Key Insights

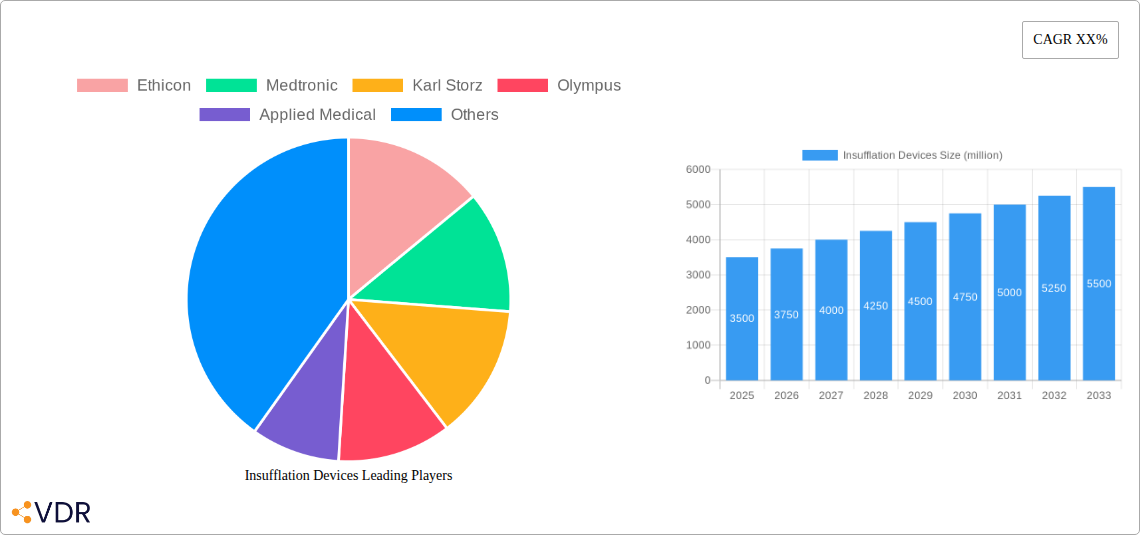

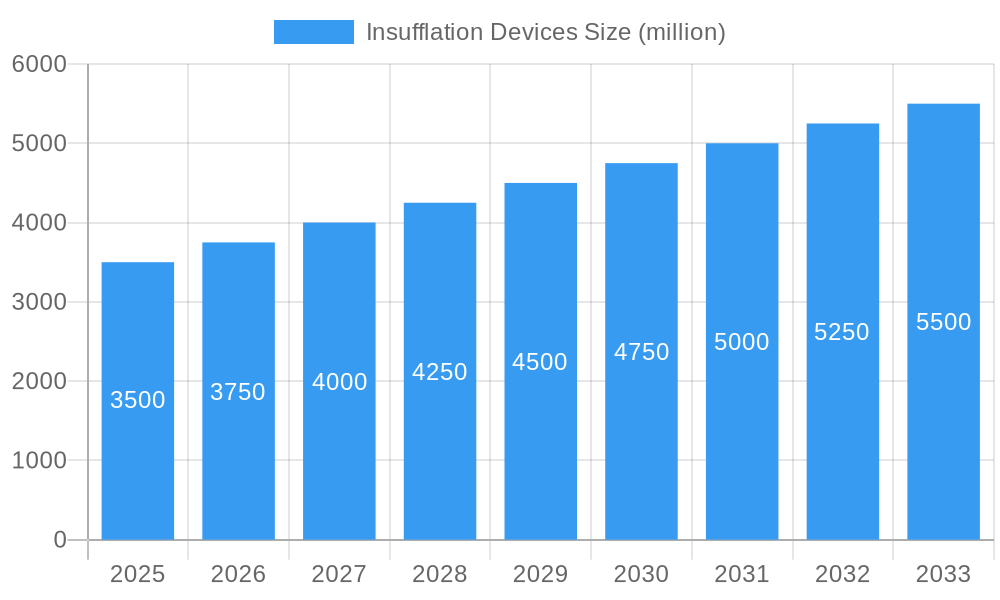

The global insufflation devices market is poised for substantial growth, projected to reach an estimated USD 3,500 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of XX% through 2033. This expansion is primarily fueled by the increasing prevalence of minimally invasive surgeries, a key driver in modern healthcare. As laparoscopic and endoscopic procedures become the standard of care across various surgical specialties, the demand for advanced insufflation systems to create pneumoperitoneum and enhance surgical visualization is surging. Factors such as a growing aging population, leading to a higher incidence of chronic diseases requiring surgical intervention, and the continuous technological advancements in insufflation technology, including smart insufflators with precise CO2 delivery and pressure control, are further propelling market growth. The adoption of these devices is also influenced by their ability to reduce patient recovery times, minimize scarring, and lower the risk of complications compared to traditional open surgeries.

Insufflation Devices Market Size (In Billion)

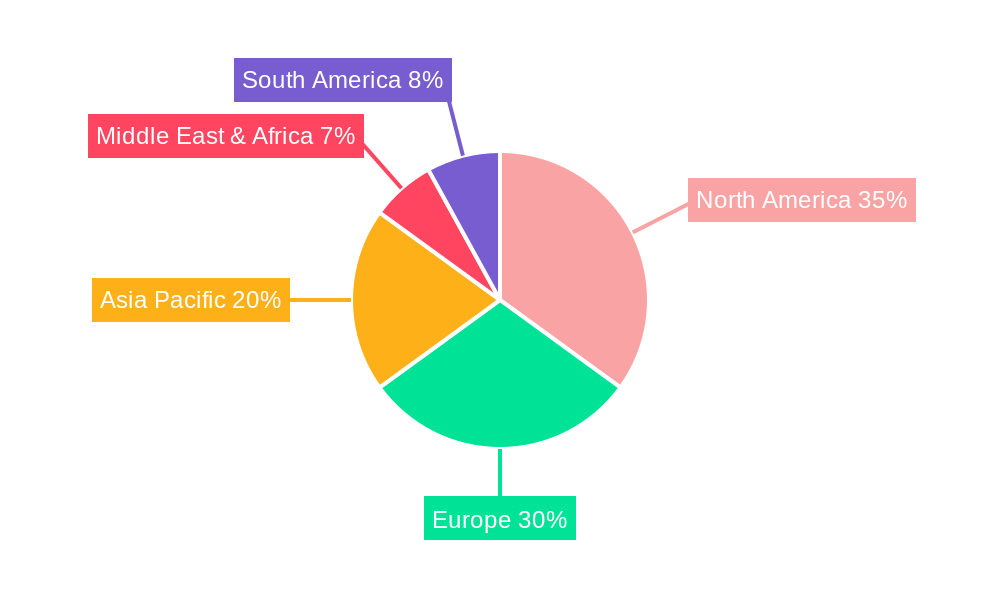

The market segmentation reveals a dynamic landscape, with Disposable Insufflation Devices expected to witness higher adoption rates due to their inherent benefits of infection control and convenience, particularly in high-volume surgical settings. Conversely, Reusable Insufflation Devices will continue to hold a significant share, driven by cost-effectiveness in the long run and technological improvements enhancing their efficacy and safety. Geographically, North America and Europe are expected to dominate the market, owing to well-established healthcare infrastructures, high disposable incomes, and a proactive approach to adopting advanced surgical technologies. The Asia Pacific region, however, is anticipated to exhibit the fastest growth, driven by a burgeoning healthcare sector, increasing surgical volumes, and a growing awareness of minimally invasive techniques. Key players such as Ethicon, Medtronic, and Karl Storz are actively investing in research and development to innovate and expand their product portfolios, further shaping the competitive dynamics of this vital market.

Insufflation Devices Company Market Share

Insufflation Devices Market: Comprehensive Industry Report (2019-2033)

This comprehensive report offers an in-depth analysis of the global insufflation devices market, encompassing market dynamics, growth trends, regional dominance, product landscape, key drivers, challenges, opportunities, and a detailed outlook for the period 2019–2033, with a base year of 2025. The report is meticulously structured to provide actionable insights for industry professionals, investors, and stakeholders.

Insufflation Devices Market Dynamics & Structure

The global insufflation devices market exhibits a moderately consolidated structure, with leading players like Ethicon, Medtronic, and Karl Storz holding significant market shares. Technological innovation serves as a primary driver, with continuous advancements in disposable insufflation devices enhancing patient safety and procedural efficiency. Regulatory frameworks, particularly those governing medical devices, play a crucial role in market access and product development. Competitive product substitutes, primarily the shift towards minimally invasive surgery techniques that reduce the need for extensive insufflation, present a constant challenge. End-user demographics are evolving, with an increasing demand for sophisticated, user-friendly devices in both hospital and clinic settings. Mergers and acquisitions (M&A) trends indicate strategic consolidation and expansion of product portfolios. For instance, the acquisition of smaller innovative companies by larger corporations aims to bolster their offerings in advanced insufflation technologies. The market is projected to reach approximately $2,500 million in 2025, with an estimated CAGR of 6.5% over the forecast period.

- Market Concentration: Moderately consolidated with a few key players dominating.

- Technological Innovation Drivers: Miniaturization, enhanced CO2 delivery control, and integration with advanced imaging systems.

- Regulatory Frameworks: Stringent FDA and EMA approvals are critical for market entry and product longevity.

- Competitive Product Substitutes: Development of novel surgical techniques and energy-based devices that minimize insufflation requirements.

- End-User Demographics: Growing preference for single-use devices in hospitals and the increasing adoption of laparoscopic procedures in outpatient clinics.

- M&A Trends: Strategic acquisitions to gain access to innovative technologies and expand geographic reach, with an estimated 5-7 significant M&A deals annually.

Insufflation Devices Growth Trends & Insights

The global insufflation devices market is poised for robust growth, driven by the increasing prevalence of minimally invasive surgeries (MIS) across various medical specialties, including general surgery, gynecology, urology, and cardiology. The adoption of laparoscopic and robotic-assisted procedures, which rely heavily on effective CO2 insufflation for optimal visualization and maneuverability, is a significant catalyst. The market size is projected to expand from approximately $2,200 million in 2019 to an estimated $4,500 million by 2033. This growth is underpinned by rising healthcare expenditure globally, a growing aging population prone to conditions requiring surgical intervention, and an increasing awareness among healthcare providers about the benefits of MIS, such as reduced patient recovery times and lower complication rates.

Disposable insufflation devices are experiencing particularly rapid adoption due to concerns regarding infection control and the convenience they offer, driving their market penetration to an estimated 70% of the total market by 2033. Technological disruptions are also playing a pivotal role, with manufacturers introducing insufflators with advanced features like automatic pressure regulation, leak detection, and integration with surgical navigation systems. For instance, the development of "intelligent" insufflators that adapt to varying surgical needs and patient physiologies is transforming surgical workflows. Consumer behavior shifts are evident in the growing demand for cost-effective and reliable insufflation solutions, pushing manufacturers to innovate in both performance and affordability. The market penetration of advanced insufflation systems is expected to reach 75% in developed economies by 2033. The compound annual growth rate (CAGR) for the period 2025-2033 is estimated at 6.5%.

Dominant Regions, Countries, or Segments in Insufflation Devices

North America currently dominates the global insufflation devices market, driven by a highly developed healthcare infrastructure, significant investment in medical technology, and the high prevalence of minimally invasive surgeries. The United States, in particular, is a key contributor, with its advanced hospital systems and widespread adoption of innovative surgical techniques. Economic policies that support medical device innovation and reimbursement structures that favor minimally invasive procedures further bolster this dominance. The region is estimated to hold a market share of approximately 38% in 2025.

In terms of application, hospitals are the largest segment, accounting for an estimated 85% of the market share in 2025. This is attributed to the higher volume of complex surgical procedures performed in hospital settings, necessitating advanced insufflation capabilities. Clinics, particularly ambulatory surgical centers, are witnessing a steady rise in adoption due to the increasing trend of outpatient surgeries.

The "Disposable Insufflation Devices" segment is experiencing the most dynamic growth and is projected to capture a significant market share, estimated at 70% by 2033. This is propelled by stringent infection control protocols, convenience for surgical teams, and the increasing preference for single-use medical supplies. Reusable insufflation devices, while still important, face challenges related to sterilization costs and potential for cross-contamination. Infrastructure development, including the expansion of surgical facilities and the integration of advanced operating room technologies, also plays a crucial role in regional market dominance. Growth potential in emerging economies, particularly in Asia-Pacific, is substantial due to increasing healthcare access and a growing middle class, indicating future shifts in regional market leadership.

Insufflation Devices Product Landscape

The insufflation devices product landscape is characterized by a steady stream of innovations focused on enhancing precision, safety, and ease of use. Manufacturers are prioritizing the development of intelligent insufflators with features such as advanced CO2 leak detection systems, real-time pressure and flow monitoring, and integrated patient data management capabilities. Disposable insufflation sets are gaining traction due to their convenience and reduced risk of cross-contamination. Companies like Ethicon and Medtronic are at the forefront of developing next-generation insufflation systems that integrate seamlessly with robotic surgical platforms, offering unparalleled control and visualization during complex procedures. Applications span across laparoscopic, endoscopic, and robotic surgeries, with key performance metrics revolving around accurate gas delivery, patient comfort, and procedural efficiency.

Key Drivers, Barriers & Challenges in Insufflation Devices

Key Drivers:

- Rising prevalence of minimally invasive surgeries (MIS): Drives demand for effective insufflation for visualization and access.

- Technological advancements: Development of smarter, more precise, and user-friendly insufflation devices.

- Growing aging population: Increased incidence of diseases requiring surgical intervention.

- Government initiatives and R&D funding: Support for medical device innovation and healthcare infrastructure development.

Barriers & Challenges:

- High cost of advanced insufflation systems: Can limit adoption in resource-constrained settings.

- Stringent regulatory approvals: The lengthy and complex process can delay product launches.

- Availability of counterfeit products: Poses risks to patient safety and erodes market trust.

- Competition from alternative surgical approaches: Development of techniques that minimize or eliminate the need for insufflation.

- Supply chain disruptions: Global events can impact the availability of critical components. Estimated impact of supply chain issues could lead to a 5-10% delay in product availability.

Emerging Opportunities in Insufflation Devices

Emerging opportunities lie in the development of portable and wireless insufflation devices for remote or field surgical applications. The integration of artificial intelligence (AI) for predictive analytics of insufflation needs and potential complications presents a significant avenue for innovation. Furthermore, the untapped potential in emerging economies with rapidly expanding healthcare sectors offers substantial growth prospects. A focus on cost-effective, high-performance insufflation solutions tailored for developing markets can unlock new revenue streams. The increasing demand for patient-centric solutions also presents opportunities for devices that minimize patient discomfort and optimize recovery.

Growth Accelerators in the Insufflation Devices Industry

Key growth accelerators include the ongoing expansion of robotic-assisted surgery, which inherently relies on advanced insufflation technologies for optimal performance. Strategic partnerships between insufflation device manufacturers and robotic surgery platform developers are crucial for synergistic growth. Market expansion into underdeveloped regions with growing healthcare infrastructure represents another significant accelerator. Furthermore, continuous product innovation, focusing on enhancing safety features, improving workflow integration, and reducing procedure times, will fuel long-term market expansion. Investment in clinical trials to demonstrate the superior outcomes of MIS facilitated by advanced insufflation will also act as a significant growth stimulant.

Key Players Shaping the Insufflation Devices Market

- Ethicon

- Medtronic

- Karl Storz

- Olympus

- Applied Medical

- Richard Wolf

- Bayer AG

- Stryker

- B. Braun Aesculap

- ERBE

- LiNA Medical

- ConMed

- Microline Surgical

- Apollo Endosurgery

Notable Milestones in Insufflation Devices Sector

- 2019: Introduction of AI-powered CO2 insufflators for enhanced surgical feedback.

- 2020: Increased demand for disposable insufflation devices due to global pandemic concerns regarding infection control.

- 2021: Significant investment in R&D for next-generation insufflators by leading players.

- 2022: Strategic acquisitions by larger companies to expand product portfolios in advanced insufflation technologies.

- 2023: Development of wireless insufflation systems for enhanced OR flexibility.

- 2024: Launch of integrated insufflation and smoke evacuation systems for improved surgical safety.

In-Depth Insufflation Devices Market Outlook

The future of the insufflation devices market is exceptionally promising, driven by the undeniable shift towards minimally invasive surgical techniques. Future growth accelerators will be deeply rooted in the relentless pursuit of technological innovation, such as the development of smart insufflators with predictive capabilities and ultra-precise gas control. Strategic collaborations between insufflation device manufacturers and pioneers in robotic surgery will be paramount, fostering an ecosystem of integrated surgical solutions. Expanding market penetration into underserved geographies, coupled with the introduction of affordable yet high-quality devices, will unlock substantial potential. Continued focus on clinical validation and demonstrating the benefits of advanced insufflation in improving patient outcomes will further solidify market expansion and strategic opportunities for all stakeholders.

Insufflation Devices Segmentation

-

1. Application

- 1.1. Hospital

- 1.2. Clinic

-

2. Types

- 2.1. Disposable Insufflation Devices

- 2.2. Reusable Insufflation Devices

Insufflation Devices Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Insufflation Devices Regional Market Share

Geographic Coverage of Insufflation Devices

Insufflation Devices REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospital

- 5.1.2. Clinic

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Disposable Insufflation Devices

- 5.2.2. Reusable Insufflation Devices

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Insufflation Devices Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospital

- 6.1.2. Clinic

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Disposable Insufflation Devices

- 6.2.2. Reusable Insufflation Devices

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Insufflation Devices Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospital

- 7.1.2. Clinic

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Disposable Insufflation Devices

- 7.2.2. Reusable Insufflation Devices

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Insufflation Devices Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospital

- 8.1.2. Clinic

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Disposable Insufflation Devices

- 8.2.2. Reusable Insufflation Devices

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Insufflation Devices Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospital

- 9.1.2. Clinic

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Disposable Insufflation Devices

- 9.2.2. Reusable Insufflation Devices

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Insufflation Devices Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospital

- 10.1.2. Clinic

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Disposable Insufflation Devices

- 10.2.2. Reusable Insufflation Devices

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Insufflation Devices Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Hospital

- 11.1.2. Clinic

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Disposable Insufflation Devices

- 11.2.2. Reusable Insufflation Devices

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Ethicon

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Medtronic

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Karl Storz

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Olympus

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Applied Medical

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Richard Wolf

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Bayer AG

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Stryker

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 B. Braun Aesculap

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 ERBE

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 LiNA Medical

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 ConMed

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Microline Surgical

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Apollo Endosurgery

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 Ethicon

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Insufflation Devices Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Insufflation Devices Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Insufflation Devices Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Insufflation Devices Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Insufflation Devices Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Insufflation Devices Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Insufflation Devices Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Insufflation Devices Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Insufflation Devices Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Insufflation Devices Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Insufflation Devices Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Insufflation Devices Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Insufflation Devices Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Insufflation Devices Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Insufflation Devices Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Insufflation Devices Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Insufflation Devices Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Insufflation Devices Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Insufflation Devices Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Insufflation Devices Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Insufflation Devices Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Insufflation Devices Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Insufflation Devices Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Insufflation Devices Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Insufflation Devices Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Insufflation Devices Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Insufflation Devices Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Insufflation Devices Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Insufflation Devices Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Insufflation Devices Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Insufflation Devices Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Insufflation Devices Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Insufflation Devices Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Insufflation Devices Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Insufflation Devices Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Insufflation Devices Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Insufflation Devices Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Insufflation Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Insufflation Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Insufflation Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Insufflation Devices Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Insufflation Devices Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Insufflation Devices Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Insufflation Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Insufflation Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Insufflation Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Insufflation Devices Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Insufflation Devices Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Insufflation Devices Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Insufflation Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Insufflation Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Insufflation Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Insufflation Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Insufflation Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Insufflation Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Insufflation Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Insufflation Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Insufflation Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Insufflation Devices Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Insufflation Devices Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Insufflation Devices Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Insufflation Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Insufflation Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Insufflation Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Insufflation Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Insufflation Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Insufflation Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Insufflation Devices Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Insufflation Devices Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Insufflation Devices Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Insufflation Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Insufflation Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Insufflation Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Insufflation Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Insufflation Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Insufflation Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Insufflation Devices Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Insufflation Devices?

The projected CAGR is approximately 6.4%.

2. Which companies are prominent players in the Insufflation Devices?

Key companies in the market include Ethicon, Medtronic, Karl Storz, Olympus, Applied Medical, Richard Wolf, Bayer AG, Stryker, B. Braun Aesculap, ERBE, LiNA Medical, ConMed, Microline Surgical, Apollo Endosurgery.

3. What are the main segments of the Insufflation Devices?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.76 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Insufflation Devices," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Insufflation Devices report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Insufflation Devices?

To stay informed about further developments, trends, and reports in the Insufflation Devices, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence