Key Insights

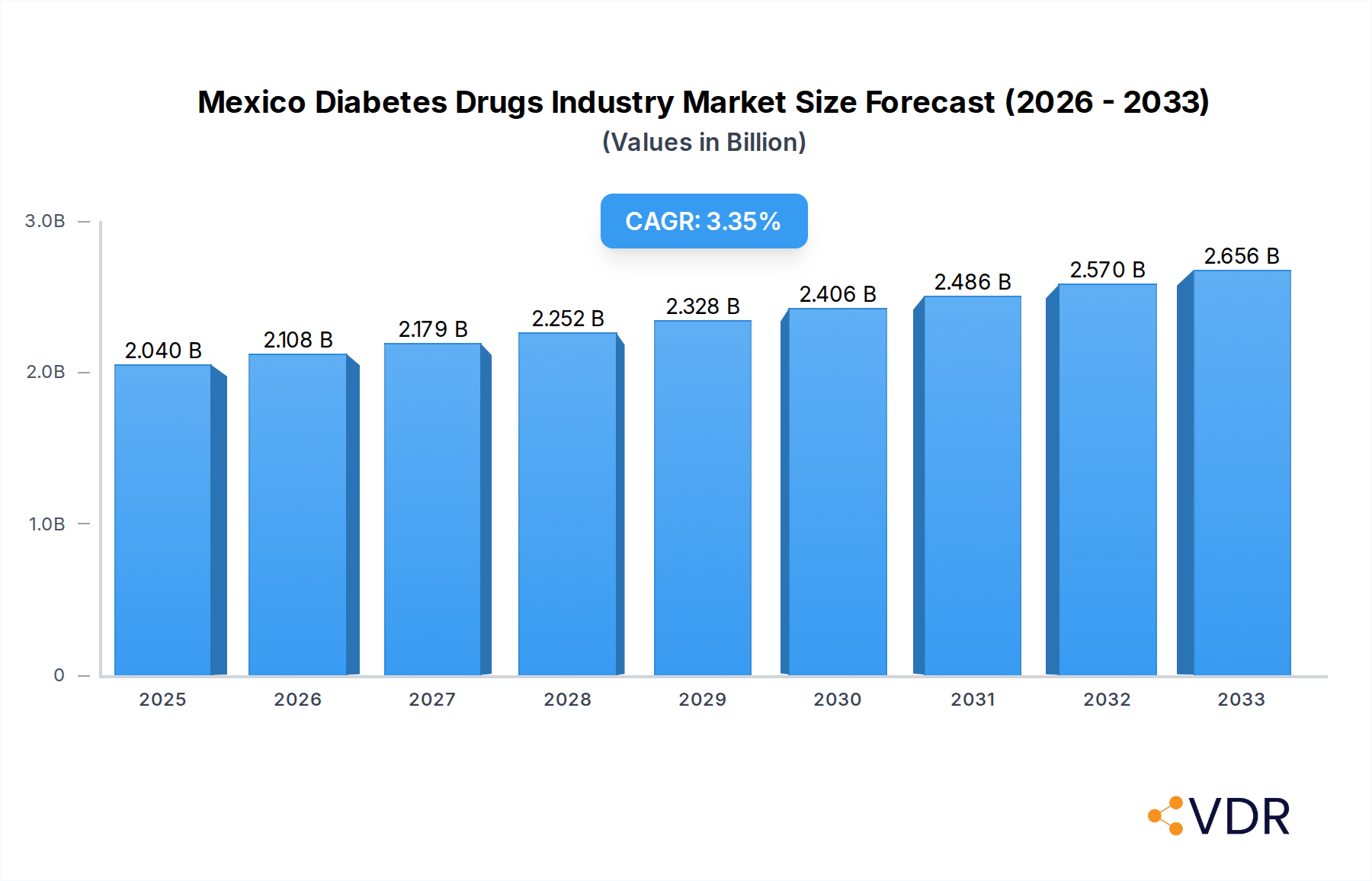

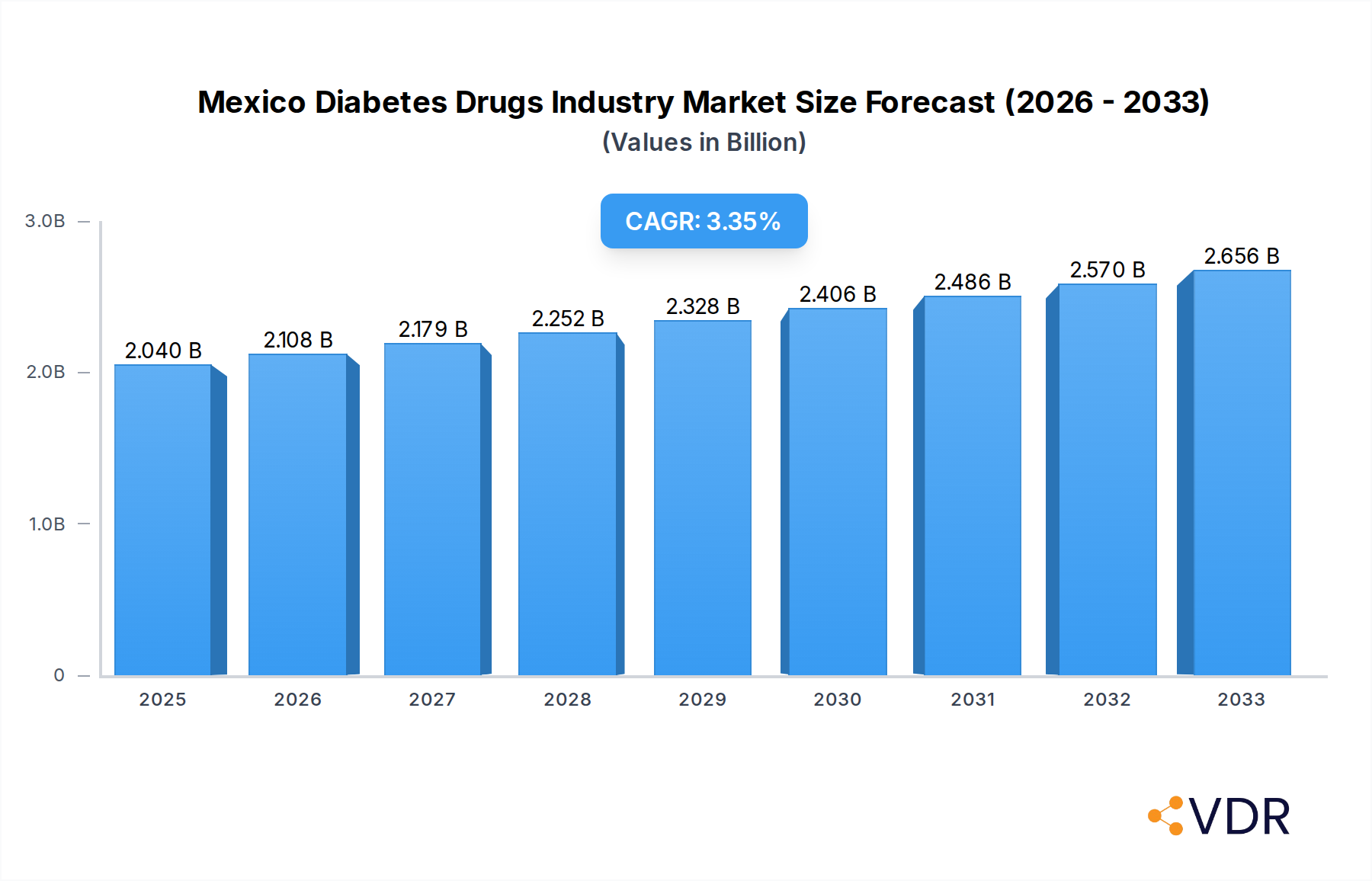

The Mexico Diabetes Drugs market is poised for substantial growth, with a market size of $2.04 billion in 2025 and a projected Compound Annual Growth Rate (CAGR) of 3.30% through 2033. This expansion is largely fueled by the increasing prevalence of diabetes in Mexico, a growing aging population susceptible to chronic diseases, and rising healthcare expenditure. The market is segmented across various therapeutic classes, including insulins (basal, bolus, traditional human, and biosimilar), oral anti-diabetic drugs (biguanides, alpha-glucosidase inhibitors, SGLT-2 inhibitors, DPP-4 inhibitors, sulfonylureas, meglitinides, and dopamine D2 receptor agonists), non-insulin injectable drugs (GLP-1 receptor agonists, amylin analogues), and combination drugs (insulin and oral combinations). The rising adoption of newer generation anti-diabetic medications, coupled with a greater emphasis on patient adherence and personalized treatment plans, will further propel market expansion. Furthermore, increased investment in research and development by key players to introduce innovative and effective diabetes management solutions will contribute to this positive trajectory.

Mexico Diabetes Drugs Industry Market Size (In Billion)

The market dynamics are influenced by several key drivers. Growing awareness among patients and healthcare providers regarding the long-term complications of uncontrolled diabetes encourages proactive management and the use of advanced therapeutic options. The increasing availability of biosimilar insulins and a wider array of oral and injectable anti-diabetic agents are enhancing treatment accessibility and affordability, particularly within the Mexican healthcare landscape. However, challenges such as stringent regulatory approvals for new drugs and the high cost associated with some novel therapies could present moderate restraints. Despite these, the overall outlook for the Mexico Diabetes Drugs market remains robust, driven by the persistent need for effective diabetes management and the continuous innovation within the pharmaceutical sector. The focus on integrated care models and digital health solutions for diabetes management is also emerging as a significant trend, promising to optimize patient outcomes and streamline healthcare delivery.

Mexico Diabetes Drugs Industry Company Market Share

Comprehensive Report: Mexico Diabetes Drugs Industry Market Outlook, Dynamics, and Growth Trajectories (2019-2033)

This in-depth report provides a definitive analysis of the Mexico diabetes drugs industry, offering critical insights into market dynamics, growth trends, key players, and future opportunities. Covering the historical period from 2019-2024 and a robust forecast period from 2025-2033, with 2025 as the base and estimated year, this study delves into parent and child market segments to offer a holistic view. Leveraging high-traffic keywords such as "Mexico diabetes treatment," "oral anti-diabetic drugs," "insulin market Mexico," and "diabetes drug market share," this report is optimized for maximum search engine visibility and industry professional engagement. We present all values in Million units for clear quantitative analysis.

Mexico Diabetes Drugs Industry Market Dynamics & Structure

The Mexico diabetes drugs industry exhibits a dynamic market structure influenced by a confluence of factors. Market concentration is moderately high, with established global pharmaceutical giants like Novo Nordisk A/S, Eli Lilly, and Sanofi Aventis holding significant sway due to extensive product portfolios and strong distribution networks. Technological innovation serves as a primary growth driver, with continuous advancements in drug formulations, delivery methods, and the development of novel therapeutic agents. The regulatory framework, overseen by COFEPRIS, plays a crucial role in drug approval, pricing, and market access, ensuring patient safety and drug efficacy. Competitive product substitutes, particularly the increasing availability of biosimilar insulins, present a growing challenge to branded drug manufacturers, driving price competition and emphasizing value-based offerings. End-user demographics are shaped by a rising prevalence of type 2 diabetes (T2D), an aging population, and an increasing awareness of diabetes management. Mergers and acquisitions (M&A) trends are less pronounced but focus on strategic alliances and collaborations to enhance R&D capabilities and market reach.

- Market Concentration: Moderate to high, dominated by multinational pharmaceutical companies.

- Technological Innovation: Driven by new drug development, improved delivery systems (e.g., oral insulin), and advanced diagnostics.

- Regulatory Framework: Governed by COFEPRIS, impacting market entry, pricing, and post-market surveillance.

- Competitive Product Substitutes: Biosimilar insulins are gaining traction, intensifying competition.

- End-User Demographics: Increasing T2D prevalence, aging population, and growing health consciousness.

- M&A Trends: Focused on strategic partnerships and niche acquisitions rather than large-scale consolidation.

Mexico Diabetes Drugs Industry Growth Trends & Insights

The Mexico diabetes drugs industry is poised for significant growth, driven by an escalating burden of diabetes and increasing access to advanced treatment options. The market size is projected to expand considerably over the forecast period. This growth is underpinned by rising adoption rates of newer drug classes, such as SGLT-2 inhibitors and DPP-4 inhibitors, which offer improved glycemic control and cardiovascular benefits. Technological disruptions are a constant feature, with the pursuit of oral insulin formulations like Oramed's ORMD-0801 representing a potential game-changer in insulin delivery. Consumer behavior shifts are also critical; patients are becoming more informed about their condition and actively seek out the most effective and convenient treatment regimens. The growing prevalence of diabetes, estimated to affect millions of Mexicans, coupled with increased healthcare spending and government initiatives aimed at disease management, further fuels market expansion. The CAGR for the forecast period is expected to be robust, reflecting the unmet medical needs and the introduction of innovative therapies. Market penetration for advanced diabetes medications is gradually increasing as awareness and affordability improve. The shift towards personalized medicine and combination therapies tailored to individual patient profiles also contributes to market evolution.

Dominant Regions, Countries, or Segments in Mexico Diabetes Drugs Industry

Within the multifaceted Mexico diabetes drugs industry, the Oral Anti-diabetic drugs segment is emerging as a dominant force, with specific sub-segments showing exceptional growth potential. This dominance is propelled by the sheer volume of patients diagnosed with type 2 diabetes (T2D), where oral medications often serve as the first line of treatment.

- Biguanides (Metformin): Remaining the cornerstone of T2D management due to its efficacy, safety profile, and affordability, Biguanides are expected to maintain a substantial market share. Its role as a foundational therapy makes it indispensable.

- DPP-4 inhibitors: These drugs have witnessed strong uptake due to their favorable efficacy and tolerability. Their ability to improve glycemic control without significant weight gain or hypoglycemia makes them a preferred choice for many patients and physicians.

- SGLT-2 inhibitors: This class is experiencing rapid growth, driven by their dual benefits of glycemic control and significant cardiovascular and renal protection. As awareness of these pleiotropic effects grows, their market penetration is set to increase dramatically.

- GLP-1 receptor agonists (Non-Insulin Injectable drugs): While injectables, the growing success and expanding indications of GLP-1 receptor agonists, particularly for weight management in T2D patients, are making them increasingly prominent. Novo Nordisk's expansion of its GLP-1 drug production facility highlights the immense demand and future potential in this sub-segment.

The growth in these oral and injectable segments is further amplified by Mexico's expanding healthcare infrastructure, increasing public health awareness campaigns focused on diabetes prevention and management, and the proactive strategies of pharmaceutical companies to make these advanced therapies more accessible. The economic policies encouraging healthcare investment and the demographic shift towards a larger adult population susceptible to T2D are key factors underpinning the dominance of these segments.

Mexico Diabetes Drugs Industry Product Landscape

The Mexico diabetes drugs industry is characterized by a dynamic product landscape driven by continuous innovation. Key product advancements include the development of novel oral anti-diabetic agents with improved efficacy and reduced side effects, such as next-generation DPP-4 inhibitors and SGLT-2 inhibitors. In the insulin market, advancements focus on long-acting basal insulins offering more predictable glucose control and faster-acting bolus insulins to better mimic physiological insulin secretion. The growing availability of biosimilar insulins provides cost-effective alternatives, expanding patient access. Furthermore, the exploration of innovative delivery mechanisms, such as oral insulin capsules (e.g., Oramed's ORMD-0801), promises to revolutionize insulin therapy by offering a more convenient and patient-friendly option. Combination drugs, integrating multiple active pharmaceutical ingredients into a single dosage form, are also gaining prominence, simplifying treatment regimens and improving patient adherence.

Key Drivers, Barriers & Challenges in Mexico Diabetes Drugs Industry

The Mexico diabetes drugs industry is propelled by several key drivers. The escalating prevalence of diabetes, particularly type 2 diabetes (T2D), fueled by lifestyle factors and an aging population, creates a persistent and growing demand for effective treatments. Technological advancements in drug development, leading to more efficacious and safer medications with reduced side effects, are critical. Government initiatives and public health campaigns aimed at diabetes awareness and management also contribute significantly. The increasing disposable income and greater healthcare expenditure further support market growth.

However, the industry faces significant barriers and challenges. High drug prices for novel therapies can limit patient access, especially for those without comprehensive insurance coverage. Stringent regulatory approval processes, while ensuring safety, can prolong the time to market for new drugs. The strong presence of established generic and biosimilar manufacturers intensifies price competition, impacting the profitability of branded products. Supply chain disruptions, particularly in the wake of global events, can affect the availability of essential medications. Furthermore, physician and patient education regarding the benefits of newer treatment modalities is an ongoing challenge.

Emerging Opportunities in Mexico Diabetes Drugs Industry

Emerging opportunities in the Mexico diabetes drugs industry are largely centered on addressing unmet medical needs and leveraging innovative technologies. The development and commercialization of novel oral anti-diabetic drugs with superior efficacy and safety profiles present a significant avenue. Expansion of biosimilar insulin markets through strategic partnerships and cost-effective manufacturing is another key opportunity. The increasing focus on preventing or delaying diabetes complications, such as cardiovascular and renal diseases, through targeted therapies like SGLT-2 inhibitors and GLP-1 receptor agonists, offers substantial growth potential. Furthermore, the burgeoning telemedicine sector and digital health solutions for diabetes management create opportunities for integrated drug delivery and patient monitoring systems. The growing demand for personalized medicine, tailored to individual patient genetic profiles and metabolic responses, will also drive innovation and market expansion.

Growth Accelerators in the Mexico Diabetes Drugs Industry Industry

Several catalysts are accelerating the long-term growth of the Mexico diabetes drugs industry. Foremost among these is the relentless pace of technological breakthroughs in pharmaceutical research and development, leading to the introduction of innovative drugs that offer improved patient outcomes and quality of life. Strategic partnerships between global pharmaceutical giants and local players are crucial for expanding market reach, facilitating drug distribution, and adapting to regional healthcare needs. Government policies that incentivize healthcare investment and promote public health awareness around diabetes management are also key accelerators. The increasing adoption of value-based healthcare models, which reward effective treatment outcomes, encourages the use of advanced and cost-effective therapies. Furthermore, the growing trend of market expansion into underserved regions and the development of patient support programs to enhance adherence are critical for sustained growth.

Key Players Shaping the Mexico Diabetes Drugs Industry Market

- Pfizer

- Takeda

- Janssen Pharmaceuticals

- Eli Lilly

- Novartis

- Merck and Co

- AstraZeneca

- Sanofi Aventis

- Bristol Myers Squibb

- Novo Nordisk A/S

- Boehringer Ingelheim

- Astellas

Notable Milestones in Mexico Diabetes Drugs Industry Sector

- November 2023: Novo Nordisk has recently expanded its site to produce GLP-1 drugs, aiming to sustain its robust growth in the treatment of type 2 diabetes (T2D) following the introduction of Eli Lilly's Zepbound earlier this month.

- March 2022: Oramed announced ORMD-0801 (a new molecule) is being evaluated in two pivotal Phase 3 trials and can be the first oral insulin capsule with the most convenient and safest way to deliver insulin therapy. This drug is expected to be a game-changer in the insulin and oral anti-diabetes drugs markets.

In-Depth Mexico Diabetes Drugs Industry Market Outlook

The outlook for the Mexico diabetes drugs industry remains highly optimistic, driven by a sustained increase in diabetes prevalence and the continuous introduction of innovative therapies. Growth accelerators, including groundbreaking advancements in drug discovery and formulation, alongside strategic collaborations between key industry players, are poised to further expand the market. Government support for public health initiatives and increasing healthcare expenditure will bolster patient access to a wider range of treatments, from advanced oral anti-diabetic drugs to novel insulin formulations and non-insulin injectables. The industry's focus on developing solutions for both glycemic control and the management of associated comorbidities, such as cardiovascular and renal diseases, will be a significant driver of future market potential. Strategic opportunities lie in further penetration of biosimilar markets, expansion of digital health solutions for diabetes management, and the development of personalized treatment approaches, all contributing to a robust and dynamic market evolution.

Mexico Diabetes Drugs Industry Segmentation

-

1. Insulins

- 1.1. Basal or Long Acting Insulins

- 1.2. Bolus or Fast Acting Insulins

- 1.3. Traditional Human Insulins

- 1.4. Biosimilar Insulins

-

2. Oral Anti-diabetic drugs

- 2.1. Biguanides

- 2.2. Alpha-Glucosidase Inhibitors

- 2.3. Dopamine D2 receptor agonist

- 2.4. SGLT-2 inhibitors

- 2.5. DPP-4 inhibitors

- 2.6. Sulfonylureas

- 2.7. Meglitinides

-

3. Non-Insulin Injectable drugs

- 3.1. GLP-1 receptor agonists

- 3.2. Amylin Analogue

-

4. Combination drugs

- 4.1. Insulin combinations

- 4.2. Oral Combinations

Mexico Diabetes Drugs Industry Segmentation By Geography

- 1. Mexico

Mexico Diabetes Drugs Industry Regional Market Share

Geographic Coverage of Mexico Diabetes Drugs Industry

Mexico Diabetes Drugs Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.30% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Insulins

- 5.1.1. Basal or Long Acting Insulins

- 5.1.2. Bolus or Fast Acting Insulins

- 5.1.3. Traditional Human Insulins

- 5.1.4. Biosimilar Insulins

- 5.2. Market Analysis, Insights and Forecast - by Oral Anti-diabetic drugs

- 5.2.1. Biguanides

- 5.2.2. Alpha-Glucosidase Inhibitors

- 5.2.3. Dopamine D2 receptor agonist

- 5.2.4. SGLT-2 inhibitors

- 5.2.5. DPP-4 inhibitors

- 5.2.6. Sulfonylureas

- 5.2.7. Meglitinides

- 5.3. Market Analysis, Insights and Forecast - by Non-Insulin Injectable drugs

- 5.3.1. GLP-1 receptor agonists

- 5.3.2. Amylin Analogue

- 5.4. Market Analysis, Insights and Forecast - by Combination drugs

- 5.4.1. Insulin combinations

- 5.4.2. Oral Combinations

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. Mexico

- 5.1. Market Analysis, Insights and Forecast - by Insulins

- 6. Mexico Diabetes Drugs Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Insulins

- 6.1.1. Basal or Long Acting Insulins

- 6.1.2. Bolus or Fast Acting Insulins

- 6.1.3. Traditional Human Insulins

- 6.1.4. Biosimilar Insulins

- 6.2. Market Analysis, Insights and Forecast - by Oral Anti-diabetic drugs

- 6.2.1. Biguanides

- 6.2.2. Alpha-Glucosidase Inhibitors

- 6.2.3. Dopamine D2 receptor agonist

- 6.2.4. SGLT-2 inhibitors

- 6.2.5. DPP-4 inhibitors

- 6.2.6. Sulfonylureas

- 6.2.7. Meglitinides

- 6.3. Market Analysis, Insights and Forecast - by Non-Insulin Injectable drugs

- 6.3.1. GLP-1 receptor agonists

- 6.3.2. Amylin Analogue

- 6.4. Market Analysis, Insights and Forecast - by Combination drugs

- 6.4.1. Insulin combinations

- 6.4.2. Oral Combinations

- 6.1. Market Analysis, Insights and Forecast - by Insulins

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Pfizer

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Takeda

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Other

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Janssen Pharmaceuticals

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Eli Lilly

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Novartis

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Merck and Co

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 AstraZeneca

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Sanofi Aventis

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Bristol Myers Squibb

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Novo Nordisk A/S

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Boehringer Ingelheim

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Sanofi Aventis

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Astellas

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.1 Pfizer

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Mexico Diabetes Drugs Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Mexico Diabetes Drugs Industry Share (%) by Company 2025

List of Tables

- Table 1: Mexico Diabetes Drugs Industry Revenue Million Forecast, by Insulins 2020 & 2033

- Table 2: Mexico Diabetes Drugs Industry Volume K Unit Forecast, by Insulins 2020 & 2033

- Table 3: Mexico Diabetes Drugs Industry Revenue Million Forecast, by Oral Anti-diabetic drugs 2020 & 2033

- Table 4: Mexico Diabetes Drugs Industry Volume K Unit Forecast, by Oral Anti-diabetic drugs 2020 & 2033

- Table 5: Mexico Diabetes Drugs Industry Revenue Million Forecast, by Non-Insulin Injectable drugs 2020 & 2033

- Table 6: Mexico Diabetes Drugs Industry Volume K Unit Forecast, by Non-Insulin Injectable drugs 2020 & 2033

- Table 7: Mexico Diabetes Drugs Industry Revenue Million Forecast, by Combination drugs 2020 & 2033

- Table 8: Mexico Diabetes Drugs Industry Volume K Unit Forecast, by Combination drugs 2020 & 2033

- Table 9: Mexico Diabetes Drugs Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 10: Mexico Diabetes Drugs Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 11: Mexico Diabetes Drugs Industry Revenue Million Forecast, by Insulins 2020 & 2033

- Table 12: Mexico Diabetes Drugs Industry Volume K Unit Forecast, by Insulins 2020 & 2033

- Table 13: Mexico Diabetes Drugs Industry Revenue Million Forecast, by Oral Anti-diabetic drugs 2020 & 2033

- Table 14: Mexico Diabetes Drugs Industry Volume K Unit Forecast, by Oral Anti-diabetic drugs 2020 & 2033

- Table 15: Mexico Diabetes Drugs Industry Revenue Million Forecast, by Non-Insulin Injectable drugs 2020 & 2033

- Table 16: Mexico Diabetes Drugs Industry Volume K Unit Forecast, by Non-Insulin Injectable drugs 2020 & 2033

- Table 17: Mexico Diabetes Drugs Industry Revenue Million Forecast, by Combination drugs 2020 & 2033

- Table 18: Mexico Diabetes Drugs Industry Volume K Unit Forecast, by Combination drugs 2020 & 2033

- Table 19: Mexico Diabetes Drugs Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 20: Mexico Diabetes Drugs Industry Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Mexico Diabetes Drugs Industry?

The projected CAGR is approximately 3.30%.

2. Which companies are prominent players in the Mexico Diabetes Drugs Industry?

Key companies in the market include Pfizer, Takeda, Other, Janssen Pharmaceuticals, Eli Lilly, Novartis, Merck and Co, AstraZeneca, Sanofi Aventis, Bristol Myers Squibb, Novo Nordisk A/S, Boehringer Ingelheim, Sanofi Aventis, Astellas.

3. What are the main segments of the Mexico Diabetes Drugs Industry?

The market segments include Insulins, Oral Anti-diabetic drugs, Non-Insulin Injectable drugs, Combination drugs.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.04 Million as of 2022.

5. What are some drivers contributing to market growth?

; The Rise in Global Prevalence of Cases of Obesity due to Modern Sedentary Lifestyles; Rise in Awareness and Disposable Income in Developed Economies.

6. What are the notable trends driving market growth?

The oral anti-diabetic drugs segment holds the highest market share in the Mexico Diabetes Drugs Market in the current year.

7. Are there any restraints impacting market growth?

; Highly Cost of Branded Products in Emerging Countries; Severe Adverse Associated with Medication Including Seizures. Suicidal Attempts and Even Death; Adoption of Traditional Yoga and Herbal Products.

8. Can you provide examples of recent developments in the market?

November 2023: Novo Nordisk has recently expanded its site to produce GLP-1 drugs, aiming to sustain its robust growth in the treatment of type 2 diabetes (T2D) following the introduction of Eli Lilly's Zepbound earlier this month.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Mexico Diabetes Drugs Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Mexico Diabetes Drugs Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Mexico Diabetes Drugs Industry?

To stay informed about further developments, trends, and reports in the Mexico Diabetes Drugs Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence