Key Insights

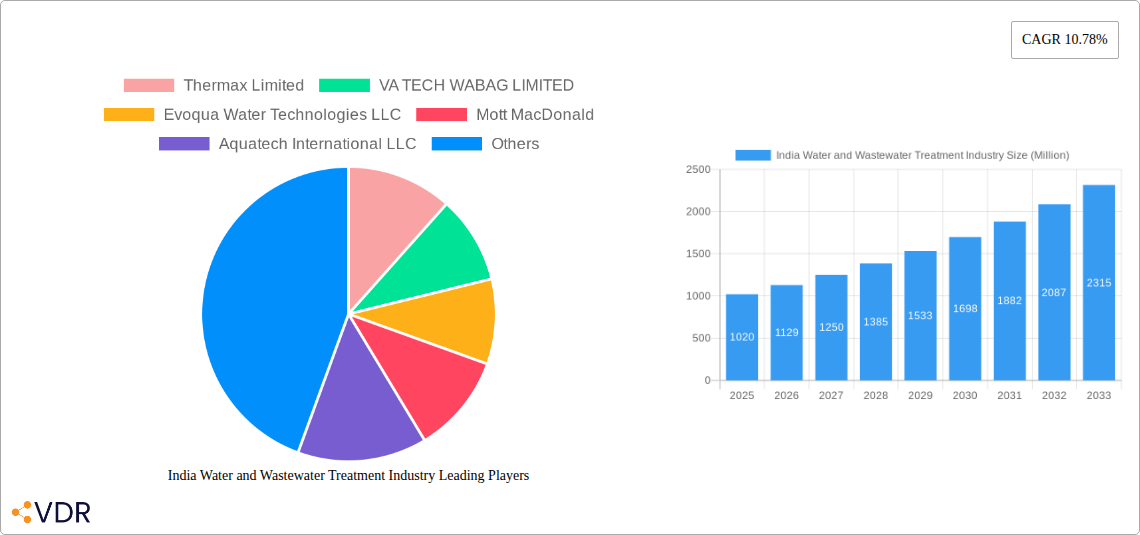

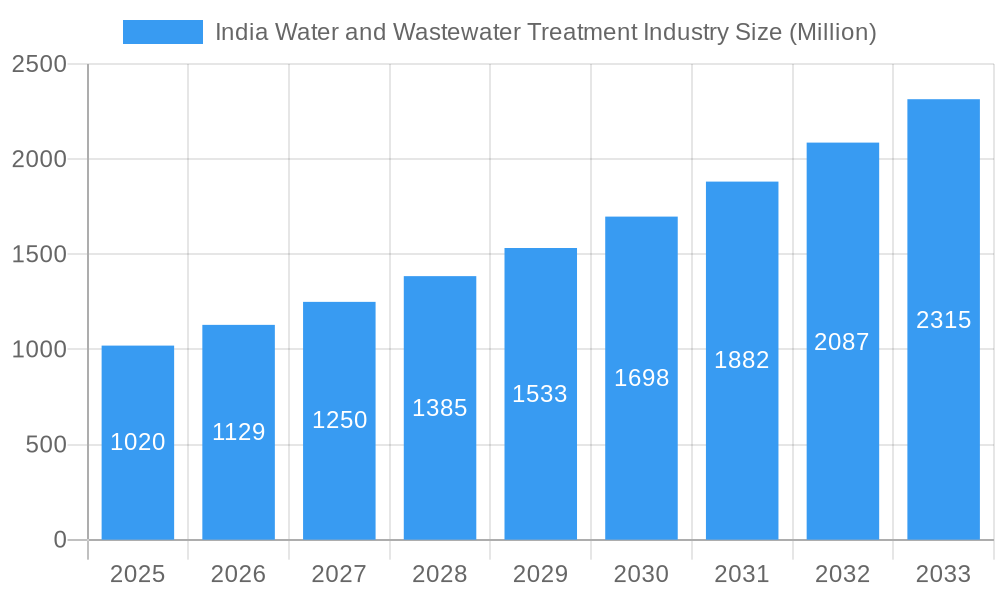

The Indian Water and Wastewater Treatment Industry is poised for significant expansion, with a projected market size of 1020 million by 2025. This growth is fueled by an impressive 10.78% Compound Annual Growth Rate (CAGR), indicating robust momentum in the sector. The escalating demand for clean water, coupled with stringent environmental regulations and increasing industrialization, are the primary drivers. Key industries like Municipal, Food & Beverage, Pulp & Paper, and Oil & Gas are investing heavily in advanced treatment solutions to meet their water needs and comply with discharge standards. The market is segmented across various treatment equipment, including oil/water separation, suspended solids removal, dissolved solids removal, biological treatment for nutrient and metals recovery, and disinfection/oxidation technologies. Process control equipment and pumps also form a crucial part of the infrastructure.

India Water and Wastewater Treatment Industry Market Size (In Billion)

Several emerging trends are shaping the Indian water and wastewater treatment landscape. There's a growing emphasis on decentralized treatment systems, smart water management technologies, and the adoption of membrane filtration and advanced oxidation processes for more efficient contaminant removal. The focus on water recycling and reuse is also gaining traction, driven by water scarcity concerns. However, challenges such as high initial investment costs, a lack of skilled personnel in remote areas, and policy implementation hurdles can act as restraints. Despite these, the strong commitment from major players like Thermax Limited, VA TECH WABAG LIMITED, Evoqua Water Technologies LLC, and Veolia, along with government initiatives promoting water conservation and treatment, are expected to propel the industry forward. The continuous innovation in treatment technologies and the expanding industrial base will further solidify India's position as a key market for water and wastewater solutions.

India Water and Wastewater Treatment Industry Company Market Share

Here is a comprehensive, SEO-optimized report description for the India Water and Wastewater Treatment Industry, incorporating high-traffic keywords, parent/child market dynamics, and all specified details without placeholders.

India Water and Wastewater Treatment Industry Market Dynamics & Structure

The India water and wastewater treatment market is characterized by a moderately concentrated structure, with key players like Thermax Limited, VA TECH WABAG LIMITED, and Veolia dominating market share. Technological innovation, particularly in areas like membrane filtration, advanced oxidation processes, and digital monitoring solutions, serves as a significant growth driver. Stringent regulatory frameworks, such as the National Water Policy and initiatives by the Ministry of Jal Shakti, are compelling widespread adoption of advanced treatment technologies. Competitive product substitutes are emerging from localized, smaller players offering cost-effective solutions, posing a challenge to established manufacturers. End-user demographics are rapidly shifting towards increased industrial demand and a growing focus on municipal wastewater reuse, driven by water scarcity. Mergers and acquisitions (M&A) are expected to accelerate as larger entities seek to consolidate their market position and acquire innovative technologies. For instance, in 2023, the market witnessed an estimated 3-5 significant M&A deals focused on acquiring specialized wastewater treatment capabilities. Barriers to innovation include high initial capital expenditure for advanced technologies and the need for skilled workforce training in operating and maintaining complex systems.

- Market Concentration: Moderately concentrated with leading players holding substantial market share.

- Technological Innovation Drivers: Advanced filtration, biological treatment, digital solutions, and IoT integration.

- Regulatory Frameworks: National Water Policy, Jal Jeevan Mission, Swachh Bharat Abhiyan, and state-specific environmental regulations.

- Competitive Product Substitutes: Lower-cost, localized solutions and DIY treatment systems.

- End-User Demographics: Growing demand from industrial sectors and increasing focus on municipal wastewater reuse.

- M&A Trends: Expected to increase, targeting technology acquisition and market consolidation.

- Innovation Barriers: High capital investment, skilled workforce scarcity.

India Water and Wastewater Treatment Industry Growth Trends & Insights

The India water and wastewater treatment market is poised for substantial expansion, projecting a CAGR of approximately 8-10% during the forecast period of 2025–2033. This robust growth trajectory is fueled by a confluence of factors, including escalating water scarcity, rising industrial activity, and a strong government emphasis on sanitation and water resource management. The market size, estimated at XXX billion units in 2025, is anticipated to reach XXX billion units by 2033. Adoption rates for advanced treatment technologies are surging, particularly among the Food and Beverage and Chemical and Petrochemical industries, driven by the need to meet stringent discharge norms and the growing trend of water recycling and reuse. Technological disruptions are evident in the increased integration of smart technologies, such as IoT-enabled sensors for real-time monitoring and AI-driven process optimization, enhancing operational efficiency and reducing treatment costs. Consumer behavior is shifting towards greater environmental awareness, with a growing demand for treated wastewater for non-potable uses, thus creating new revenue streams for treatment solution providers. The increasing prevalence of Zero Liquid Discharge (ZLD) plants across industries further underscores this trend. Government initiatives like the National Mission for Clean Ganga (NMCG) are also acting as significant catalysts, driving investments in municipal wastewater treatment infrastructure. The increasing urbanization and population growth are further augmenting the demand for effective wastewater management solutions, contributing to the overall market penetration of water and wastewater treatment technologies. The shift from a traditional linear water management approach to a circular economy model where water is conserved and reused is a pivotal behavioral change impacting the industry.

Dominant Regions, Countries, or Segments in India Water and Wastewater Treatment Industry

Within the India water and wastewater treatment industry, Treatment Equipment emerges as the dominant market segment, driven by substantial investments across various sub-segments. Within Treatment Equipment, Biological Treatment/Nutrient and Metals Recovery is witnessing particularly rapid growth, propelled by stringent regulations on nutrient discharge and the increasing focus on resource recovery from wastewater. The Municipal end-user industry represents a significant driver of growth, with ongoing and planned investments in Sewage Treatment Plants (STPs) and Effluent Treatment Plants (ETPs) across urban and semi-urban areas. Economically, states with a high concentration of industrial activity, such as Gujarat, Maharashtra, and Tamil Nadu, are leading the adoption of advanced industrial wastewater treatment solutions. These regions benefit from supportive industrial policies and a proactive approach to environmental compliance. The Oil and Gas and Chemical and Petrochemical sectors are also major contributors, demanding sophisticated treatment technologies like Oil/Water Separation and Dissolved Solids Removal to manage complex industrial effluents and comply with environmental norms. The Food and Beverage industry’s increasing emphasis on water recycling for process applications is also fueling demand for advanced Disinfection/Oxidation and Suspended Solids Removal equipment. Government initiatives like the Swachh Bharat Abhiyan and the Jal Jeevan Mission, aimed at improving sanitation and providing potable water to all households, are further accelerating the demand for municipal treatment solutions across all regions. The Process Control Equipment and Pumps segment, while not as large as Treatment Equipment, is crucial for the efficient operation of all treatment processes and is experiencing steady growth due to the increasing sophistication of treatment plants. The Poultry and Agriculture sector, though currently a smaller market, holds significant untapped potential for wastewater treatment solutions, particularly for managing animal waste and agricultural runoff, reflecting a growing awareness of sustainable practices.

- Dominant Segment: Treatment Equipment

- Key Sub-segments: Biological Treatment/Nutrient and Metals Recovery, Oil/Water Separation, Dissolved Solids Removal, Suspended Solids Removal.

- Dominant End-user Industry: Municipal

- Driving Factors: Urbanization, government sanitation programs (Swachh Bharat Abhiyan), safe drinking water initiatives (Jal Jeevan Mission).

- Leading Regions (Industrial): Gujarat, Maharashtra, Tamil Nadu

- Key Industries: Chemical and Petrochemical, Oil and Gas, Food and Beverage.

- Growth Potential in Emerging Sectors: Poultry and Agriculture.

- Ancillary Segment Growth: Process Control Equipment and Pumps.

India Water and Wastewater Treatment Industry Product Landscape

The product landscape in the India water and wastewater treatment industry is characterized by a drive towards greater efficiency, sustainability, and automation. Innovations in Treatment Equipment include highly efficient membrane bioreactors for enhanced biological treatment, advanced ceramic membranes for superior filtration, and compact, modular solutions for decentralized applications. Oil/Water Separators are evolving with coalescing technologies that offer higher separation efficiency. Dissolved Solids Removal technologies are seeing advancements in electrodialysis and forward osmosis, reducing energy consumption. Biological treatment systems are incorporating advanced nutrient and metal recovery techniques, turning waste into valuable resources. Disinfection/Oxidation methods are increasingly leveraging UV-LED technology and advanced oxidation processes (AOPs) for effective pathogen inactivation and pollutant breakdown. The integration of Process Control Equipment and Pumps with IoT capabilities allows for real-time data analytics, predictive maintenance, and remote monitoring, optimizing treatment plant performance and minimizing operational costs. These advancements cater to diverse applications across municipal and industrial sectors, offering enhanced performance metrics such as higher recovery rates, lower energy footprints, and reduced chemical consumption.

Key Drivers, Barriers & Challenges in India Water and Wastewater Treatment Industry

The India water and wastewater treatment industry is propelled by several key drivers, including stringent environmental regulations mandating effective wastewater management, increasing water scarcity driving the need for recycling and reuse, and a growing government focus on sanitation and clean water initiatives. Technological advancements in treatment processes and the rising adoption of smart technologies also act as significant growth accelerators. Furthermore, the expanding industrial base, particularly in sectors like Chemical and Petrochemical and Food and Beverage, necessitates robust wastewater treatment solutions.

However, the industry faces several barriers and challenges. High capital expenditure for establishing advanced treatment facilities remains a significant hurdle, especially for smaller municipalities and industries. Operational and maintenance costs, coupled with a shortage of skilled manpower to operate complex treatment plants, pose ongoing challenges. Supply chain disruptions can impact the availability of critical components and chemicals. Regulatory enforcement can be inconsistent, leading to non-compliance in some sectors. Intense competition from both domestic and international players, coupled with price sensitivity in certain market segments, also presents challenges.

Emerging Opportunities in India Water and Wastewater Treatment Industry

Emerging opportunities in the India water and wastewater treatment industry lie in the burgeoning market for decentralized wastewater treatment systems for rural and peri-urban areas. The growing demand for treated industrial wastewater for non-potable applications, particularly in water-stressed industrial clusters, presents a significant opportunity. Innovations in resource recovery from wastewater, such as biogas generation and nutrient extraction, are gaining traction. The digitalization of water management through IoT and AI offers opportunities for smart monitoring, predictive maintenance, and optimized plant operations. Furthermore, the increasing awareness and adoption of Zero Liquid Discharge (ZLD) technologies across various industries are creating new avenues for specialized solutions.

Growth Accelerators in the India Water and Wastewater Treatment Industry Industry

Several catalysts are accelerating the long-term growth of the India water and wastewater treatment industry. Technological breakthroughs in membrane filtration, advanced oxidation processes, and biological treatment continue to enhance efficiency and reduce costs. Strategic partnerships between technology providers, engineering firms, and government agencies are crucial for project execution and market penetration. Market expansion strategies focusing on underserved rural areas and specific industrial niches are key to unlocking new growth potential. The increasing emphasis on a circular economy approach to water management, promoting water recycling and reuse, is a significant long-term growth accelerator.

Key Players Shaping the India Water and Wastewater Treatment Industry Market

- Thermax Limited

- VA TECH WABAG LIMITED

- Evoqua Water Technologies LLC

- Mott MacDonald

- Aquatech International LLC

- Hitachi Ltd

- DuPont

- Hindustan Dorr-Oliver Ltd

- Suez

- Siemens Water Solutions

- Schlumberger Limited

- Veolia

Notable Milestones in India Water and Wastewater Treatment Industry Sector

- November 2022: WABAG LIMITED signed an agreement with the Asian Development Bank ('ADB') for raising a fund of INR 200 crores (~ USD 24.6 million) through unlisted Non-Convertible Debentures carrying five years and three months tenors. ADB will subscribe to it for over 12 months in its water treatment business.

- August 2022: An Israeli company, Huliot Pipes, launched the ClearBlack Sewage Treatment Plant customized for the Indian market for wastewater recycling and reuse.

In-Depth India Water and Wastewater Treatment Industry Market Outlook

The future market potential for the India water and wastewater treatment industry is exceptionally bright, driven by a sustained commitment to water security and environmental sustainability. Strategic opportunities lie in leveraging advanced technologies for resource recovery, expanding the reach of decentralized treatment solutions, and fostering innovation in digital water management platforms. The increasing adoption of circular economy principles in water usage will further shape market dynamics, creating demand for integrated solutions that prioritize reuse and minimize waste. Investments in infrastructure development, coupled with evolving industrial and municipal needs, will continue to drive robust growth in the coming years.

India Water and Wastewater Treatment Industry Segmentation

-

1. Equipment Type

-

1.1. Treatment Equipment

- 1.1.1. Oil/Water Separation

- 1.1.2. Suspended Solids Removal

- 1.1.3. Dissolved Solids Removal

- 1.1.4. Biological Treatment/Nutrient and Metals Recovery

- 1.1.5. Disinfection/Oxidation

- 1.1.6. Other Treatment Equipment

- 1.2. Process Control Equipment and Pumps

-

1.1. Treatment Equipment

-

2. End-user Industry

- 2.1. Municipal

- 2.2. Food and Beverage

- 2.3. Pulp and Paper

- 2.4. Oil and Gas

- 2.5. Healthcare

- 2.6. Poultry and Agriculture

- 2.7. Chemical and Petrochemical

- 2.8. Other End-user Industries

India Water and Wastewater Treatment Industry Segmentation By Geography

- 1. India

India Water and Wastewater Treatment Industry Regional Market Share

Geographic Coverage of India Water and Wastewater Treatment Industry

India Water and Wastewater Treatment Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.78% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Equipment Type

- 5.1.1. Treatment Equipment

- 5.1.1.1. Oil/Water Separation

- 5.1.1.2. Suspended Solids Removal

- 5.1.1.3. Dissolved Solids Removal

- 5.1.1.4. Biological Treatment/Nutrient and Metals Recovery

- 5.1.1.5. Disinfection/Oxidation

- 5.1.1.6. Other Treatment Equipment

- 5.1.2. Process Control Equipment and Pumps

- 5.1.1. Treatment Equipment

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Municipal

- 5.2.2. Food and Beverage

- 5.2.3. Pulp and Paper

- 5.2.4. Oil and Gas

- 5.2.5. Healthcare

- 5.2.6. Poultry and Agriculture

- 5.2.7. Chemical and Petrochemical

- 5.2.8. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. India

- 5.1. Market Analysis, Insights and Forecast - by Equipment Type

- 6. India Water and Wastewater Treatment Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Equipment Type

- 6.1.1. Treatment Equipment

- 6.1.1.1. Oil/Water Separation

- 6.1.1.2. Suspended Solids Removal

- 6.1.1.3. Dissolved Solids Removal

- 6.1.1.4. Biological Treatment/Nutrient and Metals Recovery

- 6.1.1.5. Disinfection/Oxidation

- 6.1.1.6. Other Treatment Equipment

- 6.1.2. Process Control Equipment and Pumps

- 6.1.1. Treatment Equipment

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Municipal

- 6.2.2. Food and Beverage

- 6.2.3. Pulp and Paper

- 6.2.4. Oil and Gas

- 6.2.5. Healthcare

- 6.2.6. Poultry and Agriculture

- 6.2.7. Chemical and Petrochemical

- 6.2.8. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Equipment Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Thermax Limited

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 VA TECH WABAG LIMITED

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Evoqua Water Technologies LLC

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Mott MacDonald

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Aquatech International LLC

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Hitachi Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 DuPont

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Hindustan Dorr-Oliver Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Suez

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Siemens Water Solutions

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Schlumberger Limited

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Veolia

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 Thermax Limited

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: India Water and Wastewater Treatment Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: India Water and Wastewater Treatment Industry Share (%) by Company 2025

List of Tables

- Table 1: India Water and Wastewater Treatment Industry Revenue Million Forecast, by Equipment Type 2020 & 2033

- Table 2: India Water and Wastewater Treatment Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 3: India Water and Wastewater Treatment Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: India Water and Wastewater Treatment Industry Revenue Million Forecast, by Equipment Type 2020 & 2033

- Table 5: India Water and Wastewater Treatment Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 6: India Water and Wastewater Treatment Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Water and Wastewater Treatment Industry?

The projected CAGR is approximately 10.78%.

2. Which companies are prominent players in the India Water and Wastewater Treatment Industry?

Key companies in the market include Thermax Limited, VA TECH WABAG LIMITED, Evoqua Water Technologies LLC, Mott MacDonald, Aquatech International LLC, Hitachi Ltd, DuPont, Hindustan Dorr-Oliver Ltd, Suez, Siemens Water Solutions, Schlumberger Limited, Veolia.

3. What are the main segments of the India Water and Wastewater Treatment Industry?

The market segments include Equipment Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.02 Million as of 2022.

5. What are some drivers contributing to market growth?

Rapidly Diminishing Fresh Water Resources; Growing Wastewater Complexities.

6. What are the notable trends driving market growth?

Treatment Equipment to Dominate the Market.

7. Are there any restraints impacting market growth?

High Cost of Water Treatment Technology.

8. Can you provide examples of recent developments in the market?

November 2022: WABAG LIMITED signed an agreement with the Asian Development Bank ('ADB') for raising a fund of INR 200 crores (~ USD 24.6 million) through unlisted Non-Convertible Debentures carrying five years and three months tenors. ADB will subscribe to it for over 12 months in its water treatment business.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Water and Wastewater Treatment Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Water and Wastewater Treatment Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Water and Wastewater Treatment Industry?

To stay informed about further developments, trends, and reports in the India Water and Wastewater Treatment Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence