Key Insights

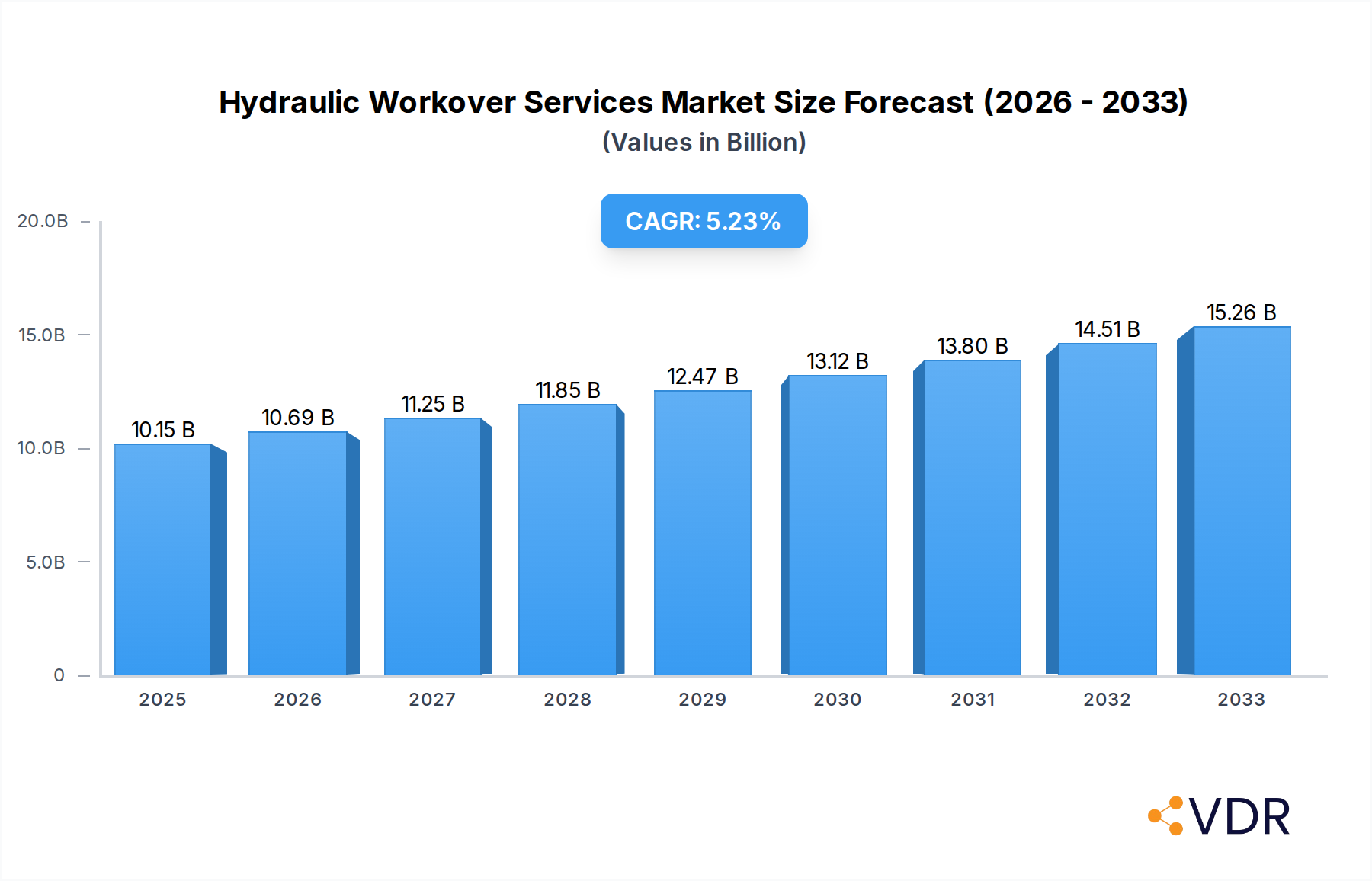

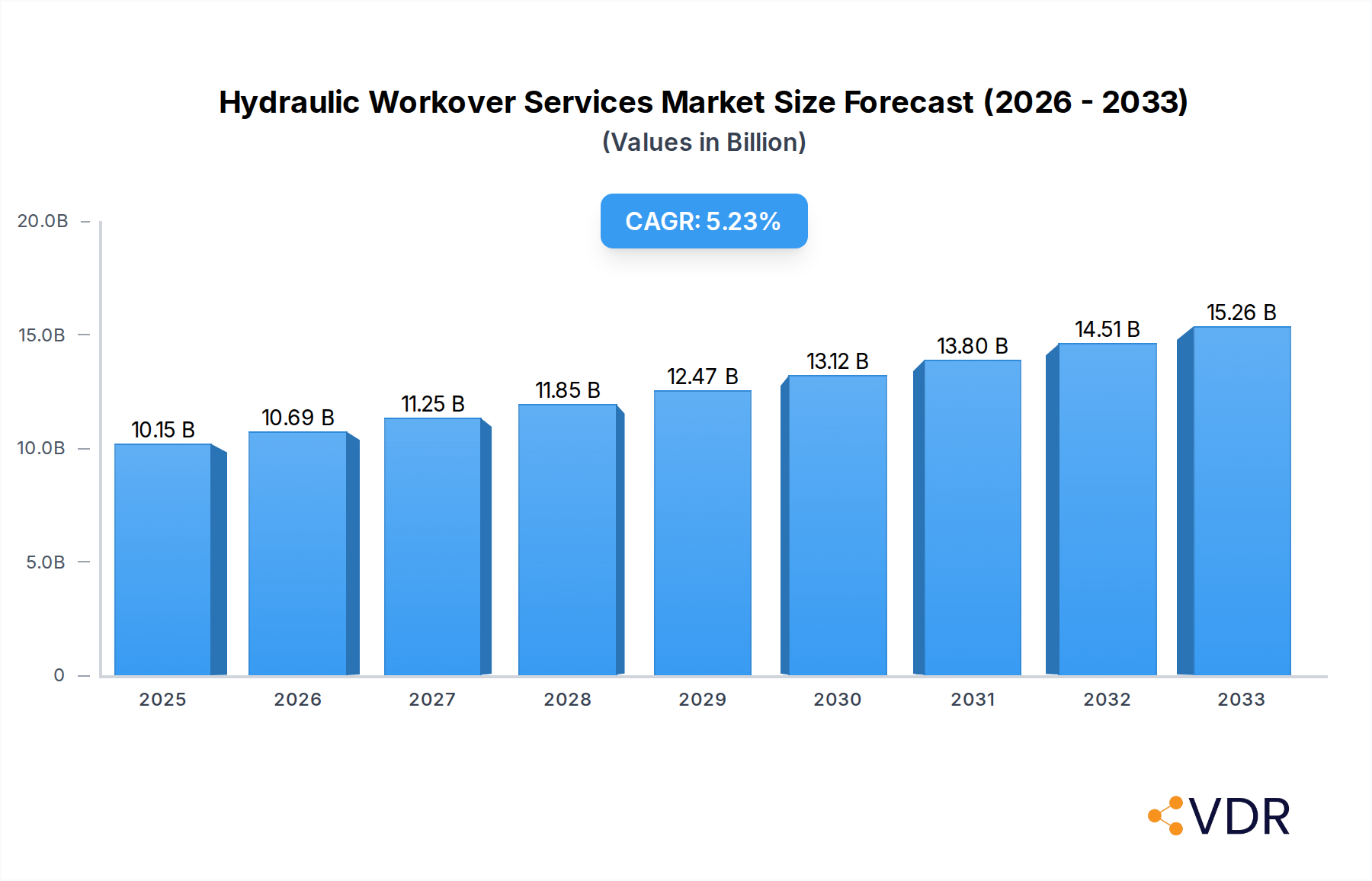

The global Hydraulic Workover Services market is poised for significant expansion, projected to reach $10.15 billion in 2025. This growth is fueled by increasing demand for enhanced oil recovery (EOR) techniques and the need to maintain production from aging oil and gas wells, particularly in mature fields. The market is expected to witness a Compound Annual Growth Rate (CAGR) of 5.22% during the forecast period of 2025-2033, indicating a robust and sustained upward trajectory. Key drivers include the ongoing exploration and production activities in both onshore and offshore environments, as well as the inherent cost-effectiveness and operational flexibility of hydraulic workover units compared to conventional drilling rigs for specific well servicing tasks. The imperative to optimize production from existing reserves, coupled with advancements in hydraulic workover technology, is creating substantial opportunities for service providers.

Hydraulic Workover Services Market Size (In Billion)

The market segmentation reveals a strong emphasis on the "Onshore" application, reflecting the vast number of existing onshore wells requiring maintenance and intervention. While offshore operations represent a smaller but growing segment, the complexity and high cost associated with offshore workover necessitate specialized and efficient solutions. The "Workover" segment is anticipated to dominate due to the continuous need for wellbore maintenance, intervention, and remediation to sustain production. Emerging trends such as the integration of advanced digital technologies for real-time monitoring and data analytics, alongside a growing focus on environmental sustainability and reduced operational footprint, are shaping the future of hydraulic workover services. Despite the positive outlook, factors such as fluctuating oil prices, stringent environmental regulations, and the availability of skilled labor can present challenges to market expansion.

Hydraulic Workover Services Company Market Share

Here's the SEO-optimized report description for Hydraulic Workover Services, incorporating your requirements:

Hydraulic Workover Services Market Dynamics & Structure

The global Hydraulic Workover Services market is characterized by a moderate to high level of concentration, with leading players like Halliburton, Superior Energy Services, Precision Drilling, and Nabors Industries holding significant market share. Technological innovation remains a primary driver, fueled by the demand for more efficient, cost-effective, and environmentally conscious well intervention solutions. Advancements in coiled tubing technology, remote monitoring, and automated systems are transforming operational capabilities. Regulatory frameworks, particularly concerning environmental protection and safety standards, continue to shape market entry and operational practices. Competitive product substitutes, such as conventional workover rigs and wireline services, present ongoing challenges, necessitating continuous innovation and differentiation. End-user demographics are increasingly influenced by the shift towards unconventional resource development and the aging of existing well infrastructure, demanding specialized workover expertise. Mergers and acquisitions (M&A) activity has been sporadic but significant, driven by consolidation strategies and the pursuit of expanded service portfolios and geographic reach. Key M&A trends focus on acquiring specialized technologies and niche market capabilities. For instance, the market is segmented into onshore and offshore applications, with workover and snubbing representing the primary service types. The market is projected to witness steady growth.

- Market Concentration: Moderate to high, with a few dominant players.

- Technological Innovation Drivers: Demand for efficiency, cost reduction, environmental compliance, and advanced well intervention.

- Regulatory Frameworks: Stringent safety and environmental regulations influence operational standards.

- Competitive Product Substitutes: Conventional workover rigs, wireline services, and alternative well intervention methods.

- End-User Demographics: Oil and gas exploration and production companies focusing on unconventional resources and mature field maintenance.

- M&A Trends: Consolidation for expanded service offerings and market access, acquisition of specialized technologies.

Hydraulic Workover Services Growth Trends & Insights

The Hydraulic Workover Services market is poised for robust expansion, driven by a confluence of factors that underscore the critical role of well intervention in the oil and gas lifecycle. The global market size for hydraulic workover services is projected to reach an estimated $25 billion by the end of the forecast period in 2033. This growth trajectory is supported by a Compound Annual Growth Rate (CAGR) of approximately 5.8% from the base year of 2025. Adoption rates are steadily increasing as operators increasingly recognize the inherent advantages of hydraulic workover units, including their mobility, faster rig-up/rig-down times, and suitability for a wider range of well conditions compared to conventional rigs. Technological disruptions are continuously reshaping the landscape. The integration of advanced automation, real-time data analytics, and specialized coiled tubing technologies is enhancing operational efficiency, safety, and the ability to perform complex interventions in challenging environments, particularly in the offshore segment where space and accessibility are at a premium. Consumer behavior shifts within the oil and gas industry are also playing a pivotal role. There's a growing emphasis on optimizing production from existing mature fields, extending well life, and performing cost-effective plug and abandonment operations. This necessitates specialized workover services that can deliver precise and efficient interventions. The market penetration of hydraulic workover services is expected to deepen as operators prioritize asset integrity management and production optimization strategies. Furthermore, the increasing complexity of new reservoir developments and the need for enhanced wellbore integrity are creating sustained demand. The inherent flexibility and adaptability of hydraulic workover systems make them indispensable for a variety of applications, from routine maintenance to emergency well control. The market is also influenced by the global energy transition, with a continued need for efficient hydrocarbon production while simultaneously supporting the development of new energy sources, where well intervention might still be required. The estimated market size in the base year of 2025 is approximately $15 billion.

Dominant Regions, Countries, or Segments in Hydraulic Workover Services

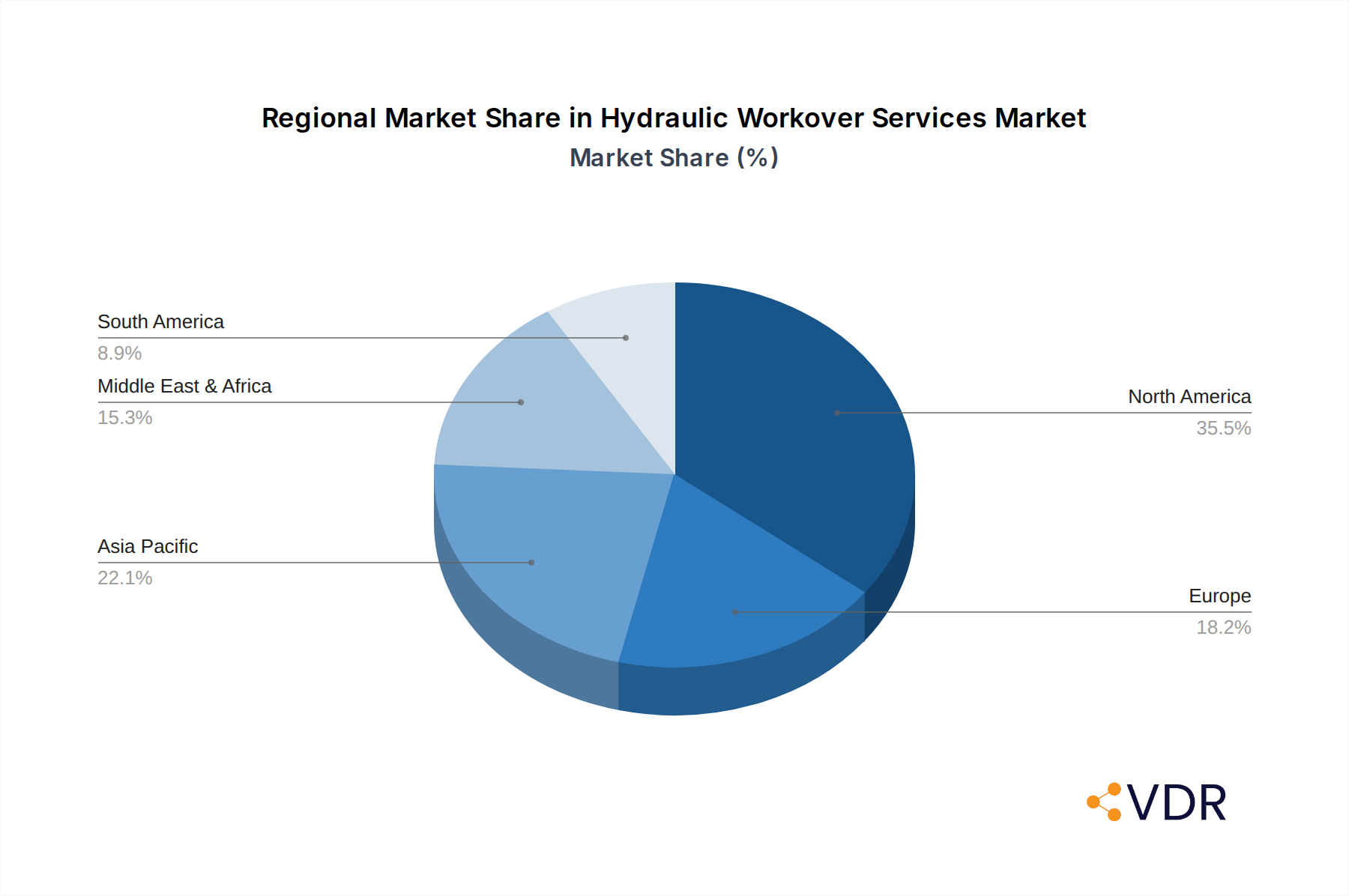

The Onshore segment of the hydraulic workover services market is currently the dominant force driving global growth, accounting for an estimated 65% of the total market value. This dominance is primarily attributed to the vast number of mature onshore oil and gas fields worldwide that require continuous intervention for optimization and maintenance. North America, particularly the United States, is a leading country within this segment, fueled by extensive unconventional resource plays and a well-established oil and gas infrastructure. The region's significant shale oil and gas production necessitates a constant stream of workover activities, including well stimulation, artificial lift optimization, and repair operations. Economic policies that support domestic energy production and a robust network of service providers contribute to North America's leading position.

- Key Drivers in Onshore Dominance:

- Mature Field Development: Extensive infrastructure and aging wells requiring ongoing intervention.

- Unconventional Resource Plays: Continuous need for well workovers in shale plays for production optimization.

- Cost-Effectiveness: Onshore operations generally incur lower logistical and operational costs compared to offshore.

- Technological Advancements: Improved coiled tubing and snubbing technologies enhance onshore efficiency.

The Offshore segment, while currently smaller in market share, is exhibiting a higher growth potential. This is driven by the increasing complexity of deepwater exploration and production, the need for extended well life in offshore assets, and stringent decommissioning requirements. The Asia-Pacific region, particularly countries with significant offshore reserves like China and Southeast Asian nations, is emerging as a key growth area due to ongoing exploration activities and the development of challenging offshore fields. The higher cost of offshore operations is offset by the necessity of specialized services that hydraulic workover rigs can provide more efficiently and safely than traditional methods in a harsh environment.

- Key Drivers in Offshore Growth Potential:

- Deepwater Exploration & Production: Growing complexity and operational demands in offshore basins.

- Well Decommissioning: Increasing focus on responsible well abandonment in offshore environments.

- Technological Sophistication: Demand for advanced solutions for remote and challenging offshore interventions.

- Limited Accessibility: Hydraulic workover's mobility and reduced footprint are advantageous offshore.

Among the Types, the Workover segment accounts for the largest share due to its broad applicability in well maintenance, repair, and artificial lift installation. However, the Snubbing segment is experiencing significant growth due to its specialized capability in handling live wells and high-pressure environments, a growing concern in both onshore and offshore fields.

Hydraulic Workover Services Product Landscape

Hydraulic workover services are defined by their robust and versatile equipment, primarily consisting of hydraulic-powered rigs and associated coiled tubing or jointed pipe systems. Innovations focus on enhancing mobility, reducing rig-up times, and improving operational precision. Recent advancements include the development of more compact and powerful hydraulic units for confined onshore locations and specialized offshore-rated equipment capable of withstanding extreme environmental conditions. Performance metrics emphasize faster intervention times, reduced non-productive time (NPT), and enhanced safety features, such as automated control systems and improved wellbore pressure management. Unique selling propositions lie in the ability to perform complex operations like fishing, milling, reperforation, and artificial lift installation with greater efficiency and reduced risk.

Key Drivers, Barriers & Challenges in Hydraulic Workover Services

Key Drivers:

- Demand for Well Optimization: Continuous need to maintain and enhance production from existing oil and gas wells.

- Technological Advancements: Innovations in coiled tubing, snubbing, and control systems enhance efficiency and safety.

- Environmental Regulations: Increasing focus on well integrity and responsible decommissioning drives demand.

- Cost-Effectiveness: Hydraulic workover offers a more economical alternative for certain interventions compared to conventional rigs.

- Unconventional Resource Development: Ongoing exploration and production in shale plays necessitate specialized workover services.

Key Barriers & Challenges:

- Price Volatility of Crude Oil: Fluctuations in oil prices can impact E&P budgets and subsequently, workover service demand.

- Skilled Workforce Shortage: A limited pool of experienced personnel can hinder operational capacity and innovation.

- Geopolitical Instability: Disruptions in key oil-producing regions can affect project timelines and investments.

- Supply Chain Disruptions: Global supply chain issues can impact equipment availability and maintenance.

- Intense Competition: A fragmented market with numerous service providers can lead to price pressures.

Emerging Opportunities in Hydraulic Workover Services

Emerging opportunities in the hydraulic workover services sector are largely driven by the evolving energy landscape and the increasing demand for specialized well intervention solutions. The growing emphasis on extending the life of mature fields presents a significant opportunity for hydraulic workover services to perform complex interventions, increasing reserves and production. Furthermore, the transition towards cleaner energy sources is indirectly creating opportunities; as conventional oil and gas infrastructure ages, the need for well plugging and abandonment services, where hydraulic workover excels, will surge. There is also a growing niche for hydraulic workover in supporting carbon capture and storage (CCS) projects, particularly in the injection and monitoring phases of wells. The development of advanced digital solutions for real-time monitoring, predictive maintenance, and remote operational control will further enhance the appeal and efficiency of these services, opening doors for new service models and market penetration.

Growth Accelerators in the Hydraulic Workover Services Industry

Several key factors are accelerating the growth of the hydraulic workover services industry. Technological breakthroughs, particularly in the miniaturization and enhanced power of hydraulic systems, alongside advancements in coiled tubing materials and deployment techniques, are enabling interventions in more challenging environments and at greater depths. Strategic partnerships between service providers and E&P companies are crucial for developing tailored solutions and securing long-term contracts, fostering stability and innovation. Market expansion strategies, including the penetration of emerging oil and gas regions and the diversification of service offerings beyond traditional workovers to include specialized decommissioning and monitoring services, are also contributing significantly to sustained growth. The industry's ability to adapt to evolving regulatory landscapes and to champion environmentally responsible practices will further solidify its growth trajectory.

Key Players Shaping the Hydraulic Workover Services Market

- Halliburton

- Superior Energy Services

- Precision Drilling

- Basic Energy Services

- Cudd Energy Services

- Nabors Industries

- UMW Oil & Gas

- EMAS Energy Services

- Archer Limited

- High Arctic Energy Services

Notable Milestones in Hydraulic Workover Services Sector

- 2019: Introduction of advanced remote monitoring and control systems for hydraulic workover units, enhancing safety and efficiency.

- 2020: Increased adoption of coiled tubing with higher tensile strength and improved pressure ratings, allowing for deeper and more complex interventions.

- 2021: Significant investments in automation for hydraulic workover operations, reducing human intervention in critical phases.

- 2022: Growing demand for specialized hydraulic workover solutions for well decommissioning and plugging in mature fields.

- 2023: Development of more compact and mobile hydraulic workover units for efficient deployment in remote onshore locations.

- 2024: Enhanced integration of real-time data analytics and AI for predictive maintenance and optimized operational planning.

In-Depth Hydraulic Workover Services Market Outlook

The hydraulic workover services market is set for sustained and accelerated growth in the coming years. Growth accelerators such as continued technological innovation, particularly in automation and data analytics, will drive operational efficiencies and expand the scope of achievable interventions. Strategic partnerships between service providers and exploration and production companies will be pivotal in securing market share and fostering the development of bespoke solutions for evolving field challenges. The market's ability to cater to the increasing demand for well decommissioning services, driven by environmental regulations and the aging of global oil and gas infrastructure, presents a significant and enduring opportunity. Furthermore, the ongoing global demand for hydrocarbons, coupled with the necessity of maintaining and optimizing existing production, ensures a baseline requirement for hydraulic workover services. The industry's adaptability and commitment to safety and environmental stewardship will further solidify its position as an indispensable component of the upstream oil and gas value chain.

Hydraulic Workover Services Segmentation

-

1. Application

- 1.1. Onshore

- 1.2. Offshore

-

2. Types

- 2.1. Workover

- 2.2. Snubbing

Hydraulic Workover Services Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Hydraulic Workover Services Regional Market Share

Geographic Coverage of Hydraulic Workover Services

Hydraulic Workover Services REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.22% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Hydraulic Workover Services Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Onshore

- 5.1.2. Offshore

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Workover

- 5.2.2. Snubbing

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Hydraulic Workover Services Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Onshore

- 6.1.2. Offshore

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Workover

- 6.2.2. Snubbing

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Hydraulic Workover Services Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Onshore

- 7.1.2. Offshore

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Workover

- 7.2.2. Snubbing

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Hydraulic Workover Services Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Onshore

- 8.1.2. Offshore

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Workover

- 8.2.2. Snubbing

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Hydraulic Workover Services Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Onshore

- 9.1.2. Offshore

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Workover

- 9.2.2. Snubbing

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Hydraulic Workover Services Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Onshore

- 10.1.2. Offshore

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Workover

- 10.2.2. Snubbing

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Halliburton

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Superior Energy Services

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Precision Drilling

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Basic Energy Services

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Cudd Energy Services

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Nabors Industries

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 UMW Oil & Gas

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 EMAS Energy Services

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Archer Limited

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 High Arctic Energy Services

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Halliburton

List of Figures

- Figure 1: Global Hydraulic Workover Services Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Hydraulic Workover Services Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Hydraulic Workover Services Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Hydraulic Workover Services Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Hydraulic Workover Services Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Hydraulic Workover Services Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Hydraulic Workover Services Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Hydraulic Workover Services Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Hydraulic Workover Services Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Hydraulic Workover Services Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Hydraulic Workover Services Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Hydraulic Workover Services Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Hydraulic Workover Services Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Hydraulic Workover Services Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Hydraulic Workover Services Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Hydraulic Workover Services Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Hydraulic Workover Services Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Hydraulic Workover Services Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Hydraulic Workover Services Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Hydraulic Workover Services Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Hydraulic Workover Services Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Hydraulic Workover Services Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Hydraulic Workover Services Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Hydraulic Workover Services Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Hydraulic Workover Services Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Hydraulic Workover Services Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Hydraulic Workover Services Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Hydraulic Workover Services Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Hydraulic Workover Services Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Hydraulic Workover Services Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Hydraulic Workover Services Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Hydraulic Workover Services Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Hydraulic Workover Services Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Hydraulic Workover Services Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Hydraulic Workover Services Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Hydraulic Workover Services Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Hydraulic Workover Services Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Hydraulic Workover Services Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Hydraulic Workover Services Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Hydraulic Workover Services Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Hydraulic Workover Services Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Hydraulic Workover Services Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Hydraulic Workover Services Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Hydraulic Workover Services Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Hydraulic Workover Services Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Hydraulic Workover Services Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Hydraulic Workover Services Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Hydraulic Workover Services Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Hydraulic Workover Services Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Hydraulic Workover Services Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Hydraulic Workover Services Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Hydraulic Workover Services Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Hydraulic Workover Services Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Hydraulic Workover Services Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Hydraulic Workover Services Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Hydraulic Workover Services Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Hydraulic Workover Services Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Hydraulic Workover Services Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Hydraulic Workover Services Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Hydraulic Workover Services Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Hydraulic Workover Services Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Hydraulic Workover Services Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Hydraulic Workover Services Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Hydraulic Workover Services Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Hydraulic Workover Services Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Hydraulic Workover Services Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Hydraulic Workover Services Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Hydraulic Workover Services Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Hydraulic Workover Services Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Hydraulic Workover Services Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Hydraulic Workover Services Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Hydraulic Workover Services Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Hydraulic Workover Services Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Hydraulic Workover Services Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Hydraulic Workover Services Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Hydraulic Workover Services Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Hydraulic Workover Services Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Hydraulic Workover Services?

The projected CAGR is approximately 5.22%.

2. Which companies are prominent players in the Hydraulic Workover Services?

Key companies in the market include Halliburton, Superior Energy Services, Precision Drilling, Basic Energy Services, Cudd Energy Services, Nabors Industries, UMW Oil & Gas, EMAS Energy Services, Archer Limited, High Arctic Energy Services.

3. What are the main segments of the Hydraulic Workover Services?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 10.15 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Hydraulic Workover Services," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Hydraulic Workover Services report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Hydraulic Workover Services?

To stay informed about further developments, trends, and reports in the Hydraulic Workover Services, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence