Key Insights

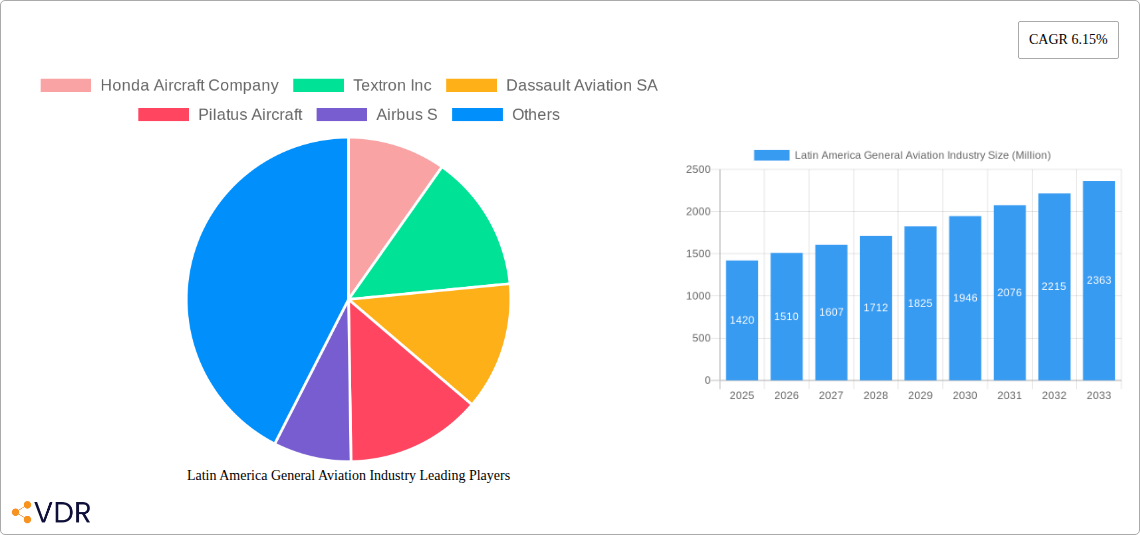

The Latin American general aviation market, valued at $1.42 billion in 2025, is projected to experience robust growth, driven by factors such as increasing tourism, infrastructure development, and the expanding business aviation sector. The region's diverse geography and significant distances between cities necessitate air travel, particularly for business and leisure purposes, fueling demand for helicopters, piston fixed-wing aircraft, turboprops, and business jets. Brazil and Mexico represent the largest markets within Latin America, accounting for a substantial portion of the overall market size. Growth is further propelled by governmental initiatives focused on improving air connectivity and supporting the development of the aviation industry. While economic fluctuations and regulatory hurdles could pose challenges, the long-term outlook remains positive, underpinned by sustained economic growth in key Latin American nations and increasing disposable incomes within the region's burgeoning middle class. The segment breakdown suggests a significant demand for diverse aircraft types, catering to various needs and operational requirements. The presence of major global players, alongside regional operators, signifies a competitive landscape encouraging innovation and service improvements within the Latin American general aviation sector.

Latin America General Aviation Industry Market Size (In Billion)

The forecast period (2025-2033) anticipates a compound annual growth rate (CAGR) of 6.15%, resulting in significant market expansion. This growth trajectory will be influenced by several key trends, including the adoption of advanced technologies in aircraft manufacturing, increasing utilization of business jets by corporations and high-net-worth individuals, and a growing preference for efficient and flexible air travel solutions. However, potential restraints include economic uncertainty in certain Latin American countries and the need for continued investment in airport infrastructure to fully realize the market's potential. This necessitates a collaborative effort between governments, industry stakeholders, and aviation service providers to overcome challenges and ensure the sustainable growth of the general aviation sector in Latin America. The market's segmentation, covering various aircraft types across key Latin American countries, offers a detailed understanding of regional demand patterns and enables strategic planning for manufacturers and service providers.

Latin America General Aviation Industry Company Market Share

This comprehensive report provides a detailed analysis of the Latin America General Aviation (GA) industry, encompassing market dynamics, growth trends, regional performance, product landscape, key players, and future outlook. The study period covers 2019-2033, with 2025 as the base and estimated year. The report offers invaluable insights for industry professionals, investors, and strategic decision-makers seeking to understand and capitalize on opportunities within this dynamic market.

Latin America General Aviation Industry Market Dynamics & Structure

The Latin America GA market is characterized by a moderately fragmented structure, with a mix of multinational corporations and regional players. Market concentration is relatively low, with no single entity commanding a dominant share. Technological innovation, driven by increasing demand for advanced avionics and safety features, is a key dynamic. Regulatory frameworks vary across Latin American nations, impacting operational costs and market access. Competitive substitutes, such as commercial air travel for shorter distances, exert pressure, particularly in the business jet segment. The end-user demographic is diverse, encompassing private owners, charter operators, corporate fleets, and government agencies. M&A activity has been moderate, with a focus on consolidating regional operators and enhancing market share.

- Market Concentration: Low to moderate, with top 5 players holding approximately xx% market share (2025 estimate).

- Technological Innovation Drivers: Advanced avionics, enhanced safety features, fuel-efficient engines.

- Regulatory Frameworks: Varying regulations across countries, impacting operational costs and ease of entry.

- Competitive Substitutes: Commercial airlines, particularly for shorter routes.

- End-User Demographics: Private owners, charter operators, corporations, government agencies.

- M&A Trends: Moderate activity, focused on consolidation and expansion. Estimated xx M&A deals in 2019-2024.

Latin America General Aviation Industry Growth Trends & Insights

The Latin America GA market experienced [Insert quantitative data based on your XXX source - e.g., a CAGR of x% during 2019-2024] driven by factors such as increasing disposable incomes in certain segments of the population, expanding business travel needs, and the growth of tourism in key regions. Adoption rates vary across aircraft types, with business jets experiencing faster growth than piston fixed-wing aircraft. Technological disruptions, such as the development of electric and hybrid-electric aircraft, are poised to reshape the market in the coming years. Shifting consumer preferences toward greater safety, comfort, and technological sophistication are also driving market evolution. The market is expected to experience a CAGR of xx% during the forecast period (2025-2033), reaching a market size of xx million units by 2033. Market penetration is highest in Brazil and Mexico, with significant untapped potential in the rest of Latin America.

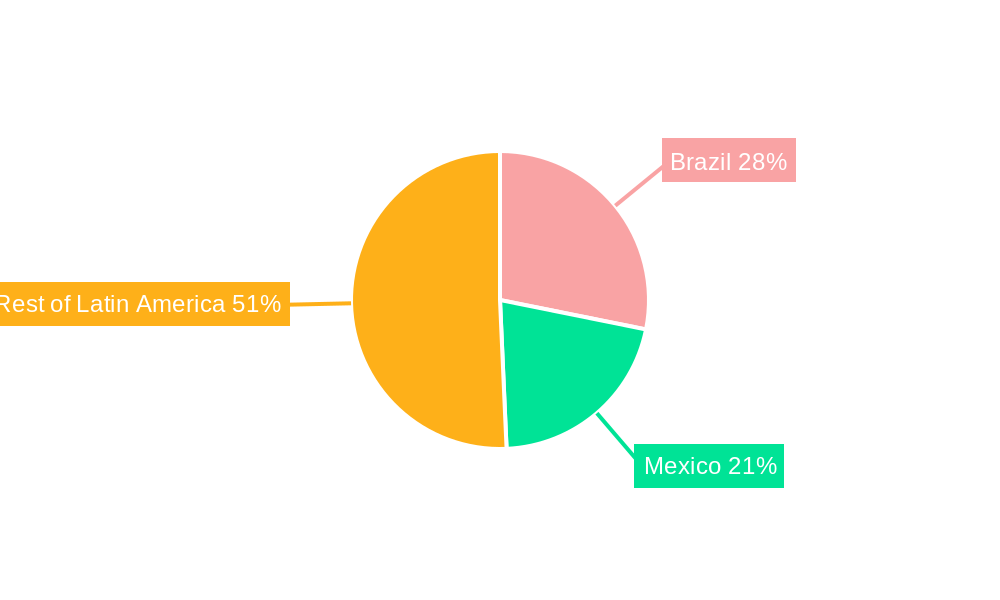

Dominant Regions, Countries, or Segments in Latin America General Aviation Industry

Brazil and Mexico are the dominant markets in the Latin American GA industry, accounting for approximately xx% and yy% of the total market size in 2025, respectively. The business jet segment exhibits the highest growth potential due to increasing demand from high-net-worth individuals and corporations.

- Brazil: Strong economic growth, robust infrastructure in key areas, and a large domestic market drive its dominance.

- Mexico: Growing tourism sector, increased business activities, and a relatively developed GA infrastructure contribute to its significant market share.

- Rest of Latin America: Significant untapped potential for growth, hampered by limited infrastructure development and economic disparities across regions.

- Business Jets: Fastest-growing segment driven by increasing high-net-worth individuals and corporate demand.

- Helicopters: Steady growth driven by emergency medical services (EMS), oil & gas operations, and law enforcement.

- Turboprops: Significant market share, serving general purpose and regional transport needs.

- Piston Fixed-wing: Mature segment with relatively stable demand.

Latin America General Aviation Industry Product Landscape

The Latin American GA market features a diverse range of aircraft types, from single-engine piston aircraft to sophisticated business jets. Innovation focuses on enhancing fuel efficiency, integrating advanced avionics, and improving safety features. Key selling propositions include superior performance, enhanced comfort, and advanced technological capabilities. Recent technological advancements include the incorporation of fly-by-wire systems, improved engine designs, and advanced materials for lighter and stronger airframes.

Key Drivers, Barriers & Challenges in Latin America General Aviation Industry

Key Drivers:

- Growing economies and rising disposable incomes.

- Expansion of tourism and business travel.

- Demand for efficient and reliable transportation solutions.

- Technological advancements in aircraft design and avionics.

Challenges:

- Infrastructure limitations in certain regions.

- High operating costs, including fuel and maintenance.

- Regulatory hurdles and bureaucratic complexities.

- Intense competition from established players.

- xx% increase in maintenance costs due to supply chain disruptions (estimated).

Emerging Opportunities in Latin America General Aviation Industry

- Expanding charter services to underserved regions.

- Growth of air taxi services.

- Adoption of advanced air mobility (AAM) solutions.

- Development of sustainable aviation fuels (SAF) to reduce environmental impact.

- Increased demand for specialized aircraft, like agricultural aircraft and aerial survey aircraft.

Growth Accelerators in the Latin America General Aviation Industry

Technological breakthroughs in aircraft design, the adoption of sustainable aviation practices, strategic partnerships between manufacturers and operators, and targeted market expansion strategies in less-developed regions are key growth catalysts for the Latin American GA industry. Government incentives promoting GA development are also expected to accelerate market growth.

Key Players Shaping the Latin America General Aviation Industry Market

Notable Milestones in Latin America General Aviation Industry Sector

- 2021: Embraer SA launched a new generation of regional jets.

- 2022: Increased investment in GA infrastructure development by the Mexican government.

- 2023: Several M&A deals involving regional GA operators in Brazil.

- 2024: Introduction of new safety regulations in several Latin American countries. (Further milestones to be added based on available data)

In-Depth Latin America General Aviation Industry Market Outlook

The Latin American GA market is poised for sustained growth over the forecast period (2025-2033), driven by strong economic growth in key regions, increasing demand for air travel, and ongoing technological advancements. Strategic opportunities exist in developing new markets, expanding existing services, and adopting innovative business models. Continued investment in infrastructure and supportive government policies will play a vital role in realizing the market's full potential. The market is expected to reach xx million units by 2033.

Latin America General Aviation Industry Segmentation

-

1. Type

- 1.1. Helicopters

- 1.2. Piston Fixed-wing

- 1.3. Turboprop

- 1.4. Business Jet

Latin America General Aviation Industry Segmentation By Geography

-

1. Latin America

- 1.1. Brazil

- 1.2. Argentina

- 1.3. Chile

- 1.4. Colombia

- 1.5. Mexico

- 1.6. Peru

- 1.7. Venezuela

- 1.8. Ecuador

- 1.9. Bolivia

- 1.10. Paraguay

Latin America General Aviation Industry Regional Market Share

Geographic Coverage of Latin America General Aviation Industry

Latin America General Aviation Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.15% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Helicopters

- 5.1.2. Piston Fixed-wing

- 5.1.3. Turboprop

- 5.1.4. Business Jet

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Latin America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Latin America General Aviation Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Helicopters

- 6.1.2. Piston Fixed-wing

- 6.1.3. Turboprop

- 6.1.4. Business Jet

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Honda Aircraft Company

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Textron Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Dassault Aviation SA

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Pilatus Aircraft

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Airbus S

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Embraer SA

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Leonardo S p A

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Bombardier Inc

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Gulfstream Aerospace Corporation

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Piper Aircraft Inc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 AeroAndina SA

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 Honda Aircraft Company

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Latin America General Aviation Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Latin America General Aviation Industry Share (%) by Company 2025

List of Tables

- Table 1: Latin America General Aviation Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Latin America General Aviation Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Latin America General Aviation Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 4: Latin America General Aviation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 5: Brazil Latin America General Aviation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 6: Argentina Latin America General Aviation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 7: Chile Latin America General Aviation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Colombia Latin America General Aviation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Latin America General Aviation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Peru Latin America General Aviation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Venezuela Latin America General Aviation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Ecuador Latin America General Aviation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Bolivia Latin America General Aviation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Paraguay Latin America General Aviation Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Latin America General Aviation Industry?

The projected CAGR is approximately 6.15%.

2. Which companies are prominent players in the Latin America General Aviation Industry?

Key companies in the market include Honda Aircraft Company, Textron Inc, Dassault Aviation SA, Pilatus Aircraft, Airbus S, Embraer SA, Leonardo S p A, Bombardier Inc, Gulfstream Aerospace Corporation, Piper Aircraft Inc, AeroAndina SA.

3. What are the main segments of the Latin America General Aviation Industry?

The market segments include Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.42 Million as of 2022.

5. What are some drivers contributing to market growth?

Increase in Internet of Things (IoT) and Autonomous Systems; Rise in Demand for Military and Defense Satellite Communication Solutions.

6. What are the notable trends driving market growth?

The Helicopters Segment to Experience the Highest Growth During the Forecast Period.

7. Are there any restraints impacting market growth?

Cybersecurity Threats to Satellite Communication; Interference in Transmission of Data.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Latin America General Aviation Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Latin America General Aviation Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Latin America General Aviation Industry?

To stay informed about further developments, trends, and reports in the Latin America General Aviation Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence