Key Insights

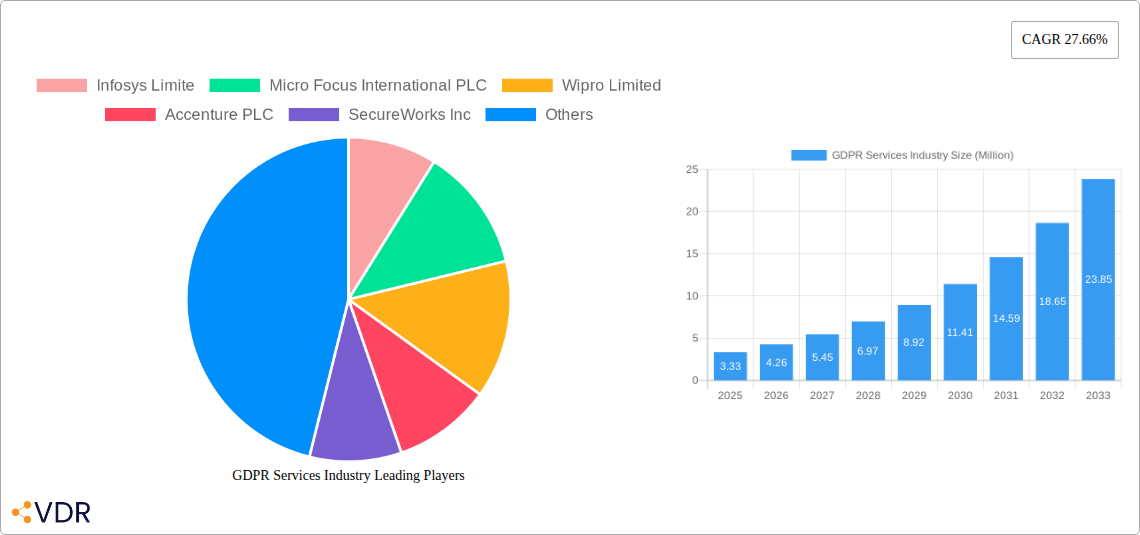

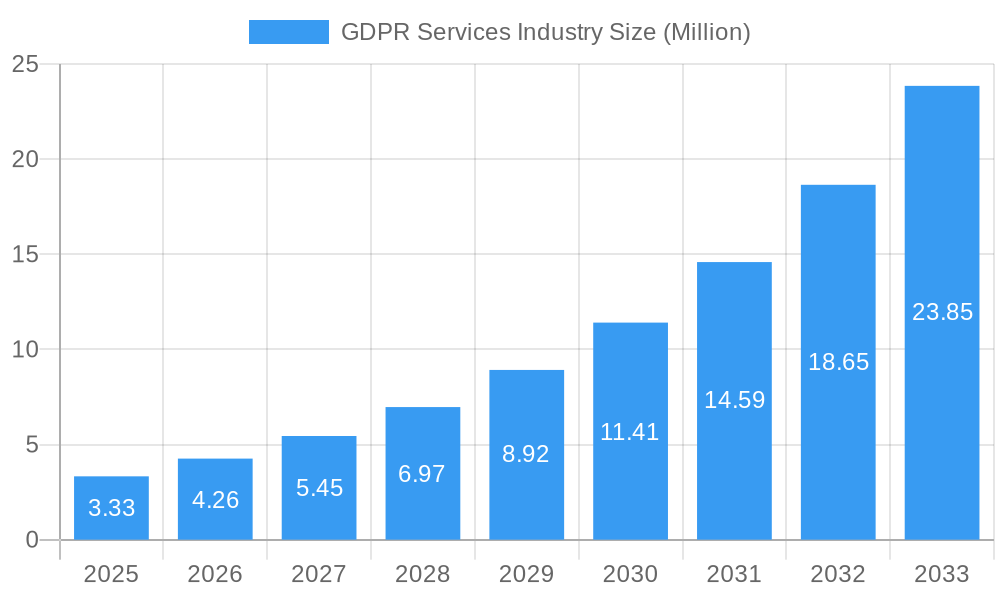

The GDPR Services Industry is experiencing remarkable growth, projected to reach an estimated $3.33 million by 2025 and expand at a compound annual growth rate (CAGR) of 27.66% through 2033. This robust expansion is fueled by escalating concerns surrounding data privacy and security, coupled with the ongoing imperative for organizations across all sectors to achieve and maintain compliance with the General Data Protection Regulation (GDPR). Key drivers include the increasing volume and complexity of data being generated, a heightened awareness of the severe financial and reputational repercussions of data breaches and non-compliance, and the continuous evolution of data privacy landscapes. The industry is witnessing significant demand for comprehensive solutions encompassing data management, data discovery and mapping, robust data governance frameworks, and efficient API management to facilitate secure data flow.

GDPR Services Industry Market Size (In Million)

The market is characterized by a dynamic interplay of deployment models and a broad spectrum of end-user industries. While cloud-based solutions are gaining traction due to their scalability and flexibility, on-premise deployments remain relevant for organizations with specific security or regulatory requirements. Large enterprises, with their extensive data holdings and complex operations, are major adopters, alongside a growing number of small and medium-sized enterprises (SMEs) recognizing the critical need for GDPR compliance. The Banking, Financial Services, and Insurance (BFSI) sector, along with Telecom and IT, Retail, Healthcare, and Manufacturing industries, are leading the charge in seeking specialized GDPR services. Emerging markets in Asia Pacific are showing particularly strong growth potential, driven by rapid digitalization and increasing regulatory scrutiny. Challenges such as the evolving nature of cyber threats and the high cost of implementing comprehensive compliance measures are present, but the overarching benefits of enhanced data protection and customer trust continue to propel market expansion.

GDPR Services Industry Company Market Share

Here's the SEO-optimized report description for the GDPR Services Industry, crafted for maximum impact and without any placeholder text.

This in-depth report provides a detailed analysis of the global GDPR Services Industry, encompassing market dynamics, growth trends, competitive landscape, and future opportunities. Covering the historical period from 2019 to 2024 and a forecast period from 2025 to 2033, with a base and estimated year of 2025, this report offers actionable insights for stakeholders. We explore the intricacies of the parent market and its crucial child markets, utilizing high-traffic keywords to ensure maximum search engine visibility for "GDPR compliance," "data privacy solutions," "data protection services," "API management," "data governance," and "BFSI data security."

GDPR Services Industry Market Dynamics & Structure

The GDPR Services Industry is characterized by a dynamic interplay of regulatory adherence, technological innovation, and evolving end-user needs. Market concentration is observed among leading technology and consulting firms, yet significant opportunities exist for specialized niche players. Technological innovation drivers, such as advancements in AI-driven data discovery and automated compliance tools, are paramount, alongside the constant evolution of regulatory frameworks. Competitive product substitutes are emerging, driven by the increasing demand for comprehensive data protection. End-user demographics span across all enterprise sizes, from Large Enterprises to Small and Medium-sized Enterprises (SMEs), with a particular emphasis on highly regulated sectors. Mergers and Acquisitions (M&A) trends are indicative of market consolidation and strategic expansion. For instance, in 2023, an estimated xx M&A deals, with an aggregate value of $xx million, were recorded. Key innovation barriers include the complexity of global data privacy laws and the high cost of implementing robust data governance solutions. The market's structure is influenced by the increasing demand for cloud-based GDPR services.

- Market Concentration: Dominated by a mix of large IT service providers and specialized data privacy consultancies.

- Technological Innovation Drivers: AI/ML for data mapping, automated compliance reporting, encryption technologies, and privacy-enhancing computation.

- Regulatory Frameworks: The General Data Protection Regulation (GDPR) remains the cornerstone, with evolving interpretations and enforcement impacting service offerings.

- Competitive Product Substitutes: Rise of in-house compliance teams, open-source data privacy tools, and manual data audit processes.

- End-User Demographics: Broad adoption across BFSI, Telecom & IT, Healthcare & Life Sciences, and Retail.

- M&A Trends: Consolidation driven by the need for comprehensive service portfolios and expanded geographic reach.

- Innovation Barriers: High implementation costs, data silo complexity, and the constant need for regulatory updates.

GDPR Services Industry Growth Trends & Insights

The GDPR Services Industry is experiencing robust growth, driven by increasing data volumes, escalating cyber threats, and stringent regulatory enforcement worldwide. The market size is projected to grow from an estimated $xx billion in 2025 to over $xx billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of xx%. Adoption rates for comprehensive data protection solutions are surging, particularly within the Banking, Financial Services, and Insurance (BFSI) sector, where the cost of non-compliance is exceptionally high. Technological disruptions, including the rise of privacy-preserving AI and federated learning, are reshaping how organizations approach data management and compliance. Consumer behavior shifts towards greater data privacy awareness are compelling businesses to invest proactively in GDPR services. The market penetration of specialized GDPR services is estimated to reach xx% by 2028. The expansion of cloud-based data storage and processing further fuels the demand for cloud-native GDPR solutions. The increasing complexity of data architectures and the proliferation of data sources necessitate sophisticated data discovery and mapping capabilities.

The growth of the parent market for GDPR services is significantly influenced by the child markets of Data Management and API Management. As businesses increasingly rely on seamless data integration and application connectivity, the demand for robust API management solutions that adhere to privacy standards is skyrocketing. This surge is directly linked to the need for secure exposure and consumption of data, a core tenet of GDPR. Furthermore, the sheer volume of data generated and processed necessitates advanced Data Management services, including data discovery, classification, and governance, to ensure compliance. The evolving digital landscape, marked by the proliferation of web applications and the adoption of event-driven architectures, underscores the critical role of API management in enabling secure and compliant data exchange. This interconnectedness between data management, API security, and GDPR compliance is a primary growth catalyst.

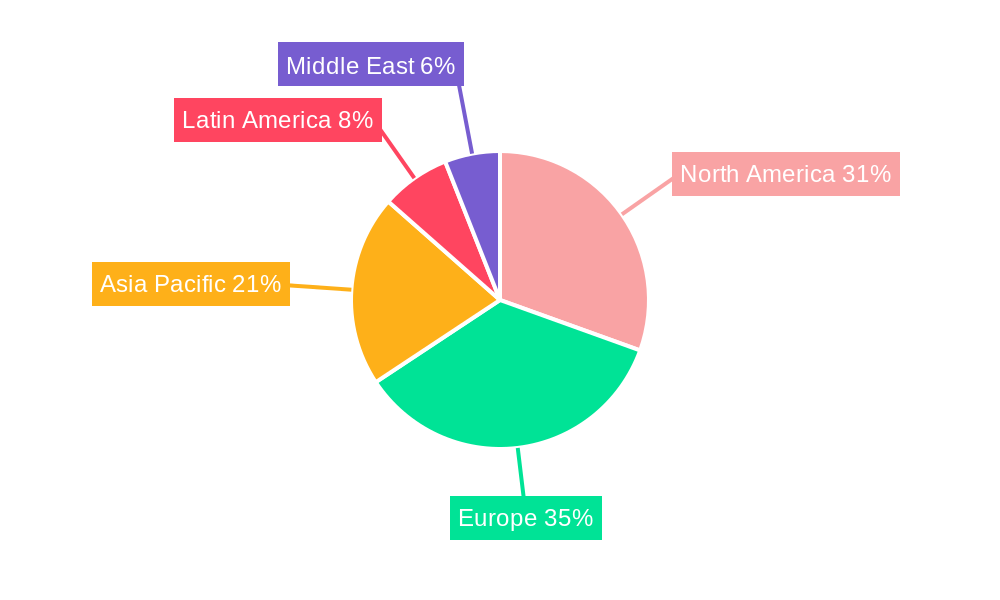

Dominant Regions, Countries, or Segments in GDPR Services Industry

The Cloud deployment model is emerging as the dominant segment within the GDPR Services Industry, driven by its scalability, flexibility, and cost-effectiveness. North America, particularly the United States, leads in market share due to its robust technological infrastructure, high adoption of digital services, and proactive regulatory enforcement. However, Europe remains a critical market due to the GDPR's origin and strict adherence requirements. The Banking, Financial Services, and Insurance (BFSI) sector is the largest end-user industry, accounting for an estimated xx% of the market revenue in 2025. This dominance is attributed to the highly sensitive nature of financial data and the severe penalties for non-compliance. Within the Offering segment, Data Management services, encompassing data discovery and mapping, are experiencing substantial growth, projected at a CAGR of xx%. Large Enterprises constitute the largest customer segment, driven by their extensive data footprints and complex compliance needs.

- Dominant Deployment: Cloud, with an estimated market share of xx% in 2025.

- Leading Region: North America, followed closely by Europe.

- Dominant End User: Banking, Financial Services, and Insurance (BFSI), with an estimated market size of $xx million in 2025.

- Key Offering Driver: Data Management (including Data Discovery and Mapping), projected CAGR of xx%.

- Primary Organization Size: Large Enterprises, representing xx% of market revenue.

- Growth Potential in Europe: Strong due to ongoing regulatory scrutiny and evolving data localization requirements.

- APAC Market Outlook: Rapidly growing due to increasing digital transformation and data privacy awareness.

GDPR Services Industry Product Landscape

The GDPR Services Industry product landscape is defined by an array of innovative solutions designed to streamline compliance and enhance data protection. Key product innovations include AI-powered data discovery tools that automatically map sensitive data across disparate systems, such as those offered by Informatica's IDMC platform, which processes over 44 trillion cloud transactions monthly. Advanced data governance suites provide granular control over data access, usage, and retention. API management platforms, like Gravitee.io, are increasingly integrating robust security and compliance features to manage synchronous RESTful and asynchronous event-driven APIs securely. Performance metrics for these solutions are gauged by their efficiency in reducing manual effort, accuracy in data identification, and effectiveness in mitigating data breach risks. Unique selling propositions often lie in their ability to provide end-to-end compliance, real-time monitoring, and seamless integration with existing IT infrastructures.

Key Drivers, Barriers & Challenges in GDPR Services Industry

Key Drivers:

- Stringent Regulatory Enforcement: The increasing number of fines and penalties for GDPR violations acts as a powerful motivator for organizations to invest in compliance services.

- Growing Data Volumes and Complexity: The exponential growth of data, coupled with the adoption of cloud and hybrid environments, necessitates advanced data management and protection solutions.

- Rising Cyber Threats: The escalating sophistication of cyberattacks drives demand for robust data security and privacy services.

- Customer Demand for Privacy: Consumers are increasingly aware of their data rights, pushing businesses to prioritize data privacy to maintain trust and brand reputation.

- Technological Advancements: Innovations in AI, machine learning, and automation are enabling more efficient and effective GDPR compliance.

Barriers & Challenges:

- High Implementation Costs: The initial investment in GDPR services, including software, hardware, and consulting, can be substantial, particularly for SMEs.

- Talent Shortage: A scarcity of skilled professionals with expertise in data privacy laws and technologies poses a significant challenge.

- Regulatory Interpretation and Evolution: The GDPR framework is subject to ongoing interpretation and updates, requiring continuous adaptation of compliance strategies.

- Integration Complexity: Integrating new GDPR solutions with legacy IT systems can be technically challenging and time-consuming.

- Data Silos and Legacy Systems: Existing data architectures often present difficulties in achieving comprehensive data discovery and mapping.

- Global Compliance Harmonization: Navigating differing data privacy regulations across various jurisdictions adds complexity for multinational corporations.

Emerging Opportunities in GDPR Services Industry

Emerging opportunities in the GDPR Services Industry lie in the growing demand for specialized solutions catering to niche sectors, such as the burgeoning IoT data management and the increasingly regulated healthcare data landscape. The rise of privacy-enhancing technologies (PETs) presents a significant avenue for innovation, enabling organizations to leverage data while minimizing privacy risks. Furthermore, the expansion of GDPR principles into other global data privacy regulations, like the California Consumer Privacy Act (CCPA) and Brazil's LGPD, creates a substantial international market for GDPR expertise and services. Untapped markets in developing economies that are beginning to implement their own data protection laws also represent significant growth potential. The increasing need for automated data subject access request (DSAR) management and the development of AI-driven privacy impact assessments (PIAs) are also key areas of opportunity.

Growth Accelerators in the GDPR Services Industry Industry

Long-term growth in the GDPR Services Industry is being significantly accelerated by breakthroughs in privacy-preserving technologies such as differential privacy and homomorphic encryption. Strategic partnerships between technology providers and cybersecurity firms are creating comprehensive, end-to-end data protection ecosystems. Market expansion strategies by global IT service providers into underserved regions are also a major catalyst. Furthermore, the increasing adoption of data governance frameworks that integrate GDPR compliance as a core component is driving demand. The evolving landscape of cloud computing and multi-cloud environments necessitates specialized GDPR services that can manage data across diverse platforms. The trend towards proactive data privacy, rather than reactive compliance, is also a key accelerator.

Key Players Shaping the GDPR Services Industry Market

- Infosys Limite

- Micro Focus International PLC

- Wipro Limited

- Accenture PLC

- SecureWorks Inc

- IBM Corporation

- Capgemini SE

- Veritas Technologies LLC

- Microsoft Corporation

- Larsen & Toubro Infotech Limited

- Tata Consultancy Services Limited

- Amazon Web Services Inc

- DXC Technology Company

- Atos SE

- Oracle Corporation

- SAP SE

Notable Milestones in GDPR Services Industry Sector

- November 2022: Informatica's Intelligent Data Management Cloud (IDMC) platform became available for state and local governments, processing over 44 trillion cloud transactions monthly to assist public agencies in providing efficient services.

- October 2022: Gravitee.io and Solace formed a strategic alliance to offer a unified API management experience for synchronous RESTful and asynchronous event-driven APIs, addressing the growing need for secure application and asset connection in digital enterprises.

In-Depth GDPR Services Industry Market Outlook

The future of the GDPR Services Industry is exceptionally promising, driven by an ongoing commitment to data privacy and security. The increasing demand for sophisticated Data Management and API Management solutions, particularly within the cloud deployment model, will continue to fuel market expansion. Strategic partnerships and technological advancements in AI and privacy-enhancing technologies will further accelerate growth. Organizations are increasingly viewing GDPR compliance not just as a regulatory burden but as a competitive differentiator, leading to sustained investment in proactive data protection strategies. The global adoption of similar data privacy frameworks will broaden the market reach for GDPR service providers, creating significant opportunities for sustained revenue growth and innovation.

GDPR Services Industry Segmentation

-

1. Type of Deployment

- 1.1. On-premise

- 1.2. Cloud

-

2. Offering

- 2.1. Data Management

- 2.2. Data Discovery and Mapping

- 2.3. Data Governance

- 2.4. API Management

-

3. Organization size

- 3.1. Large Enterprises

- 3.2. Small and Medium-sized Enterprises

-

4. End User

- 4.1. Banking, Financial Services, and Insurance (BFSI)

- 4.2. Telecom and IT

- 4.3. Retail and Consumer Goods

- 4.4. Healthcare and Life Sciences

- 4.5. Manufacturing

- 4.6. Other End-user Industries

GDPR Services Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East

GDPR Services Industry Regional Market Share

Geographic Coverage of GDPR Services Industry

GDPR Services Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 27.66% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type of Deployment

- 5.1.1. On-premise

- 5.1.2. Cloud

- 5.2. Market Analysis, Insights and Forecast - by Offering

- 5.2.1. Data Management

- 5.2.2. Data Discovery and Mapping

- 5.2.3. Data Governance

- 5.2.4. API Management

- 5.3. Market Analysis, Insights and Forecast - by Organization size

- 5.3.1. Large Enterprises

- 5.3.2. Small and Medium-sized Enterprises

- 5.4. Market Analysis, Insights and Forecast - by End User

- 5.4.1. Banking, Financial Services, and Insurance (BFSI)

- 5.4.2. Telecom and IT

- 5.4.3. Retail and Consumer Goods

- 5.4.4. Healthcare and Life Sciences

- 5.4.5. Manufacturing

- 5.4.6. Other End-user Industries

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. Europe

- 5.5.3. Asia Pacific

- 5.5.4. Latin America

- 5.5.5. Middle East

- 5.1. Market Analysis, Insights and Forecast - by Type of Deployment

- 6. Global GDPR Services Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type of Deployment

- 6.1.1. On-premise

- 6.1.2. Cloud

- 6.2. Market Analysis, Insights and Forecast - by Offering

- 6.2.1. Data Management

- 6.2.2. Data Discovery and Mapping

- 6.2.3. Data Governance

- 6.2.4. API Management

- 6.3. Market Analysis, Insights and Forecast - by Organization size

- 6.3.1. Large Enterprises

- 6.3.2. Small and Medium-sized Enterprises

- 6.4. Market Analysis, Insights and Forecast - by End User

- 6.4.1. Banking, Financial Services, and Insurance (BFSI)

- 6.4.2. Telecom and IT

- 6.4.3. Retail and Consumer Goods

- 6.4.4. Healthcare and Life Sciences

- 6.4.5. Manufacturing

- 6.4.6. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Type of Deployment

- 7. North America GDPR Services Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Type of Deployment

- 7.1.1. On-premise

- 7.1.2. Cloud

- 7.2. Market Analysis, Insights and Forecast - by Offering

- 7.2.1. Data Management

- 7.2.2. Data Discovery and Mapping

- 7.2.3. Data Governance

- 7.2.4. API Management

- 7.3. Market Analysis, Insights and Forecast - by Organization size

- 7.3.1. Large Enterprises

- 7.3.2. Small and Medium-sized Enterprises

- 7.4. Market Analysis, Insights and Forecast - by End User

- 7.4.1. Banking, Financial Services, and Insurance (BFSI)

- 7.4.2. Telecom and IT

- 7.4.3. Retail and Consumer Goods

- 7.4.4. Healthcare and Life Sciences

- 7.4.5. Manufacturing

- 7.4.6. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Type of Deployment

- 8. Europe GDPR Services Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Type of Deployment

- 8.1.1. On-premise

- 8.1.2. Cloud

- 8.2. Market Analysis, Insights and Forecast - by Offering

- 8.2.1. Data Management

- 8.2.2. Data Discovery and Mapping

- 8.2.3. Data Governance

- 8.2.4. API Management

- 8.3. Market Analysis, Insights and Forecast - by Organization size

- 8.3.1. Large Enterprises

- 8.3.2. Small and Medium-sized Enterprises

- 8.4. Market Analysis, Insights and Forecast - by End User

- 8.4.1. Banking, Financial Services, and Insurance (BFSI)

- 8.4.2. Telecom and IT

- 8.4.3. Retail and Consumer Goods

- 8.4.4. Healthcare and Life Sciences

- 8.4.5. Manufacturing

- 8.4.6. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Type of Deployment

- 9. Asia Pacific GDPR Services Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Type of Deployment

- 9.1.1. On-premise

- 9.1.2. Cloud

- 9.2. Market Analysis, Insights and Forecast - by Offering

- 9.2.1. Data Management

- 9.2.2. Data Discovery and Mapping

- 9.2.3. Data Governance

- 9.2.4. API Management

- 9.3. Market Analysis, Insights and Forecast - by Organization size

- 9.3.1. Large Enterprises

- 9.3.2. Small and Medium-sized Enterprises

- 9.4. Market Analysis, Insights and Forecast - by End User

- 9.4.1. Banking, Financial Services, and Insurance (BFSI)

- 9.4.2. Telecom and IT

- 9.4.3. Retail and Consumer Goods

- 9.4.4. Healthcare and Life Sciences

- 9.4.5. Manufacturing

- 9.4.6. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Type of Deployment

- 10. Latin America GDPR Services Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Type of Deployment

- 10.1.1. On-premise

- 10.1.2. Cloud

- 10.2. Market Analysis, Insights and Forecast - by Offering

- 10.2.1. Data Management

- 10.2.2. Data Discovery and Mapping

- 10.2.3. Data Governance

- 10.2.4. API Management

- 10.3. Market Analysis, Insights and Forecast - by Organization size

- 10.3.1. Large Enterprises

- 10.3.2. Small and Medium-sized Enterprises

- 10.4. Market Analysis, Insights and Forecast - by End User

- 10.4.1. Banking, Financial Services, and Insurance (BFSI)

- 10.4.2. Telecom and IT

- 10.4.3. Retail and Consumer Goods

- 10.4.4. Healthcare and Life Sciences

- 10.4.5. Manufacturing

- 10.4.6. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Type of Deployment

- 11. Middle East GDPR Services Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Type of Deployment

- 11.1.1. On-premise

- 11.1.2. Cloud

- 11.2. Market Analysis, Insights and Forecast - by Offering

- 11.2.1. Data Management

- 11.2.2. Data Discovery and Mapping

- 11.2.3. Data Governance

- 11.2.4. API Management

- 11.3. Market Analysis, Insights and Forecast - by Organization size

- 11.3.1. Large Enterprises

- 11.3.2. Small and Medium-sized Enterprises

- 11.4. Market Analysis, Insights and Forecast - by End User

- 11.4.1. Banking, Financial Services, and Insurance (BFSI)

- 11.4.2. Telecom and IT

- 11.4.3. Retail and Consumer Goods

- 11.4.4. Healthcare and Life Sciences

- 11.4.5. Manufacturing

- 11.4.6. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Type of Deployment

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Infosys Limite

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Micro Focus International PLC

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Wipro Limited

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Accenture PLC

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 SecureWorks Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 IBM Corporation

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Capgemini SE

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Veritas Technologies LLC

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Microsoft Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Larsen & Toubro Infotech Limited

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Tata Consultancy Services Limited

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Amazon Web Services Inc

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 DXC Technology Company

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Atos SE

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Oracle Corporation

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 SAP SE

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.1 Infosys Limite

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global GDPR Services Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America GDPR Services Industry Revenue (Million), by Type of Deployment 2025 & 2033

- Figure 3: North America GDPR Services Industry Revenue Share (%), by Type of Deployment 2025 & 2033

- Figure 4: North America GDPR Services Industry Revenue (Million), by Offering 2025 & 2033

- Figure 5: North America GDPR Services Industry Revenue Share (%), by Offering 2025 & 2033

- Figure 6: North America GDPR Services Industry Revenue (Million), by Organization size 2025 & 2033

- Figure 7: North America GDPR Services Industry Revenue Share (%), by Organization size 2025 & 2033

- Figure 8: North America GDPR Services Industry Revenue (Million), by End User 2025 & 2033

- Figure 9: North America GDPR Services Industry Revenue Share (%), by End User 2025 & 2033

- Figure 10: North America GDPR Services Industry Revenue (Million), by Country 2025 & 2033

- Figure 11: North America GDPR Services Industry Revenue Share (%), by Country 2025 & 2033

- Figure 12: Europe GDPR Services Industry Revenue (Million), by Type of Deployment 2025 & 2033

- Figure 13: Europe GDPR Services Industry Revenue Share (%), by Type of Deployment 2025 & 2033

- Figure 14: Europe GDPR Services Industry Revenue (Million), by Offering 2025 & 2033

- Figure 15: Europe GDPR Services Industry Revenue Share (%), by Offering 2025 & 2033

- Figure 16: Europe GDPR Services Industry Revenue (Million), by Organization size 2025 & 2033

- Figure 17: Europe GDPR Services Industry Revenue Share (%), by Organization size 2025 & 2033

- Figure 18: Europe GDPR Services Industry Revenue (Million), by End User 2025 & 2033

- Figure 19: Europe GDPR Services Industry Revenue Share (%), by End User 2025 & 2033

- Figure 20: Europe GDPR Services Industry Revenue (Million), by Country 2025 & 2033

- Figure 21: Europe GDPR Services Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Asia Pacific GDPR Services Industry Revenue (Million), by Type of Deployment 2025 & 2033

- Figure 23: Asia Pacific GDPR Services Industry Revenue Share (%), by Type of Deployment 2025 & 2033

- Figure 24: Asia Pacific GDPR Services Industry Revenue (Million), by Offering 2025 & 2033

- Figure 25: Asia Pacific GDPR Services Industry Revenue Share (%), by Offering 2025 & 2033

- Figure 26: Asia Pacific GDPR Services Industry Revenue (Million), by Organization size 2025 & 2033

- Figure 27: Asia Pacific GDPR Services Industry Revenue Share (%), by Organization size 2025 & 2033

- Figure 28: Asia Pacific GDPR Services Industry Revenue (Million), by End User 2025 & 2033

- Figure 29: Asia Pacific GDPR Services Industry Revenue Share (%), by End User 2025 & 2033

- Figure 30: Asia Pacific GDPR Services Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Asia Pacific GDPR Services Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: Latin America GDPR Services Industry Revenue (Million), by Type of Deployment 2025 & 2033

- Figure 33: Latin America GDPR Services Industry Revenue Share (%), by Type of Deployment 2025 & 2033

- Figure 34: Latin America GDPR Services Industry Revenue (Million), by Offering 2025 & 2033

- Figure 35: Latin America GDPR Services Industry Revenue Share (%), by Offering 2025 & 2033

- Figure 36: Latin America GDPR Services Industry Revenue (Million), by Organization size 2025 & 2033

- Figure 37: Latin America GDPR Services Industry Revenue Share (%), by Organization size 2025 & 2033

- Figure 38: Latin America GDPR Services Industry Revenue (Million), by End User 2025 & 2033

- Figure 39: Latin America GDPR Services Industry Revenue Share (%), by End User 2025 & 2033

- Figure 40: Latin America GDPR Services Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Latin America GDPR Services Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Middle East GDPR Services Industry Revenue (Million), by Type of Deployment 2025 & 2033

- Figure 43: Middle East GDPR Services Industry Revenue Share (%), by Type of Deployment 2025 & 2033

- Figure 44: Middle East GDPR Services Industry Revenue (Million), by Offering 2025 & 2033

- Figure 45: Middle East GDPR Services Industry Revenue Share (%), by Offering 2025 & 2033

- Figure 46: Middle East GDPR Services Industry Revenue (Million), by Organization size 2025 & 2033

- Figure 47: Middle East GDPR Services Industry Revenue Share (%), by Organization size 2025 & 2033

- Figure 48: Middle East GDPR Services Industry Revenue (Million), by End User 2025 & 2033

- Figure 49: Middle East GDPR Services Industry Revenue Share (%), by End User 2025 & 2033

- Figure 50: Middle East GDPR Services Industry Revenue (Million), by Country 2025 & 2033

- Figure 51: Middle East GDPR Services Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global GDPR Services Industry Revenue Million Forecast, by Type of Deployment 2020 & 2033

- Table 2: Global GDPR Services Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 3: Global GDPR Services Industry Revenue Million Forecast, by Organization size 2020 & 2033

- Table 4: Global GDPR Services Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 5: Global GDPR Services Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global GDPR Services Industry Revenue Million Forecast, by Type of Deployment 2020 & 2033

- Table 7: Global GDPR Services Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 8: Global GDPR Services Industry Revenue Million Forecast, by Organization size 2020 & 2033

- Table 9: Global GDPR Services Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 10: Global GDPR Services Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 11: Global GDPR Services Industry Revenue Million Forecast, by Type of Deployment 2020 & 2033

- Table 12: Global GDPR Services Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 13: Global GDPR Services Industry Revenue Million Forecast, by Organization size 2020 & 2033

- Table 14: Global GDPR Services Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 15: Global GDPR Services Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global GDPR Services Industry Revenue Million Forecast, by Type of Deployment 2020 & 2033

- Table 17: Global GDPR Services Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 18: Global GDPR Services Industry Revenue Million Forecast, by Organization size 2020 & 2033

- Table 19: Global GDPR Services Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 20: Global GDPR Services Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: Global GDPR Services Industry Revenue Million Forecast, by Type of Deployment 2020 & 2033

- Table 22: Global GDPR Services Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 23: Global GDPR Services Industry Revenue Million Forecast, by Organization size 2020 & 2033

- Table 24: Global GDPR Services Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 25: Global GDPR Services Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 26: Global GDPR Services Industry Revenue Million Forecast, by Type of Deployment 2020 & 2033

- Table 27: Global GDPR Services Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 28: Global GDPR Services Industry Revenue Million Forecast, by Organization size 2020 & 2033

- Table 29: Global GDPR Services Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 30: Global GDPR Services Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the GDPR Services Industry?

The projected CAGR is approximately 27.66%.

2. Which companies are prominent players in the GDPR Services Industry?

Key companies in the market include Infosys Limite, Micro Focus International PLC, Wipro Limited, Accenture PLC, SecureWorks Inc, IBM Corporation, Capgemini SE, Veritas Technologies LLC, Microsoft Corporation, Larsen & Toubro Infotech Limited, Tata Consultancy Services Limited, Amazon Web Services Inc, DXC Technology Company, Atos SE, Oracle Corporation, SAP SE.

3. What are the main segments of the GDPR Services Industry?

The market segments include Type of Deployment, Offering , Organization size, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.33 Million as of 2022.

5. What are some drivers contributing to market growth?

Rapid Digital Transformation in the Financial Service Sector; Robust Roll Out of 5G.

6. What are the notable trends driving market growth?

Need for data security and privacy in the wake of a data breach.

7. Are there any restraints impacting market growth?

Lack of Awareness among Professionals.

8. Can you provide examples of recent developments in the market?

November 2022: Informatica, an enterprise cloud data management player, said the Intelligent Data Management Cloud (IDMC) platform is now available for state and local governments during the Informatica World Tour in Washington, DC. Informatica's IDMC platform, which currently processes over 44 trillion cloud transactions monthly, is intended to assist state and local government agencies in providing timely and efficient public services.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "GDPR Services Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the GDPR Services Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the GDPR Services Industry?

To stay informed about further developments, trends, and reports in the GDPR Services Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence