Key Insights

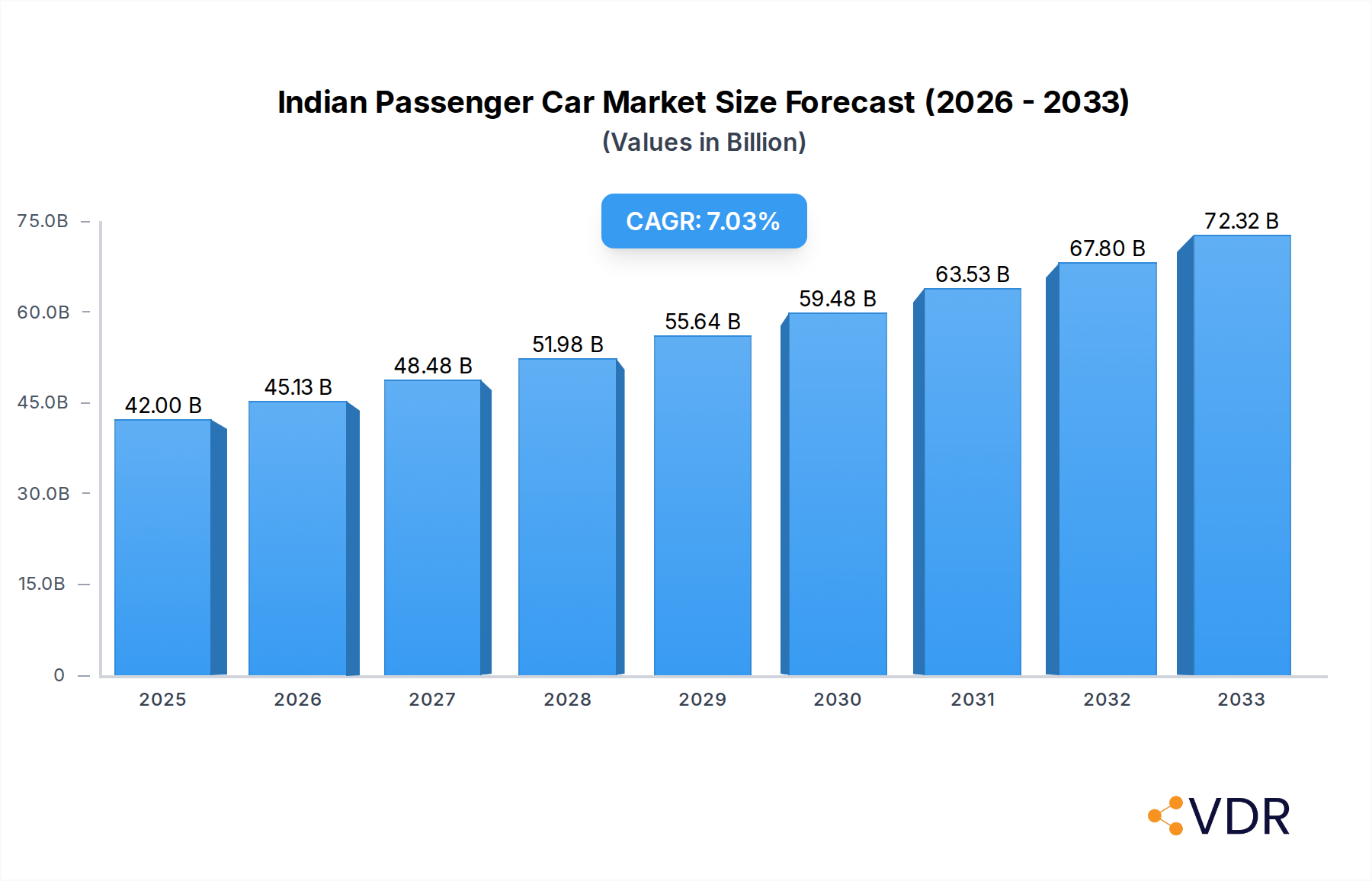

The Indian passenger car market is poised for substantial growth, with a projected market size of USD 42 billion in 2025, expanding at a robust Compound Annual Growth Rate (CAGR) of 7.51% through 2033. This upward trajectory is primarily fueled by a confluence of evolving consumer preferences, increasing disposable incomes, and a growing appetite for technologically advanced vehicles. The "Make in India" initiative and government incentives supporting automotive manufacturing further bolster domestic production and market expansion. Key drivers include a burgeoning young population, a growing middle class with enhanced purchasing power, and a demand for diverse vehicle configurations such as Sports Utility Vehicles (SUVs) and Multi-purpose Vehicles (MPVs) that cater to family needs and urban lifestyles. Furthermore, the increasing awareness and adoption of sustainable mobility solutions are significantly influencing the market, with Hybrid and Electric Vehicles (HEVs, PHEVs, BEVs, FCEVs) gaining considerable traction. The government's push towards electrifying transport and reducing emissions is accelerating the development and sales of these eco-friendly alternatives, marking a significant shift in the propulsion type landscape.

Indian Passenger Car Market Market Size (In Billion)

While the market demonstrates strong growth potential, certain restraints could temper the pace. These include fluctuating raw material costs, potential infrastructure challenges related to charging networks for electric vehicles, and the impact of economic slowdowns or policy shifts. However, the inherent resilience of the Indian automotive sector, coupled with aggressive expansion strategies by major players like Maruti Suzuki, Tata Motors, Hyundai, and Mahindra & Mahindra, is expected to mitigate these challenges. The competitive landscape is characterized by intense innovation, with companies focusing on introducing feature-rich models across various price points and segments. The increasing penetration of advanced technologies, including connected car features and enhanced safety systems, is also a critical trend attracting a wider consumer base. Regional distribution highlights India as the primary market, with a focus on expanding reach in Tier 2 and Tier 3 cities, indicating a broad-based demand across the nation.

Indian Passenger Car Market Company Market Share

This in-depth report provides an exhaustive analysis of the Indian Passenger Car Market, a critical segment of the automotive industry experiencing dynamic evolution. Covering the historical period from 2019 to 2024, with a base and estimated year of 2025, and projecting growth through 2033, this study leverages proprietary data and expert insights to deliver actionable intelligence. We meticulously examine market structure, growth trajectories, regional dominance, product innovation, key players, and emerging opportunities. This report is essential for automotive manufacturers, suppliers, investors, policymakers, and industry analysts seeking to understand and capitalize on the burgeoning Indian passenger car landscape.

Indian Passenger Car Market Dynamics & Structure

The Indian passenger car market is characterized by a highly competitive landscape with a few dominant players holding significant market share, interspersed with emerging manufacturers vying for consumer attention. Technological innovation is a primary driver, fueled by the increasing demand for advanced features, safety, and sustainable mobility solutions. Regulatory frameworks, particularly those aimed at emission reduction and promoting electric vehicles (EVs), are profoundly shaping product development and market entry strategies. Competitive product substitutes, ranging from ride-sharing services to alternative transportation modes, also influence consumer choices, though personal vehicle ownership remains a strong aspiration. End-user demographics are shifting, with a growing young, urban population demanding connected car technology and fuel-efficient options. Mergers and acquisitions (M&A) trends are evident, as companies seek to consolidate market positions, acquire technological capabilities, and expand their product portfolios to cater to diverse consumer needs.

- Market Concentration: Dominated by Maruti Suzuki India Limited and Hyundai Motor India Limited, with other key players like Tata Motors, Mahindra & Mahindra, and Kia Corporation steadily increasing their presence.

- Technological Innovation: Focus on advanced driver-assistance systems (ADAS), connected car technologies, and cleaner propulsion systems.

- Regulatory Influence: Government initiatives like FAME (Faster Adoption and Manufacturing of Hybrid and Electric Vehicles) and PLI (Production Linked Incentive) schemes are incentivizing EV adoption and local manufacturing.

- Competitive Product Substitutes: Rise of ride-hailing platforms and increasing public transportation investments present indirect competition for car ownership.

- End-User Demographics: Growing disposable incomes, urbanization, and a young demographic with a preference for SUVs and feature-rich vehicles.

- M&A Trends: Strategic alliances and acquisitions aimed at expanding product portfolios and strengthening market share, particularly in the EV space.

Indian Passenger Car Market Growth Trends & Insights

The Indian Passenger Car Market is poised for significant expansion, driven by a confluence of economic prosperity, evolving consumer preferences, and supportive government policies. The market size is projected to witness a robust Compound Annual Growth Rate (CAGR) of approximately xx% from the base year of 2025 through 2033, reaching an estimated value of $XXX billion units by the end of the forecast period. Historical data from 2019-2024 indicates a resilient recovery and steady growth, underscoring the market's inherent strength. Adoption rates for new technologies, especially in the electric and hybrid vehicle segments, are accelerating, moving from early adopters to the mainstream market. This shift is propelled by increased model availability, improved charging infrastructure, and growing environmental awareness among consumers. Technological disruptions, such as advancements in battery technology, autonomous driving features, and in-car infotainment systems, are redefining the automotive experience and driving consumer demand for newer, more advanced models. Consumer behavior is also undergoing a transformation; buyers are increasingly influenced by factors beyond mere price, including vehicle safety, fuel efficiency, brand reputation, and the overall digital experience offered by a car. The demand for Sport Utility Vehicles (SUVs) continues to dominate, reflecting a preference for versatility, higher ground clearance, and a commanding road presence. Furthermore, the growing preference for connected car features and personalized in-car experiences is shaping the development roadmap for manufacturers. The burgeoning middle class, coupled with a young demographic eager to embrace modern technologies, forms a powerful consumer base, fueling the sustained growth of the Indian passenger car sector.

Dominant Regions, Countries, or Segments in Indian Passenger Car Market

Within the Indian Passenger Car Market, the Sports Utility Vehicle (SUV) segment, a crucial sub-segment of Passenger Cars, is unequivocally dominating market growth. This ascendancy is propelled by a confluence of socio-economic factors and evolving consumer aspirations across key urban and semi-urban regions. The SUV’s versatility, offering higher ground clearance suitable for varied Indian road conditions, spacious interiors, and a commanding road presence, perfectly aligns with the preferences of a burgeoning middle class seeking both practicality and a sense of prestige. This preference is particularly pronounced in economically vibrant states like Maharashtra, Gujarat, and Tamil Nadu, which exhibit high per capita incomes and a strong manufacturing base, translating into greater purchasing power for passenger vehicles.

Dominant Segment (Vehicle Configuration): Sports Utility Vehicle (SUV)

- Key Drivers: Higher ground clearance for diverse road conditions, spacious interiors, commanding road presence, and a perception of safety and robustness.

- Market Share: SUVs currently command over xx% of the passenger car market share, a figure projected to grow further.

- Growth Potential: High, driven by continuous new model launches and increasing consumer preference.

Dominant Propulsion Type: Internal Combustion Engine (ICE) - Gasoline

- Key Drivers: Extensive refueling infrastructure, lower upfront cost compared to EVs, and a wide range of affordable and feature-rich models.

- Market Share: Gasoline-powered vehicles continue to hold the largest share, estimated at over xx% of the market.

- Growth Potential: Steady growth, especially in entry-level and mid-segment cars, though facing increasing competition from hybrids and EVs.

Emerging Propulsion Type: Hybrid and Electric Vehicles (HEVs and BEVs)

- Key Drivers: Government incentives (FAME II, PLI schemes), growing environmental consciousness, falling battery costs, and increasing model availability from major manufacturers.

- Market Share: While currently smaller, the share of BEVs and HEVs is experiencing rapid growth, projected to reach xx% by 2033.

- Growth Potential: Exponential growth anticipated, driven by technological advancements and policy support.

Leading Regions: Western India (Maharashtra, Gujarat) and Southern India (Tamil Nadu, Karnataka)

- Key Drivers: Strong economic growth, high urbanization rates, significant disposable incomes, established automotive manufacturing hubs, and a greater propensity to adopt new technologies.

- Market Share: These regions collectively contribute over xx% of the total passenger car sales in India.

- Growth Potential: Sustained high growth due to continued economic development and a large, aspirational consumer base.

Indian Passenger Car Market Product Landscape

The product landscape within the Indian Passenger Car Market is rapidly evolving, showcasing significant innovations aimed at meeting diverse consumer demands and stricter regulatory requirements. Manufacturers are focusing on enhancing fuel efficiency through advanced engine technologies and lightweight materials. The integration of sophisticated infotainment systems, connected car features, and advanced driver-assistance systems (ADAS) is becoming standard, even in lower segments. There is a notable trend towards offering a wider array of vehicle configurations, with a particular emphasis on the ever-popular SUV segment, catering to families and individuals seeking utility and style. The propulsion type landscape is also dynamic, with a strong push towards greener alternatives.

- Key Innovations: Advanced driver-assistance systems (ADAS), in-car connectivity platforms, over-the-air (OTA) software updates, and advanced safety features.

- Performance Metrics: Increased focus on fuel economy (km/liter), reduced emissions (grams of CO2 per km), and improved acceleration.

- Unique Selling Propositions: Manufacturers are differentiating through distinctive design elements, extensive feature lists at competitive price points, and robust after-sales service networks.

- Technological Advancements: Adoption of modular platforms, electrification technologies (hybrid, plug-in hybrid, battery electric), and sophisticated powertrain management systems.

Key Drivers, Barriers & Challenges in Indian Passenger Car Market

The Indian Passenger Car Market is propelled by several key drivers, including the growing disposable income of the Indian populace, leading to increased affordability and aspirational buying. Government initiatives promoting manufacturing and adoption of electric vehicles (EVs) and stricter emission norms are also significant catalysts. Technological advancements offering enhanced safety, comfort, and connectivity further stimulate demand. The expansion of the dealer and service network, especially in Tier 2 and Tier 3 cities, is also making car ownership more accessible.

Conversely, several barriers and challenges temper market growth. Infrastructure limitations, particularly the availability of EV charging stations and the quality of road networks in some areas, pose significant hurdles. High taxation on automobiles and rising fuel prices can impact consumer purchasing power. Supply chain disruptions, as witnessed globally, can affect production and vehicle availability. Intense competition among established and new players can lead to price wars and reduced profit margins.

Emerging Opportunities in Indian Passenger Car Market

Emerging opportunities within the Indian Passenger Car Market are abundant, primarily driven by the rapid urbanization and the expanding middle class, creating a vast pool of first-time car buyers. The growing demand for electric vehicles (EVs) presents a significant opportunity for manufacturers to introduce innovative and affordable EV models, supported by government incentives and a developing charging infrastructure. The increasing preference for connected car technologies and advanced digital features opens avenues for software-driven services and personalized user experiences. Furthermore, the untapped potential in semi-urban and rural markets offers substantial growth prospects as economic development spreads to these regions.

Growth Accelerators in the Indian Passenger Car Market Industry

Several catalysts are accelerating the growth of the Indian Passenger Car Market. The Production Linked Incentive (PLI) schemes for the automotive sector are encouraging domestic manufacturing and technological innovation, particularly in the EV domain. Strategic partnerships and joint ventures between Indian and global automakers are facilitating the introduction of advanced technologies and a wider product range. The continuous expansion of financial lending facilities for vehicle purchases is making car ownership more accessible to a broader segment of the population. Moreover, the increasing focus on exports and global competitiveness is pushing manufacturers to enhance product quality and adopt international standards, indirectly benefiting the domestic market.

Key Players Shaping the Indian Passenger Car Market Market

- Toyota Kirloskar Motor Pvt Ltd

- MG Motor India Private Limited

- Volkswagen AG

- Tata Motors Limited

- Kia Corporation

- Honda Cars India Limited

- Renault India Pvt Ltd

- Mahindra & Mahindra Limited

- Maruti Suzuki India Limited

- Škoda Auto Volkswagen India Pvt Ltd

- Hyundai Motor India Limited

- Nissan Motor India Pvt Ltd

Notable Milestones in Indian Passenger Car Market Sector

- August 2023: Gabriel India Limited (Gabriel India), a flagship company of Anand Group, announced that during the quarter that ended on June 30, 2023, it has developed components for Maruti Suzuki Jimny and Stellantis electric Citroen C3. At present it is developing parts for new models of VW, Tata, Stellantis, Mahindra, and Maruti Suzuki.

- August 2023: Hyundai Motor India Limited (HMIL) signed an asset purchase agreement (APA), in Gurugram, Haryana, for the acquisition and assignment of identified assets related to General Motors India (GMI)’s Talegaon Plant in Maharashtra.

- August 2023: Mahindra Electric Automobiles Limited (MEAL), a subsidiary of Mahindra & Mahindra, unveiled the “Vision Thar.e”, an electric avatar of the Thar SUV, at its Futurescape event in Cape Town, South Africa. The Thar.e boldly strides into the future on the INGLO-born electric platform, equipped with a cutting-edge high-performance AWD electric powertrain.

In-Depth Indian Passenger Car Market Market Outlook

The Indian Passenger Car Market outlook is exceptionally bright, characterized by sustained growth driven by robust economic fundamentals, a young and aspirational demographic, and a supportive policy environment. The market is set to be a significant global player, with a strong emphasis on electrification and digitalization. Manufacturers are expected to continue investing in local R&D and production capabilities, leading to more India-specific product offerings. The shift towards sustainable mobility solutions will accelerate, presenting immense opportunities for EV manufacturers and component suppliers. Strategic partnerships and technological collaborations will be crucial for navigating the evolving market dynamics and capitalizing on emerging consumer preferences. The overall trajectory indicates a dynamic and rapidly expanding market, offering substantial potential for innovation and investment.

Indian Passenger Car Market Segmentation

-

1. Vehicle Configuration

-

1.1. Passenger Cars

- 1.1.1. Hatchback

- 1.1.2. Multi-purpose Vehicle

- 1.1.3. Sedan

- 1.1.4. Sports Utility Vehicle

-

1.1. Passenger Cars

-

2. Propulsion Type

-

2.1. Hybrid and Electric Vehicles

-

2.1.1. By Fuel Category

- 2.1.1.1. BEV

- 2.1.1.2. FCEV

- 2.1.1.3. HEV

- 2.1.1.4. PHEV

-

2.1.1. By Fuel Category

-

2.2. ICE

- 2.2.1. CNG

- 2.2.2. Diesel

- 2.2.3. Gasoline

- 2.2.4. LPG

-

2.1. Hybrid and Electric Vehicles

Indian Passenger Car Market Segmentation By Geography

- 1. India

Indian Passenger Car Market Regional Market Share

Geographic Coverage of Indian Passenger Car Market

Indian Passenger Car Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.51% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Configuration

- 5.1.1. Passenger Cars

- 5.1.1.1. Hatchback

- 5.1.1.2. Multi-purpose Vehicle

- 5.1.1.3. Sedan

- 5.1.1.4. Sports Utility Vehicle

- 5.1.1. Passenger Cars

- 5.2. Market Analysis, Insights and Forecast - by Propulsion Type

- 5.2.1. Hybrid and Electric Vehicles

- 5.2.1.1. By Fuel Category

- 5.2.1.1.1. BEV

- 5.2.1.1.2. FCEV

- 5.2.1.1.3. HEV

- 5.2.1.1.4. PHEV

- 5.2.1.1. By Fuel Category

- 5.2.2. ICE

- 5.2.2.1. CNG

- 5.2.2.2. Diesel

- 5.2.2.3. Gasoline

- 5.2.2.4. LPG

- 5.2.1. Hybrid and Electric Vehicles

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. India

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Configuration

- 6. Indian Passenger Car Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Configuration

- 6.1.1. Passenger Cars

- 6.1.1.1. Hatchback

- 6.1.1.2. Multi-purpose Vehicle

- 6.1.1.3. Sedan

- 6.1.1.4. Sports Utility Vehicle

- 6.1.1. Passenger Cars

- 6.2. Market Analysis, Insights and Forecast - by Propulsion Type

- 6.2.1. Hybrid and Electric Vehicles

- 6.2.1.1. By Fuel Category

- 6.2.1.1.1. BEV

- 6.2.1.1.2. FCEV

- 6.2.1.1.3. HEV

- 6.2.1.1.4. PHEV

- 6.2.1.1. By Fuel Category

- 6.2.2. ICE

- 6.2.2.1. CNG

- 6.2.2.2. Diesel

- 6.2.2.3. Gasoline

- 6.2.2.4. LPG

- 6.2.1. Hybrid and Electric Vehicles

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Configuration

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Toyota Kirloskar Motor Pvt Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 MG Motor India Private Limited

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Volkswagen AG

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Tata Motors Limited

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Kia Corporation

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Honda Cars India Limited

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Renault India Pvt Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Mahindra & Mahindra Limited

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Maruti Suzuki India Limited

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Škoda Auto Volkswagen India Pvt Ltd

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Hyundai Motor India Limited

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Nissan Motor India Pvt Ltd

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 Toyota Kirloskar Motor Pvt Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Indian Passenger Car Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Indian Passenger Car Market Share (%) by Company 2025

List of Tables

- Table 1: Indian Passenger Car Market Revenue billion Forecast, by Vehicle Configuration 2020 & 2033

- Table 2: Indian Passenger Car Market Revenue billion Forecast, by Propulsion Type 2020 & 2033

- Table 3: Indian Passenger Car Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Indian Passenger Car Market Revenue billion Forecast, by Vehicle Configuration 2020 & 2033

- Table 5: Indian Passenger Car Market Revenue billion Forecast, by Propulsion Type 2020 & 2033

- Table 6: Indian Passenger Car Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Indian Passenger Car Market?

The projected CAGR is approximately 7.51%.

2. Which companies are prominent players in the Indian Passenger Car Market?

Key companies in the market include Toyota Kirloskar Motor Pvt Ltd, MG Motor India Private Limited, Volkswagen AG, Tata Motors Limited, Kia Corporation, Honda Cars India Limited, Renault India Pvt Ltd, Mahindra & Mahindra Limited, Maruti Suzuki India Limited, Škoda Auto Volkswagen India Pvt Ltd, Hyundai Motor India Limited, Nissan Motor India Pvt Ltd.

3. What are the main segments of the Indian Passenger Car Market?

The market segments include Vehicle Configuration, Propulsion Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 42 billion as of 2022.

5. What are some drivers contributing to market growth?

Used Car Financing To Continue Solving Consumer Challenges In Indonesia.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Trust And Transparency In Used Car Remained A Key Challenge For Consumers.

8. Can you provide examples of recent developments in the market?

August 2023: Gabriel India Limited (Gabriel India), a flagship company of Anand Group, announced that during the quarter that ended on June 30, 2023, it has developed components for Maruti Suzuki Jimny and Stellantis electric Citroen C3. At present it is developing parts for new models of VW, Tata, Stellantis, Mahindra, and Maruti Suzuki.August 2023: Hyundai Motor India Limited (HMIL) signed an asset purchase agreement (APA), in Gurugram, Haryana, for the acquisition and assignment of identified assets related to General Motors India (GMI)’s Talegaon Plant in Maharashtra.August 2023: Mahindra Electric Automobiles Limited (MEAL), a subsidiary of Mahindra & Mahindra, unveiled the “Vision Thar.e”, an electric avatar of the Thar SUV, at its Futurescape event in Cape Town, South Africa. The Thar.e boldly strides into the future on the INGLO-born electric platform, equipped with a cutting-edge high-performance AWD electric powertrain.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Indian Passenger Car Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Indian Passenger Car Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Indian Passenger Car Market?

To stay informed about further developments, trends, and reports in the Indian Passenger Car Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence