and Semiconductor

- 5.1.3. Aerospace and Defence

- 5.1.4. Medical

- 5.1.5. Industrial

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. On-premises

- 5.2.2. Cloud Based

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Model Based Manufacturing Technologies Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Automotive

- 6.1.2. Electronics and Semiconductor

- 6.1.3. Aerospace and Defence

- 6.1.4. Medical

- 6.1.5. Industrial

- 6.1.6. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. On-premises

- 6.2.2. Cloud Based

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Model Based Manufacturing Technologies Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Automotive

- 7.1.2. Electronics and Semiconductor

- 7.1.3. Aerospace and Defence

- 7.1.4. Medical

- 7.1.5. Industrial

- 7.1.6. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. On-premises

- 7.2.2. Cloud Based

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Model Based Manufacturing Technologies Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Automotive

- 8.1.2. Electronics and Semiconductor

- 8.1.3. Aerospace and Defence

- 8.1.4. Medical

- 8.1.5. Industrial

- 8.1.6. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. On-premises

- 8.2.2. Cloud Based

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Model Based Manufacturing Technologies Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Automotive

- 9.1.2. Electronics and Semiconductor

- 9.1.3. Aerospace and Defence

- 9.1.4. Medical

- 9.1.5. Industrial

- 9.1.6. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. On-premises

- 9.2.2. Cloud Based

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Model Based Manufacturing Technologies Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Automotive

- 10.1.2. Electronics and Semiconductor

- 10.1.3. Aerospace and Defence

- 10.1.4. Medical

- 10.1.5. Industrial

- 10.1.6. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. On-premises

- 10.2.2. Cloud Based

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Siemens

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 PTC

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Dassault Systèmes

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Autodesk

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 SAP

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Altair

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Ansys

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 NXP

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Capvidia

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Anark

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 MathWorks

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 dSPACE

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 ETAS

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Zuken

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.1 Siemens

List of Figures

- Figure 1: Global Model Based Manufacturing Technologies Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Model Based Manufacturing Technologies Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Model Based Manufacturing Technologies Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Model Based Manufacturing Technologies Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Model Based Manufacturing Technologies Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Model Based Manufacturing Technologies Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Model Based Manufacturing Technologies Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Model Based Manufacturing Technologies Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Model Based Manufacturing Technologies Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Model Based Manufacturing Technologies Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Model Based Manufacturing Technologies Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Model Based Manufacturing Technologies Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Model Based Manufacturing Technologies Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Model Based Manufacturing Technologies Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Model Based Manufacturing Technologies Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Model Based Manufacturing Technologies Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Model Based Manufacturing Technologies Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Model Based Manufacturing Technologies Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Model Based Manufacturing Technologies Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Model Based Manufacturing Technologies Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Model Based Manufacturing Technologies Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Model Based Manufacturing Technologies Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Model Based Manufacturing Technologies Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Model Based Manufacturing Technologies Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Model Based Manufacturing Technologies Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Model Based Manufacturing Technologies Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Model Based Manufacturing Technologies Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Model Based Manufacturing Technologies Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Model Based Manufacturing Technologies Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Model Based Manufacturing Technologies Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Model Based Manufacturing Technologies Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Model Based Manufacturing Technologies Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Model Based Manufacturing Technologies Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Model Based Manufacturing Technologies Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Model Based Manufacturing Technologies Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Model Based Manufacturing Technologies Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Model Based Manufacturing Technologies Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Model Based Manufacturing Technologies Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Model Based Manufacturing Technologies Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Model Based Manufacturing Technologies Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Model Based Manufacturing Technologies Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Model Based Manufacturing Technologies Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Model Based Manufacturing Technologies Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Model Based Manufacturing Technologies Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Model Based Manufacturing Technologies Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Model Based Manufacturing Technologies Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Model Based Manufacturing Technologies Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Model Based Manufacturing Technologies Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Model Based Manufacturing Technologies Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Model Based Manufacturing Technologies Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Model Based Manufacturing Technologies Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Model Based Manufacturing Technologies Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Model Based Manufacturing Technologies Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Model Based Manufacturing Technologies Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Model Based Manufacturing Technologies Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Model Based Manufacturing Technologies Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Model Based Manufacturing Technologies Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Model Based Manufacturing Technologies Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Model Based Manufacturing Technologies Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Model Based Manufacturing Technologies Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Model Based Manufacturing Technologies Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Model Based Manufacturing Technologies Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Model Based Manufacturing Technologies Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Model Based Manufacturing Technologies Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Model Based Manufacturing Technologies Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Model Based Manufacturing Technologies Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Model Based Manufacturing Technologies Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Model Based Manufacturing Technologies Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Model Based Manufacturing Technologies Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Model Based Manufacturing Technologies Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Model Based Manufacturing Technologies Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Model Based Manufacturing Technologies Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Model Based Manufacturing Technologies Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Model Based Manufacturing Technologies Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Model Based Manufacturing Technologies Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Model Based Manufacturing Technologies Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Model Based Manufacturing Technologies Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Model Based Manufacturing Technologies?

The projected CAGR is approximately 21.17%.

2. Which companies are prominent players in the Model Based Manufacturing Technologies?

Key companies in the market include Siemens, PTC, Dassault Systèmes, Autodesk, SAP, Altair, Ansys, NXP, Capvidia, Anark, MathWorks, dSPACE, ETAS, Zuken.

3. What are the main segments of the Model Based Manufacturing Technologies?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Model Based Manufacturing Technologies," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Model Based Manufacturing Technologies report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Model Based Manufacturing Technologies?

To stay informed about further developments, trends, and reports in the Model Based Manufacturing Technologies, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence