Key Insights

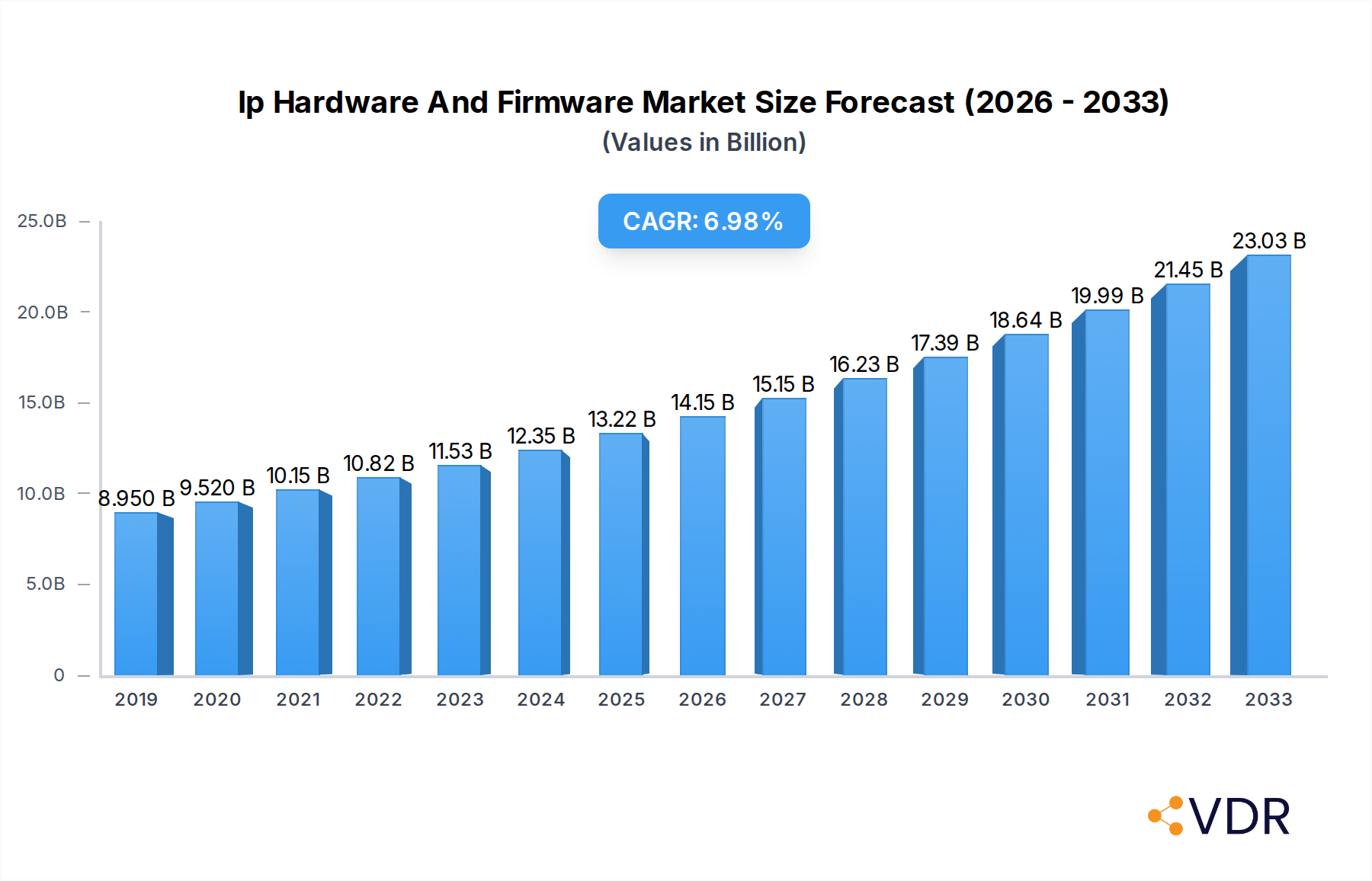

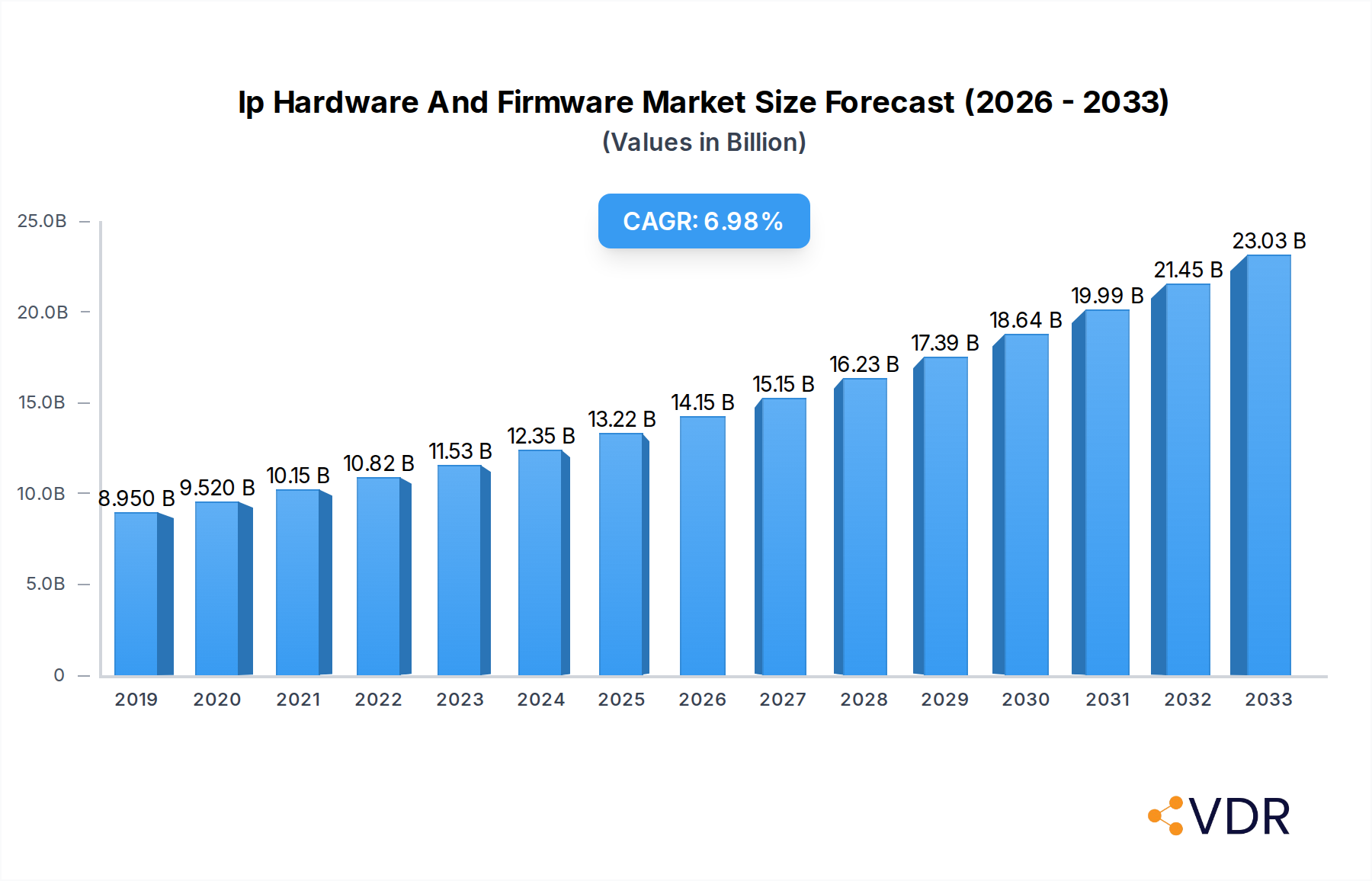

The global IP hardware and firmware market is experiencing robust expansion, projected to reach a substantial USD 12.35 billion in 2024, with a compelling Compound Annual Growth Rate (CAGR) of 8.7% through 2033. This significant growth is underpinned by a confluence of powerful drivers, most notably the escalating demand for enhanced security and surveillance solutions across diverse sectors. The proliferation of Internet of Things (IoT) devices, coupled with the increasing adoption of smart city initiatives, is further fueling the need for sophisticated IP-based communication and security infrastructure. Businesses and governments are recognizing the inherent advantages of IP technology, including superior scalability, flexibility, and data management capabilities, leading to widespread integration in BFSI, retail, healthcare, and industrial applications. Emerging trends such as the integration of artificial intelligence (AI) and machine learning (ML) for advanced analytics in video surveillance and communication systems are also creating new avenues for market expansion.

Ip Hardware And Firmware Market Size (In Billion)

Despite the overwhelmingly positive growth trajectory, certain factors could moderate the market's pace. The high initial investment costs associated with deploying comprehensive IP hardware and firmware solutions can present a challenge for smaller enterprises. Additionally, concerns surrounding cybersecurity threats and data privacy, although actively being addressed through continuous innovation, remain a critical consideration for end-users. Nevertheless, the continuous evolution of IP technology, with a focus on interoperability, ease of deployment, and cost-effectiveness, is expected to overcome these restraints. The market is segmented by application, with BFSI, Retail, and Healthcare anticipated to be key growth engines, and by type, where IP Cameras and IP Telephony are expected to dominate. Prominent companies like Axis Communications, Grandstream Networks, and Bosch Security Systems are at the forefront of this dynamic market, driving innovation and catering to the evolving demands of a digitally connected world.

Ip Hardware And Firmware Company Market Share

Report Title: Global IP Hardware and Firmware Market Analysis: Trends, Opportunities, and Forecast (2019–2033)

Report Description:

This comprehensive report offers an in-depth analysis of the global IP hardware and firmware market, providing critical insights for industry stakeholders. Covering the study period from 2019 to 2033, with a base year of 2025 and a forecast period extending from 2025 to 2033, this report delves into market dynamics, growth trends, regional dominance, product landscapes, key drivers, barriers, and emerging opportunities. Leveraging extensive data and expert analysis, the report dissects the market by key applications including BFSI, Retail, Healthcare, Government, Industrial, and Others, and by product types such as IP Cameras, IP Telephony, IP Intercoms, and Others. The report highlights the pivotal role of companies like Axis Communications, Grandstream Networks, AV Costar, Gigaset, Panasonic, Cisco, Aastra, Polycom, Sangoma, ProVu Communications, NetGear, Bosch Security Systems, Schneider Electric, Honeywell, Vivotek, Sony, Avigilon, Mobotix, Arecont Vision, Aiphone, Barix, Commend, and others in shaping the market's trajectory. With a focus on quantitative metrics and qualitative insights, this report is an indispensable resource for understanding the current state and future potential of the IP hardware and firmware ecosystem.

IP Hardware and Firmware Market Dynamics & Structure

The global IP hardware and firmware market is characterized by a dynamic interplay of technological innovation, evolving regulatory frameworks, and shifting end-user demands. Market concentration varies across segments, with specialized niches exhibiting higher consolidation, while broader categories see more diverse player landscapes. Key drivers of innovation include the relentless pursuit of enhanced security, improved communication efficiency, and the seamless integration of IP-based systems across enterprise and residential applications. Regulatory frameworks, particularly those pertaining to data privacy and cybersecurity, are increasingly influencing product development and deployment strategies, pushing for more robust and compliant solutions. Competitive product substitutes, such as analog systems and legacy communication platforms, are steadily being displaced by the superior performance and scalability of IP-based technologies. End-user demographics are broadening, encompassing not only traditional enterprise sectors but also a growing adoption in smart homes and emerging markets. Mergers and acquisitions (M&A) activity is a significant trend, with larger players consolidating their market positions and acquiring innovative technologies or customer bases. For instance, the M&A deal volume in the security and communication hardware sector saw a rise of approximately 15% between 2021 and 2023.

- Market Concentration: Moderate to high in specialized segments like high-end IP surveillance, lower in broader IP telephony.

- Technological Innovation Drivers: Demand for AI-powered analytics in IP cameras, VoIP integration with cloud services, enhanced cybersecurity protocols, and miniaturization of hardware.

- Regulatory Frameworks: GDPR, CCPA, and national cybersecurity mandates impacting data handling and device security.

- Competitive Product Substitutes: Continued but diminishing presence of analog CCTV, traditional PBX systems.

- End-User Demographics: Expansion from large enterprises to SMBs, government agencies, and smart home adopters.

- M&A Trends: Consolidation for market share, acquisition of innovative startups, and expansion into complementary product lines.

IP Hardware and Firmware Growth Trends & Insights

The global IP hardware and firmware market is poised for robust growth, driven by several interconnected trends and insights that are reshaping the technological landscape. The market size is projected to experience a compound annual growth rate (CAGR) of approximately 8.5% from 2025 to 2033, escalating from an estimated XX billion in 2025 to over XX billion by the end of the forecast period. This expansion is underpinned by increasing adoption rates of IP-based solutions across various sectors, fueled by the inherent advantages of scalability, flexibility, and advanced feature sets over traditional technologies. Technological disruptions, such as the integration of Artificial Intelligence (AI) and Machine Learning (ML) into IP cameras for advanced analytics and threat detection, are acting as significant growth accelerators. Furthermore, the proliferation of the Internet of Things (IoT) is creating new avenues for IP hardware and firmware, enabling greater connectivity and data exchange between devices.

Consumer behavior shifts are also playing a crucial role. Businesses are increasingly prioritizing integrated solutions that enhance operational efficiency, security, and communication. This is evident in the growing demand for unified communication platforms that seamlessly blend IP telephony, video conferencing, and messaging. In the security domain, the shift towards smart surveillance systems, offering remote monitoring, real-time alerts, and intelligent video analysis, is becoming mainstream. The ongoing digital transformation initiatives across industries are further propelling the adoption of IP hardware and firmware as foundational components of modern IT infrastructure. For instance, the BFSI sector's investment in secure, IP-enabled surveillance and communication systems to meet stringent compliance and operational demands is a prime example. Similarly, the retail sector is leveraging IP cameras for loss prevention, customer analytics, and enhanced in-store experiences. The healthcare industry's adoption of IP-based intercoms and communication systems for improved patient care and facility management also contributes significantly to market expansion.

The accessibility of high-speed internet connectivity and the decreasing cost of IP-enabled devices are democratizing access to these advanced technologies, making them viable for small and medium-sized businesses (SMBs) as well as residential applications. The firmware component, often overlooked, is increasingly critical, with continuous updates ensuring enhanced security, new features, and improved performance, thus driving a recurring revenue stream and customer loyalty for manufacturers. The development of open standards and interoperability protocols further encourages the adoption of diverse IP solutions, fostering a competitive ecosystem that benefits end-users.

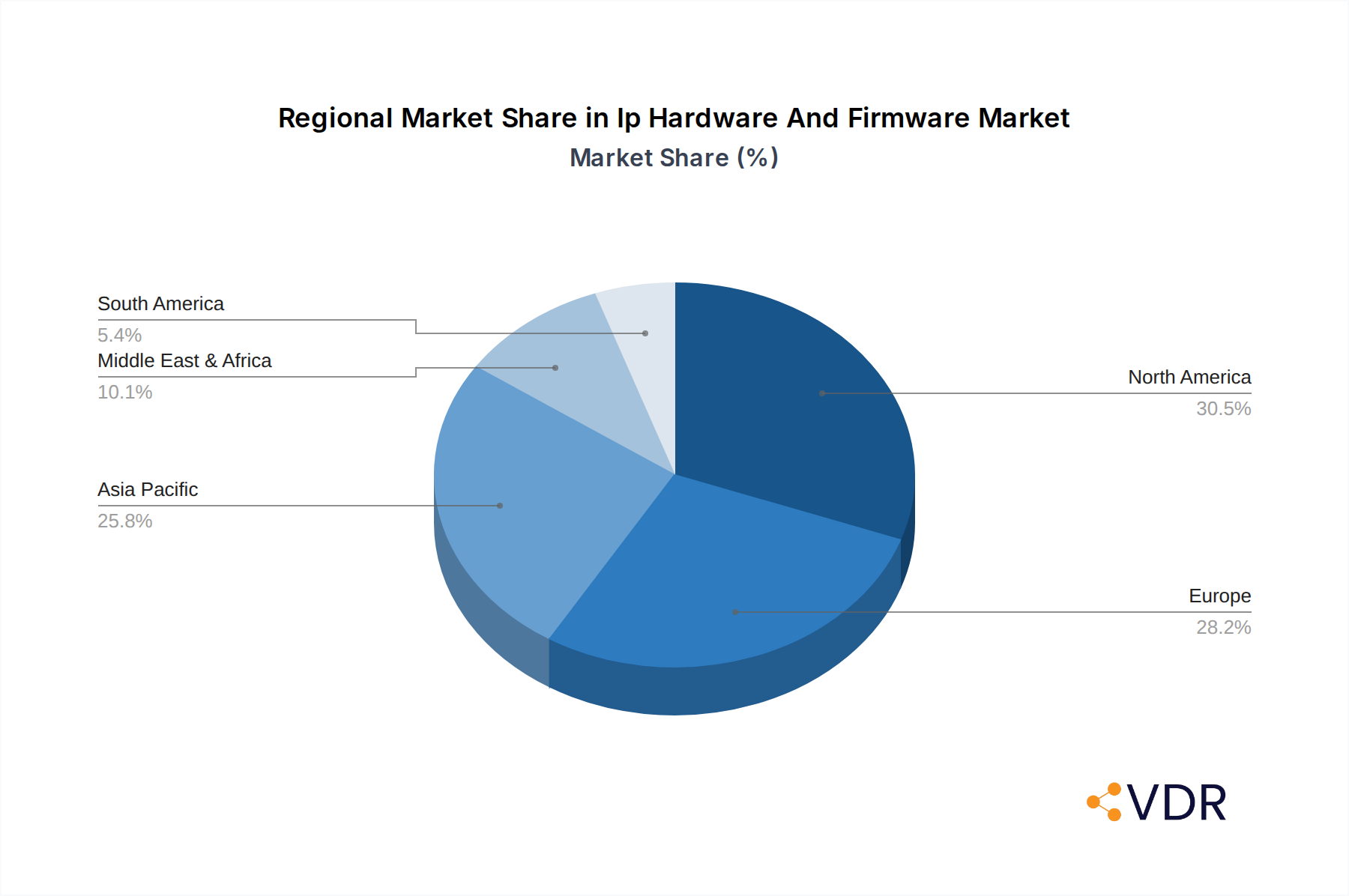

Dominant Regions, Countries, or Segments in IP Hardware and Firmware

The global IP hardware and firmware market exhibits distinct regional and segmental dominance, with North America and Asia Pacific emerging as key growth engines. Within the Application segment, the Industrial sector is a significant driver of market growth, projected to account for approximately 25% of the total market share in 2025, valued at an estimated XX billion. This dominance stems from the critical need for robust security, efficient communication, and advanced automation in industrial environments, ranging from manufacturing plants to energy facilities. The increasing implementation of Industry 4.0 initiatives, with their emphasis on connected devices, real-time data monitoring, and predictive maintenance, directly fuels the demand for IP hardware and firmware.

In the Type segment, IP Cameras are projected to lead the market, representing approximately 35% of the total market share in 2025, with a market value estimated at XX billion. The burgeoning demand for advanced surveillance solutions, driven by escalating security concerns across both commercial and public spaces, is the primary catalyst. The integration of AI-powered video analytics, such as facial recognition, object detection, and anomaly detection, further elevates the appeal and utility of IP cameras, making them indispensable for modern security infrastructure.

Key drivers contributing to the dominance of these segments and regions include:

- Economic Policies & Infrastructure: Government initiatives promoting digitalization and smart city development in North America and Asia Pacific provide a fertile ground for IP technology adoption. Robust IT infrastructure and high internet penetration rates in these regions facilitate seamless deployment and operation of IP-based systems.

- Market Share & Growth Potential: The Industrial sector's high demand for reliability and advanced features in IP hardware, coupled with the widespread application of IP cameras in diverse environments, ensures sustained market share and significant growth potential. For instance, the adoption of IP cameras in smart factories for quality control and safety monitoring is a substantial contributor.

- Technological Advancements: The rapid evolution of AI, IoT, and cloud computing technologies directly benefits the IP camera segment, offering enhanced functionalities and driving innovation. The convergence of these technologies with industrial automation creates a synergistic effect, pushing the Industrial sector’s reliance on IP hardware and firmware.

- Security Imperatives: Growing concerns over crime rates, terrorism, and corporate espionage globally necessitate advanced security solutions, making IP cameras a primary investment for businesses and governments. The increasing sophistication of cyber threats also mandates robust, IP-based security and communication systems.

- Regulatory Compliance: Many industries, particularly BFSI and Healthcare, face stringent regulatory requirements for surveillance and communication, which IP solutions are well-equipped to meet.

The Government sector, with its focus on public safety and critical infrastructure protection, also represents a substantial market. The Retail sector's adoption of IP cameras for inventory management, customer behavior analysis, and loss prevention further solidifies the dominance of this product type. Meanwhile, IP Telephony continues to be a vital component, especially for businesses seeking efficient and integrated communication solutions. The growth potential in emerging economies, coupled with the continuous innovation in feature sets and cost-effectiveness, ensures the sustained relevance and expansion of the IP hardware and firmware market globally.

IP Hardware and Firmware Product Landscape

The IP hardware and firmware product landscape is characterized by continuous innovation, focusing on enhanced functionality, seamless integration, and improved performance metrics. IP cameras are evolving beyond mere image capture to incorporate advanced AI-powered analytics for object detection, facial recognition, and behavioral analysis, improving security and operational insights. IP telephony solutions are increasingly converging with unified communication platforms, offering integrated voice, video, messaging, and collaboration tools, driven by advancements in VoIP technology and cloud integration. IP intercom systems are becoming more sophisticated, integrating with broader building management systems and offering features like video verification and remote access control for enhanced security and convenience. The underlying firmware is crucial, with regular updates delivering enhanced cybersecurity, new feature rollouts, and improved operational efficiency, ensuring devices remain state-of-the-art throughout their lifecycle.

Key Drivers, Barriers & Challenges in IP Hardware and Firmware

Key Drivers:

- Technological Advancements: The continuous integration of AI, IoT, and cloud computing into IP hardware and firmware is enhancing functionality, enabling smarter analytics, and facilitating seamless connectivity.

- Growing Security Concerns: Escalating global security threats and the need for advanced surveillance and access control are driving demand for sophisticated IP security solutions.

- Digital Transformation Initiatives: Businesses across all sectors are investing in digital transformation, making IP-based communication and security infrastructure a fundamental requirement.

- Cost-Effectiveness and Scalability: IP solutions offer long-term cost benefits and the flexibility to scale as per evolving business needs, making them attractive investments.

- Remote Work Trends: The rise of remote and hybrid work models necessitates robust IP telephony and collaboration tools for seamless communication.

Barriers & Challenges:

- Cybersecurity Threats: The interconnected nature of IP devices makes them vulnerable to cyberattacks, requiring constant vigilance and investment in robust security protocols and firmware updates.

- High Initial Investment: While cost-effective in the long run, the initial capital outlay for comprehensive IP system deployment can be a barrier for some smaller businesses.

- Integration Complexity: Integrating diverse IP hardware and firmware from different vendors can sometimes present compatibility challenges and require specialized expertise.

- Supply Chain Disruptions: Global supply chain issues, particularly concerning semiconductor components, can impact the availability and pricing of IP hardware.

- Rapid Technological Obsolescence: The fast pace of technological innovation can lead to rapid obsolescence of older hardware, necessitating frequent upgrades and impacting total cost of ownership.

Emerging Opportunities in IP Hardware and Firmware

Emerging opportunities in the IP hardware and firmware market lie in the burgeoning demand for AI-driven intelligent edge computing, where processing power is embedded directly into devices, enabling real-time analytics without constant cloud reliance. The expansion of smart cities and critical infrastructure projects worldwide presents significant growth avenues for integrated IP security and communication solutions. Furthermore, the increasing adoption of IP-based solutions in the healthcare sector for patient monitoring, telehealth, and secure communication systems, alongside the growing trend of IP integration in the automotive industry for advanced driver-assistance systems (ADAS) and in-vehicle infotainment, offers substantial untapped potential. The development of enhanced interoperability standards and open-source firmware initiatives also presents an opportunity for market growth by fostering broader adoption and innovation.

Growth Accelerators in the IP Hardware and Firmware Industry

Several key catalysts are accelerating the growth of the IP hardware and firmware industry. The relentless advancement in AI and machine learning algorithms, enabling more sophisticated video analytics, predictive maintenance, and intelligent automation, is a primary growth accelerator. Strategic partnerships between hardware manufacturers, software developers, and cloud service providers are fostering the creation of comprehensive, integrated solutions that cater to diverse industry needs. Market expansion strategies, particularly targeting emerging economies with rapidly developing IT infrastructures and a growing demand for advanced communication and security, are also driving significant growth. The increasing focus on cybersecurity by governments and enterprises alike is spurring investments in highly secure IP solutions, further bolstering market expansion.

Key Players Shaping the IP Hardware and Firmware Market

- Axis Communications

- Grandstream Networks

- AV Costar

- Gigaset

- Panasonic

- Cisco

- Aastra

- Polycom

- Sangoma

- ProVu Communications

- NetGear

- Bosch Security Systems

- Schneider Electric

- Honeywell

- Vivotek

- Sony

- Avigilon

- Mobotix

- Arecont Vision

- Aiphone

- Barix

- Commend

Notable Milestones in IP Hardware and Firmware Sector

- 2019: Introduction of AI-powered analytics in mainstream IP cameras by multiple vendors, enhancing real-time threat detection and object recognition.

- 2020: Significant surge in demand for IP telephony and collaboration tools due to the global shift to remote work, accelerating cloud-based Unified Communications (UC) adoption.

- 2021: Increased focus on cybersecurity vulnerabilities in IP devices, leading to the release of firmware updates with enhanced encryption and access control protocols.

- 2022: Expansion of edge computing capabilities in IP cameras and other devices, enabling local processing of data for faster response times and reduced bandwidth usage.

- 2023: Growing integration of IP intercom systems with smart home and building management platforms, offering advanced access control and communication features.

- 2024: Rollout of next-generation IP camera sensors with improved low-light performance and higher resolution, catering to demanding surveillance applications.

In-Depth IP Hardware and Firmware Market Outlook

The outlook for the IP hardware and firmware market is exceptionally positive, fueled by ongoing technological innovation and an expanding ecosystem of applications. The convergence of AI, IoT, and advanced connectivity solutions will continue to drive the development of more intelligent, automated, and integrated systems. Strategic partnerships and collaborations are expected to further accelerate product development and market penetration, creating value-added solutions for diverse sectors. As cybersecurity remains a paramount concern, there will be a sustained demand for robust, firmware-enhanced security devices and platforms. The expansion into emerging markets and the continued adoption across traditionally underserved segments, coupled with the inherent scalability and efficiency of IP technology, position the market for robust, long-term growth and significant future potential.

Ip Hardware And Firmware Segmentation

-

1. Application

- 1.1. BFSI

- 1.2. Retail

- 1.3. Healthcare

- 1.4. Government

- 1.5. Industrial

- 1.6. Other

-

2. Type

- 2.1. IP Cameras

- 2.2. IP Telephony

- 2.3. IP Intercoms

- 2.4. Others

Ip Hardware And Firmware Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Ip Hardware And Firmware Regional Market Share

Geographic Coverage of Ip Hardware And Firmware

Ip Hardware And Firmware REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Ip Hardware And Firmware Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. BFSI

- 5.1.2. Retail

- 5.1.3. Healthcare

- 5.1.4. Government

- 5.1.5. Industrial

- 5.1.6. Other

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. IP Cameras

- 5.2.2. IP Telephony

- 5.2.3. IP Intercoms

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Ip Hardware And Firmware Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. BFSI

- 6.1.2. Retail

- 6.1.3. Healthcare

- 6.1.4. Government

- 6.1.5. Industrial

- 6.1.6. Other

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. IP Cameras

- 6.2.2. IP Telephony

- 6.2.3. IP Intercoms

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Ip Hardware And Firmware Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. BFSI

- 7.1.2. Retail

- 7.1.3. Healthcare

- 7.1.4. Government

- 7.1.5. Industrial

- 7.1.6. Other

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. IP Cameras

- 7.2.2. IP Telephony

- 7.2.3. IP Intercoms

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Ip Hardware And Firmware Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. BFSI

- 8.1.2. Retail

- 8.1.3. Healthcare

- 8.1.4. Government

- 8.1.5. Industrial

- 8.1.6. Other

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. IP Cameras

- 8.2.2. IP Telephony

- 8.2.3. IP Intercoms

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Ip Hardware And Firmware Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. BFSI

- 9.1.2. Retail

- 9.1.3. Healthcare

- 9.1.4. Government

- 9.1.5. Industrial

- 9.1.6. Other

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. IP Cameras

- 9.2.2. IP Telephony

- 9.2.3. IP Intercoms

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Ip Hardware And Firmware Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. BFSI

- 10.1.2. Retail

- 10.1.3. Healthcare

- 10.1.4. Government

- 10.1.5. Industrial

- 10.1.6. Other

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. IP Cameras

- 10.2.2. IP Telephony

- 10.2.3. IP Intercoms

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Axis Communications

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Grandstream Networks

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 AV Costar

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Gigaset

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Panasonic

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Cisco

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Aastra

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Polycom

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Sangoma

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 ProVu Communications

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 NetGear

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Bosch Security Systems

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Schneider Electric

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Honeywell

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Vivotek

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Sony

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Avigilon

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Mobotix

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Arecont Vision

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Aiphone

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Barix

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 Commend

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.1 Axis Communications

List of Figures

- Figure 1: Global Ip Hardware And Firmware Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Ip Hardware And Firmware Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Ip Hardware And Firmware Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Ip Hardware And Firmware Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Ip Hardware And Firmware Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Ip Hardware And Firmware Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Ip Hardware And Firmware Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Ip Hardware And Firmware Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Ip Hardware And Firmware Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Ip Hardware And Firmware Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Ip Hardware And Firmware Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Ip Hardware And Firmware Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Ip Hardware And Firmware Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Ip Hardware And Firmware Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Ip Hardware And Firmware Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Ip Hardware And Firmware Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Ip Hardware And Firmware Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Ip Hardware And Firmware Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Ip Hardware And Firmware Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Ip Hardware And Firmware Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Ip Hardware And Firmware Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Ip Hardware And Firmware Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Ip Hardware And Firmware Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Ip Hardware And Firmware Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Ip Hardware And Firmware Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Ip Hardware And Firmware Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Ip Hardware And Firmware Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Ip Hardware And Firmware Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Ip Hardware And Firmware Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Ip Hardware And Firmware Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Ip Hardware And Firmware Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Ip Hardware And Firmware Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Ip Hardware And Firmware Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Ip Hardware And Firmware Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Ip Hardware And Firmware Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Ip Hardware And Firmware Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Ip Hardware And Firmware Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Ip Hardware And Firmware Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Ip Hardware And Firmware Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Ip Hardware And Firmware Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Ip Hardware And Firmware Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Ip Hardware And Firmware Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Ip Hardware And Firmware Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Ip Hardware And Firmware Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Ip Hardware And Firmware Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Ip Hardware And Firmware Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Ip Hardware And Firmware Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Ip Hardware And Firmware Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Ip Hardware And Firmware Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Ip Hardware And Firmware Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Ip Hardware And Firmware Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Ip Hardware And Firmware Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Ip Hardware And Firmware Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Ip Hardware And Firmware Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Ip Hardware And Firmware Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Ip Hardware And Firmware Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Ip Hardware And Firmware Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Ip Hardware And Firmware Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Ip Hardware And Firmware Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Ip Hardware And Firmware Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Ip Hardware And Firmware Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Ip Hardware And Firmware Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Ip Hardware And Firmware Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Ip Hardware And Firmware Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Ip Hardware And Firmware Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Ip Hardware And Firmware Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Ip Hardware And Firmware Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Ip Hardware And Firmware Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Ip Hardware And Firmware Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Ip Hardware And Firmware Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Ip Hardware And Firmware Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Ip Hardware And Firmware Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Ip Hardware And Firmware Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Ip Hardware And Firmware Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Ip Hardware And Firmware Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Ip Hardware And Firmware Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Ip Hardware And Firmware Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Ip Hardware And Firmware?

The projected CAGR is approximately 8.7%.

2. Which companies are prominent players in the Ip Hardware And Firmware?

Key companies in the market include Axis Communications, Grandstream Networks, AV Costar, Gigaset, Panasonic, Cisco, Aastra, Polycom, Sangoma, ProVu Communications, NetGear, Bosch Security Systems, Schneider Electric, Honeywell, Vivotek, Sony, Avigilon, Mobotix, Arecont Vision, Aiphone, Barix, Commend.

3. What are the main segments of the Ip Hardware And Firmware?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Ip Hardware And Firmware," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Ip Hardware And Firmware report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Ip Hardware And Firmware?

To stay informed about further developments, trends, and reports in the Ip Hardware And Firmware, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence