Key Insights

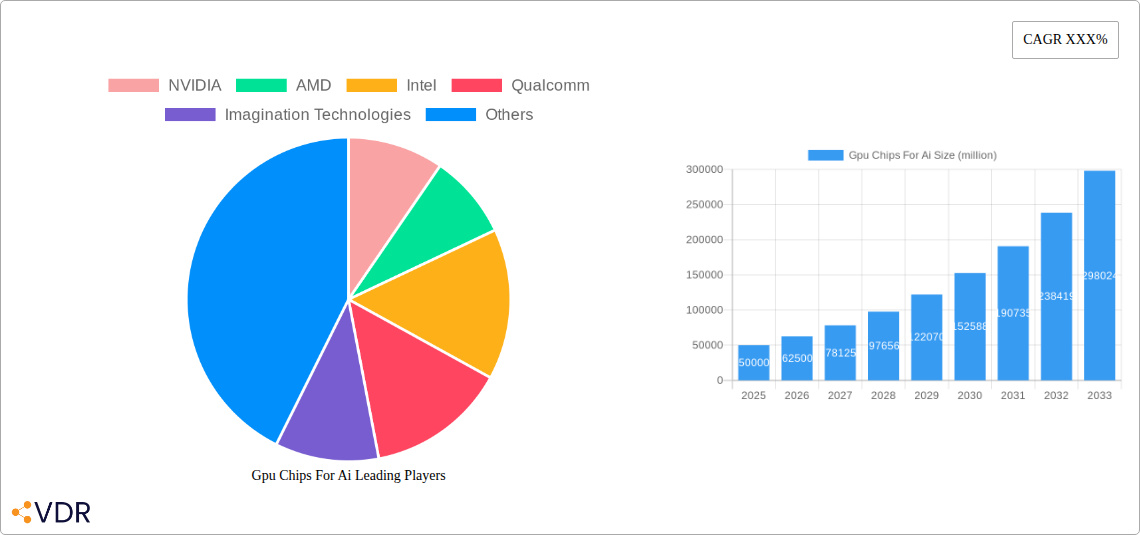

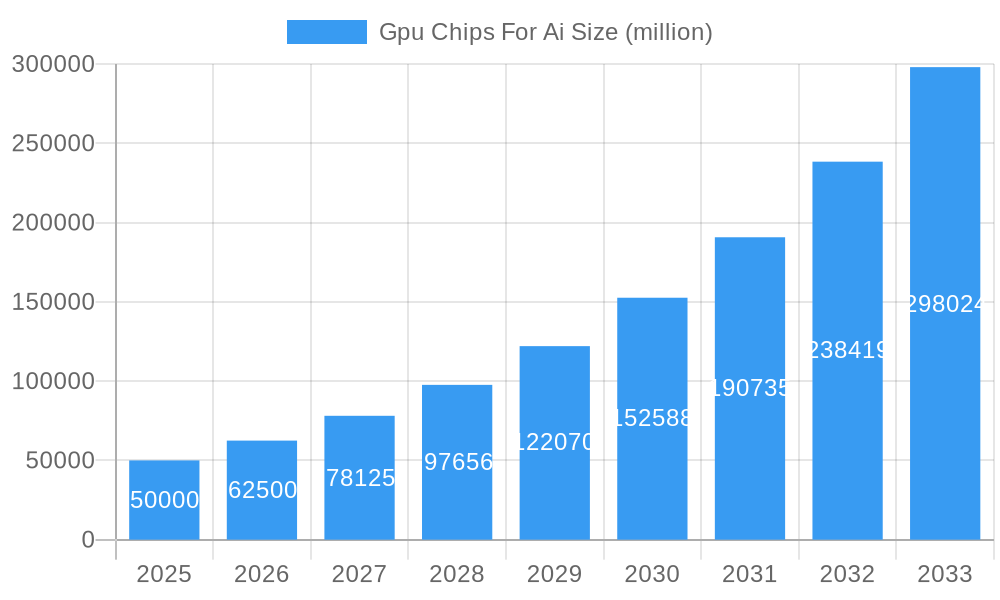

The global market for GPU chips for AI is experiencing robust expansion, projected to reach approximately $50,000 million by 2025, with a compelling Compound Annual Growth Rate (CAGR) of around 25% anticipated throughout the forecast period of 2025-2033. This surge is primarily propelled by the insatiable demand for advanced artificial intelligence capabilities across various sectors. The escalating adoption of AI in areas like AI Reasoning, AI Training, and High-Performance Computing (HPC) necessitates increasingly powerful and specialized GPU architectures. Key drivers include the exponential growth in data volumes requiring complex processing, the development of sophisticated AI algorithms, and the widespread deployment of AI-powered applications in industries such as autonomous vehicles, healthcare diagnostics, natural language processing, and personalized content delivery. Furthermore, the ongoing advancements in chip architecture, memory bandwidth, and parallel processing capabilities by leading players are instrumental in fueling this market growth.

Gpu Chips For Ai Market Size (In Billion)

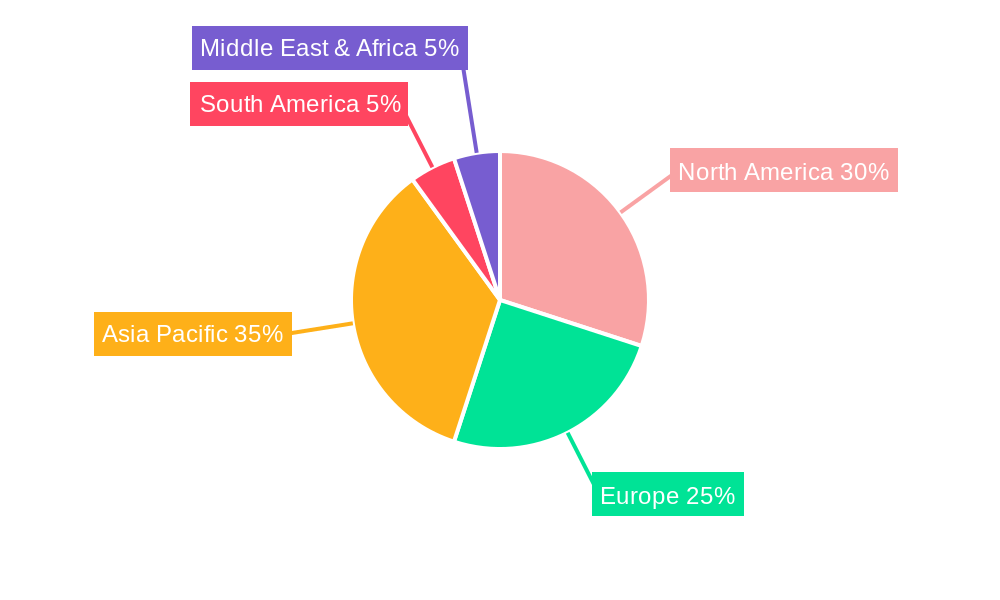

Despite the promising outlook, certain restraints could influence the market's trajectory. High manufacturing costs associated with cutting-edge GPU fabrication and the intense competition among established and emerging players, particularly in the rapidly evolving AI chip landscape, present challenges. Supply chain disruptions and geopolitical factors impacting semiconductor production could also pose significant hurdles. The market segmentation reveals a strong demand for higher-capacity GPUs, with the "24G Above" segment expected to witness the most significant growth, reflecting the increasing computational demands of advanced AI models. Geographically, Asia Pacific, led by China, is emerging as a dominant force due to its extensive AI research and development initiatives and a burgeoning manufacturing ecosystem. North America and Europe also represent substantial markets driven by significant investments in AI innovation and adoption. The competitive landscape is characterized by the dominance of NVIDIA, AMD, and Intel, alongside the strategic moves of Qualcomm, Imagination Technologies, and a host of dynamic Chinese players like Changsha Jingjia Microelectronics and Shanghai Biren Intelligent Technology, all vying for market share in this high-growth sector.

Gpu Chips For Ai Company Market Share

GPU Chips for AI Market: Comprehensive Report Analysis and Future Outlook

This in-depth report provides a definitive analysis of the global GPU chips for AI market, offering critical insights for stakeholders in the rapidly evolving artificial intelligence landscape. Covering a comprehensive study period from 2019 to 2033, with a base year of 2025 and a forecast period of 2025–2033, this report delves into market dynamics, growth trends, regional dominance, product landscapes, and the strategic imperatives shaping the industry. We analyze the competitive arena, technological advancements, and emerging opportunities, presenting a data-driven outlook for this high-growth sector.

GPU Chips For Ai Market Dynamics & Structure

The GPU chips for AI market is characterized by intense technological innovation and a dynamic competitive landscape. NVIDIA currently holds a dominant market share, estimated at approximately 65% in 2025, driven by its CUDA architecture and extensive software ecosystem. AMD is a key competitor, focusing on expanding its offerings in both training and inference, aiming for a 20% market share. Intel, through its acquisitions and ongoing development of dedicated AI accelerators, is also a significant player, projected to capture 10% of the market. Emerging players like Qualcomm, with its integrated AI solutions, and Chinese companies such as Changsha Jingjia Microelectronics and Hangjintechnology, are contributing to market diversification, particularly in specific segments and regional markets. Regulatory frameworks are increasingly influencing the market, with export controls and national semiconductor initiatives playing a role. The primary drivers of innovation include the escalating demand for AI training and inference capabilities, the development of more complex AI models, and the push for greater power efficiency. Competitive product substitutes, while limited for high-performance AI training, are emerging in the inference segment with ASICs and specialized NPUs. End-user demographics are broad, encompassing hyperscale cloud providers, enterprise data centers, automotive manufacturers, and research institutions. Mergers and acquisitions remain a key strategy for consolidation and technology acquisition, with an estimated 3-5 significant deals annually in the broader semiconductor and AI chip space. Barriers to innovation include the immense R&D costs, long product development cycles, and the need for specialized talent.

- Market Concentration: Dominated by NVIDIA, with significant contributions from AMD and Intel.

- Technological Innovation Drivers: Demand for AI training/inference, complex models, power efficiency.

- Regulatory Frameworks: Export controls, national semiconductor policies impacting global trade.

- Competitive Product Substitutes: ASICs and NPUs emerging in the inference market.

- End-User Demographics: Cloud providers, enterprises, automotive, research.

- M&A Trends: Consolidation and technology acquisition as a strategic imperative.

- Innovation Barriers: High R&D costs, long development cycles, talent scarcity.

GPU Chips For Ai Growth Trends & Insights

The global GPU chips for AI market is experiencing unprecedented growth, projected to surge from an estimated XX billion units in 2025 to XX billion units by 2033, reflecting a robust Compound Annual Growth Rate (CAGR) of approximately 28%. This explosive expansion is fueled by the ubiquitous integration of artificial intelligence across diverse industries. The primary catalyst remains the burgeoning demand for AI training, where massive datasets and complex neural networks require the immense parallel processing power offered by GPUs. In 2025, the AI training segment is expected to account for over 50% of the total market demand, followed by AI reasoning at approximately 30%, and High Performance Computing (HPC) at 15%. The remaining 5% is attributed to other niche applications.

GPU adoption rates are accelerating as more organizations recognize the transformative potential of AI. This trend is particularly evident in the hyperscale cloud computing sector, where major providers are continuously investing in GPU infrastructure to offer AI-as-a-service. Enterprise adoption is also gaining momentum, with businesses leveraging GPUs for tasks ranging from predictive analytics and natural language processing to computer vision and drug discovery. Technological disruptions are continuously reshaping the market. The evolution from discrete GPUs to integrated solutions and the development of specialized AI accelerators are key trends. Furthermore, advancements in chip architectures, such as increased Tensor Core performance and optimized memory bandwidth, are enhancing processing capabilities for AI workloads.

Consumer behavior shifts are also indirectly influencing GPU demand. The growing popularity of AI-powered applications, from virtual assistants and personalized recommendations to advanced gaming experiences and generative AI tools, is creating a snowball effect, driving further research and development in GPU hardware. The market is witnessing a significant increase in the demand for higher memory capacities, with the 24G Above segment expected to grow at the fastest CAGR, driven by the requirements of large language models (LLMs) and complex deep learning tasks. Conversely, the 8G Below segment is projected to see a slower growth trajectory, primarily catering to specific edge AI applications and lower-inference tasks. The 8G-16G and 16G-24G segments will continue to serve a broad range of AI workloads, balancing performance and cost-effectiveness.

The shift towards AI ubiquity is not merely a trend but a fundamental transformation. Organizations are no longer questioning the 'if' but the 'how' and 'when' of AI integration. This necessitates a constant upgrade cycle for GPU hardware to keep pace with the ever-increasing computational demands of AI algorithms. The market penetration of GPUs specifically designed and optimized for AI workloads is expected to reach over 70% by 2030. This pervasive adoption underscores the critical role of GPU chips as the bedrock of the AI revolution. The interplay between hardware innovation, software optimization, and the ever-expanding scope of AI applications will continue to propel this market forward at an astonishing pace.

Dominant Regions, Countries, or Segments in Gpu Chips For Ai

The Artificial Intelligence Training segment is unequivocally the dominant force driving growth in the global GPU chips for AI market. In 2025, this segment is estimated to command a substantial XX% of the total market value, projected to reach XX billion units. This dominance is attributed to the insatiable demand for computational power required to train increasingly complex deep learning models, which underpin advancements in fields like natural language processing, computer vision, and autonomous systems. The sheer scale of data involved in training these models necessitates high-performance GPUs with massive parallel processing capabilities and substantial memory bandwidth.

Regionally, North America, led by the United States, is the primary driver of GPU chip demand for AI, accounting for an estimated XX% of the global market in 2025. This leadership is fueled by the presence of major hyperscale cloud providers (e.g., Google, Amazon, Microsoft), leading AI research institutions, and a vibrant ecosystem of AI startups. The U.S. government's significant investments in AI research and development, coupled with favorable economic policies and robust venture capital funding, further bolster this dominance. The demand from North America is primarily concentrated within the 24G Above memory segment, as leading organizations push the boundaries of AI model complexity. The country's robust infrastructure and access to cutting-edge technology enable the widespread adoption of the most advanced GPU architectures for training tasks.

Following closely is Asia-Pacific, which is projected to exhibit the highest growth rate in the coming years, driven by China's aggressive push in AI development and manufacturing capabilities. China's demand is increasingly significant in both AI Training and AI Reasoning, with a growing emphasis on domestic production and the development of its own AI semiconductor ecosystem. Countries like South Korea and Japan are also contributing to the regional demand, particularly in HPC and advanced AI applications. The 16G-24G and 24G Above segments are experiencing rapid expansion in this region as well, reflecting the escalating scale of AI projects.

Europe is another key region, with a significant presence in AI Reasoning and High Performance Computing. Germany, the UK, and France are leading the charge, with a focus on AI integration in industries such as automotive, healthcare, and manufacturing. The 8G-16G and 16G-24G memory segments are particularly strong in Europe, catering to a diverse range of enterprise AI deployments.

The dominance of AI Training as a segment is directly linked to the continuous advancements in AI algorithms and the exponential growth in data generation. The need for powerful GPUs for this purpose transcends geographical boundaries and drives innovation across all regions. The 24G Above memory segment, specifically, is crucial for training the largest and most sophisticated AI models, making it a key indicator of the market's cutting-edge developments. The growth potential within this segment is immense, driven by the ongoing arms race in AI capabilities.

GPU Chips For Ai Product Landscape

The GPU chips for AI market is defined by a rapid pace of product innovation, characterized by increasingly powerful and specialized hardware designed to accelerate AI workloads. Companies are focused on enhancing core performance metrics such as TeraFLOPS (TFLOPS) for AI operations, memory bandwidth, and energy efficiency. NVIDIA's Hopper and Ampere architectures, for instance, deliver unprecedented performance for AI training and inference. AMD is making strides with its CDNA architecture, aiming to provide competitive solutions for data centers and AI workloads. Intel's Ponte Vecchio and future generations of AI accelerators are designed to address the growing demand for heterogeneous computing. Qualcomm is focusing on integrated AI solutions for edge devices and automotive applications. These products are increasingly differentiated by their memory capacities, with the 24G Above segment gaining prominence for its ability to handle massive datasets and complex models. Unique selling propositions include optimized Tensor Cores, advanced interconnect technologies for multi-GPU scaling, and robust software support ecosystems like CUDA and ROCm, which are critical for widespread adoption and efficient deployment of AI applications.

Key Drivers, Barriers & Challenges in Gpu Chips For Ai

The GPU chips for AI market is propelled by several key drivers. The exponential growth in AI adoption across industries, including autonomous vehicles, healthcare, finance, and entertainment, is creating an insatiable demand for computational power. Advancements in deep learning algorithms, requiring increasingly complex neural networks, necessitate more powerful and efficient GPUs. High-performance computing (HPC) applications, which often overlap with AI workloads, also contribute significantly to demand. Furthermore, government initiatives and investments in AI research and development globally are fostering market growth.

However, the market faces significant barriers and challenges. The high cost of advanced AI GPUs remains a considerable hurdle for smaller enterprises and research institutions. Supply chain disruptions, exacerbated by geopolitical factors and semiconductor shortages, can impact availability and lead times, affecting market expansion. Intense competition and the need for continuous R&D to stay ahead of technological curves place immense pressure on manufacturers. Regulatory hurdles, such as export controls on advanced semiconductor technology, can also restrict market access for certain regions and companies. Talent scarcity in AI hardware design and optimization further compounds these challenges.

Emerging Opportunities in Gpu Chips For Ai

Emerging opportunities in the GPU chips for AI market lie in several key areas. The burgeoning edge AI segment presents a substantial growth avenue, with demand for power-efficient, compact GPUs for applications in IoT devices, smart cameras, and robotics. The development of specialized AI accelerators beyond general-purpose GPUs, such as ASICs and FPGAs tailored for specific AI tasks like natural language processing or computer vision, offers a niche but growing market. Furthermore, the increasing focus on sustainability and energy efficiency in AI computing creates opportunities for developing greener GPU solutions with lower power consumption. The expansion of AI into new verticals such as climate modeling, personalized medicine, and advanced materials science will also unlock new demand for specialized GPU capabilities.

Growth Accelerators in the Gpu Chips For Ai Industry

Several catalysts are accelerating the long-term growth of the GPU chips for AI industry. Technological breakthroughs in chip manufacturing processes, such as advancements in node technology and 3D stacking, are enabling the creation of more powerful and cost-effective GPUs. Strategic partnerships between GPU manufacturers and AI software developers are crucial for optimizing performance and ensuring seamless integration of hardware and software. The expanding ecosystem of AI development tools and frameworks, often open-source, lowers the barrier to entry for developers, further fueling demand for GPU resources. Market expansion strategies, including aggressive pricing for enterprise solutions and the development of specialized offerings for emerging markets, are also playing a vital role in driving sustained growth. The increasing adoption of AI in critical sectors like healthcare and scientific research guarantees a continuous demand for high-performance computing power.

Key Players Shaping the Gpu Chips For Ai Market

- NVIDIA

- AMD

- Intel

- Qualcomm

- Imagination Technologies

- Changsha Jingjia Microelectronics

- Hangjintechnology

- VeriSilicon Microelectronics

- Shanghai Biren Intelligent Technolog

- Loongson Technology Corporation

- Shanghai Megacore Integrated Circuit

- MetaX

- Sietium

- Enflame-tech

- Beijing Horizon Robotics Technology R&D

- Blacksesame

- Innosilicon Technology

- HiSilicon Technologies

- Iluvatar

- Vastai Technologies

Notable Milestones in Gpu Chips For Ai Sector

- 2019: NVIDIA introduces the NVIDIA T4 Tensor Core GPU, enhancing AI inference performance.

- 2020: AMD launches its Instinct MI100 GPU, a significant step forward for its data center AI offerings.

- 2021: Intel unveils its first data center GPU, Ponte Vecchio, targeting HPC and AI workloads.

- 2021: Qualcomm announces its AI Engine for automotive applications, integrating GPU capabilities.

- 2022: NVIDIA releases the H100 Tensor Core GPU, setting new benchmarks for AI training.

- 2022: China intensifies efforts in domestic chip manufacturing, with companies like Changsha Jingjia Microelectronics gaining prominence.

- 2023: The rise of large language models (LLMs) significantly boosts demand for high-memory GPUs (24G Above).

- 2023: Growing geopolitical tensions lead to increased focus on regional semiconductor supply chains and government incentives.

- 2024: Continued advancements in chip architecture and manufacturing processes promise further performance gains and efficiency improvements.

- 2024: Increased investment in AI inference chips for edge computing and deployment on consumer devices.

In-Depth Gpu Chips For Ai Market Outlook

The future outlook for the GPU chips for AI market is exceptionally bright, driven by sustained innovation and expanding applications. Growth accelerators such as next-generation chip architectures, strategic alliances between hardware vendors and AI software pioneers, and the continuous emergence of novel AI applications will fuel demand. The market is poised for significant expansion as AI becomes more deeply embedded in global industries and everyday life. The increasing need for specialized AI hardware, coupled with ongoing advancements in manufacturing technologies, will ensure a dynamic and rapidly evolving landscape. Stakeholders can anticipate continued strong growth, with opportunities arising from edge AI, advanced HPC, and the development of more efficient and sustainable AI computing solutions. This sector remains a cornerstone of technological progress, promising substantial returns for those who can navigate its complexities.

Gpu Chips For Ai Segmentation

-

1. Application

- 1.1. Artificial Intelligence Reasoning

- 1.2. Artificial Intelligence Training

- 1.3. High Performance Computing

- 1.4. Others

-

2. Type

- 2.1. 8G Below

- 2.2. 8G-16G

- 2.3. 16G-24G

- 2.4. 24G Above

Gpu Chips For Ai Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Gpu Chips For Ai Regional Market Share

Geographic Coverage of Gpu Chips For Ai

Gpu Chips For Ai REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XXX% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Gpu Chips For Ai Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Artificial Intelligence Reasoning

- 5.1.2. Artificial Intelligence Training

- 5.1.3. High Performance Computing

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. 8G Below

- 5.2.2. 8G-16G

- 5.2.3. 16G-24G

- 5.2.4. 24G Above

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Gpu Chips For Ai Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Artificial Intelligence Reasoning

- 6.1.2. Artificial Intelligence Training

- 6.1.3. High Performance Computing

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. 8G Below

- 6.2.2. 8G-16G

- 6.2.3. 16G-24G

- 6.2.4. 24G Above

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Gpu Chips For Ai Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Artificial Intelligence Reasoning

- 7.1.2. Artificial Intelligence Training

- 7.1.3. High Performance Computing

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. 8G Below

- 7.2.2. 8G-16G

- 7.2.3. 16G-24G

- 7.2.4. 24G Above

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Gpu Chips For Ai Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Artificial Intelligence Reasoning

- 8.1.2. Artificial Intelligence Training

- 8.1.3. High Performance Computing

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. 8G Below

- 8.2.2. 8G-16G

- 8.2.3. 16G-24G

- 8.2.4. 24G Above

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Gpu Chips For Ai Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Artificial Intelligence Reasoning

- 9.1.2. Artificial Intelligence Training

- 9.1.3. High Performance Computing

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. 8G Below

- 9.2.2. 8G-16G

- 9.2.3. 16G-24G

- 9.2.4. 24G Above

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Gpu Chips For Ai Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Artificial Intelligence Reasoning

- 10.1.2. Artificial Intelligence Training

- 10.1.3. High Performance Computing

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. 8G Below

- 10.2.2. 8G-16G

- 10.2.3. 16G-24G

- 10.2.4. 24G Above

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 NVIDIA

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 AMD

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Intel

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Qualcomm

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Imagination Technologies

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Changsha Jingjia Microelectronics

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Hangjintechnology

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 VeriSilicon Microelectronics

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Shanghai Biren Intelligent Technolog

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Loongson Technology Corporation

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Shanghai Megacore Integrated Circuit

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 MetaX

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Sietium

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Enflame-tech

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Beijing Horizon Robotics Technology R&D

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Blacksesame

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Innosilicon Technology

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 HiSilicon Technologies

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Iluvatar

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Vastai Technologies

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.1 NVIDIA

List of Figures

- Figure 1: Global Gpu Chips For Ai Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: Global Gpu Chips For Ai Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Gpu Chips For Ai Revenue (million), by Application 2025 & 2033

- Figure 4: North America Gpu Chips For Ai Volume (K), by Application 2025 & 2033

- Figure 5: North America Gpu Chips For Ai Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Gpu Chips For Ai Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Gpu Chips For Ai Revenue (million), by Type 2025 & 2033

- Figure 8: North America Gpu Chips For Ai Volume (K), by Type 2025 & 2033

- Figure 9: North America Gpu Chips For Ai Revenue Share (%), by Type 2025 & 2033

- Figure 10: North America Gpu Chips For Ai Volume Share (%), by Type 2025 & 2033

- Figure 11: North America Gpu Chips For Ai Revenue (million), by Country 2025 & 2033

- Figure 12: North America Gpu Chips For Ai Volume (K), by Country 2025 & 2033

- Figure 13: North America Gpu Chips For Ai Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Gpu Chips For Ai Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Gpu Chips For Ai Revenue (million), by Application 2025 & 2033

- Figure 16: South America Gpu Chips For Ai Volume (K), by Application 2025 & 2033

- Figure 17: South America Gpu Chips For Ai Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Gpu Chips For Ai Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Gpu Chips For Ai Revenue (million), by Type 2025 & 2033

- Figure 20: South America Gpu Chips For Ai Volume (K), by Type 2025 & 2033

- Figure 21: South America Gpu Chips For Ai Revenue Share (%), by Type 2025 & 2033

- Figure 22: South America Gpu Chips For Ai Volume Share (%), by Type 2025 & 2033

- Figure 23: South America Gpu Chips For Ai Revenue (million), by Country 2025 & 2033

- Figure 24: South America Gpu Chips For Ai Volume (K), by Country 2025 & 2033

- Figure 25: South America Gpu Chips For Ai Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Gpu Chips For Ai Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Gpu Chips For Ai Revenue (million), by Application 2025 & 2033

- Figure 28: Europe Gpu Chips For Ai Volume (K), by Application 2025 & 2033

- Figure 29: Europe Gpu Chips For Ai Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Gpu Chips For Ai Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Gpu Chips For Ai Revenue (million), by Type 2025 & 2033

- Figure 32: Europe Gpu Chips For Ai Volume (K), by Type 2025 & 2033

- Figure 33: Europe Gpu Chips For Ai Revenue Share (%), by Type 2025 & 2033

- Figure 34: Europe Gpu Chips For Ai Volume Share (%), by Type 2025 & 2033

- Figure 35: Europe Gpu Chips For Ai Revenue (million), by Country 2025 & 2033

- Figure 36: Europe Gpu Chips For Ai Volume (K), by Country 2025 & 2033

- Figure 37: Europe Gpu Chips For Ai Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Gpu Chips For Ai Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Gpu Chips For Ai Revenue (million), by Application 2025 & 2033

- Figure 40: Middle East & Africa Gpu Chips For Ai Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Gpu Chips For Ai Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Gpu Chips For Ai Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Gpu Chips For Ai Revenue (million), by Type 2025 & 2033

- Figure 44: Middle East & Africa Gpu Chips For Ai Volume (K), by Type 2025 & 2033

- Figure 45: Middle East & Africa Gpu Chips For Ai Revenue Share (%), by Type 2025 & 2033

- Figure 46: Middle East & Africa Gpu Chips For Ai Volume Share (%), by Type 2025 & 2033

- Figure 47: Middle East & Africa Gpu Chips For Ai Revenue (million), by Country 2025 & 2033

- Figure 48: Middle East & Africa Gpu Chips For Ai Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Gpu Chips For Ai Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Gpu Chips For Ai Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Gpu Chips For Ai Revenue (million), by Application 2025 & 2033

- Figure 52: Asia Pacific Gpu Chips For Ai Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Gpu Chips For Ai Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Gpu Chips For Ai Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Gpu Chips For Ai Revenue (million), by Type 2025 & 2033

- Figure 56: Asia Pacific Gpu Chips For Ai Volume (K), by Type 2025 & 2033

- Figure 57: Asia Pacific Gpu Chips For Ai Revenue Share (%), by Type 2025 & 2033

- Figure 58: Asia Pacific Gpu Chips For Ai Volume Share (%), by Type 2025 & 2033

- Figure 59: Asia Pacific Gpu Chips For Ai Revenue (million), by Country 2025 & 2033

- Figure 60: Asia Pacific Gpu Chips For Ai Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Gpu Chips For Ai Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Gpu Chips For Ai Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Gpu Chips For Ai Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Gpu Chips For Ai Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Gpu Chips For Ai Revenue million Forecast, by Type 2020 & 2033

- Table 4: Global Gpu Chips For Ai Volume K Forecast, by Type 2020 & 2033

- Table 5: Global Gpu Chips For Ai Revenue million Forecast, by Region 2020 & 2033

- Table 6: Global Gpu Chips For Ai Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Gpu Chips For Ai Revenue million Forecast, by Application 2020 & 2033

- Table 8: Global Gpu Chips For Ai Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Gpu Chips For Ai Revenue million Forecast, by Type 2020 & 2033

- Table 10: Global Gpu Chips For Ai Volume K Forecast, by Type 2020 & 2033

- Table 11: Global Gpu Chips For Ai Revenue million Forecast, by Country 2020 & 2033

- Table 12: Global Gpu Chips For Ai Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Gpu Chips For Ai Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: United States Gpu Chips For Ai Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Gpu Chips For Ai Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Canada Gpu Chips For Ai Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Gpu Chips For Ai Revenue (million) Forecast, by Application 2020 & 2033

- Table 18: Mexico Gpu Chips For Ai Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Gpu Chips For Ai Revenue million Forecast, by Application 2020 & 2033

- Table 20: Global Gpu Chips For Ai Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Gpu Chips For Ai Revenue million Forecast, by Type 2020 & 2033

- Table 22: Global Gpu Chips For Ai Volume K Forecast, by Type 2020 & 2033

- Table 23: Global Gpu Chips For Ai Revenue million Forecast, by Country 2020 & 2033

- Table 24: Global Gpu Chips For Ai Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Gpu Chips For Ai Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Brazil Gpu Chips For Ai Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Gpu Chips For Ai Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Argentina Gpu Chips For Ai Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Gpu Chips For Ai Revenue (million) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Gpu Chips For Ai Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Gpu Chips For Ai Revenue million Forecast, by Application 2020 & 2033

- Table 32: Global Gpu Chips For Ai Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Gpu Chips For Ai Revenue million Forecast, by Type 2020 & 2033

- Table 34: Global Gpu Chips For Ai Volume K Forecast, by Type 2020 & 2033

- Table 35: Global Gpu Chips For Ai Revenue million Forecast, by Country 2020 & 2033

- Table 36: Global Gpu Chips For Ai Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Gpu Chips For Ai Revenue (million) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Gpu Chips For Ai Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Gpu Chips For Ai Revenue (million) Forecast, by Application 2020 & 2033

- Table 40: Germany Gpu Chips For Ai Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Gpu Chips For Ai Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: France Gpu Chips For Ai Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Gpu Chips For Ai Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: Italy Gpu Chips For Ai Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Gpu Chips For Ai Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Spain Gpu Chips For Ai Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Gpu Chips For Ai Revenue (million) Forecast, by Application 2020 & 2033

- Table 48: Russia Gpu Chips For Ai Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Gpu Chips For Ai Revenue (million) Forecast, by Application 2020 & 2033

- Table 50: Benelux Gpu Chips For Ai Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Gpu Chips For Ai Revenue (million) Forecast, by Application 2020 & 2033

- Table 52: Nordics Gpu Chips For Ai Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Gpu Chips For Ai Revenue (million) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Gpu Chips For Ai Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Gpu Chips For Ai Revenue million Forecast, by Application 2020 & 2033

- Table 56: Global Gpu Chips For Ai Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Gpu Chips For Ai Revenue million Forecast, by Type 2020 & 2033

- Table 58: Global Gpu Chips For Ai Volume K Forecast, by Type 2020 & 2033

- Table 59: Global Gpu Chips For Ai Revenue million Forecast, by Country 2020 & 2033

- Table 60: Global Gpu Chips For Ai Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Gpu Chips For Ai Revenue (million) Forecast, by Application 2020 & 2033

- Table 62: Turkey Gpu Chips For Ai Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Gpu Chips For Ai Revenue (million) Forecast, by Application 2020 & 2033

- Table 64: Israel Gpu Chips For Ai Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Gpu Chips For Ai Revenue (million) Forecast, by Application 2020 & 2033

- Table 66: GCC Gpu Chips For Ai Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Gpu Chips For Ai Revenue (million) Forecast, by Application 2020 & 2033

- Table 68: North Africa Gpu Chips For Ai Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Gpu Chips For Ai Revenue (million) Forecast, by Application 2020 & 2033

- Table 70: South Africa Gpu Chips For Ai Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Gpu Chips For Ai Revenue (million) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Gpu Chips For Ai Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Gpu Chips For Ai Revenue million Forecast, by Application 2020 & 2033

- Table 74: Global Gpu Chips For Ai Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Gpu Chips For Ai Revenue million Forecast, by Type 2020 & 2033

- Table 76: Global Gpu Chips For Ai Volume K Forecast, by Type 2020 & 2033

- Table 77: Global Gpu Chips For Ai Revenue million Forecast, by Country 2020 & 2033

- Table 78: Global Gpu Chips For Ai Volume K Forecast, by Country 2020 & 2033

- Table 79: China Gpu Chips For Ai Revenue (million) Forecast, by Application 2020 & 2033

- Table 80: China Gpu Chips For Ai Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Gpu Chips For Ai Revenue (million) Forecast, by Application 2020 & 2033

- Table 82: India Gpu Chips For Ai Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Gpu Chips For Ai Revenue (million) Forecast, by Application 2020 & 2033

- Table 84: Japan Gpu Chips For Ai Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Gpu Chips For Ai Revenue (million) Forecast, by Application 2020 & 2033

- Table 86: South Korea Gpu Chips For Ai Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Gpu Chips For Ai Revenue (million) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Gpu Chips For Ai Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Gpu Chips For Ai Revenue (million) Forecast, by Application 2020 & 2033

- Table 90: Oceania Gpu Chips For Ai Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Gpu Chips For Ai Revenue (million) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Gpu Chips For Ai Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Gpu Chips For Ai?

The projected CAGR is approximately XXX%.

2. Which companies are prominent players in the Gpu Chips For Ai?

Key companies in the market include NVIDIA, AMD, Intel, Qualcomm, Imagination Technologies, Changsha Jingjia Microelectronics, Hangjintechnology, VeriSilicon Microelectronics, Shanghai Biren Intelligent Technolog, Loongson Technology Corporation, Shanghai Megacore Integrated Circuit, MetaX, Sietium, Enflame-tech, Beijing Horizon Robotics Technology R&D, Blacksesame, Innosilicon Technology, HiSilicon Technologies, Iluvatar, Vastai Technologies.

3. What are the main segments of the Gpu Chips For Ai?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Gpu Chips For Ai," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Gpu Chips For Ai report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Gpu Chips For Ai?

To stay informed about further developments, trends, and reports in the Gpu Chips For Ai, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence