Key Insights

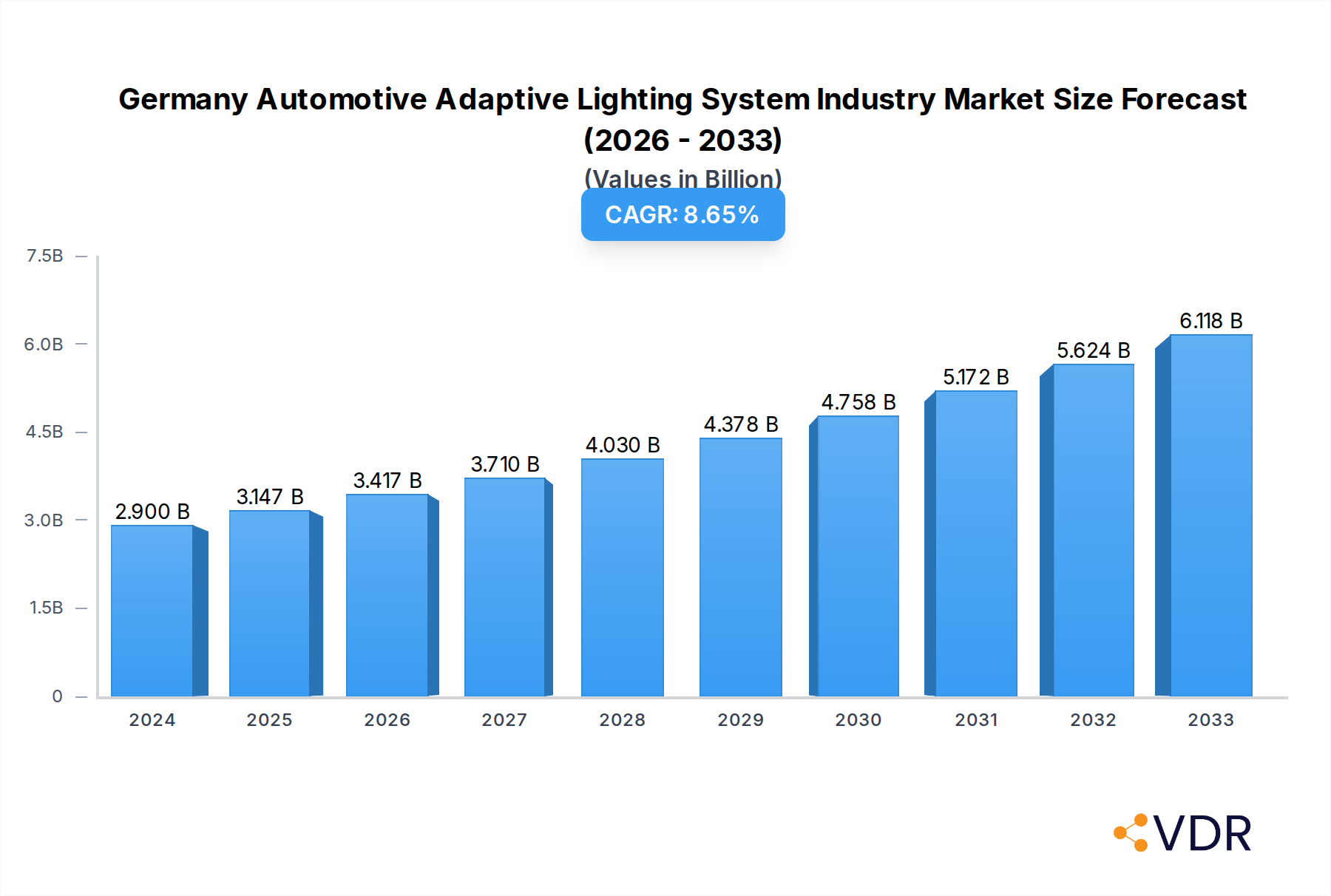

The German automotive adaptive lighting system market is poised for significant growth, driven by increasing demand for enhanced vehicle safety, improved driving comfort, and the integration of advanced driver-assistance systems (ADAS). With a robust automotive industry and stringent safety regulations, Germany is a key player in the adoption of innovative lighting technologies. The market size in 2024 is estimated to be €2.9 billion, projected to expand at a Compound Annual Growth Rate (CAGR) of 8.7% from 2025 to 2033. This growth is propelled by factors such as the rising adoption of LED and matrix LED technologies, the increasing sophistication of vehicle electronics, and consumer preference for premium features that enhance visibility and reduce driver fatigue. The trend towards autonomous driving further fuels the demand for intelligent lighting systems that can actively adapt to road conditions, traffic, and the environment.

Germany Automotive Adaptive Lighting System Industry Market Size (In Billion)

The market segmentation highlights key areas of development. Mid-segment passenger vehicles are increasingly featuring adaptive lighting, democratizing the technology. Within component types, controllers and sensors/cameras are critical for the intelligence of these systems, while lamp assemblies represent the core hardware. The OEM channel dominates sales, reflecting the integration of these systems from the manufacturing stage. Major companies like HELLA KGaA Hueck & Co., Osram, and Magneti Marelli SpA are at the forefront of innovation, developing advanced solutions. While the market benefits from strong drivers, potential restraints could include the initial high cost of advanced adaptive lighting systems and the complexity of integration, though ongoing technological advancements and economies of scale are expected to mitigate these challenges. The focus on sustainability and energy efficiency within the automotive sector also presents opportunities for the development of more power-efficient adaptive lighting solutions.

Germany Automotive Adaptive Lighting System Industry Company Market Share

This comprehensive report delves into the dynamic Germany Automotive Adaptive Lighting System Market, providing an in-depth analysis of its structure, growth trajectories, and future outlook from 2019 to 2033. With a base year of 2025, the study offers critical insights into parent and child market segments, crucial for automotive manufacturers, Tier-1 suppliers, technology providers, and investors navigating this rapidly evolving landscape. We meticulously examine the influence of cutting-edge technologies like adaptive front-lighting systems (AFS), matrix LED, and laser lighting on German automotive lighting advancements.

Germany Automotive Adaptive Lighting System Industry Market Dynamics & Structure

The Germany Automotive Adaptive Lighting System industry is characterized by a moderate market concentration, with a blend of established automotive giants and specialized lighting manufacturers. Technological innovation drivers are paramount, fueled by stringent safety regulations and a burgeoning consumer demand for advanced vehicle features. Key technologies like matrix LED and adaptive driving beam (ADB) systems are rapidly gaining traction, enhancing driver visibility and road safety. Regulatory frameworks, particularly those concerning vehicle lighting standards and emissions, play a crucial role in shaping product development and market entry. Competitive product substitutes, while present in traditional lighting, are increasingly being outpaced by the superior performance and customization offered by adaptive systems. End-user demographics are shifting towards tech-savvy consumers who prioritize safety, comfort, and premium features in their vehicles, driving demand for advanced automotive lighting solutions in Germany. Mergers and acquisitions (M&A) trends indicate a strategic consolidation of capabilities, with larger players acquiring innovative startups to secure technological leadership and expand market reach. For instance, the integration of advanced sensor technologies within lamp assemblies is a key M&A driver. Estimated market share of adaptive lighting systems within the overall automotive lighting market in Germany is projected to reach 25% by 2025, with M&A deal volumes in the automotive component sector, including lighting, experiencing a steady upward trend. Innovation barriers include the high cost of R&D for complex systems and the need for extensive testing and validation to meet safety standards.

- Market Concentration: Moderate to High in specialized segments.

- Key Innovation Drivers: Enhanced safety, comfort, and vehicle aesthetics.

- Regulatory Influence: Strict safety and emission standards mandate advanced lighting technologies.

- Competitive Landscape: Increasing dominance of adaptive systems over traditional lighting.

- End-User Demand: Growing preference for premium, safety-focused automotive features.

- M&A Trends: Strategic acquisitions to gain technological edge and market access.

Germany Automotive Adaptive Lighting System Industry Growth Trends & Insights

The Germany Automotive Adaptive Lighting System Market Size is projected for substantial growth, driven by increasing adoption rates across various vehicle segments. Fueled by a CAGR of 12.5% from 2025 to 2033, the market is expected to reach an estimated €4.2 billion by the end of the forecast period. Technological disruptions, particularly advancements in LED and laser lighting technology, are revolutionizing automotive illumination, enabling sophisticated functionalities like glare-free high beams and dynamic cornering lights. Consumer behavior shifts are also playing a significant role, with an increasing emphasis on safety features, enhanced driving experience, and the perceived value of advanced lighting systems in modern vehicles. The market penetration of adaptive lighting systems in new vehicle production is anticipated to grow from 35% in 2025 to 65% by 2033. This upward trend is underpinned by a growing consumer willingness to invest in these technologies, perceiving them as essential for nighttime driving and overall vehicle safety. Furthermore, the trend towards semi-autonomous and autonomous driving necessitates highly sophisticated lighting systems that can communicate with other vehicles and the environment, acting as a crucial sensor input. The integration of artificial intelligence and machine learning into lighting control algorithms further enhances their adaptive capabilities, predicting traffic scenarios and optimizing light distribution. This evolution transforms lighting from a passive safety feature to an active contributor to intelligent mobility. The German automotive industry's commitment to innovation and its strong focus on premium vehicle segments are key enablers of this rapid market expansion. The introduction of new vehicle models equipped with advanced adaptive lighting as standard or optional features is a consistent driver of market growth and adoption.

Dominant Regions, Countries, or Segments in Germany Automotive Adaptive Lighting System Industry

Within the German automotive landscape, Premium Vehicles stand out as the dominant vehicle type segment driving the adoption of adaptive lighting systems. This dominance is attributed to several factors, including a higher propensity for consumers of premium vehicles to invest in advanced safety and comfort features, and the strategic positioning of these vehicles as showcases for cutting-edge automotive technology. The Front lighting segment, encompassing headlamps, is the primary driver due to its critical role in visibility and safety, representing approximately 70% of the adaptive lighting market. Within component types, the Lamp Assembly segment, integrating LED modules, projectors, and control units, holds the largest market share, followed closely by Sensors/Camera technologies that enable the adaptive functionality. The OEM (Original Equipment Manufacturer) sales channel overwhelmingly dominates the market, accounting for over 90% of sales, as adaptive lighting systems are increasingly integrated from the point of vehicle manufacture.

- Dominant Vehicle Type: Premium Vehicles, showcasing advanced safety and luxury features.

- Dominant Lighting Type: Front lighting (headlamps) due to primary safety and visibility functions.

- Dominant Component Type: Lamp Assembly, integrating sophisticated lighting and control elements.

- Dominant Sales Channel: OEM, reflecting the integration of these systems during vehicle production.

- Key Drivers of Dominance in Premium Segment: High consumer willingness to pay for advanced features, strong brand positioning of technological innovation, and stringent safety expectations.

- Market Share & Growth Potential: Premium vehicle segment is expected to contribute over 60% of the total adaptive lighting market revenue in Germany by 2025, with a projected CAGR of 13% for this segment.

- Economic Policies & Infrastructure: Supportive government initiatives for automotive R&D and infrastructure development for advanced mobility contribute to this dominance.

Germany Automotive Adaptive Lighting System Industry Product Landscape

The product landscape of the Germany Automotive Adaptive Lighting System industry is characterized by rapid innovation and the integration of sophisticated technologies. Key product advancements include the widespread adoption of Matrix LED and Digital Light Processing (DLP) systems, offering highly precise and customizable light distribution. Applications extend from adaptive front-lighting systems (AFS) that automatically adjust beam patterns based on steering and speed, to intelligent tail-light functions that enhance visibility and signaling for other road users. Performance metrics are defined by increased lumen output, superior color rendering, and enhanced energy efficiency. Unique selling propositions revolve around improved night-time visibility, reduced glare for oncoming drivers, and the integration of signaling and safety communication features. Technological advancements are focusing on the miniaturization of components, enhanced computational power for real-time adaptation, and improved durability in harsh automotive environments.

Key Drivers, Barriers & Challenges in Germany Automotive Adaptive Lighting System Industry

The Germany Automotive Adaptive Lighting System Industry is propelled by several key drivers. Foremost is the escalating demand for enhanced road safety and driver comfort, directly addressed by adaptive technologies that optimize visibility. Stringent EU automotive safety regulations, mandating improved lighting performance, also act as a significant catalyst. The technological advancements in LED and laser lighting, coupled with decreasing component costs, are making these systems more accessible. Furthermore, the increasing sophistication of vehicle electronics and sensor integration supports the complex functionalities of adaptive lighting. The German automotive sector's reputation for innovation and quality further fuels the adoption of these premium features.

However, significant barriers and challenges exist. The high cost of development and implementation for sophisticated adaptive lighting systems remains a considerable hurdle, particularly for mass-market vehicles. Regulatory complexities and lengthy approval processes for new lighting technologies can slow down market entry. Supply chain disruptions for critical electronic components and specialized lighting modules can impact production volumes and timelines. Moreover, competition from established lighting manufacturers offering advanced, yet less complex, solutions and the consumer's understanding and perceived value of these advanced systems can influence adoption rates.

Emerging Opportunities in Germany Automotive Adaptive Lighting System Industry

Emerging opportunities in the Germany Automotive Adaptive Lighting System industry lie in the development of smart lighting solutions that integrate with advanced driver-assistance systems (ADAS) and autonomous driving technologies. The growing demand for vehicle customization and personalization presents opportunities for offering bespoke lighting profiles. Furthermore, the aftermarket sector is ripe for growth with the development of retrofittable adaptive lighting solutions for older vehicle models. The integration of lighting systems with vehicle-to-everything (V2X) communication to signal hazards or intentions to other road users is another promising avenue. The increasing focus on sustainability also opens doors for energy-efficient adaptive lighting solutions that optimize power consumption.

Growth Accelerators in the Germany Automotive Adaptive Lighting System Industry Industry

Several catalysts are accelerating long-term growth in the Germany Automotive Adaptive Lighting System industry. Technological breakthroughs in solid-state lighting, such as micro-LEDs and advanced laser projection, promise even more precise and efficient lighting capabilities. Strategic partnerships between automotive OEMs, Tier-1 suppliers, and technology firms are fostering collaborative innovation and faster product development cycles. The increasing integration of these systems as a standard feature in new vehicle launches across various segments is a significant market expansion strategy. Furthermore, the development of more robust and cost-effective sensor technologies, coupled with advancements in AI-powered control algorithms, will further drive adoption and unlock new functionalities, solidifying Germany's position as a leader in automotive lighting innovation.

Key Players Shaping the Germany Automotive Adaptive Lighting System Industry Market

- Magneti Marelli SpA

- Texas Instruments

- Hyundai Mobis

- Koito Manufacturing Co Ltd

- Koninklijke Philips N V

- Osram

- HELLA KGaA Hueck & Co

- Stanley Electric Co Ltd

- Valeo Group

Notable Milestones in Germany Automotive Adaptive Lighting System Industry Sector

- February 2022: Opel and the Technical University of Darmstadt announced a strategic partnership to research new lighting technologies, aiming to develop a self-adapting headlamp and tail-lamp system that adapts to its surroundings, optimizing conditions based on the environment and traffic.

- April 2021: Tesla and Samsung announced their joint venture for a lighting and headlight supply deal, with Samsung's modularized LED headlamps to be offered to Tesla through Hella, a German auto parts manufacturer.

In-Depth Germany Automotive Adaptive Lighting System Industry Market Outlook

The future outlook for the Germany Automotive Adaptive Lighting System industry is exceptionally promising, driven by a confluence of technological advancements and evolving consumer expectations. The continuous innovation in LED and laser lighting technologies will unlock new levels of performance and functionality, enabling lighting systems to become integral components of intelligent mobility. Strategic collaborations between industry leaders and research institutions will further accelerate the development and deployment of next-generation adaptive lighting solutions. The increasing integration of these systems into vehicle platforms as standard features, coupled with the growing aftermarket demand, will significantly expand market penetration. Furthermore, the convergence of automotive lighting with ADAS and autonomous driving technologies presents substantial opportunities for growth, positioning Germany at the forefront of automotive innovation.

Germany Automotive Adaptive Lighting System Industry Segmentation

-

1. Vehicle Type

- 1.1. Mid-Segment Passenger Vehicles

- 1.2. Sports Cars

- 1.3. Premium Vehicles

-

2. Type

- 2.1. Front

- 2.2. Rear

-

3. Component Type

- 3.1. Controller

- 3.2. Sensors/ Camera

- 3.3. Lamp Assembly

- 3.4. Other Cmponent Types

-

4. Sales Channel Type

- 4.1. OEM

- 4.2. Aftermarket

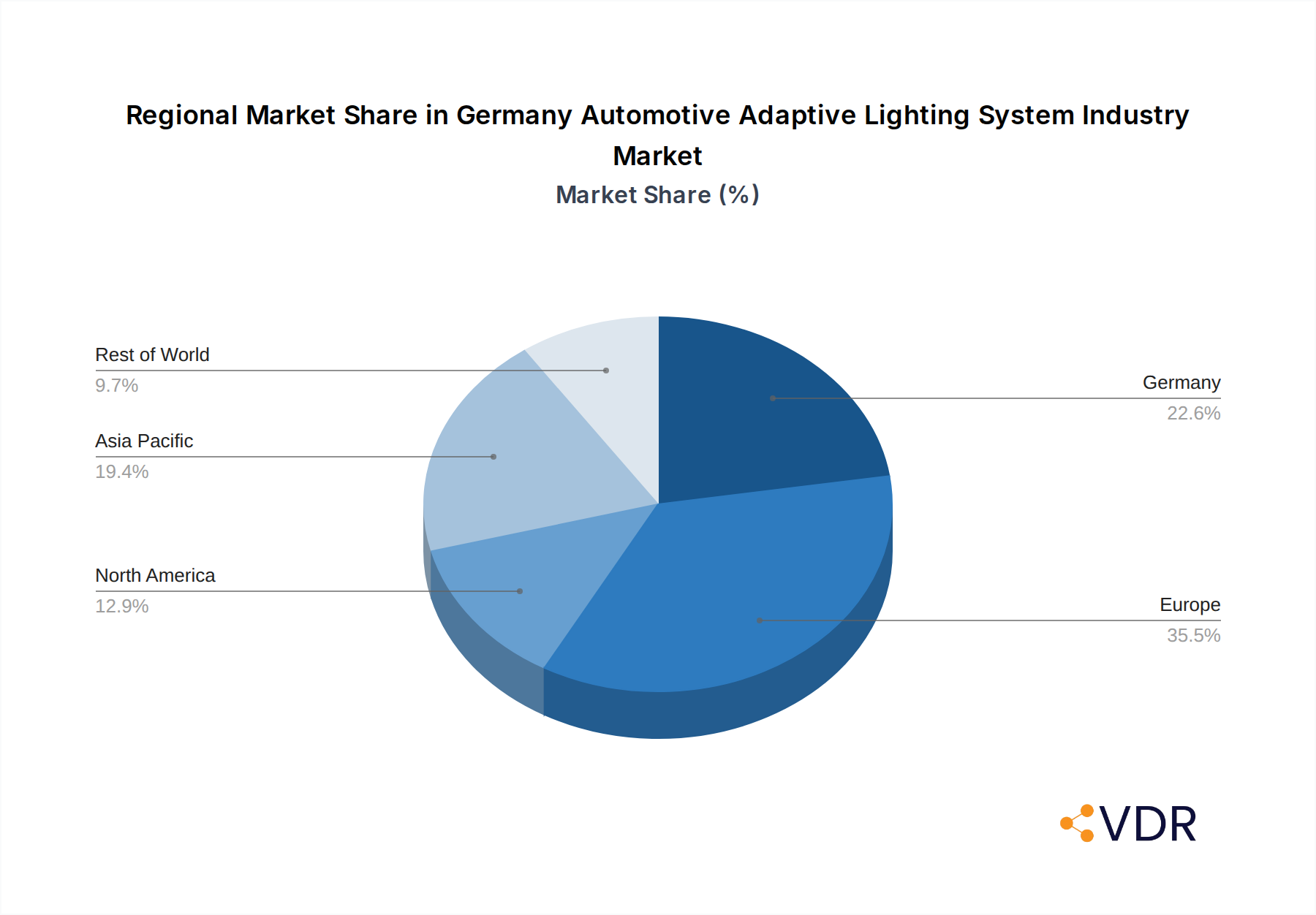

Germany Automotive Adaptive Lighting System Industry Segmentation By Geography

- 1. Germany

Germany Automotive Adaptive Lighting System Industry Regional Market Share

Geographic Coverage of Germany Automotive Adaptive Lighting System Industry

Germany Automotive Adaptive Lighting System Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Mid-Segment Passenger Vehicles

- 5.1.2. Sports Cars

- 5.1.3. Premium Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Front

- 5.2.2. Rear

- 5.3. Market Analysis, Insights and Forecast - by Component Type

- 5.3.1. Controller

- 5.3.2. Sensors/ Camera

- 5.3.3. Lamp Assembly

- 5.3.4. Other Cmponent Types

- 5.4. Market Analysis, Insights and Forecast - by Sales Channel Type

- 5.4.1. OEM

- 5.4.2. Aftermarket

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. Germany

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. Germany Automotive Adaptive Lighting System Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.1.1. Mid-Segment Passenger Vehicles

- 6.1.2. Sports Cars

- 6.1.3. Premium Vehicles

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Front

- 6.2.2. Rear

- 6.3. Market Analysis, Insights and Forecast - by Component Type

- 6.3.1. Controller

- 6.3.2. Sensors/ Camera

- 6.3.3. Lamp Assembly

- 6.3.4. Other Cmponent Types

- 6.4. Market Analysis, Insights and Forecast - by Sales Channel Type

- 6.4.1. OEM

- 6.4.2. Aftermarket

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Magneti Marelli SpA

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Texas Instruments

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Hyundai Mobis

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Koito Manufacturing Co Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Koninklijke Philips N V

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Osram

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 HELLA KGaAHueck& Co

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Stanley Electric Co Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Valeo Group

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Magneti Marelli SpA

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Germany Automotive Adaptive Lighting System Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Germany Automotive Adaptive Lighting System Industry Share (%) by Company 2025

List of Tables

- Table 1: Germany Automotive Adaptive Lighting System Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 2: Germany Automotive Adaptive Lighting System Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Germany Automotive Adaptive Lighting System Industry Revenue billion Forecast, by Component Type 2020 & 2033

- Table 4: Germany Automotive Adaptive Lighting System Industry Revenue billion Forecast, by Sales Channel Type 2020 & 2033

- Table 5: Germany Automotive Adaptive Lighting System Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Germany Automotive Adaptive Lighting System Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 7: Germany Automotive Adaptive Lighting System Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 8: Germany Automotive Adaptive Lighting System Industry Revenue billion Forecast, by Component Type 2020 & 2033

- Table 9: Germany Automotive Adaptive Lighting System Industry Revenue billion Forecast, by Sales Channel Type 2020 & 2033

- Table 10: Germany Automotive Adaptive Lighting System Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Germany Automotive Adaptive Lighting System Industry?

The projected CAGR is approximately 8.7%.

2. Which companies are prominent players in the Germany Automotive Adaptive Lighting System Industry?

Key companies in the market include Magneti Marelli SpA, Texas Instruments, Hyundai Mobis, Koito Manufacturing Co Ltd, Koninklijke Philips N V, Osram, HELLA KGaAHueck& Co, Stanley Electric Co Ltd, Valeo Group.

3. What are the main segments of the Germany Automotive Adaptive Lighting System Industry?

The market segments include Vehicle Type, Type, Component Type, Sales Channel Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.9 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Aluminium Use in Die Casting Equipment is Likely to Drive Demand for the Die-Casting Market.

6. What are the notable trends driving market growth?

Front Lightening will Lead the Market.

7. Are there any restraints impacting market growth?

High Raw Material Prices May One of The Factors That Hindering Target Market Growth..

8. Can you provide examples of recent developments in the market?

February 2022: Opel and the Technical University of Darmstadt jointly announced a strategic partnership to research new lighting technologies. The funded research will also seek to develop a self-adapting headlamp and tail-lamp system that adapts to its surroundings - providing optimal conditions based on the environment and traffic around the vehicle alongside other influencing factors.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Germany Automotive Adaptive Lighting System Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Germany Automotive Adaptive Lighting System Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Germany Automotive Adaptive Lighting System Industry?

To stay informed about further developments, trends, and reports in the Germany Automotive Adaptive Lighting System Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence