Key Insights

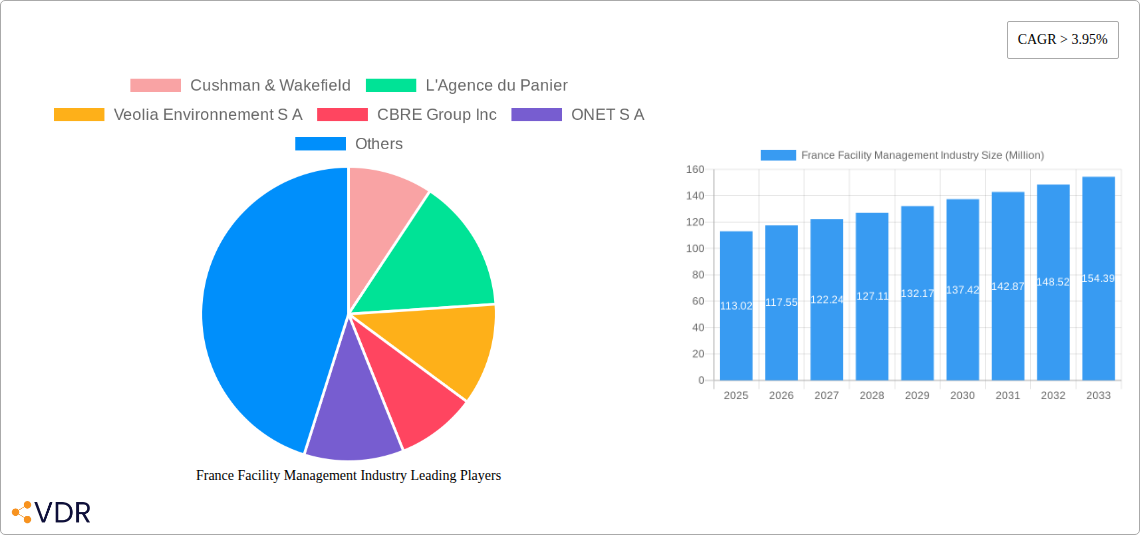

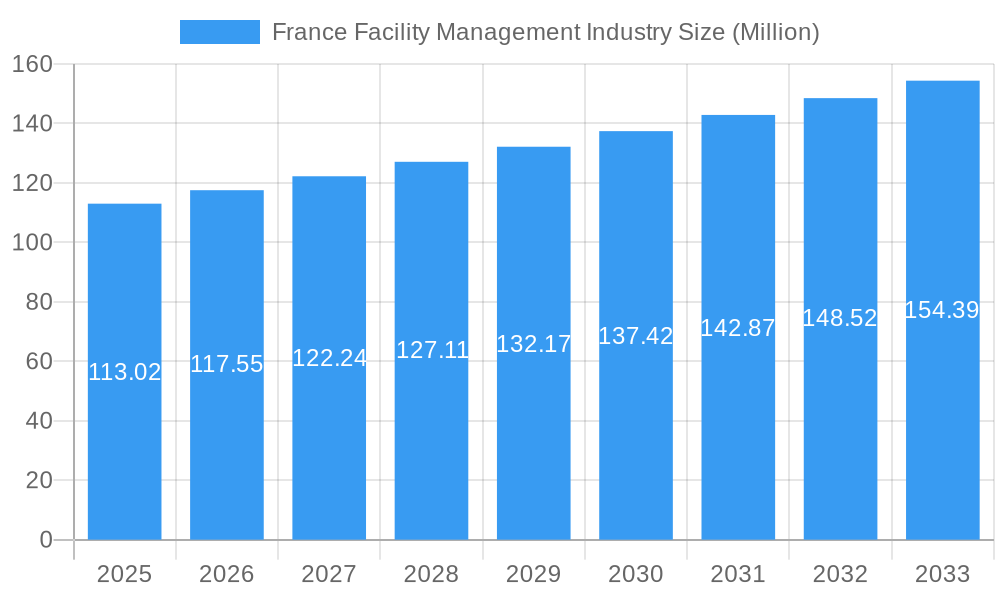

The France Facility Management industry is poised for robust growth, projected to reach a market size of $113.02 million by 2025, with a compelling Compound Annual Growth Rate (CAGR) exceeding 3.95% over the forecast period of 2025-2033. This expansion is fueled by several key drivers, including the increasing demand for specialized facility management services across commercial and industrial sectors, a growing emphasis on operational efficiency and cost optimization by businesses, and the rising adoption of integrated and bundled FM solutions that offer comprehensive service delivery. The market is also benefiting from stricter regulatory compliances and sustainability mandates, pushing organizations to invest in professional facility management to ensure safety, energy efficiency, and environmental responsibility. Furthermore, the evolving nature of workplaces, with a greater focus on employee well-being and smart building technologies, is creating new avenues for service innovation and market penetration.

France Facility Management Industry Market Size (In Million)

The market segmentation reveals a dynamic landscape. In the 'Type' segment, Outsourced Facility Management is anticipated to dominate, encompassing single, bundled, and integrated FM services, reflecting a strong trend towards externalizing non-core functions. Within 'Offering Type', Hard FM services, such as building maintenance and security, are expected to hold a significant share, alongside the rapidly growing Soft FM services, including cleaning, catering, and reception, which directly impact user experience and operational comfort. The 'End-User' segment is led by Commercial and Institutional sectors, driven by the need to manage complex facilities and provide optimal working environments. Leading companies like Cushman & Wakefield, CBRE Group Inc., Veolia Environnement S.A., and Sodexo Group are actively shaping this market through strategic investments, mergers, and acquisitions, focusing on delivering advanced technological solutions and sustainable practices. The French market, in particular, is characterized by a mature demand for high-quality FM services and a growing appetite for innovation in energy management and digital transformation.

France Facility Management Industry Company Market Share

Unlocking the Future of Facility Management in France: A Comprehensive Market Analysis (2019-2033)

This in-depth report provides a definitive analysis of the France Facility Management Industry, offering unparalleled insights into its market dynamics, growth trajectories, and future potential. Designed for industry professionals, investors, and strategic planners, this study navigates the complex landscape of outsourced facility management, integrated FM services, hard FM, and soft FM, while examining the burgeoning demand across commercial, institutional, and public/infrastructure sectors. With a focus on the parent market and its critical child markets, this report is your essential guide to understanding and capitalizing on opportunities within one of Europe's most dynamic facility management ecosystems.

The report leverages data from 2019-2024 (Historical Period), with a Base Year of 2025 and a comprehensive Forecast Period of 2025-2033. All market values are presented in Million Units.

France Facility Management Industry Market Dynamics & Structure

The French facility management market exhibits a moderately consolidated structure, characterized by the presence of a few dominant players alongside a fragmented landscape of specialized service providers. Technological innovation is a key driver, with a significant push towards smart facilities management (FM) solutions aimed at enhancing operational reliability and driving efficiency. Companies are increasingly adopting AI-based platforms and leveraging building operations data for intelligent maintenance. Regulatory frameworks, particularly concerning environmental sustainability and labor laws, play a crucial role in shaping market practices and service offerings. Competitive product substitutes are less prevalent due to the bespoke nature of many FM services, though efficiency gains through technology can be seen as a form of substitution for manual labor. End-user demographics are diverse, with growing demand from the commercial, institutional, and public/infrastructure sectors. Merger and acquisition (M&A) trends are evident as larger players seek to expand their service portfolios and geographical reach, consolidating market share.

- Market Concentration: Dominated by major global players like Cushman & Wakefield, CBRE Group Inc., Sodexo Group, ISS World Services A/S, and VINCI Facilities, alongside significant national players such as ONET S.A. and Atalian Group.

- Technological Innovation: Focus on IoT integration, AI-powered predictive maintenance, building management systems (BMS), and data analytics for optimized resource allocation and cost savings.

- Regulatory Frameworks: Stringent environmental regulations (e.g., energy efficiency standards), health and safety compliance, and labor laws significantly influence operational strategies and service delivery.

- Competitive Landscape: While direct substitutes are limited, innovations in automation and digital platforms are indirectly impacting the need for traditional labor-intensive services.

- End-User Demand: Strong growth in demand from commercial real estate, healthcare, education, and public infrastructure projects.

- M&A Trends: Strategic acquisitions to enhance capabilities in specialized areas like energy management, digital FM, and integrated service offerings.

France Facility Management Industry Growth Trends & Insights

The France Facility Management Industry is poised for robust growth, driven by increasing outsourcing trends, the growing complexity of modern facilities, and a strong emphasis on operational efficiency and sustainability. Market size evolution is marked by a consistent upward trajectory, fueled by the recognition of facility management as a strategic function rather than a mere cost center. The adoption rates for integrated FM solutions are accelerating as organizations seek to streamline operations and benefit from a single point of accountability. Technological disruptions, such as the widespread implementation of IoT sensors for real-time monitoring and the use of AI for predictive maintenance, are revolutionizing service delivery. Consumer behavior shifts are also playing a pivotal role, with a growing demand for flexible, adaptable, and technologically advanced FM services that contribute to employee well-being and productivity. The anticipated Compound Annual Growth Rate (CAGR) for the forecast period is significant, reflecting the sustained demand for professional FM services across all sectors. The market penetration of outsourced services, particularly bundled and integrated models, continues to expand, indicating a strategic shift by businesses and institutions.

Dominant Regions, Countries, or Segments in France Facility Management Industry

The Outsourced Facility Management segment, particularly Integrated FM, stands out as a dominant force driving growth within the French Facility Management Industry. This dominance is underpinned by several key factors. Firstly, the economic policies in France actively encourage businesses to focus on core competencies, leading to increased reliance on external providers for non-core facility operations. Secondly, the infrastructure development within major urban centers and the ongoing modernization of public and commercial buildings necessitate sophisticated and integrated management solutions. Hard FM services, encompassing technical building maintenance, energy management, and security, are experiencing heightened demand due to an aging building stock and stringent energy efficiency mandates. Coupled with Soft FM services like cleaning, catering, and reception, Integrated FM offers a comprehensive, cost-effective, and streamlined approach to facility management, appealing to a wide range of end-users.

Dominant Segment: Outsourced Facility Management, specifically Integrated FM.

- Key Drivers:

- Economic Policies: Government incentives for efficiency and focus on core business.

- Infrastructure Development: Modernization of commercial, public, and transportation infrastructure.

- Cost Optimization: Desire for predictable expenditure and economies of scale.

- Specialized Expertise: Access to advanced technical skills and best practices.

- Market Share: Outsourced FM accounts for over 60% of the total FM market, with Integrated FM showing the fastest growth within this category.

- Growth Potential: Continued expansion driven by large-scale urban renewal projects and the increasing complexity of building technologies.

- Key Drivers:

Leading Offering Type: Hard FM.

- Key Drivers:

- Energy Efficiency Mandates: Growing demand for sustainable building operations.

- Building Modernization: Need for upkeep of complex technical systems.

- Regulatory Compliance: Ensuring safety and operational standards.

- Market Share: Hard FM services represent approximately 55% of the total FM service market.

- Key Drivers:

End-User Dominance: Commercial and Public/Infrastructure sectors.

- Commercial: Driven by large office buildings, retail spaces, and the hospitality sector seeking to enhance employee experience and operational efficiency.

- Public/Infrastructure: Supported by government investments in transportation, healthcare facilities, and educational institutions.

France Facility Management Industry Product Landscape

The French facility management product landscape is rapidly evolving, with a strong emphasis on digital transformation and sustainability. Innovative solutions are being deployed to enhance building performance and occupant well-being. This includes the widespread adoption of IoT-enabled sensors for real-time monitoring of energy consumption, air quality, and space utilization. AI-powered platforms are central to predictive maintenance, minimizing downtime and optimizing repair schedules. Furthermore, the integration of Building Information Modeling (BIM) with FM systems is creating a seamless flow of data for lifecycle management. Unique selling propositions revolve around the ability to deliver data-driven insights, reduce operational costs, and improve the sustainability credentials of facilities. Technological advancements are also leading to more user-friendly interfaces for service requests and performance tracking, enhancing the overall client experience.

Key Drivers, Barriers & Challenges in France Facility Management Industry

Key Drivers:

- Technological Advancements: The adoption of smart FM solutions, IoT, AI, and data analytics is a significant growth accelerator, enabling greater efficiency and predictive capabilities.

- Outsourcing Trends: Businesses and institutions are increasingly outsourcing FM to focus on core competencies, leading to sustained demand for specialized services.

- Sustainability Focus: Growing environmental awareness and regulatory pressures are driving demand for eco-friendly and energy-efficient FM practices.

- Infrastructure Investment: Government and private sector investments in new infrastructure and the modernization of existing facilities create substantial opportunities.

Barriers & Challenges:

- Skilled Labor Shortage: A persistent challenge is the availability of qualified and trained personnel for specialized technical and managerial FM roles.

- Integration Complexity: Implementing and integrating diverse technology platforms and legacy systems can be complex and costly.

- Economic Volatility: Fluctuations in the broader economy can impact discretionary spending on FM services, particularly for smaller businesses.

- Regulatory Compliance: Navigating and adhering to evolving national and EU regulations regarding safety, environment, and labor can be demanding.

- Price Sensitivity: While quality is valued, intense competition can sometimes lead to price pressures, impacting profit margins.

Emerging Opportunities in France Facility Management Industry

Emerging opportunities in the France Facility Management Industry are largely centered around the integration of advanced technologies and the growing demand for specialized services. The "Smart Facilities Management" trend, as exemplified by CBRE's AI-based platform, presents a significant avenue for growth, focusing on data-driven decision-making to improve operational reliability and efficiency. There is a burgeoning market for energy management and retrofitting services, driven by stringent EU environmental targets and French climate initiatives. The demand for hyper-personalized FM solutions catering to specific occupant needs, such as flexible workspace management and enhanced employee well-being services, is also on the rise. Furthermore, opportunities exist in supporting the digital transformation of smaller and medium-sized enterprises (SMEs) by offering scalable and affordable FM technology solutions.

Growth Accelerators in the France Facility Management Industry Industry

Several catalysts are accelerating long-term growth in the France Facility Management Industry. The continuous push for digitalization, driven by companies like Cushman & Wakefield and CBRE Group Inc., is creating a demand for integrated platforms that offer seamless service delivery and data analytics. Strategic partnerships between technology providers and FM companies are becoming crucial for developing cutting-edge solutions. Furthermore, market expansion strategies, including the acquisition of niche service providers and the diversification into new service areas, are propelling growth for key players like VINCI Facilities and Atalian Group. The increasing focus on sustainability and the circular economy within facility operations also presents a significant growth avenue, encouraging the development and adoption of green FM practices.

Key Players Shaping the France Facility Management Industry Market

- Cushman & Wakefield

- L'Agence du Panier

- Veolia Environnement S A

- CBRE Group Inc

- ONET S A

- VINCI Facilities

- Elis S A

- Sodexo Group

- AItenders

- DEF networ

- Atalian Group

- ISS World Services A/S

Notable Milestones in France Facility Management Industry Sector

- August 2023: Smart Facilities Management (FM) Solutions are being utilized to improve operational reliability and drive efficiency at more than 20,000 Global Workplace Solutions client sites, totaling 1 billion sq. ft. CBRE’s Smart FM Solutions enables a more intelligent approach to facility maintenance by leveraging CBRE’s Nexus AI-based platform and its rich trove of building operations and utilization data.

- May 2022: VINCI, a global facility management service provider, would build 3 overhead stations for the planned Grand Paris Express line 18 in France and received a contract worth USD 80.9 million, which consists of the finishing work for the 3 stations, where the company would use its expertise in the Hard FM services including electrical engineering.

- March 2022: Sodexo received the contract to supply culinary services to the Olympic Village during the Paris 2024 Olympic and Paralympic Games because of its expertise in worldwide athletic and cultural events. The company would provide up to 40,000 meals daily for the 14,850 athletes from the 388 Olympic and Paralympic delegations competing at the event. Additionally, the company would offer catering services in 12 tournament locations for the general public.

In-Depth France Facility Management Industry Market Outlook

The future outlook for the France Facility Management Industry is exceptionally bright, driven by sustained demand for integrated and technologically advanced solutions. Growth accelerators such as the ongoing digital transformation and a strong commitment to sustainability will continue to shape the market. Strategic partnerships and market expansion initiatives by key players will further enhance service offerings and reach. The industry is set to witness increased adoption of AI and IoT for enhanced operational efficiency and predictive maintenance. Opportunities abound in the public and commercial sectors, fueled by infrastructure development and the drive for smarter, greener buildings. This evolving landscape presents a fertile ground for innovation and strategic investment, ensuring a robust and dynamic future for facility management in France.

France Facility Management Industry Segmentation

-

1. Type

- 1.1. Inhouse Facility Management

-

1.2. Outsourced Facility Management

- 1.2.1. Single FM

- 1.2.2. Bundled FM

- 1.2.3. Integrated FM

-

2. Offering Type

- 2.1. Hard FM

- 2.2. Soft FM

-

3. End-User

- 3.1. Commercial

- 3.2. Institutional

- 3.3. Public/Infrastructure

- 3.4. Industrial

- 3.5. Others

France Facility Management Industry Segmentation By Geography

- 1. France

France Facility Management Industry Regional Market Share

Geographic Coverage of France Facility Management Industry

France Facility Management Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of > 3.95% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Inhouse Facility Management

- 5.1.2. Outsourced Facility Management

- 5.1.2.1. Single FM

- 5.1.2.2. Bundled FM

- 5.1.2.3. Integrated FM

- 5.2. Market Analysis, Insights and Forecast - by Offering Type

- 5.2.1. Hard FM

- 5.2.2. Soft FM

- 5.3. Market Analysis, Insights and Forecast - by End-User

- 5.3.1. Commercial

- 5.3.2. Institutional

- 5.3.3. Public/Infrastructure

- 5.3.4. Industrial

- 5.3.5. Others

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. France

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. France Facility Management Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Inhouse Facility Management

- 6.1.2. Outsourced Facility Management

- 6.1.2.1. Single FM

- 6.1.2.2. Bundled FM

- 6.1.2.3. Integrated FM

- 6.2. Market Analysis, Insights and Forecast - by Offering Type

- 6.2.1. Hard FM

- 6.2.2. Soft FM

- 6.3. Market Analysis, Insights and Forecast - by End-User

- 6.3.1. Commercial

- 6.3.2. Institutional

- 6.3.3. Public/Infrastructure

- 6.3.4. Industrial

- 6.3.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Cushman & Wakefield

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 L'Agence du Panier

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Veolia Environnement S A

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 CBRE Group Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 ONET S A

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 VINCI Facilities

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Elis S A

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Sodexo Group

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 AItenders

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 DEF networ

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Atalian Group

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 ISS World Services A/S

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 Cushman & Wakefield

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: France Facility Management Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: France Facility Management Industry Share (%) by Company 2025

List of Tables

- Table 1: France Facility Management Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: France Facility Management Industry Revenue Million Forecast, by Offering Type 2020 & 2033

- Table 3: France Facility Management Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 4: France Facility Management Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: France Facility Management Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 6: France Facility Management Industry Revenue Million Forecast, by Offering Type 2020 & 2033

- Table 7: France Facility Management Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 8: France Facility Management Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the France Facility Management Industry?

The projected CAGR is approximately > 3.95%.

2. Which companies are prominent players in the France Facility Management Industry?

Key companies in the market include Cushman & Wakefield, L'Agence du Panier, Veolia Environnement S A, CBRE Group Inc, ONET S A, VINCI Facilities, Elis S A, Sodexo Group, AItenders, DEF networ, Atalian Group, ISS World Services A/S.

3. What are the main segments of the France Facility Management Industry?

The market segments include Type, Offering Type, End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD 113.02 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand for Efficiency in Supply Chain; Increasing Focus on Industry 4.0. Leading to More Manufacturing Facilities.

6. What are the notable trends driving market growth?

Commercial Buildings to Remain the Largest Market Shareholder.

7. Are there any restraints impacting market growth?

Lack of Managerial Awareness.

8. Can you provide examples of recent developments in the market?

August 2023: Smart Facilities Management (FM) Solutions are being utilized to improve operational reliability and drive efficiency at more than 20,000 Global Workplace Solutions client sites, totaling 1 billion sq. ft, Where CBRE’s Smart FM Solutions enables a more intelligent approach to facility maintenance by leveraging CBRE’s Nexus AI-based platform and its rich trove of building operations and utilization data

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "France Facility Management Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the France Facility Management Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the France Facility Management Industry?

To stay informed about further developments, trends, and reports in the France Facility Management Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence