Key Insights

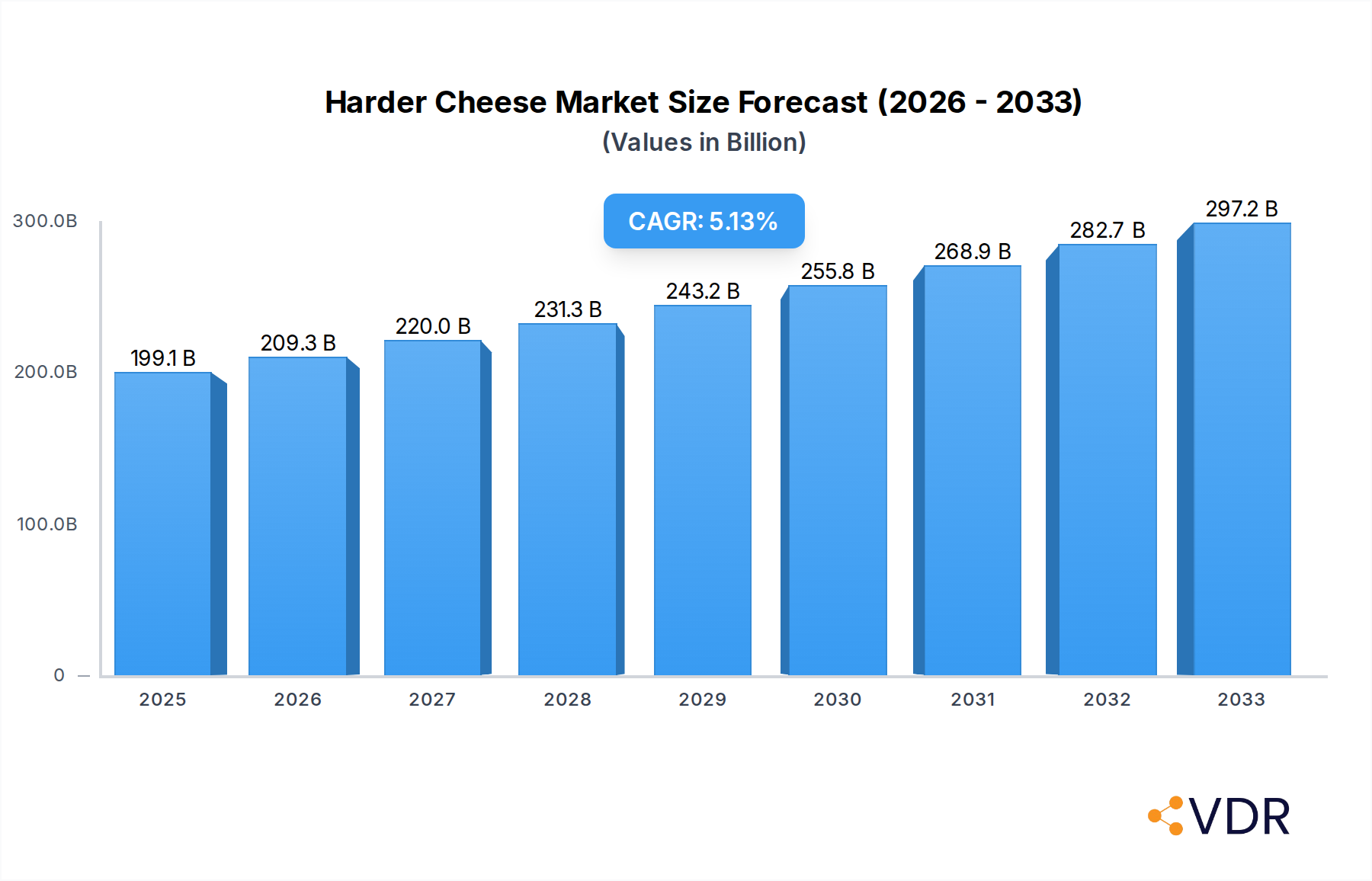

The global Harder Cheese market is poised for robust growth, projected to reach USD 199.14 billion in 2025. Driven by increasing consumer demand for versatile and flavorful cheese options, the market is expected to witness a Compound Annual Growth Rate (CAGR) of 5.15% from 2025 to 2033. This expansion is fueled by evolving dietary preferences, a growing acceptance of cheese in diverse culinary applications, and the rising popularity of premium and artisanal cheese varieties. The market's dynamism is further influenced by key trends such as the surge in online retail for dairy products and the increasing adoption of innovative packaging solutions that enhance shelf life and convenience. Supermarkets and hypermarkets are anticipated to remain dominant distribution channels, catering to a broad consumer base, while departmental and specialty stores will cater to niche markets seeking specific types of harder cheeses.

Harder Cheese Market Size (In Billion)

Despite a strong growth trajectory, the market faces certain restraints. Fluctuations in raw material prices, particularly for milk, can impact production costs and profit margins for manufacturers. Stringent regulations regarding food safety and labeling across different regions also present challenges, requiring significant compliance efforts from companies. Furthermore, the growing consumer awareness regarding health and wellness, leading to a demand for lower-fat or lactose-free alternatives, could pose a challenge to the traditional harder cheese market. However, the market's resilience is evident in its ability to adapt through product innovation, such as developing reduced-fat harder cheese varieties and catering to diverse water content preferences, ranging from 40% to over 50%, to meet varied consumer needs and culinary applications.

Harder Cheese Company Market Share

Comprehensive Harder Cheese Market Report: Dynamics, Growth, and Future Outlook (2019-2033)

This in-depth report provides an authoritative analysis of the global Harder Cheese market, a vital segment within the broader dairy industry. With a comprehensive study period of 2019–2033, including a base year of 2025 and a forecast period of 2025–2033, this research offers unparalleled insights into market dynamics, growth trajectories, and strategic opportunities. We delve into various segments, including Types based on water content (40%, 41-45%, 46-49%, 50%) and Application channels like Supermarkets/Hypermarkets, Departmental Stores, Speciality Stores, and Online Retail. This report is meticulously crafted for industry professionals, stakeholders, and decision-makers seeking a competitive edge in the evolving hard cheese industry, specialty cheese market, and aged cheese sector. Expect to find detailed quantitative data and actionable qualitative analysis, all presented in billion units for clear financial comprehension.

Harder Cheese Market Dynamics & Structure

The Harder Cheese market exhibits a moderately concentrated structure, with a few major global players dominating production and distribution. Key drivers of technological innovation include advancements in aging techniques, moisture control for extended shelf life, and the development of novel flavor profiles catering to sophisticated consumer palates. Regulatory frameworks, particularly concerning food safety, labeling, and international trade, play a significant role in shaping market access and product development. Competitive product substitutes, such as softer cheeses and alternative protein-based dairy-free options, present ongoing challenges, necessitating continuous product differentiation and marketing efforts. End-user demographics are increasingly diverse, with a growing demand from affluent urban populations and a significant influence from health-conscious consumers seeking nutrient-dense food options. Mergers and acquisitions (M&A) are a notable trend, with larger entities acquiring smaller, innovative producers to expand their product portfolios and market reach. For instance, the global aged cheese market has witnessed an average of 5-7 M&A deals annually over the past five years, with deal values ranging from tens of millions to over a billion dollars.

- Market Concentration: Dominated by a mix of multinational corporations and regional specialists.

- Technological Innovation: Focus on fermentation science, packaging technology, and flavor enhancement.

- Regulatory Landscape: Stringent food safety standards and evolving import/export regulations.

- Competitive Substitutes: Emerging plant-based alternatives and a wider array of softer cheese varieties.

- End-User Demographics: Shifting towards premiumization, health benefits, and convenience.

- M&A Trends: Strategic consolidation to gain market share and acquire proprietary technologies.

Harder Cheese Growth Trends & Insights

The Harder Cheese market is projected to experience robust growth, driven by evolving consumer preferences for artisanal and premium dairy products. The market size is expected to ascend from approximately $120 billion in 2024 to an estimated $180 billion by 2033, reflecting a Compound Annual Growth Rate (CAGR) of approximately 4.5%. This expansion is fueled by increasing disposable incomes globally, a growing appreciation for complex flavors, and the rising popularity of cheese boards and culinary exploration. Technological disruptions, such as improved cold chain logistics and advanced ripening technologies, are enhancing product quality and extending shelf life, further stimulating demand. Consumer behavior shifts are evident, with a heightened demand for transparency in sourcing and production methods, alongside a growing interest in the health benefits associated with aged cheeses, such as their protein and calcium content. The market penetration of specialty and harder cheeses is steadily increasing across both developed and emerging economies, moving beyond traditional channels to encompass online retail and direct-to-consumer models. This sustained upward trend in adoption rates signifies a maturing market actively responding to diverse consumer needs and culinary trends within the premium cheese segment.

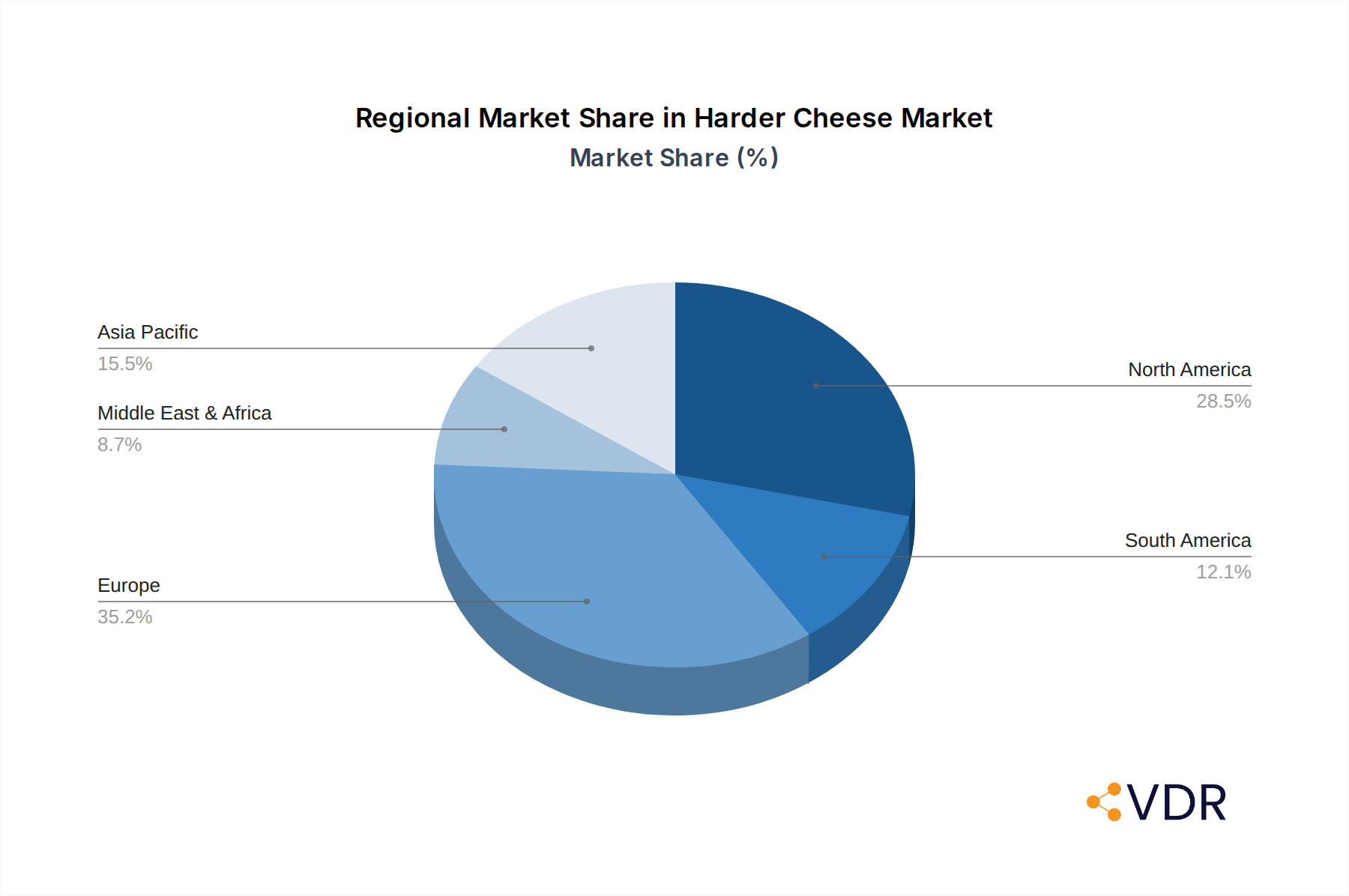

Dominant Regions, Countries, or Segments in Harder Cheese

The Supermarkets/Hypermarkets segment is poised to remain the dominant channel for Harder Cheese sales globally, accounting for an estimated 45% of the total market share by 2025. This dominance is attributed to their extensive reach, convenient one-stop shopping experience, and increasingly sophisticated in-store displays catering to a broad consumer base. Within Types, cheeses with a Water Content of 46-49% are expected to lead growth, driven by their versatility in cooking and snacking, offering a desirable balance of texture and flavor. Geographically, Europe is anticipated to maintain its position as the leading region, propelled by a deep-rooted cheese culture and high per capita consumption. Countries like Italy, France, and the United Kingdom are significant contributors, with a strong emphasis on traditional, high-quality harder cheeses. The United States, however, is emerging as a rapidly growing market, fueled by increasing consumer interest in artisanal and specialty cheeses.

- Dominant Application: Supermarkets/Hypermarkets (estimated 45% market share in 2025) offering convenience and wide selection.

- Leading Type: Water Content 46-49% is expected to drive growth due to its culinary versatility and appealing texture.

- Leading Region: Europe continues to dominate due to established cheese heritage and high consumption.

- Key Growth Country: The United States demonstrates significant expansion potential driven by the artisanal cheese trend.

- Infrastructure & Distribution: Well-developed supply chains and cold storage facilities in major regions facilitate market access.

- Economic Factors: Rising disposable incomes and a growing middle class in emerging economies are boosting demand.

Harder Cheese Product Landscape

The Harder Cheese product landscape is characterized by ongoing innovation in flavor profiles, aging processes, and packaging. Manufacturers are actively developing unique variations of cheddar, gouda, parmesan, and other hard cheeses, often incorporating specialty cultures and natural flavorings to create distinctive taste experiences. Performance metrics are increasingly focused on shelf-life extension through advanced ripening techniques and Modified Atmosphere Packaging (MAP). Unique selling propositions often revolve around provenance, artisanal craftsmanship, and specific health benefits, such as higher protein content and lower lactose levels. Technological advancements in precision fermentation are also beginning to influence the production of specific flavor compounds, offering new avenues for product development within the specialty cheese market.

Key Drivers, Barriers & Challenges in Harder Cheese

Key Drivers: The Harder Cheese market is propelled by several key drivers, including the escalating global demand for premium and artisanal food products, a growing consumer appreciation for complex flavors and culinary experiences, and the recognized health benefits associated with aged cheeses, such as high protein and calcium content. Technological advancements in cheese-making and aging processes are enhancing product quality and consistency.

Barriers & Challenges: Significant barriers include the supply chain complexities inherent in the dairy industry, requiring stringent temperature control and efficient logistics, with disruptions potentially costing the market upwards of $2 billion annually. Regulatory hurdles, particularly related to international trade agreements and differing food safety standards across regions, can impede market access. Intense competitive pressures from both domestic and international players, as well as from emerging dairy alternatives, necessitate continuous innovation and aggressive marketing strategies. The price volatility of raw milk, a primary input, also poses a considerable challenge, impacting production costs and ultimately consumer pricing.

Emerging Opportunities in Harder Cheese

Emerging opportunities in the Harder Cheese market lie in the untapped potential of plant-based alternatives formulated to mimic the texture and taste of traditional harder cheeses, catering to a growing vegan and lactose-intolerant population, a segment estimated to grow by 10-15% annually. Innovative applications in convenience foods, such as pre-shredded or pre-portioned hard cheeses for snacking and meal preparation, address the demand for on-the-go consumption. Evolving consumer preferences for health-focused products are driving interest in hard cheeses fortified with probiotics or lower in sodium. Furthermore, the expansion of online retail platforms presents a significant opportunity for direct-to-consumer sales of niche and specialty hard cheeses, reaching a wider audience beyond traditional brick-and-mortar stores.

Growth Accelerators in the Harder Cheese Industry

Several catalysts are accelerating growth in the Harder Cheese industry. Technological breakthroughs in enzyme technology and controlled ripening environments are leading to the development of cheeses with enhanced flavor profiles and extended shelf lives, contributing an estimated $3-5 billion in market value annually through improved product quality. Strategic partnerships between cheese producers and food service companies are expanding the reach of harder cheeses into new culinary applications. Market expansion strategies, particularly into emerging economies where dairy consumption is rising, are opening up significant new customer bases. The increasing consumer demand for traceability and sustainability is also a growth accelerator, pushing companies to adopt more transparent and eco-friendly production methods.

Key Players Shaping the Harder Cheese Market

- Granarolo

- Eurial

- Couturier North America

- CASA Radicci

- Flanders Milk/Ets Freddy Baines

- Winona Foods

- St. Paul

- Mammen Dairy

- DONIDO

- Tetra Pak

- Vindija

Notable Milestones in Harder Cheese Sector

- 2019: Introduction of blockchain technology for enhanced cheese traceability by select European producers, impacting market trust and transparency.

- 2020: Significant surge in online cheese sales due to pandemic-related shopping behavior shifts.

- 2021: Development of novel aging accelerators to reduce ripening time by up to 30% for select hard cheeses, impacting production efficiency.

- 2022: Increased investment in R&D for plant-based hard cheese alternatives, signaling a competitive response.

- 2023: Regulatory changes in key markets allowing for broader labeling claims related to health benefits of aged cheeses.

- 2024: Expansion of European premium hard cheese brands into North American specialty stores, driving global market reach.

In-Depth Harder Cheese Market Outlook

The future outlook for the Harder Cheese market is exceptionally positive, driven by sustained growth accelerators such as continued innovation in flavor complexity and health-centric product development. The increasing adoption of advanced manufacturing technologies will further optimize production efficiency and product quality. Strategic market expansion into Asia-Pacific and other emerging regions presents substantial untapped potential, estimated to contribute an additional $15-20 billion in market value over the forecast period. The ongoing consumer trend towards premiumization and artisanal products will continue to favor specialty hard cheeses, creating robust opportunities for market players to capitalize on evolving consumer preferences and culinary trends.

Harder Cheese Segmentation

-

1. Application

- 1.1. Supermarkets/Hypermarkets

- 1.2. Departmental Stores

- 1.3. Speciality Stores

- 1.4. Online Retail

-

2. Types

- 2.1. Water Content 40%

- 2.2. Water Content 41-45%

- 2.3. Water Content 46-49%

- 2.4. Water Content 50%

Harder Cheese Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Harder Cheese Regional Market Share

Geographic Coverage of Harder Cheese

Harder Cheese REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.15% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Harder Cheese Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Supermarkets/Hypermarkets

- 5.1.2. Departmental Stores

- 5.1.3. Speciality Stores

- 5.1.4. Online Retail

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Water Content 40%

- 5.2.2. Water Content 41-45%

- 5.2.3. Water Content 46-49%

- 5.2.4. Water Content 50%

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Harder Cheese Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Supermarkets/Hypermarkets

- 6.1.2. Departmental Stores

- 6.1.3. Speciality Stores

- 6.1.4. Online Retail

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Water Content 40%

- 6.2.2. Water Content 41-45%

- 6.2.3. Water Content 46-49%

- 6.2.4. Water Content 50%

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Harder Cheese Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Supermarkets/Hypermarkets

- 7.1.2. Departmental Stores

- 7.1.3. Speciality Stores

- 7.1.4. Online Retail

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Water Content 40%

- 7.2.2. Water Content 41-45%

- 7.2.3. Water Content 46-49%

- 7.2.4. Water Content 50%

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Harder Cheese Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Supermarkets/Hypermarkets

- 8.1.2. Departmental Stores

- 8.1.3. Speciality Stores

- 8.1.4. Online Retail

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Water Content 40%

- 8.2.2. Water Content 41-45%

- 8.2.3. Water Content 46-49%

- 8.2.4. Water Content 50%

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Harder Cheese Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Supermarkets/Hypermarkets

- 9.1.2. Departmental Stores

- 9.1.3. Speciality Stores

- 9.1.4. Online Retail

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Water Content 40%

- 9.2.2. Water Content 41-45%

- 9.2.3. Water Content 46-49%

- 9.2.4. Water Content 50%

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Harder Cheese Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Supermarkets/Hypermarkets

- 10.1.2. Departmental Stores

- 10.1.3. Speciality Stores

- 10.1.4. Online Retail

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Water Content 40%

- 10.2.2. Water Content 41-45%

- 10.2.3. Water Content 46-49%

- 10.2.4. Water Content 50%

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Granarolo

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Eurial

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Couturier North America

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 CASA Radicci

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Flanders Milk/Ets Freddy Baines

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Winona Foods

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 St. Paul

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Mammen Dairy

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 DONIDO

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Tetra Pak

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Vindija

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Granarolo

List of Figures

- Figure 1: Global Harder Cheese Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Harder Cheese Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Harder Cheese Revenue (billion), by Application 2025 & 2033

- Figure 4: North America Harder Cheese Volume (K), by Application 2025 & 2033

- Figure 5: North America Harder Cheese Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Harder Cheese Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Harder Cheese Revenue (billion), by Types 2025 & 2033

- Figure 8: North America Harder Cheese Volume (K), by Types 2025 & 2033

- Figure 9: North America Harder Cheese Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Harder Cheese Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Harder Cheese Revenue (billion), by Country 2025 & 2033

- Figure 12: North America Harder Cheese Volume (K), by Country 2025 & 2033

- Figure 13: North America Harder Cheese Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Harder Cheese Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Harder Cheese Revenue (billion), by Application 2025 & 2033

- Figure 16: South America Harder Cheese Volume (K), by Application 2025 & 2033

- Figure 17: South America Harder Cheese Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Harder Cheese Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Harder Cheese Revenue (billion), by Types 2025 & 2033

- Figure 20: South America Harder Cheese Volume (K), by Types 2025 & 2033

- Figure 21: South America Harder Cheese Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Harder Cheese Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Harder Cheese Revenue (billion), by Country 2025 & 2033

- Figure 24: South America Harder Cheese Volume (K), by Country 2025 & 2033

- Figure 25: South America Harder Cheese Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Harder Cheese Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Harder Cheese Revenue (billion), by Application 2025 & 2033

- Figure 28: Europe Harder Cheese Volume (K), by Application 2025 & 2033

- Figure 29: Europe Harder Cheese Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Harder Cheese Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Harder Cheese Revenue (billion), by Types 2025 & 2033

- Figure 32: Europe Harder Cheese Volume (K), by Types 2025 & 2033

- Figure 33: Europe Harder Cheese Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Harder Cheese Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Harder Cheese Revenue (billion), by Country 2025 & 2033

- Figure 36: Europe Harder Cheese Volume (K), by Country 2025 & 2033

- Figure 37: Europe Harder Cheese Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Harder Cheese Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Harder Cheese Revenue (billion), by Application 2025 & 2033

- Figure 40: Middle East & Africa Harder Cheese Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Harder Cheese Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Harder Cheese Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Harder Cheese Revenue (billion), by Types 2025 & 2033

- Figure 44: Middle East & Africa Harder Cheese Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Harder Cheese Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Harder Cheese Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Harder Cheese Revenue (billion), by Country 2025 & 2033

- Figure 48: Middle East & Africa Harder Cheese Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Harder Cheese Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Harder Cheese Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Harder Cheese Revenue (billion), by Application 2025 & 2033

- Figure 52: Asia Pacific Harder Cheese Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Harder Cheese Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Harder Cheese Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Harder Cheese Revenue (billion), by Types 2025 & 2033

- Figure 56: Asia Pacific Harder Cheese Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Harder Cheese Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Harder Cheese Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Harder Cheese Revenue (billion), by Country 2025 & 2033

- Figure 60: Asia Pacific Harder Cheese Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Harder Cheese Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Harder Cheese Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Harder Cheese Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Harder Cheese Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Harder Cheese Revenue billion Forecast, by Types 2020 & 2033

- Table 4: Global Harder Cheese Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Harder Cheese Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Harder Cheese Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Harder Cheese Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Global Harder Cheese Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Harder Cheese Revenue billion Forecast, by Types 2020 & 2033

- Table 10: Global Harder Cheese Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Harder Cheese Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global Harder Cheese Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Harder Cheese Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United States Harder Cheese Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Harder Cheese Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Harder Cheese Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Harder Cheese Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Mexico Harder Cheese Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Harder Cheese Revenue billion Forecast, by Application 2020 & 2033

- Table 20: Global Harder Cheese Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Harder Cheese Revenue billion Forecast, by Types 2020 & 2033

- Table 22: Global Harder Cheese Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Harder Cheese Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global Harder Cheese Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Harder Cheese Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Brazil Harder Cheese Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Harder Cheese Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Argentina Harder Cheese Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Harder Cheese Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Harder Cheese Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Harder Cheese Revenue billion Forecast, by Application 2020 & 2033

- Table 32: Global Harder Cheese Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Harder Cheese Revenue billion Forecast, by Types 2020 & 2033

- Table 34: Global Harder Cheese Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Harder Cheese Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global Harder Cheese Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Harder Cheese Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Harder Cheese Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Harder Cheese Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Germany Harder Cheese Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Harder Cheese Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: France Harder Cheese Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Harder Cheese Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Italy Harder Cheese Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Harder Cheese Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Spain Harder Cheese Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Harder Cheese Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Russia Harder Cheese Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Harder Cheese Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Benelux Harder Cheese Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Harder Cheese Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Nordics Harder Cheese Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Harder Cheese Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Harder Cheese Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Harder Cheese Revenue billion Forecast, by Application 2020 & 2033

- Table 56: Global Harder Cheese Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Harder Cheese Revenue billion Forecast, by Types 2020 & 2033

- Table 58: Global Harder Cheese Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Harder Cheese Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global Harder Cheese Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Harder Cheese Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Turkey Harder Cheese Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Harder Cheese Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Israel Harder Cheese Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Harder Cheese Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: GCC Harder Cheese Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Harder Cheese Revenue (billion) Forecast, by Application 2020 & 2033

- Table 68: North Africa Harder Cheese Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Harder Cheese Revenue (billion) Forecast, by Application 2020 & 2033

- Table 70: South Africa Harder Cheese Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Harder Cheese Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Harder Cheese Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Harder Cheese Revenue billion Forecast, by Application 2020 & 2033

- Table 74: Global Harder Cheese Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Harder Cheese Revenue billion Forecast, by Types 2020 & 2033

- Table 76: Global Harder Cheese Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Harder Cheese Revenue billion Forecast, by Country 2020 & 2033

- Table 78: Global Harder Cheese Volume K Forecast, by Country 2020 & 2033

- Table 79: China Harder Cheese Revenue (billion) Forecast, by Application 2020 & 2033

- Table 80: China Harder Cheese Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Harder Cheese Revenue (billion) Forecast, by Application 2020 & 2033

- Table 82: India Harder Cheese Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Harder Cheese Revenue (billion) Forecast, by Application 2020 & 2033

- Table 84: Japan Harder Cheese Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Harder Cheese Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: South Korea Harder Cheese Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Harder Cheese Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Harder Cheese Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Harder Cheese Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: Oceania Harder Cheese Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Harder Cheese Revenue (billion) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Harder Cheese Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Harder Cheese?

The projected CAGR is approximately 5.15%.

2. Which companies are prominent players in the Harder Cheese?

Key companies in the market include Granarolo, Eurial, Couturier North America, CASA Radicci, Flanders Milk/Ets Freddy Baines, Winona Foods, St. Paul, Mammen Dairy, DONIDO, Tetra Pak, Vindija.

3. What are the main segments of the Harder Cheese?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 199.14 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Harder Cheese," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Harder Cheese report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Harder Cheese?

To stay informed about further developments, trends, and reports in the Harder Cheese, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence