Key Insights

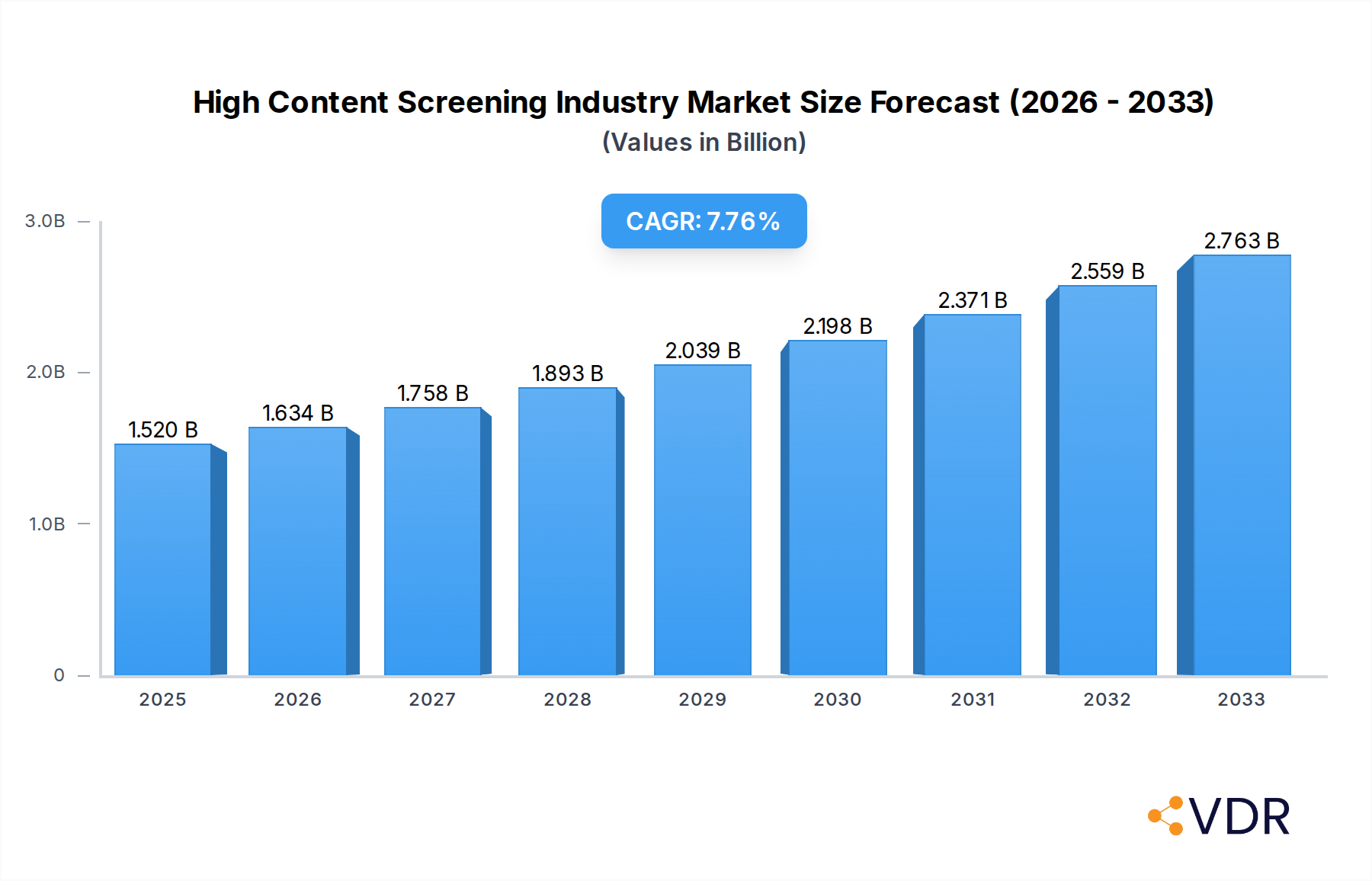

The High Content Screening (HCS) industry is poised for significant expansion, with a projected market size of USD 1.52 billion in 2025, driven by an impressive Compound Annual Growth Rate (CAGR) of 7.5% through 2033. This robust growth is propelled by the escalating demand for efficient drug discovery and development processes within pharmaceutical and biotechnology sectors. Key drivers include advancements in cell imaging and analysis technologies, alongside the increasing adoption of automation and sophisticated data analysis software, which are crucial for identifying potential drug candidates and understanding their efficacy and safety profiles. The industry's expansion is further fueled by a growing emphasis on personalized medicine and the need to screen vast libraries of compounds for novel therapeutic targets. Innovations in reagents and assay kits, coupled with the development of advanced microplates, are enhancing the precision and throughput of HCS platforms.

High Content Screening Industry Market Size (In Billion)

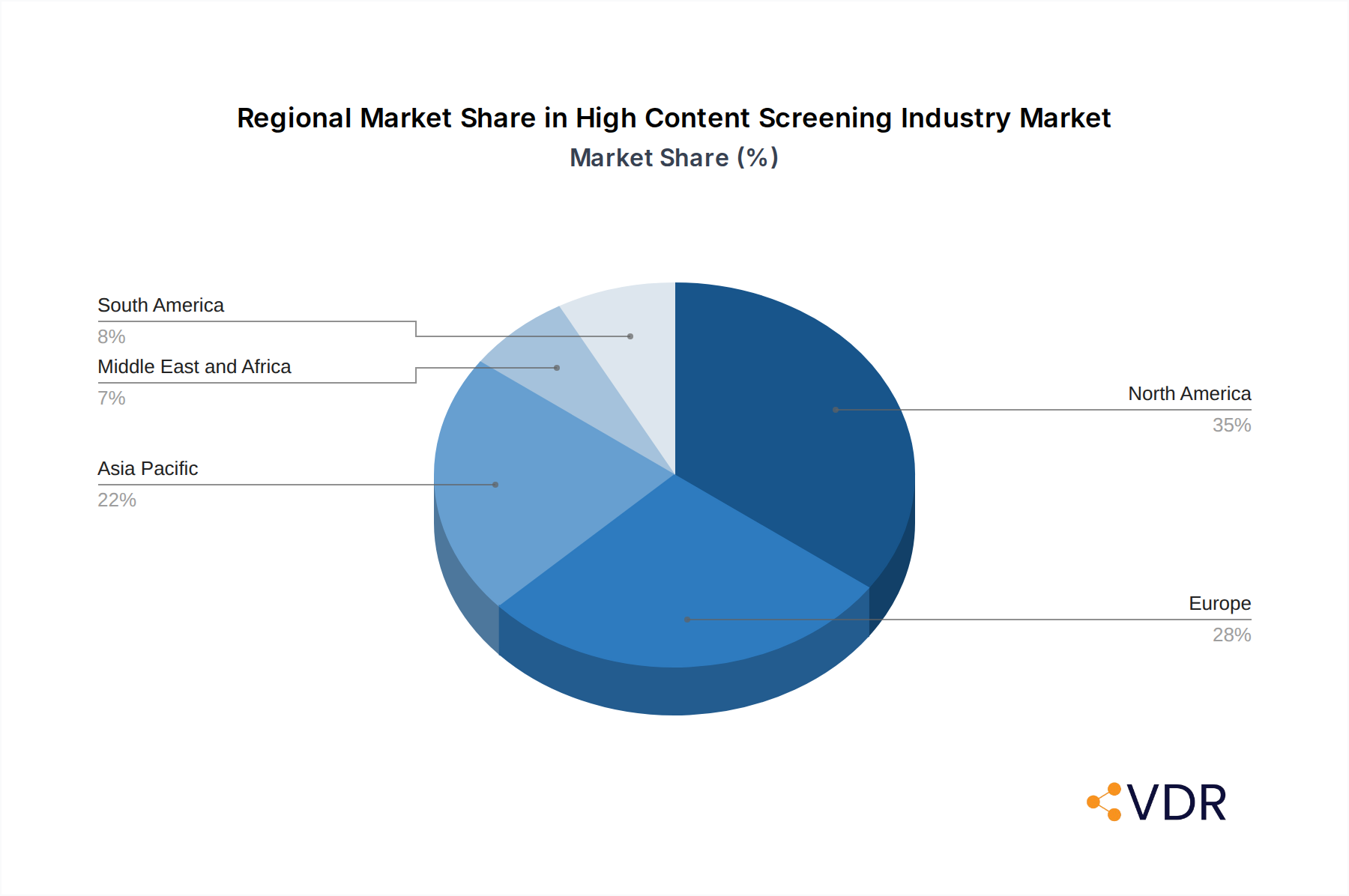

The market is segmented across product types, including instruments like cell imaging and analysis systems and flow cytometers, as well as consumables such as reagents, assay kits, and microplates. Software and services also represent vital components of the HCS ecosystem. Applications are diverse, ranging from primary and secondary screening and target identification to toxicity studies and compound profiling, all of which are critical stages in bringing new pharmaceuticals to market. Pharmaceutical and biotechnology companies, academic and government institutions, and contract research organizations are the primary end-users, actively investing in HCS solutions. Geographically, North America currently leads the market, with strong growth anticipated in the Asia Pacific region, particularly in China and India, owing to increasing R&D investments and a burgeoning life sciences industry. Restraints such as high initial investment costs for sophisticated HCS systems and the need for specialized expertise are being mitigated by the development of more accessible solutions and cloud-based data analysis platforms.

High Content Screening Industry Company Market Share

High Content Screening Industry Report: Market Analysis, Trends, and Forecast 2019–2033

This comprehensive report delves into the dynamic High Content Screening (HCS) industry, providing in-depth analysis of market size, growth drivers, key trends, and competitive landscape. It forecasts market evolution from 2019 to 2033, with a base year of 2025, offering actionable insights for stakeholders. Explore the parent market's influence and child market segments' growth potential, supported by robust quantitative data and expert qualitative analysis.

High Content Screening Industry Market Dynamics & Structure

The High Content Screening (HCS) market is characterized by moderate to high concentration, driven by a few dominant players and a growing number of specialized firms. Technological innovation remains a primary driver, with advancements in microscopy, automation, and data analysis continuously pushing the boundaries of HCS capabilities. Regulatory frameworks, particularly concerning drug discovery and development, indirectly shape market growth by setting standards for efficacy and safety testing. Competitive substitutes, while present in individual assay types, struggle to replicate the comprehensive, multi-parametric analysis offered by HCS platforms. End-user demographics are shifting towards a greater reliance on HCS in pharmaceutical and biotechnology companies for early-stage drug discovery and in academic research for complex biological investigations. Mergers and acquisitions (M&A) are significant, consolidating market share and expanding portfolios of key companies.

- Market Concentration: Dominated by established players, but with increasing fragmentation due to specialized technology providers.

- Technological Innovation: Continuous advancements in imaging resolution, automation, and AI-powered data interpretation.

- Regulatory Influence: Stringent drug discovery pipelines necessitate advanced screening technologies like HCS.

- End-User Demographics: Growing demand from pharmaceutical, biotech, and academic sectors for efficient drug discovery and biological research.

- M&A Trends: Strategic acquisitions aimed at portfolio expansion and market consolidation are prevalent.

High Content Screening Industry Growth Trends & Insights

The High Content Screening (HCS) industry is poised for substantial growth, projected to expand significantly over the forecast period. The market size is evolving rapidly, driven by increasing adoption rates in drug discovery and development pipelines across the pharmaceutical and biotechnology sectors. Technological disruptions, such as the integration of artificial intelligence (AI) and machine learning (ML) for advanced data analysis and interpretation, are revolutionizing HCS workflows. Furthermore, shifts in consumer behavior, including a greater emphasis on personalized medicine and the need for faster identification of novel drug targets, are fueling demand for sophisticated screening solutions. The increasing complexity of biological targets and the drive to reduce the attrition rate in drug development are also key factors contributing to the market's upward trajectory. The CAGR for the HCS market is estimated at XX% between 2025 and 2033. Market penetration is steadily increasing as more research institutions and companies recognize the value proposition of HCS in accelerating R&D timelines and improving the accuracy of experimental outcomes. This growth is further bolstered by the increasing prevalence of chronic diseases and the continuous pursuit of novel therapeutic interventions, creating a sustained demand for advanced screening technologies. The integration of HCS with other omics technologies is also opening new avenues for comprehensive biological understanding and drug discovery.

Dominant Regions, Countries, or Segments in High Content Screening Industry

North America, particularly the United States, consistently emerges as the dominant region in the High Content Screening (HCS) industry. This leadership is attributed to a robust pharmaceutical and biotechnology ecosystem, significant government funding for life sciences research, and a high concentration of leading academic and research institutions. The region's advanced healthcare infrastructure and proactive adoption of cutting-edge technologies further solidify its dominance.

Key Drivers in North America:

- Strong Pharmaceutical and Biotechnology Hubs: Presence of major drug development companies and a thriving startup scene.

- Government Funding and Initiatives: Substantial investment in life sciences research through agencies like the National Institutes of Health (NIH).

- Technological Adoption: Early and widespread adoption of advanced HCS instruments and software.

- Skilled Workforce: Availability of highly trained scientists and researchers proficient in HCS methodologies.

Among the segments, Instruments are the primary revenue generators, with Cell Imaging and Analysis Systems holding the largest market share. This is directly linked to the core function of HCS – visualizing and quantifying cellular responses. Within instruments, the growing sophistication and decreasing cost of high-resolution imaging systems are key contributors.

Product Segment Dominance (Instruments):

- Cell Imaging and Analysis Systems: Essential for multi-parametric cellular analysis, driving significant market share.

- Flow Cytometers: Increasingly integrated with HCS for high-throughput cellular analysis and phenotyping.

In terms of Application, Primary and Secondary Screening remains the most dominant application, as HCS platforms are pivotal in the initial stages of drug discovery to identify and validate potential drug candidates. The efficiency and comprehensive data generated by HCS in these phases are invaluable for pharmaceutical companies.

Application Segment Dominance:

- Primary and Secondary Screening: Critical for identifying and validating early-stage drug candidates due to the high-throughput and multi-parametric nature of HCS.

- Target Identification and Validation: HCS plays a crucial role in understanding disease mechanisms and identifying novel therapeutic targets.

The End User segment is predominantly led by Pharmaceutical and Biotechnology Companies. Their extensive R&D budgets and the inherent need for efficient and accurate drug discovery processes make them the largest consumers of HCS solutions.

End User Segment Dominance:

- Pharmaceutical and Biotechnology Companies: The largest end-user segment, driven by extensive R&D investment and the need for accelerated drug discovery.

- Academic and Government Institutions: Significant contributors, focusing on basic research and understanding complex biological processes.

High Content Screening Industry Product Landscape

The High Content Screening (HCS) product landscape is characterized by continuous innovation, focusing on enhancing resolution, throughput, and data analysis capabilities. Key product categories include sophisticated Instruments like advanced cell imaging and analysis systems and integrated flow cytometers, alongside essential Consumables such as specialized reagents, assay kits, and microplates. The development of intuitive Software for data management and AI-powered analysis is also a critical component, streamlining complex workflows. These products are crucial for applications ranging from Primary and Secondary Screening to Toxicity Studies and Target Identification, ultimately enabling pharmaceutical and biotechnology companies, as well as academic institutions, to accelerate drug discovery and biological research with unprecedented detail and efficiency.

Key Drivers, Barriers & Challenges in High Content Screening Industry

Key Drivers:

The High Content Screening (HCS) market is propelled by several key drivers. The relentless pursuit of novel therapeutics for unmet medical needs fuels the demand for advanced drug discovery tools. Technological advancements in imaging, automation, and artificial intelligence are constantly improving HCS capabilities, enabling deeper biological insights and faster screening cycles. Increased investment in life sciences research by governments and private organizations, coupled with the growing prevalence of chronic diseases, creates a sustained need for efficient screening platforms. The drive to reduce the cost and time associated with drug development also significantly boosts the adoption of HCS.

- Demand for Novel Therapeutics: Growing need for new drugs to combat diseases.

- Technological Advancements: Innovations in imaging, automation, and AI.

- Increased R&D Investment: Higher funding in life sciences globally.

- Disease Prevalence: Rising incidence of chronic diseases.

Barriers & Challenges:

Despite its growth, the HCS market faces several barriers and challenges. The high initial cost of advanced HCS instrumentation can be a significant deterrent for smaller research institutions and emerging companies. The complexity of data generated by HCS requires specialized bioinformatics expertise for effective analysis, creating a talent gap. Stringent regulatory requirements for drug approval can lead to extended validation periods for HCS-derived data. Furthermore, the competitive landscape, with numerous providers offering overlapping functionalities, can lead to pricing pressures. Supply chain disruptions for specialized reagents and consumables can also impact research continuity.

- High Instrument Costs: Significant upfront investment required.

- Data Analysis Complexity: Need for specialized bioinformatics skills.

- Regulatory Hurdles: Challenges in meeting stringent drug approval requirements.

- Intense Competition: Pricing pressures and market fragmentation.

- Supply Chain Vulnerabilities: Potential disruptions for specialized components.

Emerging Opportunities in High Content Screening Industry

Emerging opportunities in the High Content Screening (HCS) industry lie in the expansion into novel applications, such as predictive toxicology and the study of rare diseases. The integration of HCS with single-cell multi-omics technologies presents a significant avenue for deeper biological understanding and personalized medicine approaches. Furthermore, the development of more user-friendly, cloud-based HCS platforms and AI-driven data interpretation tools can broaden market accessibility and accelerate insights for a wider range of researchers. Untapped markets in emerging economies and the increasing demand for contract research organization (CRO) services in drug discovery also offer substantial growth potential.

Growth Accelerators in the High Content Screening Industry Industry

Long-term growth in the High Content Screening (HCS) industry is being accelerated by several key catalysts. Breakthroughs in AI and machine learning are enabling more sophisticated image analysis, predictive modeling, and automation of experimental workflows, significantly enhancing the efficiency and scope of HCS. Strategic partnerships between instrument manufacturers, reagent suppliers, and software developers are leading to integrated solutions that offer seamless user experiences and expanded capabilities. Market expansion strategies, including the development of modular and scalable HCS systems, are making advanced screening technologies more accessible to a broader range of research organizations, thus driving broader adoption and fostering innovation.

Key Players Shaping the High Content Screening Industry Market

- Bio-Rad Laboratories Inc

- Perkinelmer Inc

- BD (Becton Dickinson and Company)

- Thermo Fisher Scientific Inc

- Danaher Corporation

- Merck KGaA

- Yokogawa Electric Corporation

- Agilent Technologies

Notable Milestones in High Content Screening Industry Sector

- September 2022: BD (Becton, Dickinson and Company) launched BD Research Cloud, a cloud-based software solution designed to streamline the flow cytometry workflow. Its goal is to simplify the workflow for scientists working in a variety of fields, such as immunology, virology, oncology, and infectious disease monitoring, to enable higher-quality experiments with quicker time to insight.

- April 2022: Sysmex Europe launched CE-IVD-marked Flow Cytometer XF-1600, offering clinical flow cytometry laboratories robust and reliable immunophenotyping.

In-Depth High Content Screening Industry Market Outlook

The High Content Screening (HCS) market outlook is exceptionally bright, driven by a convergence of accelerating forces. The increasing complexity of biological research and the unwavering demand for novel pharmaceuticals are creating sustained growth opportunities. Advancements in AI-powered data analytics and automation are not only enhancing the precision of HCS but also democratizing access to these powerful tools. Strategic collaborations and the development of integrated platforms are poised to streamline workflows and deliver more comprehensive insights. The market is also benefiting from the growing adoption of HCS in emerging areas like personalized medicine and predictive toxicology. This dynamic evolution positions the HCS industry as a cornerstone of future biomedical innovation and drug discovery.

High Content Screening Industry Segmentation

-

1. Product

-

1.1. Instruments

- 1.1.1. Cell Imaging and Analysis Systems

- 1.1.2. Flow Cytometers

-

1.2. Consumables

- 1.2.1. Reagents and Assay Kits

- 1.2.2. Microplates

- 1.2.3. Other Consumables

- 1.3. Software

- 1.4. Services

-

1.1. Instruments

-

2. Application

- 2.1. Primary and Secondary Screening

- 2.2. Target Identification and Validation

- 2.3. Toxicity Studies

- 2.4. Compound Profiling

- 2.5. Other Applications

-

3. End User

- 3.1. Pharmaceutical and Biotechnology Companies

- 3.2. Academic and Government Institutions

- 3.3. Contract Research Organization

High Content Screening Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

High Content Screening Industry Regional Market Share

Geographic Coverage of High Content Screening Industry

High Content Screening Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Instruments

- 5.1.1.1. Cell Imaging and Analysis Systems

- 5.1.1.2. Flow Cytometers

- 5.1.2. Consumables

- 5.1.2.1. Reagents and Assay Kits

- 5.1.2.2. Microplates

- 5.1.2.3. Other Consumables

- 5.1.3. Software

- 5.1.4. Services

- 5.1.1. Instruments

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Primary and Secondary Screening

- 5.2.2. Target Identification and Validation

- 5.2.3. Toxicity Studies

- 5.2.4. Compound Profiling

- 5.2.5. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Pharmaceutical and Biotechnology Companies

- 5.3.2. Academic and Government Institutions

- 5.3.3. Contract Research Organization

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Middle East and Africa

- 5.4.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. Global High Content Screening Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Instruments

- 6.1.1.1. Cell Imaging and Analysis Systems

- 6.1.1.2. Flow Cytometers

- 6.1.2. Consumables

- 6.1.2.1. Reagents and Assay Kits

- 6.1.2.2. Microplates

- 6.1.2.3. Other Consumables

- 6.1.3. Software

- 6.1.4. Services

- 6.1.1. Instruments

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Primary and Secondary Screening

- 6.2.2. Target Identification and Validation

- 6.2.3. Toxicity Studies

- 6.2.4. Compound Profiling

- 6.2.5. Other Applications

- 6.3. Market Analysis, Insights and Forecast - by End User

- 6.3.1. Pharmaceutical and Biotechnology Companies

- 6.3.2. Academic and Government Institutions

- 6.3.3. Contract Research Organization

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. North America High Content Screening Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Product

- 7.1.1. Instruments

- 7.1.1.1. Cell Imaging and Analysis Systems

- 7.1.1.2. Flow Cytometers

- 7.1.2. Consumables

- 7.1.2.1. Reagents and Assay Kits

- 7.1.2.2. Microplates

- 7.1.2.3. Other Consumables

- 7.1.3. Software

- 7.1.4. Services

- 7.1.1. Instruments

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Primary and Secondary Screening

- 7.2.2. Target Identification and Validation

- 7.2.3. Toxicity Studies

- 7.2.4. Compound Profiling

- 7.2.5. Other Applications

- 7.3. Market Analysis, Insights and Forecast - by End User

- 7.3.1. Pharmaceutical and Biotechnology Companies

- 7.3.2. Academic and Government Institutions

- 7.3.3. Contract Research Organization

- 7.1. Market Analysis, Insights and Forecast - by Product

- 8. Europe High Content Screening Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Product

- 8.1.1. Instruments

- 8.1.1.1. Cell Imaging and Analysis Systems

- 8.1.1.2. Flow Cytometers

- 8.1.2. Consumables

- 8.1.2.1. Reagents and Assay Kits

- 8.1.2.2. Microplates

- 8.1.2.3. Other Consumables

- 8.1.3. Software

- 8.1.4. Services

- 8.1.1. Instruments

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Primary and Secondary Screening

- 8.2.2. Target Identification and Validation

- 8.2.3. Toxicity Studies

- 8.2.4. Compound Profiling

- 8.2.5. Other Applications

- 8.3. Market Analysis, Insights and Forecast - by End User

- 8.3.1. Pharmaceutical and Biotechnology Companies

- 8.3.2. Academic and Government Institutions

- 8.3.3. Contract Research Organization

- 8.1. Market Analysis, Insights and Forecast - by Product

- 9. Asia Pacific High Content Screening Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Product

- 9.1.1. Instruments

- 9.1.1.1. Cell Imaging and Analysis Systems

- 9.1.1.2. Flow Cytometers

- 9.1.2. Consumables

- 9.1.2.1. Reagents and Assay Kits

- 9.1.2.2. Microplates

- 9.1.2.3. Other Consumables

- 9.1.3. Software

- 9.1.4. Services

- 9.1.1. Instruments

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Primary and Secondary Screening

- 9.2.2. Target Identification and Validation

- 9.2.3. Toxicity Studies

- 9.2.4. Compound Profiling

- 9.2.5. Other Applications

- 9.3. Market Analysis, Insights and Forecast - by End User

- 9.3.1. Pharmaceutical and Biotechnology Companies

- 9.3.2. Academic and Government Institutions

- 9.3.3. Contract Research Organization

- 9.1. Market Analysis, Insights and Forecast - by Product

- 10. Middle East and Africa High Content Screening Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Product

- 10.1.1. Instruments

- 10.1.1.1. Cell Imaging and Analysis Systems

- 10.1.1.2. Flow Cytometers

- 10.1.2. Consumables

- 10.1.2.1. Reagents and Assay Kits

- 10.1.2.2. Microplates

- 10.1.2.3. Other Consumables

- 10.1.3. Software

- 10.1.4. Services

- 10.1.1. Instruments

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Primary and Secondary Screening

- 10.2.2. Target Identification and Validation

- 10.2.3. Toxicity Studies

- 10.2.4. Compound Profiling

- 10.2.5. Other Applications

- 10.3. Market Analysis, Insights and Forecast - by End User

- 10.3.1. Pharmaceutical and Biotechnology Companies

- 10.3.2. Academic and Government Institutions

- 10.3.3. Contract Research Organization

- 10.1. Market Analysis, Insights and Forecast - by Product

- 11. South America High Content Screening Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Product

- 11.1.1. Instruments

- 11.1.1.1. Cell Imaging and Analysis Systems

- 11.1.1.2. Flow Cytometers

- 11.1.2. Consumables

- 11.1.2.1. Reagents and Assay Kits

- 11.1.2.2. Microplates

- 11.1.2.3. Other Consumables

- 11.1.3. Software

- 11.1.4. Services

- 11.1.1. Instruments

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Primary and Secondary Screening

- 11.2.2. Target Identification and Validation

- 11.2.3. Toxicity Studies

- 11.2.4. Compound Profiling

- 11.2.5. Other Applications

- 11.3. Market Analysis, Insights and Forecast - by End User

- 11.3.1. Pharmaceutical and Biotechnology Companies

- 11.3.2. Academic and Government Institutions

- 11.3.3. Contract Research Organization

- 11.1. Market Analysis, Insights and Forecast - by Product

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Bio-Rad Laboratories Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Perkinelmer Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 BD (Becton Dickinson and Company)

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Thermo Fisher Scientific Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Danaher Corporation

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Merck KGaA

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Yokogawa Electric Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Agilent Technologies

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.1 Bio-Rad Laboratories Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global High Content Screening Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America High Content Screening Industry Revenue (billion), by Product 2025 & 2033

- Figure 3: North America High Content Screening Industry Revenue Share (%), by Product 2025 & 2033

- Figure 4: North America High Content Screening Industry Revenue (billion), by Application 2025 & 2033

- Figure 5: North America High Content Screening Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America High Content Screening Industry Revenue (billion), by End User 2025 & 2033

- Figure 7: North America High Content Screening Industry Revenue Share (%), by End User 2025 & 2033

- Figure 8: North America High Content Screening Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: North America High Content Screening Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe High Content Screening Industry Revenue (billion), by Product 2025 & 2033

- Figure 11: Europe High Content Screening Industry Revenue Share (%), by Product 2025 & 2033

- Figure 12: Europe High Content Screening Industry Revenue (billion), by Application 2025 & 2033

- Figure 13: Europe High Content Screening Industry Revenue Share (%), by Application 2025 & 2033

- Figure 14: Europe High Content Screening Industry Revenue (billion), by End User 2025 & 2033

- Figure 15: Europe High Content Screening Industry Revenue Share (%), by End User 2025 & 2033

- Figure 16: Europe High Content Screening Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: Europe High Content Screening Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific High Content Screening Industry Revenue (billion), by Product 2025 & 2033

- Figure 19: Asia Pacific High Content Screening Industry Revenue Share (%), by Product 2025 & 2033

- Figure 20: Asia Pacific High Content Screening Industry Revenue (billion), by Application 2025 & 2033

- Figure 21: Asia Pacific High Content Screening Industry Revenue Share (%), by Application 2025 & 2033

- Figure 22: Asia Pacific High Content Screening Industry Revenue (billion), by End User 2025 & 2033

- Figure 23: Asia Pacific High Content Screening Industry Revenue Share (%), by End User 2025 & 2033

- Figure 24: Asia Pacific High Content Screening Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Asia Pacific High Content Screening Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa High Content Screening Industry Revenue (billion), by Product 2025 & 2033

- Figure 27: Middle East and Africa High Content Screening Industry Revenue Share (%), by Product 2025 & 2033

- Figure 28: Middle East and Africa High Content Screening Industry Revenue (billion), by Application 2025 & 2033

- Figure 29: Middle East and Africa High Content Screening Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Middle East and Africa High Content Screening Industry Revenue (billion), by End User 2025 & 2033

- Figure 31: Middle East and Africa High Content Screening Industry Revenue Share (%), by End User 2025 & 2033

- Figure 32: Middle East and Africa High Content Screening Industry Revenue (billion), by Country 2025 & 2033

- Figure 33: Middle East and Africa High Content Screening Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: South America High Content Screening Industry Revenue (billion), by Product 2025 & 2033

- Figure 35: South America High Content Screening Industry Revenue Share (%), by Product 2025 & 2033

- Figure 36: South America High Content Screening Industry Revenue (billion), by Application 2025 & 2033

- Figure 37: South America High Content Screening Industry Revenue Share (%), by Application 2025 & 2033

- Figure 38: South America High Content Screening Industry Revenue (billion), by End User 2025 & 2033

- Figure 39: South America High Content Screening Industry Revenue Share (%), by End User 2025 & 2033

- Figure 40: South America High Content Screening Industry Revenue (billion), by Country 2025 & 2033

- Figure 41: South America High Content Screening Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global High Content Screening Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 2: Global High Content Screening Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 3: Global High Content Screening Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 4: Global High Content Screening Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Global High Content Screening Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 6: Global High Content Screening Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 7: Global High Content Screening Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 8: Global High Content Screening Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: United States High Content Screening Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Canada High Content Screening Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Mexico High Content Screening Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Global High Content Screening Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 13: Global High Content Screening Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 14: Global High Content Screening Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 15: Global High Content Screening Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Germany High Content Screening Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: United Kingdom High Content Screening Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: France High Content Screening Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Italy High Content Screening Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Spain High Content Screening Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Rest of Europe High Content Screening Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Global High Content Screening Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 23: Global High Content Screening Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 24: Global High Content Screening Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 25: Global High Content Screening Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 26: China High Content Screening Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Japan High Content Screening Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: India High Content Screening Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: Australia High Content Screening Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: South Korea High Content Screening Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Rest of Asia Pacific High Content Screening Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Global High Content Screening Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 33: Global High Content Screening Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 34: Global High Content Screening Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 35: Global High Content Screening Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 36: GCC High Content Screening Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: South Africa High Content Screening Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Rest of Middle East and Africa High Content Screening Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: Global High Content Screening Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 40: Global High Content Screening Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 41: Global High Content Screening Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 42: Global High Content Screening Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 43: Brazil High Content Screening Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Argentina High Content Screening Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Rest of South America High Content Screening Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the High Content Screening Industry?

The projected CAGR is approximately 7.5%.

2. Which companies are prominent players in the High Content Screening Industry?

Key companies in the market include Bio-Rad Laboratories Inc, Perkinelmer Inc, BD (Becton Dickinson and Company), Thermo Fisher Scientific Inc, Danaher Corporation, Merck KGaA, Yokogawa Electric Corporation, Agilent Technologies.

3. What are the main segments of the High Content Screening Industry?

The market segments include Product, Application, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.52 billion as of 2022.

5. What are some drivers contributing to market growth?

Government Funding and Venture Capital Investments Across Developed Markets; Increasing Applications of High Content Screening in Life Science Research; Advancements in Informatic Solutions and Imaging Systems.

6. What are the notable trends driving market growth?

Flow Cytometry is Expected to Hold a Significant Market Share Over The Forecast Period.

7. Are there any restraints impacting market growth?

Lower Adoption of High Content Screening Instruments Due to Their High Prices.

8. Can you provide examples of recent developments in the market?

September 2022: BD (Becton, Dickinson and Company) launched BD Research Cloud, a cloud-based software solution designed to streamline the flow cytometry workflow. Its goal is to simplify the workflow for scientists working in a variety of fields, such as immunology, virology, oncology, and infectious disease monitoring, to enable higher-quality experiments with quicker time to insight.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "High Content Screening Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the High Content Screening Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the High Content Screening Industry?

To stay informed about further developments, trends, and reports in the High Content Screening Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence