Key Insights

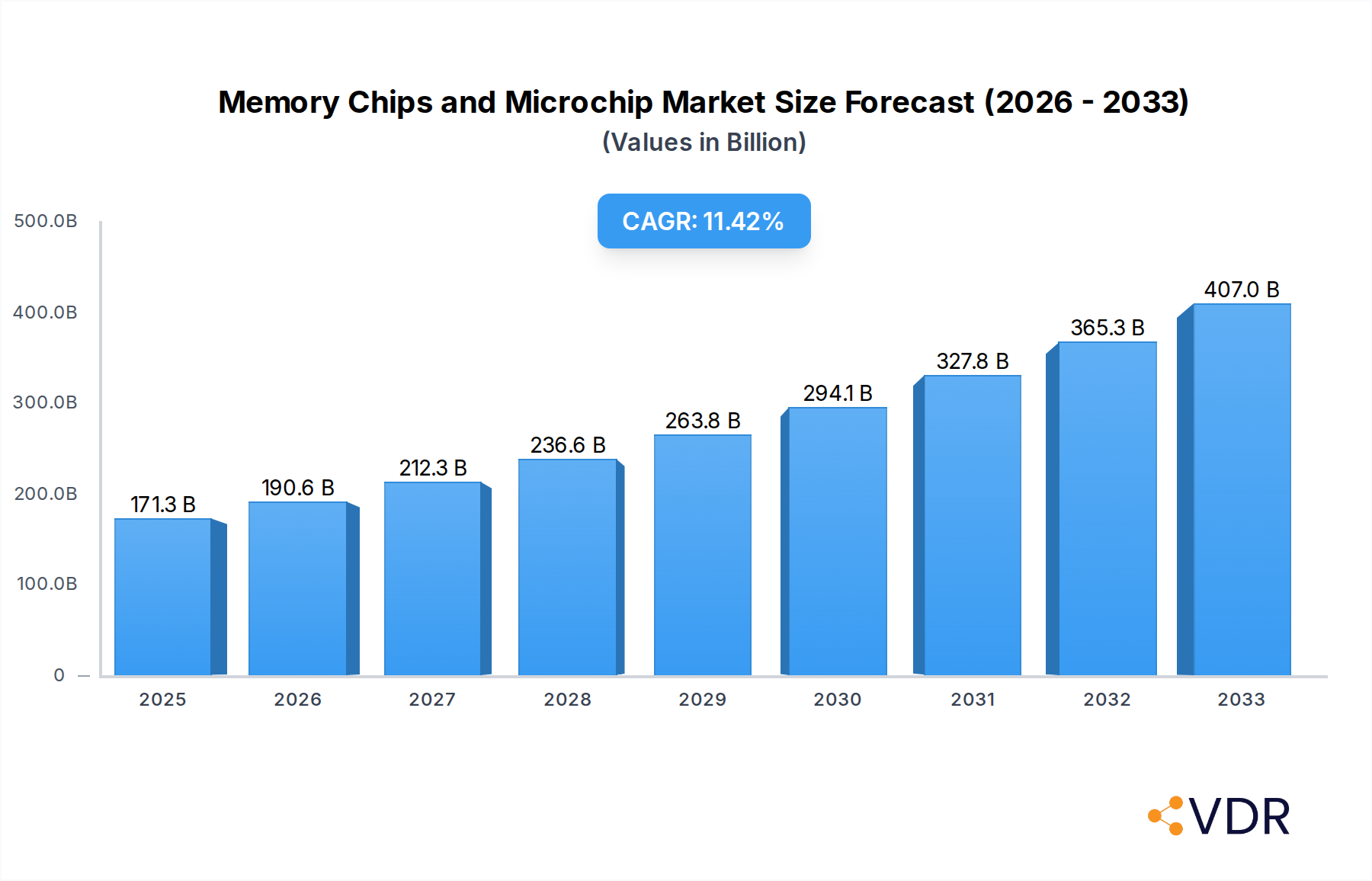

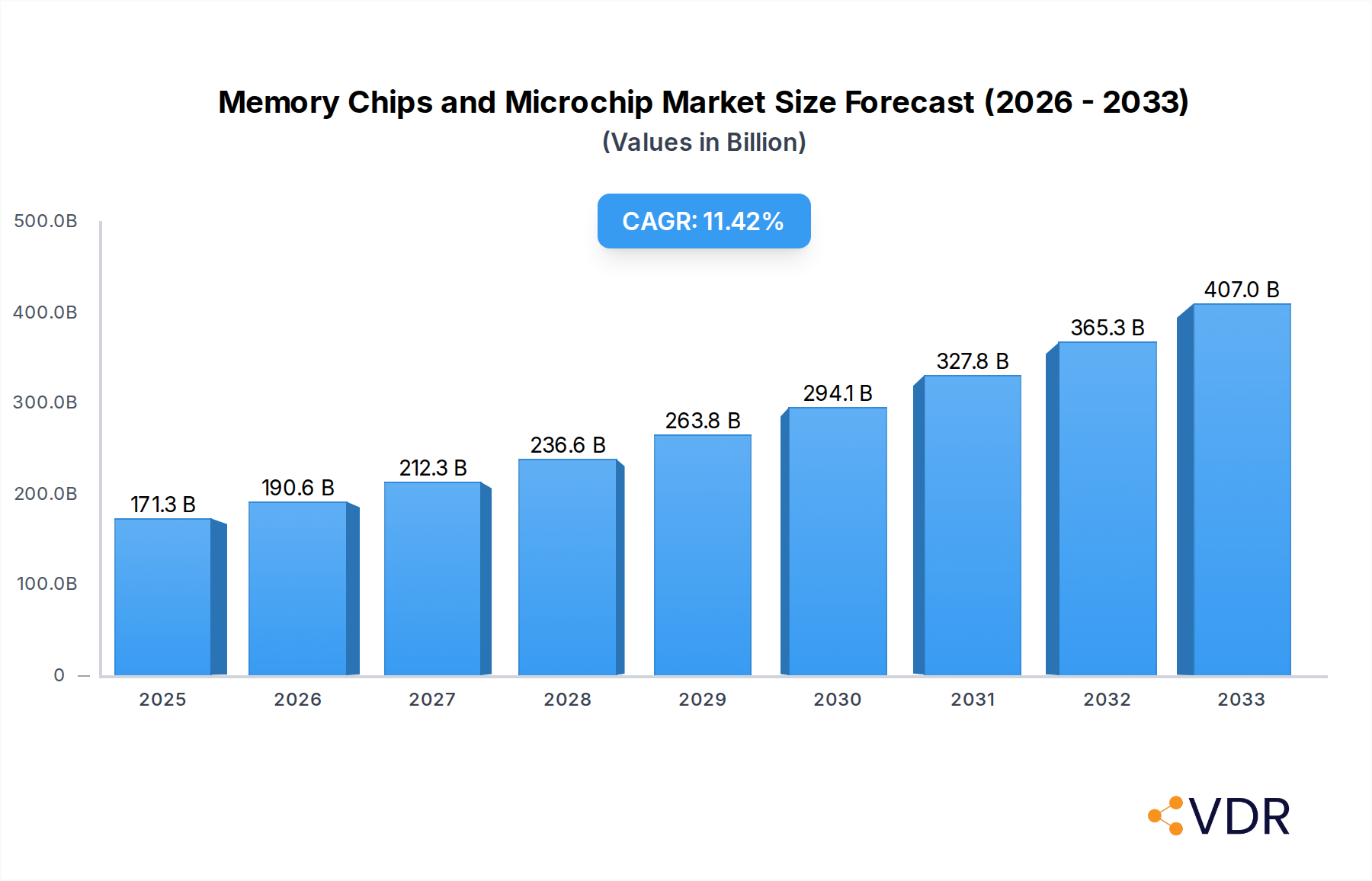

The global market for Memory Chips and Microchips is poised for significant expansion, projected to reach an estimated USD 171.31 billion in 2025. This robust growth is fueled by an impressive Compound Annual Growth Rate (CAGR) of 11.3% expected throughout the forecast period (2025-2033). The escalating demand for advanced electronic devices, particularly smartphones and tablets, serves as a primary driver. These devices, essential to modern life, continuously require more sophisticated and higher-capacity memory solutions to support their expanding functionalities, from high-resolution media consumption to complex applications and AI capabilities. Furthermore, the burgeoning adoption of IoT devices across various industries, the rapid development of 5G networks, and the increasing complexity of automotive electronics are all contributing factors that necessitate a continuous supply of high-performance memory chips. The sustained innovation in semiconductor technology, leading to smaller, faster, and more power-efficient memory solutions, further propels market growth.

Memory Chips and Microchip Market Size (In Billion)

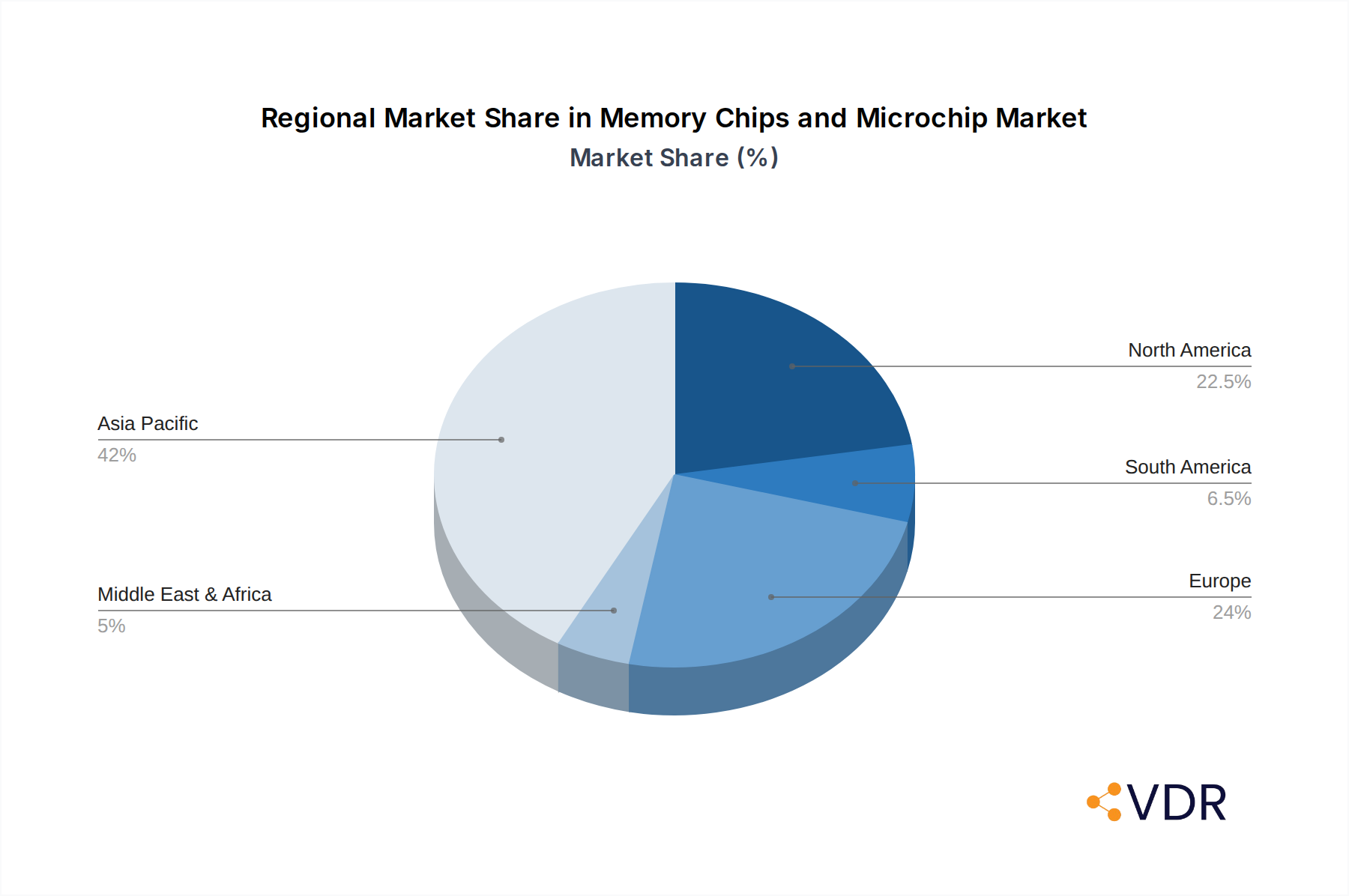

The market segmentation reveals a strong emphasis on higher storage capacities, with segments like 128GB and 256GB expected to witness substantial demand. This trend aligns with the growing need for extensive data storage in consumer electronics and enterprise applications. Geographically, the Asia Pacific region, led by China, Japan, and South Korea, is anticipated to dominate the market, driven by its strong manufacturing base and a rapidly growing consumer electronics market. North America and Europe also represent significant markets, owing to high per capita technology adoption and substantial investments in R&D and advanced manufacturing. Key industry players, including Samsung, SK Hynix, Micron Technology, and Western Digital, are at the forefront of innovation and production, actively shaping the market landscape through strategic investments in new technologies and capacity expansion to meet the surging global demand for memory solutions.

Memory Chips and Microchip Company Market Share

Memory Chips and Microchip Market Analysis: A Comprehensive 2025-2033 Outlook

This in-depth report provides a detailed analysis of the global memory chips and microchip market, a critical component of the semiconductor industry. Covering a study period from 2019 to 2033, with a base and estimated year of 2025 and a forecast period of 2025-2033, this report offers invaluable insights for industry professionals, investors, and strategists. We delve into market dynamics, growth trends, regional dominance, product landscape, key drivers, barriers, opportunities, and the influential players shaping this vital sector. All quantitative values are presented in billion units.

Memory Chips and Microchip Market Dynamics & Structure

The global memory chip and microchip market exhibits a moderately concentrated structure, with a few dominant players holding significant market share, while a long tail of smaller, specialized manufacturers contributes to the overall ecosystem. Technological innovation remains the primary engine, driven by the relentless demand for increased performance, lower power consumption, and higher storage densities across a multitude of applications. Advancements in NAND Flash and DRAM technologies, alongside emerging non-volatile memory solutions, are continuously pushing the boundaries of what's possible. Regulatory frameworks, particularly concerning trade policies and intellectual property rights, exert considerable influence on market access and competitive strategies. Competitive product substitutes, though less direct for core memory functions, emerge in the form of specialized controllers and alternative storage architectures that can impact the overall system cost and performance. End-user demographics are shifting, with an increasing reliance on data-intensive applications in consumer electronics, enterprise IT, and the burgeoning Internet of Things (IoT) segment. Mergers and acquisitions (M&A) continue to be a significant trend, as companies seek to consolidate market power, acquire critical technologies, and expand their product portfolios.

- Market Concentration: Characterized by a blend of large, integrated manufacturers and specialized component providers.

- Technological Innovation Drivers: Pursuit of higher storage density, faster read/write speeds, lower power consumption, and increased endurance.

- Regulatory Frameworks: Impact of trade tariffs, export controls, and intellectual property protection on global supply chains.

- Competitive Product Substitutes: Emerging advanced controller technologies and alternative storage solutions influencing system-level design.

- End-User Demographics: Growing demand from consumer electronics (smartphones, tablets), data centers, automotive, and industrial sectors.

- M&A Trends: Strategic acquisitions to gain market share, acquire patented technologies, and achieve economies of scale. For instance, the historical period saw numerous strategic collaborations and acquisitions, contributing to market consolidation.

Memory Chips and Microchip Growth Trends & Insights

The global memory chip and microchip market is poised for robust growth, driven by an insatiable appetite for data storage and processing power across diverse applications. Market size evolution is projected to witness a significant upward trajectory, fueled by increasing adoption rates of advanced memory technologies. The forecast period (2025–2033) is expected to see a Compound Annual Growth Rate (CAGR) of approximately 8.5%, reaching an estimated market size of $250 billion units by 2033. This expansion is underpinned by technological disruptions, such as the widespread implementation of Artificial Intelligence (AI) and Machine Learning (ML) requiring massive data processing capabilities, and the proliferation of 5G networks enabling new bandwidth-intensive applications. Consumer behavior shifts, including the growing demand for high-resolution media consumption, immersive gaming experiences, and the increasing complexity of mobile applications, are also key contributors. The penetration of solid-state drives (SSDs) in both consumer and enterprise markets continues to grow, displacing traditional hard disk drives (HDDs) in many segments due to their superior performance and energy efficiency. The "Others" application segment, encompassing industrial IoT, automotive, and edge computing, is emerging as a significant growth driver, exhibiting a CAGR exceeding 10%. The ≤32G segment, while mature, will continue to see steady demand, but higher capacity segments like 256G are expected to dominate future growth due to the increasing needs of advanced devices.

The historical period (2019–2024) provided a strong foundation, with steady growth driven by the smartphone revolution and the expansion of cloud computing. The base year of 2025 sets the stage for this accelerated growth, with an estimated market size of $180 billion units. Technological advancements such as High Bandwidth Memory (HBM) for AI accelerators and advancements in 3D NAND technology for higher density storage are critical enablers. The report leverages proprietary market intelligence and macroeconomic data to provide these precise metrics, offering a clear picture of the market's trajectory.

Dominant Regions, Countries, or Segments in Memory Chips and Microchip

Asia Pacific is unequivocally the dominant region in the memory chips and microchip market, driven by its colossal manufacturing capabilities, a burgeoning consumer electronics industry, and significant investments in R&D. China, in particular, is a powerhouse, with substantial domestic demand and increasing government support for its semiconductor industry, including significant investments in companies like Yangtze Memory. South Korea, home to global leaders like Samsung and SK Hynix, continues to spearhead innovation in DRAM and NAND Flash technologies. Taiwan, with its pivotal role in semiconductor manufacturing and design, also contributes significantly. The dominance of this region is further amplified by its position as the global hub for smartphone and tablet manufacturing, directly impacting the demand for memory solutions.

Within the Application segment, Smartphones consistently represent the largest market share, accounting for approximately 45% of the total demand in 2025, with an estimated 80 billion units consumed. This is closely followed by the Others segment, which includes a diverse range of applications like data centers, automotive, industrial IoT, and gaming consoles, expected to grow at a faster CAGR of 10.2% over the forecast period. The Tablets segment, while significant, is experiencing more moderate growth, with a projected 5% CAGR.

In terms of Types, the 256G segment is emerging as a key growth driver, driven by the need for higher storage capacity in premium smartphones, laptops, and other data-intensive devices. It is projected to grow at a CAGR of 12% and capture a substantial portion of the market by 2033. The 128G segment will continue to hold a strong market position, while the 64G segment will see stable demand. The ≤32G segment, though essential for entry-level devices and specific embedded applications, will experience slower growth compared to higher capacity offerings.

- Regional Dominance: Asia Pacific leads due to robust manufacturing ecosystems and high consumer demand.

- Country-Specific Growth: China's rapidly expanding domestic market and government initiatives; South Korea's technological prowess.

- Application Segment Leadership: Smartphones as the primary demand driver, with the "Others" segment exhibiting the highest growth potential.

- Type Segment Trends: Increasing demand for higher capacity memory (256G and 128G) driven by advanced device functionalities.

- Key Drivers of Dominance: Large population base, strong electronics manufacturing infrastructure, supportive government policies, and high adoption rates of technology.

Memory Chips and Microchip Product Landscape

The memory chips and microchip product landscape is characterized by rapid innovation and a constant push for enhanced performance and functionality. Advanced NAND Flash technologies, including advancements in 3D NAND architectures, are enabling higher storage densities and improved endurance for SSDs and embedded memory. High Bandwidth Memory (HBM) is crucial for AI and HPC applications, offering significantly increased memory bandwidth to feed powerful processors. DRAM continues to evolve with higher speeds and lower power consumption for PCs, servers, and mobile devices. Emerging non-volatile memory technologies, such as MRAM and ReRAM, are showing promise for specific niche applications demanding high speed and non-volatility.

Key Drivers, Barriers & Challenges in Memory Chips and Microchip

The memory chips and microchip market is propelled by several key drivers: the exponential growth of data, the pervasive adoption of smartphones and other connected devices, the expansion of cloud computing and data centers, and the increasing demand for AI and IoT solutions. Technological advancements in manufacturing processes and materials are crucial enablers.

However, the market faces significant barriers and challenges. Geopolitical tensions and supply chain disruptions, as highlighted by recent global events, pose substantial risks to production and availability. The capital-intensive nature of semiconductor manufacturing necessitates enormous investments, creating high barriers to entry. Intense competition and price pressures can impact profitability. Additionally, the constant need for R&D to keep pace with technological evolution requires sustained investment and innovation. Environmental regulations and concerns regarding energy consumption in data centers are also becoming increasingly important.

- Key Drivers:

- Explosive data generation across all sectors.

- Ubiquitous adoption of smartphones and advanced mobile devices.

- Growth of cloud infrastructure and big data analytics.

- Rise of Artificial Intelligence and Machine Learning applications.

- Proliferation of the Internet of Things (IoT) devices.

- Barriers & Challenges:

- Global supply chain vulnerabilities and geopolitical risks.

- High capital expenditure for advanced manufacturing facilities.

- Intense price competition and commoditization in certain segments.

- Rapid pace of technological obsolescence requiring continuous R&D.

- Stringent environmental regulations and energy efficiency demands.

Emerging Opportunities in Memory Chips and Microchip

Emerging opportunities abound in the memory chips and microchip sector. The rapidly expanding automotive sector, with its increasing demand for in-car infotainment systems, advanced driver-assistance systems (ADAS), and autonomous driving technologies, presents a significant growth avenue. The edge computing market, driven by the need for localized data processing and reduced latency, is creating demand for specialized, power-efficient memory solutions. Furthermore, the development of new memory technologies beyond NAND and DRAM, such as resistive RAM (ReRAM) and magnetoresistive RAM (MRAM), offers opportunities for niche applications requiring unique performance characteristics. The increasing focus on sustainable computing and energy-efficient memory solutions will also drive innovation and market expansion.

Growth Accelerators in the Memory Chips and Microchip Industry

Several factors are poised to accelerate growth in the memory chips and microchip industry. Continued advancements in semiconductor fabrication technologies, including the transition to smaller process nodes and improved 3D stacking techniques, will enable higher capacities and better performance. Strategic partnerships and collaborations between memory manufacturers, device makers, and software developers will foster innovation and optimize memory integration within new product designs. The expansion of 5G and future wireless communication technologies will unlock new applications and drive demand for high-speed, high-capacity memory. Furthermore, the increasing digitalization of industries and the growing adoption of smart city initiatives will create sustained demand for memory components across a wide array of applications.

Key Players Shaping the Memory Chips and Microchip Market

- Toshiba

- Samsung

- SK Hynix

- SanDisk

- Yangtze Memory

- Silicon Motion

- ICMAX

- Shenzhen Himory

- Kingston Technology

- Micron Technology

- Seagate Technology

- Greenliant Systems

- Western Digital

Notable Milestones in Memory Chips and Microchip Sector

- 2019: Samsung announces advancements in 7nm EUV DRAM manufacturing, enabling higher density and performance.

- 2020: Western Digital and Kioxia unveil innovations in 162-layer 3D NAND flash technology, pushing storage capacity limits.

- 2021: SK Hynix demonstrates its first 24Gb DDR5 DRAM chip, setting a new standard for server memory performance.

- 2022: Yangtze Memory Technology Corp. (YMTC) makes significant strides in its Xtacking 2.0 architecture for advanced NAND flash production.

- 2023: Micron Technology introduces its GDDR6X memory, powering next-generation graphics cards.

- 2024: Increased investment in AI-specific memory solutions like HBM to meet the growing demands of artificial intelligence workloads.

In-Depth Memory Chips and Microchip Market Outlook

The future outlook for the memory chips and microchip market remains exceptionally bright, driven by an ongoing digital transformation that necessitates ever-increasing data storage and processing capabilities. Growth accelerators such as the widespread deployment of AI, the continued evolution of 5G and beyond, and the expansion of the metaverse and immersive digital experiences will create sustained demand. Strategic opportunities lie in developing specialized memory solutions for emerging sectors like automotive and edge computing, as well as in the continuous pursuit of higher performance, lower power consumption, and greater sustainability. Companies that can navigate the complexities of global supply chains and consistently innovate will be well-positioned for significant growth and market leadership in the coming years.

Memory Chips and Microchip Segmentation

-

1. Application

- 1.1. Smartphones

- 1.2. Tablets

- 1.3. Others

-

2. Types

- 2.1. ≤32G

- 2.2. 64G

- 2.3. 128G

- 2.4. 256G

Memory Chips and Microchip Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Memory Chips and Microchip Regional Market Share

Geographic Coverage of Memory Chips and Microchip

Memory Chips and Microchip REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Memory Chips and Microchip Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Smartphones

- 5.1.2. Tablets

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. ≤32G

- 5.2.2. 64G

- 5.2.3. 128G

- 5.2.4. 256G

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Memory Chips and Microchip Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Smartphones

- 6.1.2. Tablets

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. ≤32G

- 6.2.2. 64G

- 6.2.3. 128G

- 6.2.4. 256G

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Memory Chips and Microchip Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Smartphones

- 7.1.2. Tablets

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. ≤32G

- 7.2.2. 64G

- 7.2.3. 128G

- 7.2.4. 256G

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Memory Chips and Microchip Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Smartphones

- 8.1.2. Tablets

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. ≤32G

- 8.2.2. 64G

- 8.2.3. 128G

- 8.2.4. 256G

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Memory Chips and Microchip Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Smartphones

- 9.1.2. Tablets

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. ≤32G

- 9.2.2. 64G

- 9.2.3. 128G

- 9.2.4. 256G

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Memory Chips and Microchip Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Smartphones

- 10.1.2. Tablets

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. ≤32G

- 10.2.2. 64G

- 10.2.3. 128G

- 10.2.4. 256G

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Toshiba

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Samsung

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 SK Hynix

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 SanDisk

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Yangtze Memory

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Silicon Motion

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 ICMAX

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Shenzhen Himory

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Kingston Technology

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Micron Technologyhttps

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Seagate Technology

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Greenliant Systems

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Western Digital

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.1 Toshiba

List of Figures

- Figure 1: Global Memory Chips and Microchip Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Memory Chips and Microchip Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Memory Chips and Microchip Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Memory Chips and Microchip Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Memory Chips and Microchip Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Memory Chips and Microchip Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Memory Chips and Microchip Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Memory Chips and Microchip Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Memory Chips and Microchip Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Memory Chips and Microchip Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Memory Chips and Microchip Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Memory Chips and Microchip Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Memory Chips and Microchip Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Memory Chips and Microchip Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Memory Chips and Microchip Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Memory Chips and Microchip Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Memory Chips and Microchip Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Memory Chips and Microchip Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Memory Chips and Microchip Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Memory Chips and Microchip Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Memory Chips and Microchip Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Memory Chips and Microchip Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Memory Chips and Microchip Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Memory Chips and Microchip Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Memory Chips and Microchip Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Memory Chips and Microchip Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Memory Chips and Microchip Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Memory Chips and Microchip Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Memory Chips and Microchip Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Memory Chips and Microchip Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Memory Chips and Microchip Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Memory Chips and Microchip Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Memory Chips and Microchip Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Memory Chips and Microchip Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Memory Chips and Microchip Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Memory Chips and Microchip Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Memory Chips and Microchip Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Memory Chips and Microchip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Memory Chips and Microchip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Memory Chips and Microchip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Memory Chips and Microchip Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Memory Chips and Microchip Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Memory Chips and Microchip Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Memory Chips and Microchip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Memory Chips and Microchip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Memory Chips and Microchip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Memory Chips and Microchip Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Memory Chips and Microchip Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Memory Chips and Microchip Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Memory Chips and Microchip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Memory Chips and Microchip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Memory Chips and Microchip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Memory Chips and Microchip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Memory Chips and Microchip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Memory Chips and Microchip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Memory Chips and Microchip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Memory Chips and Microchip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Memory Chips and Microchip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Memory Chips and Microchip Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Memory Chips and Microchip Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Memory Chips and Microchip Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Memory Chips and Microchip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Memory Chips and Microchip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Memory Chips and Microchip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Memory Chips and Microchip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Memory Chips and Microchip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Memory Chips and Microchip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Memory Chips and Microchip Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Memory Chips and Microchip Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Memory Chips and Microchip Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Memory Chips and Microchip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Memory Chips and Microchip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Memory Chips and Microchip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Memory Chips and Microchip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Memory Chips and Microchip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Memory Chips and Microchip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Memory Chips and Microchip Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Memory Chips and Microchip?

The projected CAGR is approximately 11.3%.

2. Which companies are prominent players in the Memory Chips and Microchip?

Key companies in the market include Toshiba, Samsung, SK Hynix, SanDisk, Yangtze Memory, Silicon Motion, ICMAX, Shenzhen Himory, Kingston Technology, Micron Technologyhttps, Seagate Technology, Greenliant Systems, Western Digital.

3. What are the main segments of the Memory Chips and Microchip?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Memory Chips and Microchip," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Memory Chips and Microchip report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Memory Chips and Microchip?

To stay informed about further developments, trends, and reports in the Memory Chips and Microchip, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence