Key Insights

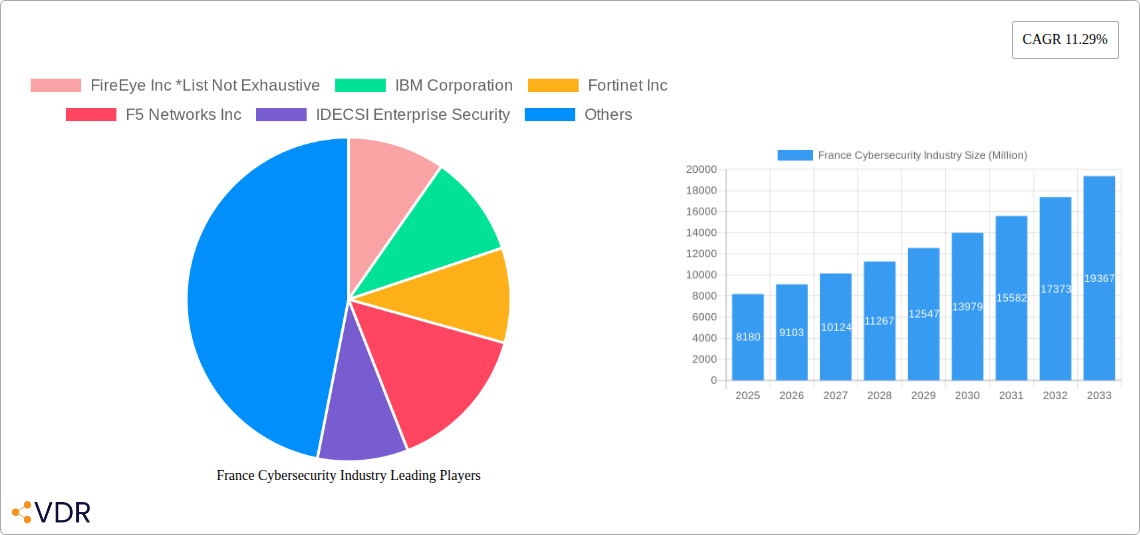

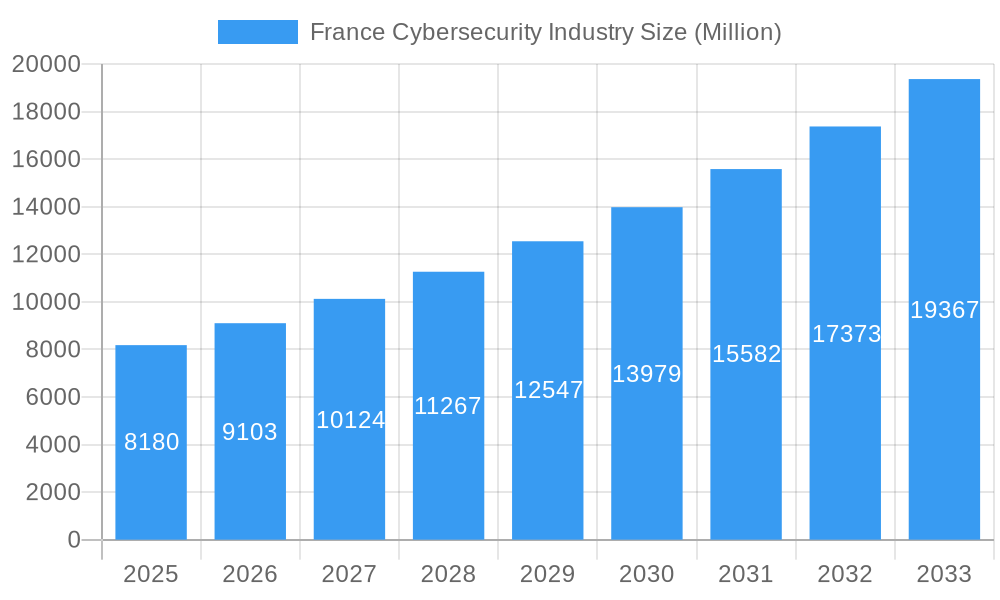

The French cybersecurity market is experiencing robust expansion, projected to reach €8180 million by 2025, driven by a compelling CAGR of 11.29%. This significant growth is fueled by an increasing volume and sophistication of cyber threats targeting businesses and government entities across France. Key growth drivers include the escalating adoption of cloud technologies, the growing complexity of IT infrastructures, and stringent regulatory compliance demands, particularly within sectors like BFSI, healthcare, and government & defense. The rising concern over data breaches and intellectual property theft further propels investment in advanced security solutions. The market is witnessing a strong demand for cloud security, identity and access management (IAM), and network security solutions as organizations strive to protect their digital assets and maintain operational continuity in an ever-evolving threat landscape. Emerging trends include the integration of AI and machine learning in threat detection and response, the growing emphasis on zero-trust architectures, and the increasing adoption of managed security services (MSSPs) for specialized expertise and proactive defense.

France Cybersecurity Industry Market Size (In Billion)

Despite this promising outlook, the French cybersecurity market faces certain restraints. A significant challenge is the persistent shortage of skilled cybersecurity professionals, which can hinder the effective implementation and management of advanced security solutions. Furthermore, the cost of implementing comprehensive security measures can be a barrier for small and medium-sized enterprises (SMEs). However, the market is adapting, with a growing emphasis on user-friendly and scalable solutions. The competitive landscape is dynamic, featuring established players like IBM Corporation, Fortinet Inc, and Cisco Systems Inc, alongside specialized firms. The increasing sophistication of cyber-attacks, coupled with the proactive stance of the French government in bolstering national cyber defenses, will continue to shape the market's trajectory, ensuring sustained growth and innovation in cybersecurity solutions and services throughout the forecast period.

France Cybersecurity Industry Company Market Share

France Cybersecurity Industry Market Overview: Safeguarding Digital Assets in a Hyper-Connected Era

This comprehensive report delivers an in-depth analysis of the France Cybersecurity Industry, a critical sector driven by escalating cyber threats and the imperative for robust digital protection. Explore market dynamics, growth trends, dominant segments, product landscapes, and the pivotal role of key players. With detailed insights into Cloud Security, Data Security, Identity Access Management, Network Security, and Infrastructure Protection, this report is essential for stakeholders navigating the evolving threat landscape. Our analysis spans from the Historical Period (2019-2024) through the Forecast Period (2025-2033), with 2025 serving as the Base Year and Estimated Year. This report is designed for immediate use, requiring no further modification.

France Cybersecurity Industry Market Dynamics & Structure

The French cybersecurity market is characterized by a dynamic interplay of technological advancements, evolving regulatory frameworks, and a burgeoning threat landscape. Market concentration is moderately fragmented, with a mix of large multinational corporations and specialized domestic players vying for market share. Technological innovation serves as a primary driver, fueled by advancements in artificial intelligence (AI), machine learning (ML), and extended detection and response (XDR) solutions. Regulatory frameworks, such as GDPR and NIS2 Directive, continue to shape compliance requirements and drive investment in secure solutions. Competitive product substitutes are emerging, particularly in areas like managed detection and response (MDR) and zero trust architecture. End-user demographics are increasingly diverse, with significant adoption across the BFSI, Healthcare, Manufacturing, Government & Defense, and IT and Telecommunication sectors. Mergers and acquisitions (M&A) trends indicate a consolidation phase, with larger entities acquiring innovative startups to enhance their portfolios and market reach.

- Market Concentration: Moderately fragmented, with key players holding significant market share in specific segments.

- Technological Innovation Drivers: AI/ML for threat detection, XDR, cloud-native security, and advancements in encryption.

- Regulatory Frameworks: GDPR, NIS2 Directive, and national cybersecurity strategies are shaping market demands.

- Competitive Product Substitutes: Growth in MDR, SASE, and security awareness training platforms.

- End-User Demographics: Strong adoption in BFSI, Healthcare, Government & Defense, and IT/Telecommunication.

- M&A Trends: Strategic acquisitions focused on expanding capabilities in cloud security, threat intelligence, and identity management.

France Cybersecurity Industry Growth Trends & Insights

The France Cybersecurity Industry is poised for substantial growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 12.5% from 2025 to 2033. This robust expansion is underpinned by a confluence of factors, including the escalating sophistication of cyberattacks, the increasing value of digital assets, and the growing awareness among businesses and individuals regarding the critical need for robust security measures. In the Base Year 2025, the market size is estimated at €18,500 Million, with projections indicating a significant increase by the end of the Forecast Period 2033.

Adoption rates for advanced cybersecurity solutions are accelerating across all end-user segments. The shift towards digital transformation initiatives, including cloud migration and the proliferation of IoT devices, presents both opportunities and heightened vulnerabilities, thereby driving demand for integrated security platforms. Technological disruptions, such as the widespread adoption of AI in cyber defense and the emergence of quantum-resistant encryption, are reshaping the competitive landscape and demanding continuous innovation from vendors. Consumer behavior is also evolving; individuals are becoming more cognizant of data privacy and are actively seeking secure online experiences, influencing the demand for consumer-focused security products and services.

The increasing reliance on cloud-based services, for instance, necessitates advanced Cloud Security solutions, including identity and access management for cloud environments, data loss prevention for cloud storage, and robust network security for hybrid cloud architectures. Similarly, the exponential growth of data generated by businesses across all sectors fuels the demand for comprehensive Data Security measures, encompassing encryption, tokenization, and data governance. The BFSI sector, a prime target for cybercriminals, is a significant contributor to market growth, investing heavily in Identity Access Management (IAM) to secure sensitive financial data and customer accounts. The Healthcare sector is rapidly adopting digital health records and telemedicine, making Data Security and Infrastructure Protection paramount. The Manufacturing sector's increasing adoption of Industry 4.0 technologies and IoT devices makes Network Security and Infrastructure Protection crucial to prevent operational disruptions and intellectual property theft. The Government & Defense sector, facing nation-state sponsored attacks, requires sophisticated Infrastructure Protection and Network Security solutions.

The IT and Telecommunication sector, being the backbone of digital infrastructure, is a major consumer of cybersecurity solutions, particularly in Network Security and Cloud Security. As remote work becomes a norm, endpoint security and Identity Access Management solutions are witnessing a surge in demand. Furthermore, the report highlights the growing importance of Consumer Security solutions, as individuals become more vulnerable to phishing attacks, malware, and identity theft.

In essence, the growth trajectory of the France cybersecurity market is a testament to the persistent and evolving nature of cyber threats, compelling organizations and individuals alike to prioritize digital resilience. The integration of advanced technologies, coupled with a heightened security consciousness, will continue to fuel market expansion and innovation throughout the forecast period.

Dominant Regions, Countries, or Segments in France Cybersecurity Industry

The France Cybersecurity Industry is experiencing dynamic growth, with specific segments and end-user sectors emerging as dominant forces. Within the Offering segment, Cloud Security is projected to exhibit the highest growth rate, driven by the pervasive adoption of cloud computing across French enterprises. The estimated market share for Cloud Security in 2025 is approximately 25%, with a projected CAGR of 13.2% during the forecast period. This dominance stems from the inherent security challenges associated with cloud environments, including data breaches, misconfigurations, and unauthorized access, necessitating robust solutions like cloud access security brokers (CASB), cloud workload protection platforms (CWPP), and cloud security posture management (CSPM).

Following closely is Network Security, which currently holds a significant market share of around 22% in 2025. The increasing complexity of network infrastructures, the rise of sophisticated network-borne attacks, and the growing adoption of remote work models are fueling the demand for next-generation firewalls, intrusion detection/prevention systems (IDPS), and virtual private networks (VPNs). The IT and Telecommunication sector, as a primary consumer of network security solutions, plays a pivotal role in this segment's growth, with an estimated spending of €4,800 Million on network security in 2025.

Data Security is another critical segment, accounting for an estimated 18% of the market in 2025. The stringent regulatory landscape, particularly GDPR, mandates robust data protection measures, including encryption, data masking, and data loss prevention (DLP). The BFSI sector, entrusted with sensitive financial and personal data, is a major driver for this segment, with projected investments of €3,600 Million in data security solutions in 2025.

Identity Access Management (IAM) is crucial for securing access to digital resources and preventing unauthorized entry. This segment represents approximately 15% of the market in 2025, with a strong growth potential driven by the adoption of multi-factor authentication (MFA) and privileged access management (PAM) solutions across all industries. The Government & Defense sector, in particular, places a high emphasis on IAM for national security reasons.

Infrastructure Protection encompasses a broad range of solutions safeguarding critical IT infrastructure, including endpoint security, server security, and operational technology (OT) security. This segment holds an estimated 12% market share in 2025. The increasing threat to critical national infrastructure (CNI) is a significant driver.

Consumer Security solutions, while representing a smaller portion of the market (approximately 6% in 2025), are gaining traction as individuals become more aware of online threats. This includes antivirus software, VPNs for personal use, and identity protection services.

In terms of Deployment, Cloud deployment models are rapidly gaining prominence, with an estimated 55% of the market share in 2025. This is largely due to the scalability, flexibility, and cost-effectiveness offered by cloud-based security solutions. On-premise deployment still holds a significant share (45%), particularly for organizations with stringent data sovereignty requirements or legacy systems.

The BFSI sector continues to be a dominant end-user, accounting for an estimated 28% of the cybersecurity spending in 2025, projected at €5,180 Million. This is attributed to the high value of financial assets and customer data, making it a prime target for cyberattacks. The Healthcare sector is another key growth driver, with an estimated spending of €2,300 Million in 2025, driven by the increasing digitization of patient records and the adoption of telemedicine, necessitating stringent Data Security and Infrastructure Protection. The Government & Defense sector's commitment to national security translates to substantial investments, estimated at €2,700 Million in 2025, focusing on advanced Infrastructure Protection and Network Security. The IT and Telecommunication sector's expenditure is estimated at €4,000 Million in 2025, underscoring its role as both a consumer and provider of cybersecurity services. The Manufacturing sector's increasing adoption of Industry 4.0 technologies, with an estimated spend of €1,800 Million in 2025, highlights the growing need for Network Security and Infrastructure Protection to secure industrial control systems.

France Cybersecurity Industry Product Landscape

The French cybersecurity product landscape is characterized by rapid innovation and a growing emphasis on integrated, intelligent solutions. Key product developments include AI-powered threat detection and response platforms that can analyze vast amounts of data in real-time to identify and neutralize sophisticated attacks. Advanced Cloud Security offerings now encompass automated vulnerability assessment and compliance management for multi-cloud environments. In Data Security, advancements in homomorphic encryption and confidential computing are enabling data analysis without compromising privacy. Identity Access Management solutions are evolving to incorporate behavioral biometrics and continuous authentication, offering more seamless yet secure user experiences. The performance metrics of these products are increasingly focused on reduced mean time to detect (MTTD) and mean time to respond (MTTR), alongside improved efficacy against zero-day exploits. Unique selling propositions often lie in vendor-specific threat intelligence feeds, seamless integration capabilities with existing IT ecosystems, and comprehensive post-sales support.

Key Drivers, Barriers & Challenges in France Cybersecurity Industry

The France Cybersecurity Industry is propelled by a combination of powerful drivers. Foremost among these is the escalating frequency and sophistication of cyber threats, including ransomware, phishing, and nation-state attacks, compelling organizations to bolster their defenses. The stringent regulatory environment, particularly the General Data Protection Regulation (GDPR) and upcoming NIS2 Directive, mandates compliance and drives investment in robust security solutions. Digital transformation initiatives, such as cloud adoption and the proliferation of IoT devices, create new attack surfaces, necessitating advanced security measures. Furthermore, the growing awareness of the financial and reputational damage associated with cyber incidents makes proactive security investments a strategic imperative. The French government's commitment to fostering a strong domestic cybersecurity sector through initiatives and funding also acts as a significant growth accelerator.

However, the industry faces several barriers and challenges. A significant challenge is the persistent shortage of skilled cybersecurity professionals, creating a talent gap that hinders the implementation and management of advanced security solutions. The high cost of implementing and maintaining comprehensive cybersecurity programs can be a barrier for small and medium-sized enterprises (SMEs). Evolving threat landscapes require continuous adaptation and innovation, posing a challenge for vendors to keep pace with new attack vectors. Supply chain vulnerabilities, where third-party software or hardware can be compromised, represent a critical risk. Regulatory compliance, while a driver, can also be a challenge due to its complexity and the need for constant updates. Competitive pressures from both established players and agile startups necessitate constant innovation and pricing strategies.

Emerging Opportunities in France Cybersecurity Industry

Emerging opportunities within the France Cybersecurity Industry are diverse and ripe for exploitation. The growing adoption of Artificial Intelligence (AI) and Machine Learning (ML) in cybersecurity presents a significant avenue for innovation, particularly in predictive threat intelligence and automated incident response. The increasing prevalence of hybrid and remote work models is creating a sustained demand for robust endpoint security, secure remote access solutions, and advanced identity and access management tools. The expansion of the Internet of Things (IoT) and Operational Technology (OT) in sectors like manufacturing and smart cities necessitates specialized security solutions to protect these critical interconnected devices. Furthermore, the increasing focus on data privacy and compliance is driving demand for sophisticated data security and privacy-enhancing technologies, such as homomorphic encryption and differential privacy. The development of quantum-resistant cryptography represents a future opportunity to safeguard sensitive data against emerging quantum computing threats.

Growth Accelerators in the France Cybersecurity Industry Industry

Several key growth accelerators are propelling the France Cybersecurity Industry forward. Technological breakthroughs, such as advancements in AI and ML for threat detection, are enhancing the efficacy and efficiency of cybersecurity solutions. Strategic partnerships between cybersecurity vendors, cloud service providers, and IT integrators are expanding market reach and offering more comprehensive solutions. Government initiatives, including funding for research and development and the establishment of national cybersecurity strategies, are fostering innovation and driving adoption. The increasing demand for managed security services (MSS) and Security Operations Centers (SOCs) as a service is enabling businesses, especially SMEs, to access advanced cybersecurity capabilities without significant in-house investment. Market expansion strategies by domestic and international players, focusing on underserved segments and developing tailored solutions for specific industries, are also contributing to sustained growth.

Key Players Shaping the France Cybersecurity Industry Market

- FireEye Inc

- IBM Corporation

- Fortinet Inc

- F5 Networks Inc

- IDECSI Enterprise Security

- Cisco Systems Inc

- AVG Technologies

- Intel Security (Intel Corporation)

- Dell Technologies Inc

Notable Milestones in France Cybersecurity Industry Sector

- 2020 February: Launch of ANSSI's (National Cybersecurity Agency of France) updated strategy for securing critical digital infrastructure, emphasizing enhanced collaboration and threat intelligence sharing.

- 2021 March: Acquisition of Sekoia.io by Thales, bolstering Thales's cybersecurity portfolio with advanced threat intelligence and detection capabilities.

- 2022 May: France's commitment to enhancing cybersecurity for SMEs through government-backed initiatives and funding programs.

- 2023 January: Introduction of new cybersecurity regulations by the French government aimed at strengthening the protection of sensitive data and critical services.

- 2024 Q2: Growing adoption of Zero Trust Architecture principles across French enterprises, driven by increased awareness of insider threats and sophisticated external attacks.

In-Depth France Cybersecurity Industry Market Outlook

The France Cybersecurity Industry is poised for continued robust expansion, driven by persistent cyber threats and an increasing imperative for digital resilience. Growth accelerators such as ongoing technological innovation in AI/ML-driven security, the expansion of cloud-native security solutions, and the government's sustained focus on strengthening national cybersecurity infrastructure will underpin this trajectory. Strategic partnerships and the burgeoning demand for managed security services will further enable market penetration, particularly among SMEs. The outlook suggests a market increasingly defined by integrated, intelligent, and proactive security frameworks, with significant opportunities in cloud security, data protection, and identity management. Stakeholders can anticipate a dynamic environment characterized by continuous evolution in threat landscapes and a corresponding demand for cutting-edge protective measures, ensuring the sector remains a vital component of France's digital economy.

France Cybersecurity Industry Segmentation

-

1. Offering

-

1.1. Security Type

- 1.1.1. Cloud Security

- 1.1.2. Data Security

- 1.1.3. Identity Access Management

- 1.1.4. Network Security

- 1.1.5. Consumer Security

- 1.1.6. Infrastructure Protection

- 1.1.7. Other Types

- 1.2. Services

-

1.1. Security Type

-

2. Deployment

- 2.1. Cloud

- 2.2. On-premise

-

3. End User

- 3.1. BFSI

- 3.2. Healthcare

- 3.3. Manufacturing

- 3.4. Government & Defense

- 3.5. IT and Telecommunication

- 3.6. Other End Users

France Cybersecurity Industry Segmentation By Geography

- 1. France

France Cybersecurity Industry Regional Market Share

Geographic Coverage of France Cybersecurity Industry

France Cybersecurity Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.29% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Offering

- 5.1.1. Security Type

- 5.1.1.1. Cloud Security

- 5.1.1.2. Data Security

- 5.1.1.3. Identity Access Management

- 5.1.1.4. Network Security

- 5.1.1.5. Consumer Security

- 5.1.1.6. Infrastructure Protection

- 5.1.1.7. Other Types

- 5.1.2. Services

- 5.1.1. Security Type

- 5.2. Market Analysis, Insights and Forecast - by Deployment

- 5.2.1. Cloud

- 5.2.2. On-premise

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. BFSI

- 5.3.2. Healthcare

- 5.3.3. Manufacturing

- 5.3.4. Government & Defense

- 5.3.5. IT and Telecommunication

- 5.3.6. Other End Users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. France

- 5.1. Market Analysis, Insights and Forecast - by Offering

- 6. France Cybersecurity Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Offering

- 6.1.1. Security Type

- 6.1.1.1. Cloud Security

- 6.1.1.2. Data Security

- 6.1.1.3. Identity Access Management

- 6.1.1.4. Network Security

- 6.1.1.5. Consumer Security

- 6.1.1.6. Infrastructure Protection

- 6.1.1.7. Other Types

- 6.1.2. Services

- 6.1.1. Security Type

- 6.2. Market Analysis, Insights and Forecast - by Deployment

- 6.2.1. Cloud

- 6.2.2. On-premise

- 6.3. Market Analysis, Insights and Forecast - by End User

- 6.3.1. BFSI

- 6.3.2. Healthcare

- 6.3.3. Manufacturing

- 6.3.4. Government & Defense

- 6.3.5. IT and Telecommunication

- 6.3.6. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Offering

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 FireEye Inc *List Not Exhaustive

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 IBM Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Fortinet Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 F5 Networks Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 IDECSI Enterprise Security

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Cisco Systems Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 AVG Technologies

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Intel Security (Intel Corporation)

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Dell Technologies Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 FireEye Inc *List Not Exhaustive

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: France Cybersecurity Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: France Cybersecurity Industry Share (%) by Company 2025

List of Tables

- Table 1: France Cybersecurity Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 2: France Cybersecurity Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 3: France Cybersecurity Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 4: France Cybersecurity Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: France Cybersecurity Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 6: France Cybersecurity Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 7: France Cybersecurity Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 8: France Cybersecurity Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the France Cybersecurity Industry?

The projected CAGR is approximately 11.29%.

2. Which companies are prominent players in the France Cybersecurity Industry?

Key companies in the market include FireEye Inc *List Not Exhaustive, IBM Corporation, Fortinet Inc, F5 Networks Inc, IDECSI Enterprise Security, Cisco Systems Inc, AVG Technologies, Intel Security (Intel Corporation), Dell Technologies Inc.

3. What are the main segments of the France Cybersecurity Industry?

The market segments include Offering, Deployment, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.18 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Digitalization and Scalable IT Infrastructure; Need to tackle risks from various trends such as third-party vendor risks. the evolution of MSSPs. and adoption of cloud-first strategy.

6. What are the notable trends driving market growth?

Network Security is Expected to Gain Popularity.

7. Are there any restraints impacting market growth?

Lack of Cybersecurity Professionals; High Reliance on Traditional Authentication Methods and Low Preparedness.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "France Cybersecurity Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the France Cybersecurity Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the France Cybersecurity Industry?

To stay informed about further developments, trends, and reports in the France Cybersecurity Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence