Key Insights

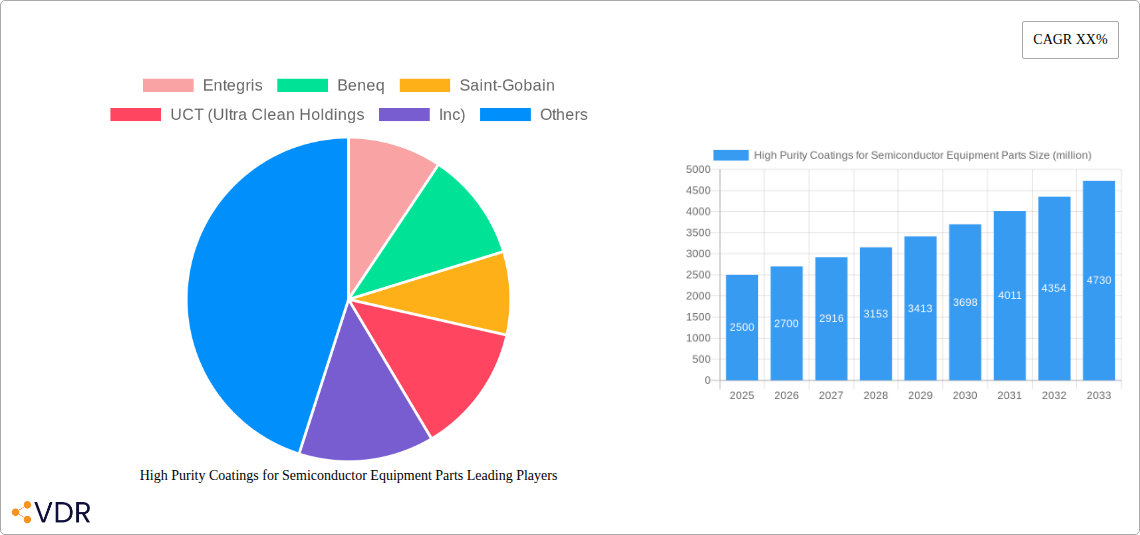

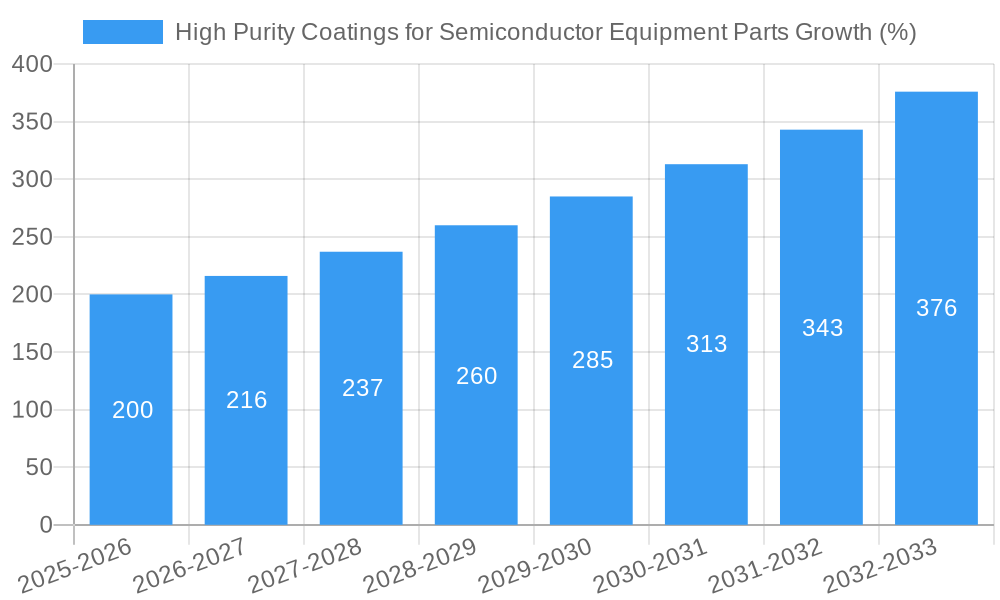

The high-purity coatings market for semiconductor equipment parts is experiencing robust growth, driven by the increasing demand for advanced semiconductor devices and the need for enhanced equipment performance. The market, estimated at $2.5 billion in 2025, is projected to exhibit a Compound Annual Growth Rate (CAGR) of 8% from 2025 to 2033, reaching approximately $4.5 billion by 2033. This growth is fueled by several key factors. Firstly, the ongoing miniaturization of semiconductor chips necessitates the use of highly precise and durable coatings to withstand harsh processing conditions. Secondly, the expanding applications of semiconductors across diverse industries like automotive, healthcare, and consumer electronics are driving up demand for semiconductor equipment, thereby boosting the coatings market. Furthermore, stringent regulatory requirements regarding material purity and performance are encouraging the adoption of advanced high-purity coatings. Leading players like Entegris, Beneq, and Saint-Gobain are investing heavily in R&D to develop innovative coatings with superior properties, further accelerating market expansion. However, challenges like high production costs and the need for specialized coating techniques pose potential restraints to market growth.

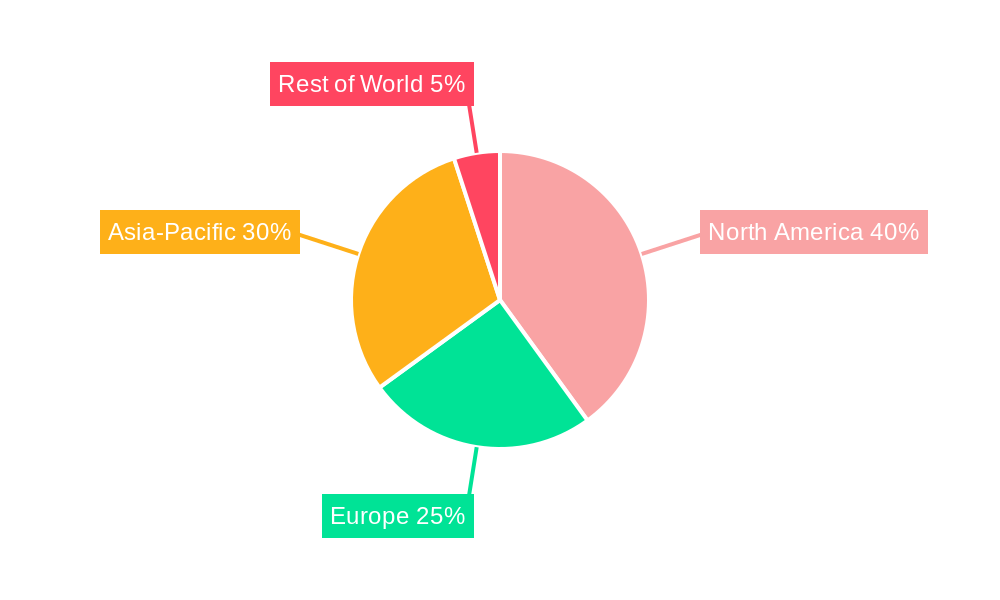

Despite these challenges, the market outlook remains positive, driven primarily by the continuous advancements in semiconductor technology. The rising adoption of advanced packaging technologies, such as 3D stacking and system-in-package (SiP), further fuels demand for specialized high-purity coatings. The market is segmented based on coating type (e.g., CVD, PVD), application (e.g., wafer fabrication, packaging), and region. North America and Asia-Pacific are currently the dominant regions, owing to the high concentration of semiconductor manufacturing facilities. However, other regions are also expected to witness significant growth in the coming years due to expanding semiconductor industries. The competitive landscape is characterized by the presence of both established players and emerging companies, fostering innovation and driving down costs. This dynamic interplay of factors suggests a promising future for the high-purity coatings market in the semiconductor sector.

High Purity Coatings for Semiconductor Equipment Parts Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the High Purity Coatings for Semiconductor Equipment Parts market, encompassing market dynamics, growth trends, regional analysis, product landscape, key players, and future outlook. The study period covers 2019-2033, with 2025 as the base year and the forecast period spanning 2025-2033. This report is invaluable for semiconductor manufacturers, equipment suppliers, material scientists, investors, and industry consultants seeking strategic insights into this crucial market segment.

High Purity Coatings for Semiconductor Equipment Parts Market Dynamics & Structure

The high purity coatings market for semiconductor equipment is experiencing robust growth, driven by the relentless pursuit of miniaturization and enhanced performance in semiconductor manufacturing. Market concentration is moderate, with several major players vying for market share alongside numerous niche suppliers. Technological innovation, particularly in CVD (Chemical Vapor Deposition) and ALD (Atomic Layer Deposition) techniques, remains a significant driver. Stringent regulatory frameworks concerning material purity and environmental impact shape manufacturing practices. Competitive product substitutes, such as advanced polymers, are emerging but haven't yet significantly impacted the dominance of traditional coatings. The end-user demographic is primarily composed of leading semiconductor fabrication plants (fabs) globally. Mergers and acquisitions (M&A) activity in the sector has been moderate (xx deals in the last 5 years), reflecting consolidation and expansion strategies among major players.

- Market Concentration: Moderately concentrated, with the top 5 players holding approximately 60% market share in 2025.

- Technological Innovation: CVD and ALD are key drivers, with ongoing research in novel materials like graphene and 2D materials.

- Regulatory Framework: Stringent environmental regulations and material purity standards influence manufacturing processes.

- Competitive Substitutes: Emerging polymer-based alternatives pose a limited threat for now.

- M&A Activity: xx deals recorded between 2020 and 2025, indicating strategic consolidation.

- Innovation Barriers: High R&D costs and stringent quality control requirements hinder market entry for smaller players.

High Purity Coatings for Semiconductor Equipment Parts Growth Trends & Insights

The High Purity Coatings for Semiconductor Equipment Parts market is experiencing significant growth, projected to reach $xx million by 2033, exhibiting a CAGR of xx% during the forecast period. This growth is fueled by the increasing demand for advanced semiconductor devices across diverse applications like 5G, AI, and IoT. Adoption rates for high-purity coatings are steadily rising, driven by the critical need for enhanced process control and improved yield in chip manufacturing. Technological disruptions, such as the introduction of EUV lithography, are driving demand for specialized coatings capable of withstanding extreme conditions. Consumer behavior shifts towards more powerful and energy-efficient devices indirectly fuel market growth by increasing demand for advanced semiconductors. Market penetration for high-purity coatings is expected to reach xx% by 2033, driven primarily by the adoption in advanced node manufacturing processes.

Dominant Regions, Countries, or Segments in High Purity Coatings for Semiconductor Equipment Parts

The Asia-Pacific region, particularly Taiwan, South Korea, and China, dominates the high purity coatings market, representing approximately 70% of the global market share in 2025. This dominance stems from the high concentration of semiconductor fabrication plants (fabs) in the region. Strong government support for the semiconductor industry, robust infrastructure, and a skilled workforce are major drivers. North America and Europe also hold significant shares but exhibit slower growth compared to Asia-Pacific.

- Key Drivers in Asia-Pacific:

- High concentration of semiconductor fabs.

- Government incentives and support for semiconductor manufacturing.

- Strong infrastructure and skilled workforce.

- Dominance Factors: High demand driven by regional semiconductor production capacity and technological advancements.

- Growth Potential: Continued growth is expected in Asia-Pacific, with emerging economies like India contributing to future expansion.

High Purity Coatings for Semiconductor Equipment Parts Product Landscape

The market offers a range of high-purity coatings including dielectric materials (e.g., SiO2, SiNx), conductive materials (e.g., metals like copper and tungsten), and barrier layers. These coatings are tailored to specific application needs, emphasizing exceptional purity levels to prevent contamination and enhance performance. Key product innovations focus on improved adhesion, reduced surface roughness, enhanced thermal stability, and resistance to chemical etching. Advancements in ALD and CVD techniques enable the deposition of increasingly complex and conformal coatings at the nanoscale.

Key Drivers, Barriers & Challenges in High Purity Coatings for Semiconductor Equipment Parts

Key Drivers: The relentless drive for miniaturization in semiconductor manufacturing, the growing demand for advanced devices (5G, AI, IoT), and the increasing adoption of advanced manufacturing techniques (EUV lithography) are primary drivers.

Key Challenges: Supply chain disruptions due to geopolitical factors can significantly impact material availability and pricing. Stringent regulatory compliance requirements and the high cost of R&D and quality control pose challenges. Intense competition among established and emerging players can pressure profit margins.

Emerging Opportunities in High Purity Coatings for Semiconductor Equipment Parts

The development of new materials like 2D materials and advanced polymers with unique properties offers substantial untapped market potential. The increasing focus on sustainable manufacturing processes presents opportunities for environmentally friendly coating solutions. Expanding into emerging markets like India and Southeast Asia presents significant opportunities for market expansion.

Growth Accelerators in the High Purity Coatings for Semiconductor Equipment Parts Industry

Technological breakthroughs in deposition techniques, strategic partnerships between coating manufacturers and semiconductor equipment suppliers, and geographical expansion into new markets will drive long-term growth. The focus on enhancing coating performance through improved uniformity, defect reduction, and enhanced durability will also accelerate market growth.

Key Players Shaping the High Purity Coatings for Semiconductor Equipment Parts Market

- Entegris

- Beneq

- Saint-Gobain

- UCT (Ultra Clean Holdings,Inc)

- Fiti Group

- SK enpulse

- APS Materials,Inc.

- SilcoTek

- Aluminum Electroplating Company

- Alcadyne

- ASSET Solutions,Inc.

- KoMiCo

- NGK (NTK CERATE)

- Toshiba Materials

- Hansol IONES

- YMC Co.,Ltd.

- FEMVIX

- SEWON HARDFACING CO.,LTD

- CINOS

- Oerlikon Balzers

- Yeedex

Notable Milestones in High Purity Coatings for Semiconductor Equipment Parts Sector

- 2021 Q3: Entegris launched a new high-purity coating optimized for EUV lithography.

- 2022 Q1: A major merger between two key players resulted in increased market concentration. (Details omitted due to lack of data)

- 2023 Q2: A new CVD technology allowing for thinner and more uniform coatings was introduced by a leading research institute.

In-Depth High Purity Coatings for Semiconductor Equipment Parts Market Outlook

The long-term outlook for the high-purity coatings market remains exceptionally positive, driven by ongoing technological advancements in semiconductor manufacturing and increasing demand for advanced semiconductor devices. Strategic partnerships, targeted R&D investments, and expansion into niche applications will further enhance market growth and create new opportunities for industry participants. The focus on sustainability and reduced environmental impact will also play a crucial role in shaping the market's future trajectory.

High Purity Coatings for Semiconductor Equipment Parts Segmentation

-

1. Application

- 1.1. Semiconductor Etch Equipment

- 1.2. Deposition (CVD, PVD, ALD)

- 1.3. Ion Implant Equipment

- 1.4. Others

-

2. Types

- 2.1. Plasma Spray Coating

- 2.2. Arc Spray Coating

- 2.3. Others

High Purity Coatings for Semiconductor Equipment Parts Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

High Purity Coatings for Semiconductor Equipment Parts REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global High Purity Coatings for Semiconductor Equipment Parts Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Semiconductor Etch Equipment

- 5.1.2. Deposition (CVD, PVD, ALD)

- 5.1.3. Ion Implant Equipment

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Plasma Spray Coating

- 5.2.2. Arc Spray Coating

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America High Purity Coatings for Semiconductor Equipment Parts Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Semiconductor Etch Equipment

- 6.1.2. Deposition (CVD, PVD, ALD)

- 6.1.3. Ion Implant Equipment

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Plasma Spray Coating

- 6.2.2. Arc Spray Coating

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America High Purity Coatings for Semiconductor Equipment Parts Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Semiconductor Etch Equipment

- 7.1.2. Deposition (CVD, PVD, ALD)

- 7.1.3. Ion Implant Equipment

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Plasma Spray Coating

- 7.2.2. Arc Spray Coating

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe High Purity Coatings for Semiconductor Equipment Parts Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Semiconductor Etch Equipment

- 8.1.2. Deposition (CVD, PVD, ALD)

- 8.1.3. Ion Implant Equipment

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Plasma Spray Coating

- 8.2.2. Arc Spray Coating

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa High Purity Coatings for Semiconductor Equipment Parts Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Semiconductor Etch Equipment

- 9.1.2. Deposition (CVD, PVD, ALD)

- 9.1.3. Ion Implant Equipment

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Plasma Spray Coating

- 9.2.2. Arc Spray Coating

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific High Purity Coatings for Semiconductor Equipment Parts Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Semiconductor Etch Equipment

- 10.1.2. Deposition (CVD, PVD, ALD)

- 10.1.3. Ion Implant Equipment

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Plasma Spray Coating

- 10.2.2. Arc Spray Coating

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Entegris

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Beneq

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Saint-Gobain

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 UCT (Ultra Clean Holdings

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Inc)

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Fiti Group

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 SK enpulse

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 APS Materials

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Inc.

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 SilcoTek

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Aluminum Electroplating Company

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Alcadyne

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 ASSET Solutions

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Inc.

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 KoMiCo

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 NGK (NTK CERATE)

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Toshiba Materials

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Hansol IONES

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 YMC Co.

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Ltd.

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 FEMVIX

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 SEWON HARDFACING CO.

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 LTD

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 CINOS

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.25 Oerlikon Balzers

- 11.2.25.1. Overview

- 11.2.25.2. Products

- 11.2.25.3. SWOT Analysis

- 11.2.25.4. Recent Developments

- 11.2.25.5. Financials (Based on Availability)

- 11.2.26 Yeedex

- 11.2.26.1. Overview

- 11.2.26.2. Products

- 11.2.26.3. SWOT Analysis

- 11.2.26.4. Recent Developments

- 11.2.26.5. Financials (Based on Availability)

- 11.2.1 Entegris

List of Figures

- Figure 1: Global High Purity Coatings for Semiconductor Equipment Parts Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America High Purity Coatings for Semiconductor Equipment Parts Revenue (million), by Application 2024 & 2032

- Figure 3: North America High Purity Coatings for Semiconductor Equipment Parts Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America High Purity Coatings for Semiconductor Equipment Parts Revenue (million), by Types 2024 & 2032

- Figure 5: North America High Purity Coatings for Semiconductor Equipment Parts Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America High Purity Coatings for Semiconductor Equipment Parts Revenue (million), by Country 2024 & 2032

- Figure 7: North America High Purity Coatings for Semiconductor Equipment Parts Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America High Purity Coatings for Semiconductor Equipment Parts Revenue (million), by Application 2024 & 2032

- Figure 9: South America High Purity Coatings for Semiconductor Equipment Parts Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America High Purity Coatings for Semiconductor Equipment Parts Revenue (million), by Types 2024 & 2032

- Figure 11: South America High Purity Coatings for Semiconductor Equipment Parts Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America High Purity Coatings for Semiconductor Equipment Parts Revenue (million), by Country 2024 & 2032

- Figure 13: South America High Purity Coatings for Semiconductor Equipment Parts Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe High Purity Coatings for Semiconductor Equipment Parts Revenue (million), by Application 2024 & 2032

- Figure 15: Europe High Purity Coatings for Semiconductor Equipment Parts Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe High Purity Coatings for Semiconductor Equipment Parts Revenue (million), by Types 2024 & 2032

- Figure 17: Europe High Purity Coatings for Semiconductor Equipment Parts Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe High Purity Coatings for Semiconductor Equipment Parts Revenue (million), by Country 2024 & 2032

- Figure 19: Europe High Purity Coatings for Semiconductor Equipment Parts Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa High Purity Coatings for Semiconductor Equipment Parts Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa High Purity Coatings for Semiconductor Equipment Parts Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa High Purity Coatings for Semiconductor Equipment Parts Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa High Purity Coatings for Semiconductor Equipment Parts Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa High Purity Coatings for Semiconductor Equipment Parts Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa High Purity Coatings for Semiconductor Equipment Parts Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific High Purity Coatings for Semiconductor Equipment Parts Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific High Purity Coatings for Semiconductor Equipment Parts Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific High Purity Coatings for Semiconductor Equipment Parts Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific High Purity Coatings for Semiconductor Equipment Parts Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific High Purity Coatings for Semiconductor Equipment Parts Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific High Purity Coatings for Semiconductor Equipment Parts Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global High Purity Coatings for Semiconductor Equipment Parts Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global High Purity Coatings for Semiconductor Equipment Parts Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global High Purity Coatings for Semiconductor Equipment Parts Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global High Purity Coatings for Semiconductor Equipment Parts Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global High Purity Coatings for Semiconductor Equipment Parts Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global High Purity Coatings for Semiconductor Equipment Parts Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global High Purity Coatings for Semiconductor Equipment Parts Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States High Purity Coatings for Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada High Purity Coatings for Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico High Purity Coatings for Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global High Purity Coatings for Semiconductor Equipment Parts Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global High Purity Coatings for Semiconductor Equipment Parts Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global High Purity Coatings for Semiconductor Equipment Parts Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil High Purity Coatings for Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina High Purity Coatings for Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America High Purity Coatings for Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global High Purity Coatings for Semiconductor Equipment Parts Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global High Purity Coatings for Semiconductor Equipment Parts Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global High Purity Coatings for Semiconductor Equipment Parts Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom High Purity Coatings for Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany High Purity Coatings for Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France High Purity Coatings for Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy High Purity Coatings for Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain High Purity Coatings for Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia High Purity Coatings for Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux High Purity Coatings for Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics High Purity Coatings for Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe High Purity Coatings for Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global High Purity Coatings for Semiconductor Equipment Parts Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global High Purity Coatings for Semiconductor Equipment Parts Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global High Purity Coatings for Semiconductor Equipment Parts Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey High Purity Coatings for Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel High Purity Coatings for Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC High Purity Coatings for Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa High Purity Coatings for Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa High Purity Coatings for Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa High Purity Coatings for Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global High Purity Coatings for Semiconductor Equipment Parts Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global High Purity Coatings for Semiconductor Equipment Parts Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global High Purity Coatings for Semiconductor Equipment Parts Revenue million Forecast, by Country 2019 & 2032

- Table 41: China High Purity Coatings for Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India High Purity Coatings for Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan High Purity Coatings for Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea High Purity Coatings for Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN High Purity Coatings for Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania High Purity Coatings for Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific High Purity Coatings for Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the High Purity Coatings for Semiconductor Equipment Parts?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the High Purity Coatings for Semiconductor Equipment Parts?

Key companies in the market include Entegris, Beneq, Saint-Gobain, UCT (Ultra Clean Holdings, Inc), Fiti Group, SK enpulse, APS Materials, Inc., SilcoTek, Aluminum Electroplating Company, Alcadyne, ASSET Solutions, Inc., KoMiCo, NGK (NTK CERATE), Toshiba Materials, Hansol IONES, YMC Co., Ltd., FEMVIX, SEWON HARDFACING CO., LTD, CINOS, Oerlikon Balzers, Yeedex.

3. What are the main segments of the High Purity Coatings for Semiconductor Equipment Parts?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4350.00, USD 6525.00, and USD 8700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "High Purity Coatings for Semiconductor Equipment Parts," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the High Purity Coatings for Semiconductor Equipment Parts report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the High Purity Coatings for Semiconductor Equipment Parts?

To stay informed about further developments, trends, and reports in the High Purity Coatings for Semiconductor Equipment Parts, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence