Key Insights

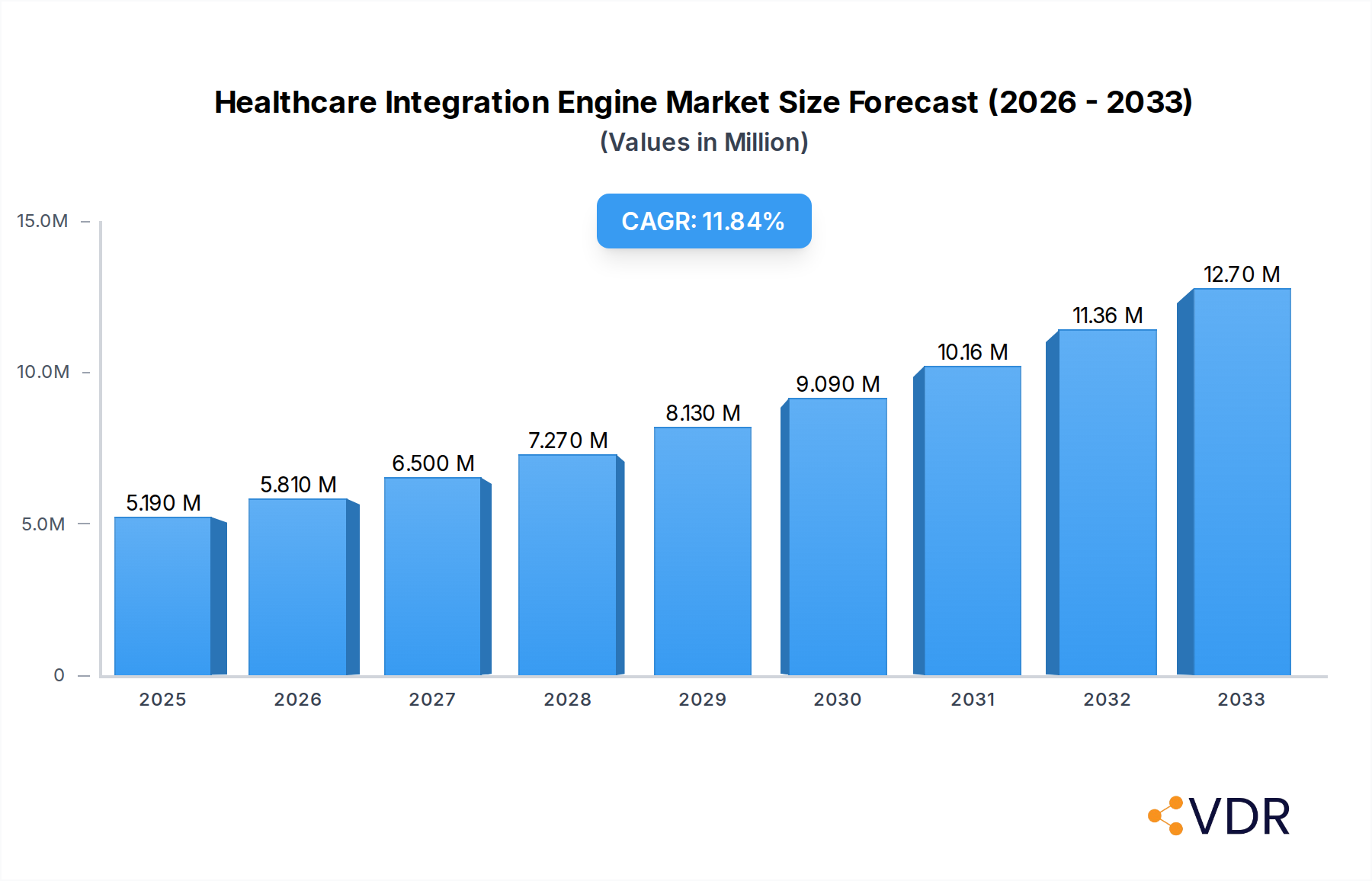

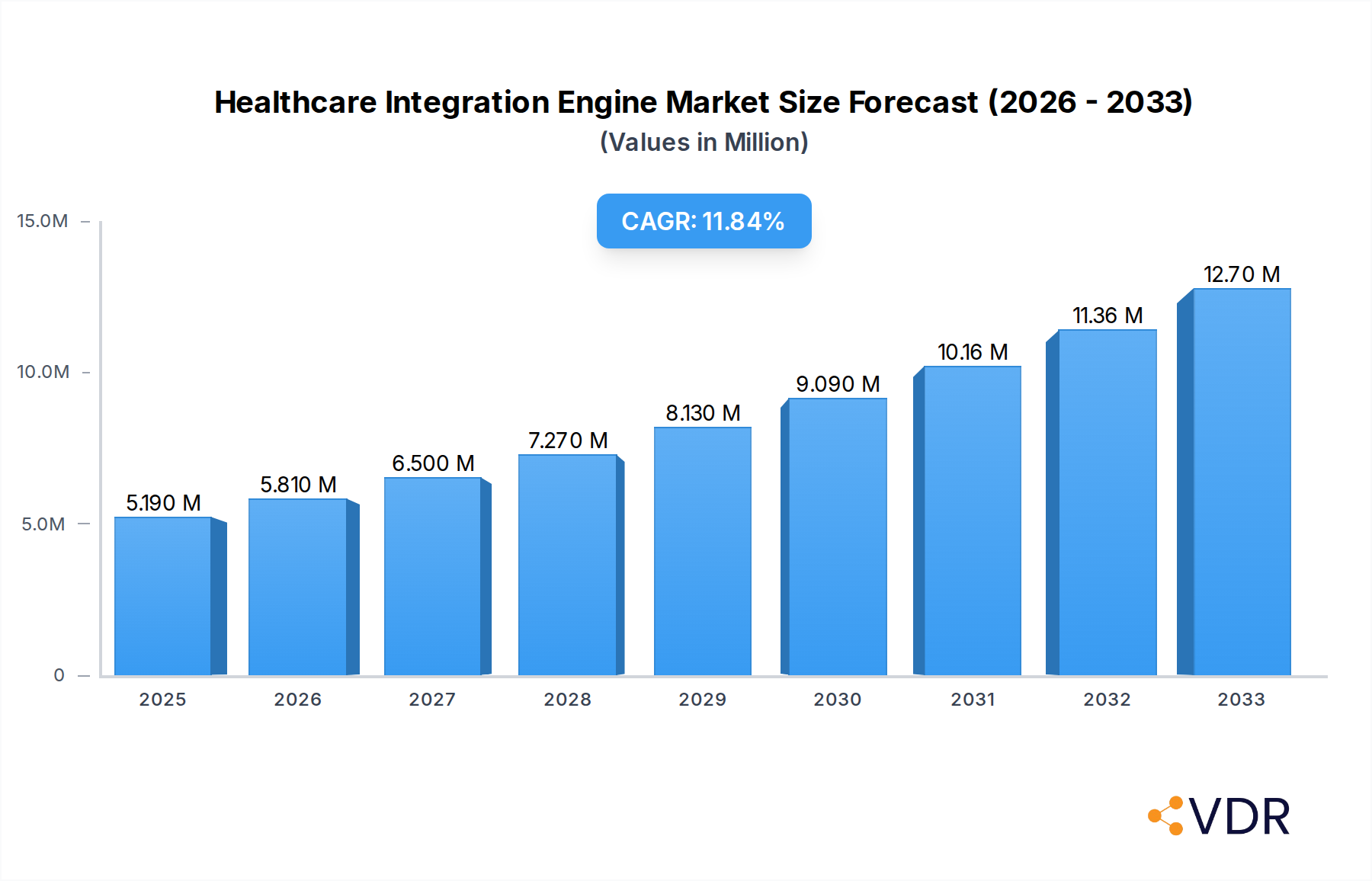

The Healthcare Integration Engine Market is poised for significant expansion, with a projected market size of $5.19 Million in 2025, growing at a robust Compound Annual Growth Rate (CAGR) of 11.85% throughout the forecast period of 2025-2033. This substantial growth is primarily fueled by the escalating need for seamless data exchange and interoperability across disparate healthcare systems. The increasing adoption of Electronic Health Records (EHRs), the proliferation of connected medical devices, and the growing demand for advanced analytics in patient care are key drivers propelling market expansion. Furthermore, the imperative to comply with stringent healthcare regulations, such as HIPAA, and the pursuit of improved operational efficiencies within healthcare organizations are also contributing to the demand for sophisticated integration engines. The market's trajectory indicates a strong shift towards platforms that can effectively manage complex data flows, ensuring data security, accuracy, and accessibility for enhanced clinical decision-making and patient outcomes.

Healthcare Integration Engine Market Market Size (In Million)

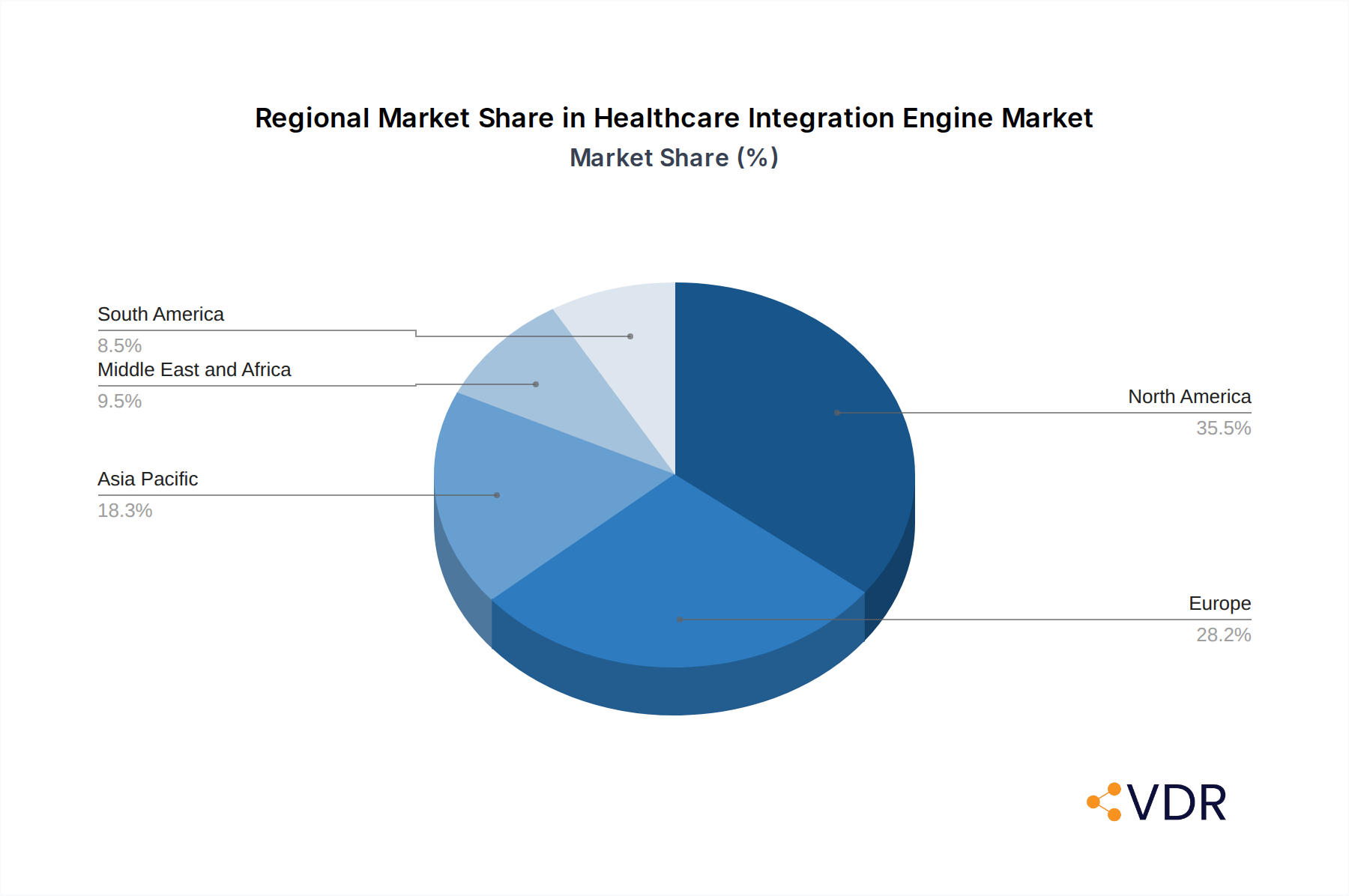

The market is characterized by diverse segmentation across product types, service modes, and end-users. Interface Engines and Medical Device Integration Setups are expected to witness strong demand, reflecting the core functionalities required for healthcare data interoperability. Operation Services, Support and Upkeep Services, and Training are crucial for ensuring the efficient deployment and ongoing management of these integration solutions. Hospitals, clinics, and laboratories represent the primary end-users, with radiology and other specialized healthcare settings also contributing to market growth. Geographically, North America is anticipated to lead the market, driven by its advanced healthcare infrastructure and early adoption of health IT solutions. Asia Pacific, with its rapidly growing economies and increasing investments in healthcare, is expected to emerge as a high-growth region. Addressing the need for secure and efficient data flow is paramount for optimizing patient care and operational effectiveness within the evolving healthcare landscape.

Healthcare Integration Engine Market Company Market Share

This in-depth report provides a critical analysis of the global Healthcare Integration Engine Market, projected to reach USD 5,500 Million by 2033, exhibiting a robust CAGR of 12.5% from 2025 to 2033. Dive into the dynamic forces shaping the seamless exchange of health data, essential for modern healthcare delivery. Our comprehensive study, spanning from 2019 to 2033, with a base and estimated year of 2025, leverages cutting-edge market intelligence to deliver actionable insights. Explore parent and child market dynamics, identifying key growth drivers, emerging opportunities, and the competitive landscape. This report is indispensable for healthcare providers, technology vendors, investors, and policymakers seeking to navigate the complexities and capitalize on the burgeoning demand for efficient healthcare data integration solutions.

Healthcare Integration Engine Market Market Dynamics & Structure

The Healthcare Integration Engine Market is characterized by a moderately concentrated landscape, driven by rapid technological innovation and evolving regulatory frameworks aimed at improving patient care and data security. Key drivers include the increasing adoption of Electronic Health Records (EHRs), the growing demand for interoperability across disparate healthcare systems, and the burgeoning use of big data analytics and AI in healthcare. The push for value-based care models further necessitates seamless data flow between providers, payers, and patients. However, challenges such as the high cost of implementation, concerns over data privacy and security (HIPAA, GDPR compliance), and the technical complexities of integrating legacy systems with newer platforms act as innovation barriers. Mergers and acquisitions (M&A) are a notable trend, with approximately 15-20 significant M&A deals observed annually between 2019-2024, indicating consolidation and strategic expansion among key players aiming to enhance their service portfolios and market reach. Competitive product substitutes, while present in niche areas, often lack the comprehensive interoperability capabilities offered by dedicated integration engines. End-user demographics are shifting towards larger hospital systems and integrated delivery networks (IDNs) seeking sophisticated solutions for managing vast amounts of patient data.

- Market Concentration: Moderately concentrated with a mix of established giants and emerging innovators.

- Technological Innovation Drivers: EHR adoption, interoperability mandates, AI/ML in healthcare, telehealth expansion.

- Regulatory Frameworks: HIPAA, HITECH Act, GDPR, ONC certification requirements significantly influence market development.

- Competitive Product Substitutes: Basic data conversion tools, point-to-point interfaces (less scalable).

- End-User Demographics: Growing preference for comprehensive solutions from large healthcare organizations.

- M&A Trends: Active consolidation to acquire advanced technologies and expand market share.

Healthcare Integration Engine Market Growth Trends & Insights

The Healthcare Integration Engine Market is experiencing substantial growth, fueled by the imperative for seamless data exchange in modern healthcare ecosystems. The market size has witnessed a steady upward trajectory, projected to surge from an estimated USD 2,800 Million in 2025 to USD 5,500 Million by 2033. This growth is underpinned by an average market penetration rate of approximately 45% in developed economies, with significant room for expansion in emerging markets. Technological disruptions, such as the advancement of cloud-based integration platforms and the increasing application of FHIR (Fast Healthcare Interoperability Resources) standards, are accelerating adoption rates. Consumer behavior shifts, with patients becoming more engaged in their healthcare and demanding access to their data, are also pushing providers to invest in robust integration solutions. The compound annual growth rate (CAGR) for the forecast period (2025–2033) is estimated at a robust 12.5%. The increasing digitization of healthcare, coupled with the growing emphasis on data-driven decision-making for improved patient outcomes and operational efficiency, positions the Healthcare Integration Engine Market for sustained and significant expansion. The shift towards value-based care models, which reward providers for quality of care rather than volume of services, further emphasizes the need for comprehensive data integration to track patient journeys and outcomes across various care settings.

Dominant Regions, Countries, or Segments in Healthcare Integration Engine Market

North America currently dominates the Healthcare Integration Engine Market, driven by its advanced healthcare infrastructure, stringent interoperability mandates, and high adoption rates of digital health technologies. The United States, in particular, represents a significant market share, estimated at over 50% of the global market in 2025. This dominance is bolstered by substantial government initiatives, such as the Meaningful Use program (now Promoting Interoperability) and the ongoing push for interoperability through organizations like the Office of the National Coordinator for Health Information Technology (ONC). Economically, the region boasts significant investment in healthcare IT.

- Dominant Region: North America

- Key Country: United States

Within the product segment, Interface Engines are the leading category, accounting for an estimated 60% of the market share in 2025. This is attributed to their fundamental role in connecting disparate healthcare systems and facilitating the exchange of patient information.

- Dominant Product Segment: Interface Engines

In terms of the mode of service, Operation Services hold the largest market share, estimated at 45% in 2025, reflecting the ongoing need for robust management and maintenance of complex integration platforms.

- Dominant Mode of Service: Operation Services

Among end-users, Hospitals represent the largest segment, contributing approximately 55% of the market revenue in 2025. This is due to their critical need for integrated systems to manage patient care across various departments and facilities.

- Dominant End User Segment: Hospitals

Key drivers for dominance in these segments include:

- North America: Robust regulatory landscape, significant healthcare IT spending, strong presence of key players.

- Interface Engines: Essential for foundational interoperability, broad applicability across healthcare settings.

- Operation Services: Critical for ensuring system uptime, security, and compliance in complex healthcare environments.

- Hospitals: High volume of patient data, complex care pathways, and the need for efficient workflow management.

Healthcare Integration Engine Market Product Landscape

The product landscape of the Healthcare Integration Engine Market is diverse, encompassing sophisticated interface engines, specialized medical device integration setups, and a range of ancillary products. Interface engines, such as those offered by vendors like Epic Systems Corporation and Oracle Cerner, provide robust message routing, transformation, and orchestration capabilities, supporting numerous healthcare standards like HL7, FHIR, and DICOM. Medical device integration solutions are increasingly crucial, enabling real-time data capture from patient monitoring devices directly into EHRs, enhancing clinical decision-making and patient safety. Examples include solutions for ICU monitors, ventilators, and infusion pumps. Ancillary products often include data analytics tools, patient portals, and secure messaging platforms that leverage the integrated data. Key performance metrics revolve around data throughput, latency, security, and compliance with evolving interoperability standards.

Key Drivers, Barriers & Challenges in Healthcare Integration Engine Market

Key Drivers:

The Healthcare Integration Engine Market is propelled by several key forces. The increasing demand for interoperability is paramount, driven by regulatory mandates and the pursuit of seamless patient care across the continuum. The proliferation of Electronic Health Records (EHRs) necessitates robust integration solutions to consolidate patient data. Furthermore, the growing adoption of telehealth and remote patient monitoring solutions requires real-time data exchange capabilities. The rise of value-based care models also incentivizes providers to integrate data for better outcome tracking and cost management.

Barriers & Challenges:

Significant barriers and challenges exist within the market. The high initial investment costs for implementing and maintaining integration engines can be prohibitive for smaller healthcare organizations. Data security and privacy concerns, especially with the increasing volume of sensitive patient information, present ongoing hurdles, requiring adherence to stringent regulations like HIPAA. The complexity of integrating legacy systems with modern platforms, coupled with a shortage of skilled IT professionals in healthcare, adds to implementation difficulties. Competitive pressures from numerous vendors offering varied solutions also create market complexities.

Emerging Opportunities in Healthcare Integration Engine Market

Emerging opportunities in the Healthcare Integration Engine Market are vast and promising. The growing adoption of AI and machine learning in healthcare presents a significant avenue for integration engines to facilitate the flow of data for predictive analytics, personalized medicine, and clinical decision support. The expansion of remote patient monitoring and telehealth services, particularly in underserved regions, will require sophisticated integration solutions for seamless data exchange. The increasing focus on patient-generated health data (PGHD) from wearable devices and health apps offers a new frontier for integration, empowering patients and enhancing preventative care. Furthermore, the global push for interoperability standards like FHIR presents an opportunity for vendors to develop solutions that are compliant and easily adoptable across diverse healthcare ecosystems.

Growth Accelerators in the Healthcare Integration Engine Market Industry

Several key catalysts are accelerating growth within the Healthcare Integration Engine Market. Technological breakthroughs in cloud computing are enabling more scalable, flexible, and cost-effective integration solutions. Strategic partnerships between integration engine vendors and EHR providers, as well as with AI and analytics firms, are creating comprehensive ecosystems that address the evolving needs of healthcare organizations. Market expansion strategies, particularly focusing on emerging economies with rapidly developing healthcare infrastructures, are unlocking new revenue streams. The continuous evolution of interoperability standards, encouraging greater data sharing, also acts as a powerful growth accelerator, driving demand for compliant integration engines.

Key Players Shaping the Healthcare Integration Engine Market Market

- Siemens Healthcare GmbH

- Epic Systems Corporation

- IBM Corporation

- InterSystems Corporation

- Lyniate

- Summit Healthcare

- General Electric Company (GE Healthcare)

- Allscripts Healthcare Solutions Inc

- Orion Health

- Oracle Cerner

Notable Milestones in Healthcare Integration Engine Market Sector

- July 2022: Aster DM Healthcare Group's innovation hub, the Aster Innovation and Research Centre, partnered with Intel Corporation and AI platform provider CARPL.ai to develop and launch an AI-powered health data platform in India.

- May 2022: The San Francisco-based healthcare technology startup Innovaccer and Montana-based nonprofit health system St. Peter's Health are collaborating to integrate the latter's healthcare cloud platform into care locations and enhance care management.

In-Depth Healthcare Integration Engine Market Market Outlook

The Healthcare Integration Engine Market is poised for continued robust growth, driven by the fundamental need for efficient and secure health data exchange. Future market potential lies in the increasing integration of AI and IoT devices into healthcare workflows, demanding advanced interoperability solutions. Strategic opportunities include developing cloud-native integration platforms that offer enhanced scalability and agility, and focusing on specialized integration needs for areas like genomics and personalized medicine. The ongoing global push for standardized data formats and open APIs will further fuel the demand for sophisticated integration engines that can bridge the gap between diverse systems, ultimately leading to improved patient outcomes and a more connected healthcare ecosystem.

Healthcare Integration Engine Market Segmentation

-

1. Product

- 1.1. Interface Engines

- 1.2. Medical Device Integration Setup

- 1.3. Other Products

-

2. Mode of Service

- 2.1. Operation Services

- 2.2. Support and Upkeep Services

- 2.3. Training

-

3. End User

- 3.1. Hospitals

- 3.2. Clinics

- 3.3. Labs

- 3.4. Radiology

- 3.5. Other End Users

Healthcare Integration Engine Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Healthcare Integration Engine Market Regional Market Share

Geographic Coverage of Healthcare Integration Engine Market

Healthcare Integration Engine Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.85% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Interface Engines

- 5.1.2. Medical Device Integration Setup

- 5.1.3. Other Products

- 5.2. Market Analysis, Insights and Forecast - by Mode of Service

- 5.2.1. Operation Services

- 5.2.2. Support and Upkeep Services

- 5.2.3. Training

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Hospitals

- 5.3.2. Clinics

- 5.3.3. Labs

- 5.3.4. Radiology

- 5.3.5. Other End Users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Middle East and Africa

- 5.4.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. Global Healthcare Integration Engine Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Interface Engines

- 6.1.2. Medical Device Integration Setup

- 6.1.3. Other Products

- 6.2. Market Analysis, Insights and Forecast - by Mode of Service

- 6.2.1. Operation Services

- 6.2.2. Support and Upkeep Services

- 6.2.3. Training

- 6.3. Market Analysis, Insights and Forecast - by End User

- 6.3.1. Hospitals

- 6.3.2. Clinics

- 6.3.3. Labs

- 6.3.4. Radiology

- 6.3.5. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. North America Healthcare Integration Engine Market Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Product

- 7.1.1. Interface Engines

- 7.1.2. Medical Device Integration Setup

- 7.1.3. Other Products

- 7.2. Market Analysis, Insights and Forecast - by Mode of Service

- 7.2.1. Operation Services

- 7.2.2. Support and Upkeep Services

- 7.2.3. Training

- 7.3. Market Analysis, Insights and Forecast - by End User

- 7.3.1. Hospitals

- 7.3.2. Clinics

- 7.3.3. Labs

- 7.3.4. Radiology

- 7.3.5. Other End Users

- 7.1. Market Analysis, Insights and Forecast - by Product

- 8. Europe Healthcare Integration Engine Market Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Product

- 8.1.1. Interface Engines

- 8.1.2. Medical Device Integration Setup

- 8.1.3. Other Products

- 8.2. Market Analysis, Insights and Forecast - by Mode of Service

- 8.2.1. Operation Services

- 8.2.2. Support and Upkeep Services

- 8.2.3. Training

- 8.3. Market Analysis, Insights and Forecast - by End User

- 8.3.1. Hospitals

- 8.3.2. Clinics

- 8.3.3. Labs

- 8.3.4. Radiology

- 8.3.5. Other End Users

- 8.1. Market Analysis, Insights and Forecast - by Product

- 9. Asia Pacific Healthcare Integration Engine Market Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Product

- 9.1.1. Interface Engines

- 9.1.2. Medical Device Integration Setup

- 9.1.3. Other Products

- 9.2. Market Analysis, Insights and Forecast - by Mode of Service

- 9.2.1. Operation Services

- 9.2.2. Support and Upkeep Services

- 9.2.3. Training

- 9.3. Market Analysis, Insights and Forecast - by End User

- 9.3.1. Hospitals

- 9.3.2. Clinics

- 9.3.3. Labs

- 9.3.4. Radiology

- 9.3.5. Other End Users

- 9.1. Market Analysis, Insights and Forecast - by Product

- 10. Middle East and Africa Healthcare Integration Engine Market Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Product

- 10.1.1. Interface Engines

- 10.1.2. Medical Device Integration Setup

- 10.1.3. Other Products

- 10.2. Market Analysis, Insights and Forecast - by Mode of Service

- 10.2.1. Operation Services

- 10.2.2. Support and Upkeep Services

- 10.2.3. Training

- 10.3. Market Analysis, Insights and Forecast - by End User

- 10.3.1. Hospitals

- 10.3.2. Clinics

- 10.3.3. Labs

- 10.3.4. Radiology

- 10.3.5. Other End Users

- 10.1. Market Analysis, Insights and Forecast - by Product

- 11. South America Healthcare Integration Engine Market Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Product

- 11.1.1. Interface Engines

- 11.1.2. Medical Device Integration Setup

- 11.1.3. Other Products

- 11.2. Market Analysis, Insights and Forecast - by Mode of Service

- 11.2.1. Operation Services

- 11.2.2. Support and Upkeep Services

- 11.2.3. Training

- 11.3. Market Analysis, Insights and Forecast - by End User

- 11.3.1. Hospitals

- 11.3.2. Clinics

- 11.3.3. Labs

- 11.3.4. Radiology

- 11.3.5. Other End Users

- 11.1. Market Analysis, Insights and Forecast - by Product

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Siemens Healthcare GmbH

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Epic Systems Corporation

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 IBM Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 InterSystems Corporation

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Lyniate

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Summit Healthcare

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 General Electric Company (GE Healthcare)

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Allscripts Healthcare Solutions Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Orion Health

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Oracle Cerner

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Siemens Healthcare GmbH

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Healthcare Integration Engine Market Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Healthcare Integration Engine Market Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Healthcare Integration Engine Market Revenue (Million), by Product 2025 & 2033

- Figure 4: North America Healthcare Integration Engine Market Volume (K Unit), by Product 2025 & 2033

- Figure 5: North America Healthcare Integration Engine Market Revenue Share (%), by Product 2025 & 2033

- Figure 6: North America Healthcare Integration Engine Market Volume Share (%), by Product 2025 & 2033

- Figure 7: North America Healthcare Integration Engine Market Revenue (Million), by Mode of Service 2025 & 2033

- Figure 8: North America Healthcare Integration Engine Market Volume (K Unit), by Mode of Service 2025 & 2033

- Figure 9: North America Healthcare Integration Engine Market Revenue Share (%), by Mode of Service 2025 & 2033

- Figure 10: North America Healthcare Integration Engine Market Volume Share (%), by Mode of Service 2025 & 2033

- Figure 11: North America Healthcare Integration Engine Market Revenue (Million), by End User 2025 & 2033

- Figure 12: North America Healthcare Integration Engine Market Volume (K Unit), by End User 2025 & 2033

- Figure 13: North America Healthcare Integration Engine Market Revenue Share (%), by End User 2025 & 2033

- Figure 14: North America Healthcare Integration Engine Market Volume Share (%), by End User 2025 & 2033

- Figure 15: North America Healthcare Integration Engine Market Revenue (Million), by Country 2025 & 2033

- Figure 16: North America Healthcare Integration Engine Market Volume (K Unit), by Country 2025 & 2033

- Figure 17: North America Healthcare Integration Engine Market Revenue Share (%), by Country 2025 & 2033

- Figure 18: North America Healthcare Integration Engine Market Volume Share (%), by Country 2025 & 2033

- Figure 19: Europe Healthcare Integration Engine Market Revenue (Million), by Product 2025 & 2033

- Figure 20: Europe Healthcare Integration Engine Market Volume (K Unit), by Product 2025 & 2033

- Figure 21: Europe Healthcare Integration Engine Market Revenue Share (%), by Product 2025 & 2033

- Figure 22: Europe Healthcare Integration Engine Market Volume Share (%), by Product 2025 & 2033

- Figure 23: Europe Healthcare Integration Engine Market Revenue (Million), by Mode of Service 2025 & 2033

- Figure 24: Europe Healthcare Integration Engine Market Volume (K Unit), by Mode of Service 2025 & 2033

- Figure 25: Europe Healthcare Integration Engine Market Revenue Share (%), by Mode of Service 2025 & 2033

- Figure 26: Europe Healthcare Integration Engine Market Volume Share (%), by Mode of Service 2025 & 2033

- Figure 27: Europe Healthcare Integration Engine Market Revenue (Million), by End User 2025 & 2033

- Figure 28: Europe Healthcare Integration Engine Market Volume (K Unit), by End User 2025 & 2033

- Figure 29: Europe Healthcare Integration Engine Market Revenue Share (%), by End User 2025 & 2033

- Figure 30: Europe Healthcare Integration Engine Market Volume Share (%), by End User 2025 & 2033

- Figure 31: Europe Healthcare Integration Engine Market Revenue (Million), by Country 2025 & 2033

- Figure 32: Europe Healthcare Integration Engine Market Volume (K Unit), by Country 2025 & 2033

- Figure 33: Europe Healthcare Integration Engine Market Revenue Share (%), by Country 2025 & 2033

- Figure 34: Europe Healthcare Integration Engine Market Volume Share (%), by Country 2025 & 2033

- Figure 35: Asia Pacific Healthcare Integration Engine Market Revenue (Million), by Product 2025 & 2033

- Figure 36: Asia Pacific Healthcare Integration Engine Market Volume (K Unit), by Product 2025 & 2033

- Figure 37: Asia Pacific Healthcare Integration Engine Market Revenue Share (%), by Product 2025 & 2033

- Figure 38: Asia Pacific Healthcare Integration Engine Market Volume Share (%), by Product 2025 & 2033

- Figure 39: Asia Pacific Healthcare Integration Engine Market Revenue (Million), by Mode of Service 2025 & 2033

- Figure 40: Asia Pacific Healthcare Integration Engine Market Volume (K Unit), by Mode of Service 2025 & 2033

- Figure 41: Asia Pacific Healthcare Integration Engine Market Revenue Share (%), by Mode of Service 2025 & 2033

- Figure 42: Asia Pacific Healthcare Integration Engine Market Volume Share (%), by Mode of Service 2025 & 2033

- Figure 43: Asia Pacific Healthcare Integration Engine Market Revenue (Million), by End User 2025 & 2033

- Figure 44: Asia Pacific Healthcare Integration Engine Market Volume (K Unit), by End User 2025 & 2033

- Figure 45: Asia Pacific Healthcare Integration Engine Market Revenue Share (%), by End User 2025 & 2033

- Figure 46: Asia Pacific Healthcare Integration Engine Market Volume Share (%), by End User 2025 & 2033

- Figure 47: Asia Pacific Healthcare Integration Engine Market Revenue (Million), by Country 2025 & 2033

- Figure 48: Asia Pacific Healthcare Integration Engine Market Volume (K Unit), by Country 2025 & 2033

- Figure 49: Asia Pacific Healthcare Integration Engine Market Revenue Share (%), by Country 2025 & 2033

- Figure 50: Asia Pacific Healthcare Integration Engine Market Volume Share (%), by Country 2025 & 2033

- Figure 51: Middle East and Africa Healthcare Integration Engine Market Revenue (Million), by Product 2025 & 2033

- Figure 52: Middle East and Africa Healthcare Integration Engine Market Volume (K Unit), by Product 2025 & 2033

- Figure 53: Middle East and Africa Healthcare Integration Engine Market Revenue Share (%), by Product 2025 & 2033

- Figure 54: Middle East and Africa Healthcare Integration Engine Market Volume Share (%), by Product 2025 & 2033

- Figure 55: Middle East and Africa Healthcare Integration Engine Market Revenue (Million), by Mode of Service 2025 & 2033

- Figure 56: Middle East and Africa Healthcare Integration Engine Market Volume (K Unit), by Mode of Service 2025 & 2033

- Figure 57: Middle East and Africa Healthcare Integration Engine Market Revenue Share (%), by Mode of Service 2025 & 2033

- Figure 58: Middle East and Africa Healthcare Integration Engine Market Volume Share (%), by Mode of Service 2025 & 2033

- Figure 59: Middle East and Africa Healthcare Integration Engine Market Revenue (Million), by End User 2025 & 2033

- Figure 60: Middle East and Africa Healthcare Integration Engine Market Volume (K Unit), by End User 2025 & 2033

- Figure 61: Middle East and Africa Healthcare Integration Engine Market Revenue Share (%), by End User 2025 & 2033

- Figure 62: Middle East and Africa Healthcare Integration Engine Market Volume Share (%), by End User 2025 & 2033

- Figure 63: Middle East and Africa Healthcare Integration Engine Market Revenue (Million), by Country 2025 & 2033

- Figure 64: Middle East and Africa Healthcare Integration Engine Market Volume (K Unit), by Country 2025 & 2033

- Figure 65: Middle East and Africa Healthcare Integration Engine Market Revenue Share (%), by Country 2025 & 2033

- Figure 66: Middle East and Africa Healthcare Integration Engine Market Volume Share (%), by Country 2025 & 2033

- Figure 67: South America Healthcare Integration Engine Market Revenue (Million), by Product 2025 & 2033

- Figure 68: South America Healthcare Integration Engine Market Volume (K Unit), by Product 2025 & 2033

- Figure 69: South America Healthcare Integration Engine Market Revenue Share (%), by Product 2025 & 2033

- Figure 70: South America Healthcare Integration Engine Market Volume Share (%), by Product 2025 & 2033

- Figure 71: South America Healthcare Integration Engine Market Revenue (Million), by Mode of Service 2025 & 2033

- Figure 72: South America Healthcare Integration Engine Market Volume (K Unit), by Mode of Service 2025 & 2033

- Figure 73: South America Healthcare Integration Engine Market Revenue Share (%), by Mode of Service 2025 & 2033

- Figure 74: South America Healthcare Integration Engine Market Volume Share (%), by Mode of Service 2025 & 2033

- Figure 75: South America Healthcare Integration Engine Market Revenue (Million), by End User 2025 & 2033

- Figure 76: South America Healthcare Integration Engine Market Volume (K Unit), by End User 2025 & 2033

- Figure 77: South America Healthcare Integration Engine Market Revenue Share (%), by End User 2025 & 2033

- Figure 78: South America Healthcare Integration Engine Market Volume Share (%), by End User 2025 & 2033

- Figure 79: South America Healthcare Integration Engine Market Revenue (Million), by Country 2025 & 2033

- Figure 80: South America Healthcare Integration Engine Market Volume (K Unit), by Country 2025 & 2033

- Figure 81: South America Healthcare Integration Engine Market Revenue Share (%), by Country 2025 & 2033

- Figure 82: South America Healthcare Integration Engine Market Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Healthcare Integration Engine Market Revenue Million Forecast, by Product 2020 & 2033

- Table 2: Global Healthcare Integration Engine Market Volume K Unit Forecast, by Product 2020 & 2033

- Table 3: Global Healthcare Integration Engine Market Revenue Million Forecast, by Mode of Service 2020 & 2033

- Table 4: Global Healthcare Integration Engine Market Volume K Unit Forecast, by Mode of Service 2020 & 2033

- Table 5: Global Healthcare Integration Engine Market Revenue Million Forecast, by End User 2020 & 2033

- Table 6: Global Healthcare Integration Engine Market Volume K Unit Forecast, by End User 2020 & 2033

- Table 7: Global Healthcare Integration Engine Market Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Global Healthcare Integration Engine Market Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: Global Healthcare Integration Engine Market Revenue Million Forecast, by Product 2020 & 2033

- Table 10: Global Healthcare Integration Engine Market Volume K Unit Forecast, by Product 2020 & 2033

- Table 11: Global Healthcare Integration Engine Market Revenue Million Forecast, by Mode of Service 2020 & 2033

- Table 12: Global Healthcare Integration Engine Market Volume K Unit Forecast, by Mode of Service 2020 & 2033

- Table 13: Global Healthcare Integration Engine Market Revenue Million Forecast, by End User 2020 & 2033

- Table 14: Global Healthcare Integration Engine Market Volume K Unit Forecast, by End User 2020 & 2033

- Table 15: Global Healthcare Integration Engine Market Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Healthcare Integration Engine Market Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: United States Healthcare Integration Engine Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: United States Healthcare Integration Engine Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Canada Healthcare Integration Engine Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Canada Healthcare Integration Engine Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 21: Mexico Healthcare Integration Engine Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Mexico Healthcare Integration Engine Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: Global Healthcare Integration Engine Market Revenue Million Forecast, by Product 2020 & 2033

- Table 24: Global Healthcare Integration Engine Market Volume K Unit Forecast, by Product 2020 & 2033

- Table 25: Global Healthcare Integration Engine Market Revenue Million Forecast, by Mode of Service 2020 & 2033

- Table 26: Global Healthcare Integration Engine Market Volume K Unit Forecast, by Mode of Service 2020 & 2033

- Table 27: Global Healthcare Integration Engine Market Revenue Million Forecast, by End User 2020 & 2033

- Table 28: Global Healthcare Integration Engine Market Volume K Unit Forecast, by End User 2020 & 2033

- Table 29: Global Healthcare Integration Engine Market Revenue Million Forecast, by Country 2020 & 2033

- Table 30: Global Healthcare Integration Engine Market Volume K Unit Forecast, by Country 2020 & 2033

- Table 31: Germany Healthcare Integration Engine Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Germany Healthcare Integration Engine Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: United Kingdom Healthcare Integration Engine Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: United Kingdom Healthcare Integration Engine Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: France Healthcare Integration Engine Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: France Healthcare Integration Engine Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Italy Healthcare Integration Engine Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Italy Healthcare Integration Engine Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 39: Spain Healthcare Integration Engine Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Spain Healthcare Integration Engine Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 41: Rest of Europe Healthcare Integration Engine Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Rest of Europe Healthcare Integration Engine Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 43: Global Healthcare Integration Engine Market Revenue Million Forecast, by Product 2020 & 2033

- Table 44: Global Healthcare Integration Engine Market Volume K Unit Forecast, by Product 2020 & 2033

- Table 45: Global Healthcare Integration Engine Market Revenue Million Forecast, by Mode of Service 2020 & 2033

- Table 46: Global Healthcare Integration Engine Market Volume K Unit Forecast, by Mode of Service 2020 & 2033

- Table 47: Global Healthcare Integration Engine Market Revenue Million Forecast, by End User 2020 & 2033

- Table 48: Global Healthcare Integration Engine Market Volume K Unit Forecast, by End User 2020 & 2033

- Table 49: Global Healthcare Integration Engine Market Revenue Million Forecast, by Country 2020 & 2033

- Table 50: Global Healthcare Integration Engine Market Volume K Unit Forecast, by Country 2020 & 2033

- Table 51: China Healthcare Integration Engine Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 52: China Healthcare Integration Engine Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 53: Japan Healthcare Integration Engine Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 54: Japan Healthcare Integration Engine Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 55: India Healthcare Integration Engine Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 56: India Healthcare Integration Engine Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 57: Australia Healthcare Integration Engine Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 58: Australia Healthcare Integration Engine Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 59: South Korea Healthcare Integration Engine Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 60: South Korea Healthcare Integration Engine Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 61: Rest of Asia Pacific Healthcare Integration Engine Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 62: Rest of Asia Pacific Healthcare Integration Engine Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 63: Global Healthcare Integration Engine Market Revenue Million Forecast, by Product 2020 & 2033

- Table 64: Global Healthcare Integration Engine Market Volume K Unit Forecast, by Product 2020 & 2033

- Table 65: Global Healthcare Integration Engine Market Revenue Million Forecast, by Mode of Service 2020 & 2033

- Table 66: Global Healthcare Integration Engine Market Volume K Unit Forecast, by Mode of Service 2020 & 2033

- Table 67: Global Healthcare Integration Engine Market Revenue Million Forecast, by End User 2020 & 2033

- Table 68: Global Healthcare Integration Engine Market Volume K Unit Forecast, by End User 2020 & 2033

- Table 69: Global Healthcare Integration Engine Market Revenue Million Forecast, by Country 2020 & 2033

- Table 70: Global Healthcare Integration Engine Market Volume K Unit Forecast, by Country 2020 & 2033

- Table 71: GCC Healthcare Integration Engine Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 72: GCC Healthcare Integration Engine Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 73: South Africa Healthcare Integration Engine Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 74: South Africa Healthcare Integration Engine Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 75: Rest of Middle East and Africa Healthcare Integration Engine Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 76: Rest of Middle East and Africa Healthcare Integration Engine Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 77: Global Healthcare Integration Engine Market Revenue Million Forecast, by Product 2020 & 2033

- Table 78: Global Healthcare Integration Engine Market Volume K Unit Forecast, by Product 2020 & 2033

- Table 79: Global Healthcare Integration Engine Market Revenue Million Forecast, by Mode of Service 2020 & 2033

- Table 80: Global Healthcare Integration Engine Market Volume K Unit Forecast, by Mode of Service 2020 & 2033

- Table 81: Global Healthcare Integration Engine Market Revenue Million Forecast, by End User 2020 & 2033

- Table 82: Global Healthcare Integration Engine Market Volume K Unit Forecast, by End User 2020 & 2033

- Table 83: Global Healthcare Integration Engine Market Revenue Million Forecast, by Country 2020 & 2033

- Table 84: Global Healthcare Integration Engine Market Volume K Unit Forecast, by Country 2020 & 2033

- Table 85: Brazil Healthcare Integration Engine Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 86: Brazil Healthcare Integration Engine Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 87: Argentina Healthcare Integration Engine Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 88: Argentina Healthcare Integration Engine Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 89: Rest of South America Healthcare Integration Engine Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 90: Rest of South America Healthcare Integration Engine Market Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Healthcare Integration Engine Market?

The projected CAGR is approximately 11.85%.

2. Which companies are prominent players in the Healthcare Integration Engine Market?

Key companies in the market include Siemens Healthcare GmbH, Epic Systems Corporation, IBM Corporation, InterSystems Corporation, Lyniate, Summit Healthcare, General Electric Company (GE Healthcare), Allscripts Healthcare Solutions Inc, Orion Health, Oracle Cerner.

3. What are the main segments of the Healthcare Integration Engine Market?

The market segments include Product, Mode of Service, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.19 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Need of Electronic Health Records and Other Healthcare IT Solutions; Growing Demand for Telehealth Services and Remote Patient Monitoring Solutions.

6. What are the notable trends driving market growth?

Interface Engine Segment is Expected to Hold the Highest Market Share Over the Forecast Period.

7. Are there any restraints impacting market growth?

Lack of Skilled Professionals.

8. Can you provide examples of recent developments in the market?

In July 2022, Aster DM Healthcare Group's innovation hub, the Aster Innovation and Research Centre, partnered with Intel Corporation and AI platform provider CARPL.ai to develop and launch an AI-powered health data platform in India.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Healthcare Integration Engine Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Healthcare Integration Engine Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Healthcare Integration Engine Market?

To stay informed about further developments, trends, and reports in the Healthcare Integration Engine Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence