Key Insights

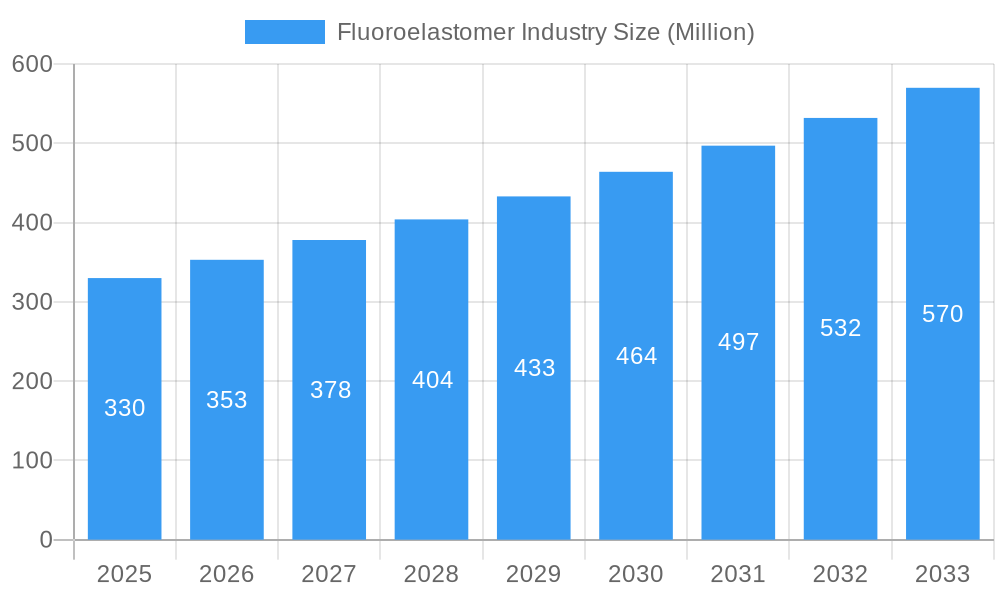

The global Fluoroelastomer market is projected for robust expansion, estimated at USD 0.33 billion in 2025, and is poised to grow at a significant Compound Annual Growth Rate (CAGR) of 6.98% through 2033. This growth is primarily fueled by increasing demand from critical sectors such as automotive and aerospace, where the exceptional resistance of fluoroelastomers to heat, chemicals, and extreme temperatures is indispensable. The automotive industry's transition towards electrification and stringent emission standards necessitates advanced sealing solutions, a key application for these high-performance polymers. Similarly, the aerospace sector's continuous innovation in aircraft design and operations relies heavily on materials that can withstand demanding environments, driving the adoption of fluoroelastomers in critical components like fuel hoses and seals. Furthermore, the burgeoning oil and gas industry, with its challenging operational conditions, also represents a substantial driver for the market, as fluoroelastomers offer superior performance in corrosive and high-pressure scenarios.

Fluoroelastomer Industry Market Size (In Million)

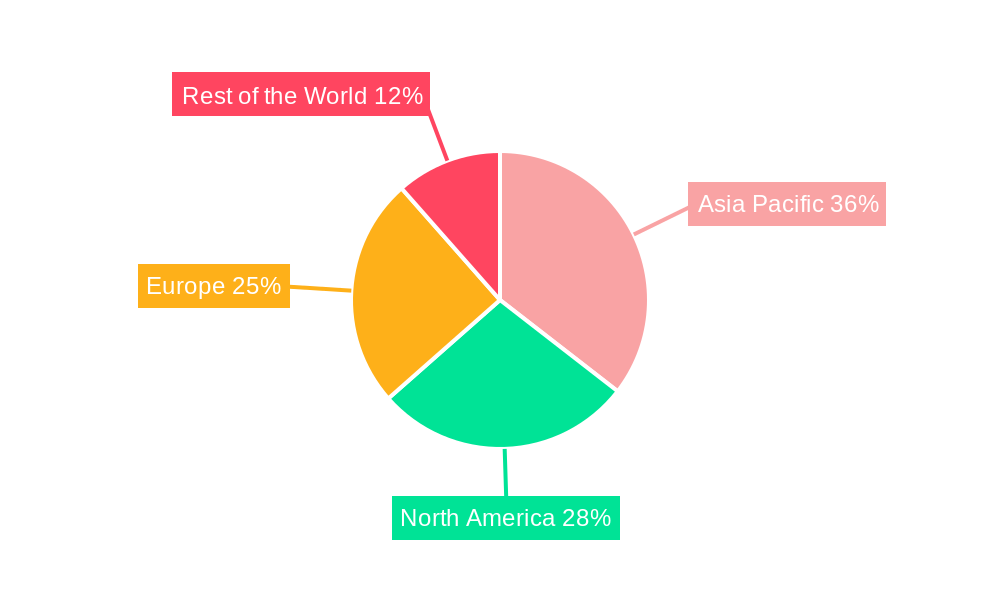

The market's trajectory is further shaped by evolving trends and strategic initiatives from leading players. Innovations in product development, focusing on enhanced properties and specialized grades for niche applications, are expanding the market's reach. Key segments like Fluorocarbon Elastomers and Fluorosilicone Elastomers are witnessing continuous development, catering to diverse end-user needs in diaphragms, valves, O-rings, and seals. While the market presents substantial opportunities, certain restraints, such as the high cost of raw materials and complex manufacturing processes, need to be navigated. However, the persistent demand for high-performance materials in harsh environments, coupled with strategic investments in research and development by companies like Daikin Industries, Solvay, and 3M, are expected to offset these challenges. Geographically, Asia Pacific is anticipated to be a key growth region, driven by rapid industrialization and increasing manufacturing capabilities in countries like China and India, alongside established markets like Japan and South Korea.

Fluoroelastomer Industry Company Market Share

Fluoroelastomer Industry Report: Comprehensive Market Analysis and Forecast (2019-2033)

This in-depth report delivers a comprehensive analysis of the global Fluoroelastomer Industry, providing critical insights into market dynamics, growth trends, regional dominance, product landscape, key drivers, challenges, and emerging opportunities. Covering the historical period from 2019 to 2024, a base and estimated year of 2025, and a forecast period extending to 2033, this report is an essential resource for stakeholders seeking to navigate and capitalize on the evolving fluoroelastomer market. We delve into parent and child market segments, leveraging high-traffic keywords to ensure maximum search engine visibility and engagement with industry professionals, decision-makers, and investors.

Fluoroelastomer Industry Market Dynamics & Structure

The fluoroelastomer market, projected to reach $XX billion by 2025 and forecast to expand to $XX billion by 2033, exhibits a moderate level of market concentration. Key players like Shanghai Fluoron Chemicals Co Ltd, Daikin Industries Ltd, GARLOCK, Solvay, and 3M hold significant shares, driven by continuous technological innovation in developing high-performance materials that withstand extreme temperatures, aggressive chemicals, and harsh environments. Regulatory frameworks, particularly concerning environmental impact and material safety, are increasingly shaping product development and manufacturing processes, necessitating adherence to stringent standards. Competitive product substitutes, such as high-performance silicones and advanced thermoplastics, pose a growing challenge, requiring fluoroelastomer manufacturers to emphasize unique value propositions like superior chemical resistance and thermal stability. End-user demographics are shifting towards industries demanding enhanced reliability and longevity, such as aerospace and advanced automotive applications. Merger and acquisition (M&A) trends are active, with companies seeking to consolidate market presence, acquire innovative technologies, and expand geographical reach. For instance, recent M&A activities aim to integrate specialized product lines and enhance R&D capabilities.

- Market Concentration: Moderate, with a few dominant players.

- Technological Innovation Drivers: Demand for extreme temperature and chemical resistance, advanced sealing solutions.

- Regulatory Frameworks: Increasing focus on environmental compliance and material safety standards.

- Competitive Product Substitutes: High-performance silicones, advanced thermoplastics.

- End-user Demographics: Growing demand from automotive, aerospace, and oil & gas sectors.

- M&A Trends: Strategic acquisitions to enhance product portfolios and market access.

Fluoroelastomer Industry Growth Trends & Insights

The global Fluoroelastomer Industry is on a robust growth trajectory, driven by escalating demand across diverse end-user sectors and continuous technological advancements. The market size, estimated at $XX billion in 2025, is poised for significant expansion, with a projected Compound Annual Growth Rate (CAGR) of XX% during the forecast period (2025-2033). This growth is underpinned by the indispensable properties of fluoroelastomers, including exceptional resistance to heat, chemicals, oils, and fuels, making them critical components in demanding applications. The automotive industry, in particular, is a major growth engine, fueled by the increasing adoption of electric vehicles (EVs) and stringent emission standards that necessitate high-performance sealing solutions for battery systems, fuel lines, and engine components. The aerospace sector's demand for lightweight, durable, and chemically inert materials for seals, O-rings, and hoses further contributes to market expansion.

Technological disruptions, such as the development of advanced manufacturing techniques and novel fluoroelastomer formulations with enhanced properties, are continuously pushing the boundaries of application possibilities. For example, innovations leading to improved processing capabilities and reduced curing times are enhancing manufacturing efficiency and cost-effectiveness. Consumer behavior shifts are also playing a role, with an increasing preference for products that offer longer lifespans, greater reliability, and improved safety, all of which are hallmarks of fluoroelastomer applications. The oil and gas industry continues to be a significant market, with fluoroelastomers essential for seals and components operating in extreme pressures and corrosive environments encountered in exploration, production, and refining. The growing emphasis on sustainability is also driving innovation in fluoroelastomer production and recycling processes.

- Market Size Evolution: Significant expansion from an estimated $XX billion in 2025 to $XX billion by 2033.

- Adoption Rates: High adoption in demanding applications across key industries.

- Technological Disruptions: Development of advanced formulations and manufacturing processes.

- Consumer Behavior Shifts: Growing demand for durable, reliable, and safe products.

- CAGR: Projected XX% during the forecast period.

- Market Penetration: Deep penetration in automotive, aerospace, and oil & gas sectors.

Dominant Regions, Countries, or Segments in Fluoroelastomer Industry

The fluoroelastomer market's dominance is characterized by key regional players and product segments that are setting the pace for growth and innovation. North America and Asia-Pacific are emerging as the leading regions, driven by a confluence of factors including a robust industrial base, significant investments in research and development, and a strong presence of key end-user industries. In North America, the automotive and aerospace sectors, with their stringent material requirements, are primary demand drivers. The region's advanced manufacturing capabilities and the presence of major fluoroelastomer producers like 3M and The Chemours Company contribute to its market leadership. Stringent regulations promoting safety and performance in these sectors further bolster the demand for high-performance fluoroelastomers.

In the Asia-Pacific region, rapid industrialization, particularly in China and India, coupled with substantial investments in infrastructure and manufacturing, has propelled significant growth. The increasing automotive production, coupled with the expansion of the oil and gas industry, fuels demand for specialized elastomers. Countries like China are not only major consumers but also significant producers, with companies such as Shanghai Fluoron Chemicals Co Ltd and Zhonghao Chenguang Research Institute of Chemical Industry playing crucial roles.

From a product type perspective, Fluorocarbon Elastomers (FKM) consistently hold the largest market share, accounting for approximately XX% of the global market in 2025. Their superior performance characteristics in terms of heat, chemical, and oil resistance make them indispensable across a wide range of applications. Fluorosilicone Elastomers and Perfluorocarbon Elastomers cater to more specialized, albeit smaller, market niches requiring extreme temperature ranges and specialized chemical inertness.

In terms of applications, Seals and Sealants represent the largest segment, accounting for around XX% of the market in 2025. This dominance is attributed to their critical role in preventing leaks and protecting sensitive components in virtually all end-user industries. O-rings and Valves also constitute significant sub-segments within this application category.

- Leading Regions: North America and Asia-Pacific dominate due to industrial strength and R&D focus.

- Key Countries: USA, China, Germany, Japan.

- Dominant Product Type: Fluorocarbon Elastomers (FKM) with approximately XX% market share.

- Dominant Application: Seals and Sealants, representing approximately XX% of the market.

- Key Drivers in North America: Advanced automotive and aerospace industries, stringent regulations.

- Key Drivers in Asia-Pacific: Rapid industrialization, growing automotive and oil & gas sectors, manufacturing investments.

- Growth Potential in Other End-user Industries: Chemical and Defense sectors show increasing demand for high-performance materials.

Fluoroelastomer Industry Product Landscape

The fluoroelastomer product landscape is defined by its commitment to high performance and specialized applications. Innovations focus on enhancing chemical resistance, thermal stability, and mechanical properties to meet the evolving demands of critical industries. Key product types include Fluorocarbon Elastomers (FKM), known for their excellent resistance to fuels, oils, and high temperatures, making them ideal for automotive fuel systems and industrial seals. Fluorosilicone Elastomers offer a unique combination of broad temperature range and resistance to fuels and oils, finding applications in aerospace and extreme cold environments. Perfluorocarbon Elastomers (FFKM) represent the pinnacle of chemical inertness and thermal stability, used in highly aggressive chemical processing and semiconductor manufacturing. Performance metrics such as tensile strength, elongation at break, compression set, and chemical resistance are meticulously engineered to meet specific industry standards.

Key Drivers, Barriers & Challenges in Fluoroelastomer Industry

The fluoroelastomer industry is propelled by several key drivers, including the ever-increasing demand for high-performance materials capable of withstanding extreme operating conditions in sectors like automotive, aerospace, and oil & gas. Technological advancements in material science, leading to enhanced properties like superior chemical resistance and thermal stability, are crucial. Growing stringent regulations that mandate safer and more durable components also contribute to market growth.

However, the industry faces significant barriers and challenges. The high cost of raw materials and complex manufacturing processes contribute to the premium pricing of fluoroelastomers, limiting their adoption in cost-sensitive applications. Supply chain volatility and geopolitical factors can impact raw material availability and pricing. Intense competition from alternative high-performance elastomers and the development of new material technologies present ongoing challenges. Environmental concerns and regulatory scrutiny surrounding certain fluorinated compounds necessitate continuous innovation in sustainable production and product alternatives.

Key Drivers:

- Demand for extreme performance (temperature, chemical resistance).

- Growth in automotive, aerospace, and oil & gas industries.

- Technological innovation in material science.

- Stringent regulatory mandates for safety and durability.

Barriers & Challenges:

- High cost of raw materials and production.

- Supply chain disruptions and price volatility.

- Competition from substitute materials.

- Environmental concerns and regulatory scrutiny.

Emerging Opportunities in Fluoroelastomer Industry

Emerging opportunities in the fluoroelastomer industry lie in the continuous innovation of specialized grades and novel applications. The burgeoning electric vehicle (EV) market presents a significant opportunity for fluoroelastomers in battery seals, thermal management systems, and high-voltage cable insulation, where superior chemical resistance and thermal stability are paramount. The expansion of the renewable energy sector, particularly in wind and solar power, also creates demand for durable sealing solutions in harsh environmental conditions. Furthermore, advancements in medical devices and pharmaceutical processing, which require materials with exceptional biocompatibility and chemical inertness, offer lucrative avenues for growth. The development of sustainable fluoroelastomer formulations and circular economy initiatives also presents a significant opportunity for market differentiation and meeting evolving environmental regulations.

Growth Accelerators in the Fluoroelastomer Industry Industry

Several factors are acting as significant growth accelerators for the fluoroelastomer industry. The relentless pursuit of enhanced performance and reliability by key end-user industries, particularly automotive and aerospace, is a primary catalyst. Continuous investment in R&D by leading companies is leading to the development of next-generation fluoroelastomers with improved properties and novel functionalities, thereby expanding their application spectrum. Strategic partnerships and collaborations between material manufacturers and end-users are fostering co-development of customized solutions, accelerating product adoption. Furthermore, the increasing global focus on safety and sustainability standards is driving the demand for high-quality, long-lasting materials, which fluoroelastomers inherently provide, thus acting as a substantial growth accelerator.

Key Players Shaping the Fluoroelastomer Industry Market

- Shanghai Fluoron Chemicals Co Ltd

- Daikin Industries Ltd

- GARLOCK

- Solvay

- Trp Polymer Solutions Limited

- 3M

- Stockwell Elastomerics Inc

- LANXESS

- Eagle Elastomer Inc

- HaloPolymer

- Precision Associates Inc

- Freudenberg Sealing Technologies

- The Chemours Company

- All Seals Inc

- KUREHA CORPORATION

- Zrunek Gummiwaren GmbH

- AGC Inc

- Zhonghao Chenguang Research Institute of Chemical Industry

- Parker Hannifin Corp

- Minor Rubber Products

- Gujarat Fluorochemicals Limited

Notable Milestones in Fluoroelastomer Industry Sector

- January 2022: AGC Chemicals Americas Inc. (AGCCA) announced an expansion at its Thorndale, Pennsylvania, production facility that will add up to 50% more manufacturing, quality control lab, and office space. The multi-use facility will be configured to meet the growing needs of the current business and accommodate future production increases and new capabilities.

- June 2022: Solvay announced that it is introducing to the market a new portfolio of high-performance Tecnoflon peroxide curable fluoroelastomers (FKM) produced without the use of fluorosurfactants. The company aims to transition Tecnoflon® FKM to NFS by the first quarter of 2024.

In-Depth Fluoroelastomer Industry Market Outlook

The future of the fluoroelastomer industry appears exceptionally promising, fueled by an unyielding demand for advanced material solutions in critical sectors. The ongoing transition towards electric mobility, coupled with the expansion of aerospace and defense, will continue to be significant growth accelerators. Innovations in product development, focusing on enhanced thermal management, superior chemical inertness, and improved sustainability, will unlock new application frontiers. Strategic collaborations and capacity expansions by key players, as evidenced by recent milestones, underscore the industry's commitment to meeting escalating global demand. The market is expected to witness a surge in demand for specialized fluoroelastomers that offer tailored performance characteristics, positioning the industry for sustained robust growth and profitability.

Fluoroelastomer Industry Segmentation

-

1. Product Type

- 1.1. Fluorocarbon Elastomers

- 1.2. Fluorosilicone Elastomers

- 1.3. Perfluorocarbon Elastomers

-

2. Application

- 2.1. Diaphragms

- 2.2. Valves

- 2.3. O-rings, Seals, and Sealants

- 2.4. Other Applications (Fuel Hoses, Joints)

-

3. End-user Industry

- 3.1. Automotive

- 3.2. Aerospace

- 3.3. Oil and Gas

- 3.4. Industrial

- 3.5. Other End-user Industries (Chemical, Defense)

Fluoroelastomer Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. Italy

- 3.4. France

- 3.5. Rest of Europe

-

4. Rest of the World

- 4.1. Brazil

- 4.2. Saudi Arabia

- 4.3. South Africa

- 4.4. Rest of the World

Fluoroelastomer Industry Regional Market Share

Geographic Coverage of Fluoroelastomer Industry

Fluoroelastomer Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.85% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Fluorocarbon Elastomers

- 5.1.2. Fluorosilicone Elastomers

- 5.1.3. Perfluorocarbon Elastomers

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Diaphragms

- 5.2.2. Valves

- 5.2.3. O-rings, Seals, and Sealants

- 5.2.4. Other Applications (Fuel Hoses, Joints)

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Automotive

- 5.3.2. Aerospace

- 5.3.3. Oil and Gas

- 5.3.4. Industrial

- 5.3.5. Other End-user Industries (Chemical, Defense)

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Asia Pacific

- 5.4.2. North America

- 5.4.3. Europe

- 5.4.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global Fluoroelastomer Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Fluorocarbon Elastomers

- 6.1.2. Fluorosilicone Elastomers

- 6.1.3. Perfluorocarbon Elastomers

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Diaphragms

- 6.2.2. Valves

- 6.2.3. O-rings, Seals, and Sealants

- 6.2.4. Other Applications (Fuel Hoses, Joints)

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Automotive

- 6.3.2. Aerospace

- 6.3.3. Oil and Gas

- 6.3.4. Industrial

- 6.3.5. Other End-user Industries (Chemical, Defense)

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Asia Pacific Fluoroelastomer Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Fluorocarbon Elastomers

- 7.1.2. Fluorosilicone Elastomers

- 7.1.3. Perfluorocarbon Elastomers

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Diaphragms

- 7.2.2. Valves

- 7.2.3. O-rings, Seals, and Sealants

- 7.2.4. Other Applications (Fuel Hoses, Joints)

- 7.3. Market Analysis, Insights and Forecast - by End-user Industry

- 7.3.1. Automotive

- 7.3.2. Aerospace

- 7.3.3. Oil and Gas

- 7.3.4. Industrial

- 7.3.5. Other End-user Industries (Chemical, Defense)

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. North America Fluoroelastomer Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Fluorocarbon Elastomers

- 8.1.2. Fluorosilicone Elastomers

- 8.1.3. Perfluorocarbon Elastomers

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Diaphragms

- 8.2.2. Valves

- 8.2.3. O-rings, Seals, and Sealants

- 8.2.4. Other Applications (Fuel Hoses, Joints)

- 8.3. Market Analysis, Insights and Forecast - by End-user Industry

- 8.3.1. Automotive

- 8.3.2. Aerospace

- 8.3.3. Oil and Gas

- 8.3.4. Industrial

- 8.3.5. Other End-user Industries (Chemical, Defense)

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Europe Fluoroelastomer Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Fluorocarbon Elastomers

- 9.1.2. Fluorosilicone Elastomers

- 9.1.3. Perfluorocarbon Elastomers

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Diaphragms

- 9.2.2. Valves

- 9.2.3. O-rings, Seals, and Sealants

- 9.2.4. Other Applications (Fuel Hoses, Joints)

- 9.3. Market Analysis, Insights and Forecast - by End-user Industry

- 9.3.1. Automotive

- 9.3.2. Aerospace

- 9.3.3. Oil and Gas

- 9.3.4. Industrial

- 9.3.5. Other End-user Industries (Chemical, Defense)

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. Rest of the World Fluoroelastomer Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Fluorocarbon Elastomers

- 10.1.2. Fluorosilicone Elastomers

- 10.1.3. Perfluorocarbon Elastomers

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Diaphragms

- 10.2.2. Valves

- 10.2.3. O-rings, Seals, and Sealants

- 10.2.4. Other Applications (Fuel Hoses, Joints)

- 10.3. Market Analysis, Insights and Forecast - by End-user Industry

- 10.3.1. Automotive

- 10.3.2. Aerospace

- 10.3.3. Oil and Gas

- 10.3.4. Industrial

- 10.3.5. Other End-user Industries (Chemical, Defense)

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Shanghai Fluoron Chemicals Co Ltd

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Daikin Industries Ltd

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 GARLOCK

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Solvay

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Trp Polymer Solutions Limited

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 3M

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Stockwell Elastomerics Inc

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 LANXESS

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Eagle Elastomer Inc

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 HaloPolymer

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 Precision Associates Inc

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 Freudenberg Sealing Technologies

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.13 The Chemours Company

- 11.1.13.1. Company Overview

- 11.1.13.2. Products

- 11.1.13.3. Company Financials

- 11.1.13.4. SWOT Analysis

- 11.1.14 All Seals Inc

- 11.1.14.1. Company Overview

- 11.1.14.2. Products

- 11.1.14.3. Company Financials

- 11.1.14.4. SWOT Analysis

- 11.1.15 KUREHA CORPORATION

- 11.1.15.1. Company Overview

- 11.1.15.2. Products

- 11.1.15.3. Company Financials

- 11.1.15.4. SWOT Analysis

- 11.1.16 Zrunek Gummiwaren GmbH*List Not Exhaustive

- 11.1.16.1. Company Overview

- 11.1.16.2. Products

- 11.1.16.3. Company Financials

- 11.1.16.4. SWOT Analysis

- 11.1.17 AGC Inc

- 11.1.17.1. Company Overview

- 11.1.17.2. Products

- 11.1.17.3. Company Financials

- 11.1.17.4. SWOT Analysis

- 11.1.18 Zhonghao Chenguang Research Institute of Chemical Industry

- 11.1.18.1. Company Overview

- 11.1.18.2. Products

- 11.1.18.3. Company Financials

- 11.1.18.4. SWOT Analysis

- 11.1.19 Parker Hannifin Corp

- 11.1.19.1. Company Overview

- 11.1.19.2. Products

- 11.1.19.3. Company Financials

- 11.1.19.4. SWOT Analysis

- 11.1.20 Minor Rubber Products

- 11.1.20.1. Company Overview

- 11.1.20.2. Products

- 11.1.20.3. Company Financials

- 11.1.20.4. SWOT Analysis

- 11.1.21 Gujarat Fluorochemicals Limited

- 11.1.21.1. Company Overview

- 11.1.21.2. Products

- 11.1.21.3. Company Financials

- 11.1.21.4. SWOT Analysis

- 11.1.1 Shanghai Fluoron Chemicals Co Ltd

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Fluoroelastomer Industry Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: Asia Pacific Fluoroelastomer Industry Revenue (million), by Product Type 2025 & 2033

- Figure 3: Asia Pacific Fluoroelastomer Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 4: Asia Pacific Fluoroelastomer Industry Revenue (million), by Application 2025 & 2033

- Figure 5: Asia Pacific Fluoroelastomer Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: Asia Pacific Fluoroelastomer Industry Revenue (million), by End-user Industry 2025 & 2033

- Figure 7: Asia Pacific Fluoroelastomer Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 8: Asia Pacific Fluoroelastomer Industry Revenue (million), by Country 2025 & 2033

- Figure 9: Asia Pacific Fluoroelastomer Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: North America Fluoroelastomer Industry Revenue (million), by Product Type 2025 & 2033

- Figure 11: North America Fluoroelastomer Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 12: North America Fluoroelastomer Industry Revenue (million), by Application 2025 & 2033

- Figure 13: North America Fluoroelastomer Industry Revenue Share (%), by Application 2025 & 2033

- Figure 14: North America Fluoroelastomer Industry Revenue (million), by End-user Industry 2025 & 2033

- Figure 15: North America Fluoroelastomer Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 16: North America Fluoroelastomer Industry Revenue (million), by Country 2025 & 2033

- Figure 17: North America Fluoroelastomer Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Europe Fluoroelastomer Industry Revenue (million), by Product Type 2025 & 2033

- Figure 19: Europe Fluoroelastomer Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 20: Europe Fluoroelastomer Industry Revenue (million), by Application 2025 & 2033

- Figure 21: Europe Fluoroelastomer Industry Revenue Share (%), by Application 2025 & 2033

- Figure 22: Europe Fluoroelastomer Industry Revenue (million), by End-user Industry 2025 & 2033

- Figure 23: Europe Fluoroelastomer Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: Europe Fluoroelastomer Industry Revenue (million), by Country 2025 & 2033

- Figure 25: Europe Fluoroelastomer Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Rest of the World Fluoroelastomer Industry Revenue (million), by Product Type 2025 & 2033

- Figure 27: Rest of the World Fluoroelastomer Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 28: Rest of the World Fluoroelastomer Industry Revenue (million), by Application 2025 & 2033

- Figure 29: Rest of the World Fluoroelastomer Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Rest of the World Fluoroelastomer Industry Revenue (million), by End-user Industry 2025 & 2033

- Figure 31: Rest of the World Fluoroelastomer Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 32: Rest of the World Fluoroelastomer Industry Revenue (million), by Country 2025 & 2033

- Figure 33: Rest of the World Fluoroelastomer Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Fluoroelastomer Industry Revenue million Forecast, by Product Type 2020 & 2033

- Table 2: Global Fluoroelastomer Industry Revenue million Forecast, by Application 2020 & 2033

- Table 3: Global Fluoroelastomer Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 4: Global Fluoroelastomer Industry Revenue million Forecast, by Region 2020 & 2033

- Table 5: Global Fluoroelastomer Industry Revenue million Forecast, by Product Type 2020 & 2033

- Table 6: Global Fluoroelastomer Industry Revenue million Forecast, by Application 2020 & 2033

- Table 7: Global Fluoroelastomer Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 8: Global Fluoroelastomer Industry Revenue million Forecast, by Country 2020 & 2033

- Table 9: China Fluoroelastomer Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: India Fluoroelastomer Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 11: Japan Fluoroelastomer Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 12: South Korea Fluoroelastomer Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 13: Rest of Asia Pacific Fluoroelastomer Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Global Fluoroelastomer Industry Revenue million Forecast, by Product Type 2020 & 2033

- Table 15: Global Fluoroelastomer Industry Revenue million Forecast, by Application 2020 & 2033

- Table 16: Global Fluoroelastomer Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 17: Global Fluoroelastomer Industry Revenue million Forecast, by Country 2020 & 2033

- Table 18: United States Fluoroelastomer Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 19: Canada Fluoroelastomer Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Mexico Fluoroelastomer Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: Global Fluoroelastomer Industry Revenue million Forecast, by Product Type 2020 & 2033

- Table 22: Global Fluoroelastomer Industry Revenue million Forecast, by Application 2020 & 2033

- Table 23: Global Fluoroelastomer Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 24: Global Fluoroelastomer Industry Revenue million Forecast, by Country 2020 & 2033

- Table 25: Germany Fluoroelastomer Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: United Kingdom Fluoroelastomer Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Italy Fluoroelastomer Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: France Fluoroelastomer Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 29: Rest of Europe Fluoroelastomer Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 30: Global Fluoroelastomer Industry Revenue million Forecast, by Product Type 2020 & 2033

- Table 31: Global Fluoroelastomer Industry Revenue million Forecast, by Application 2020 & 2033

- Table 32: Global Fluoroelastomer Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 33: Global Fluoroelastomer Industry Revenue million Forecast, by Country 2020 & 2033

- Table 34: Brazil Fluoroelastomer Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: Saudi Arabia Fluoroelastomer Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: South Africa Fluoroelastomer Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Rest of the World Fluoroelastomer Industry Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Fluoroelastomer Industry?

The projected CAGR is approximately 4.85%.

2. Which companies are prominent players in the Fluoroelastomer Industry?

Key companies in the market include Shanghai Fluoron Chemicals Co Ltd, Daikin Industries Ltd, GARLOCK, Solvay, Trp Polymer Solutions Limited, 3M, Stockwell Elastomerics Inc, LANXESS, Eagle Elastomer Inc, HaloPolymer, Precision Associates Inc, Freudenberg Sealing Technologies, The Chemours Company, All Seals Inc, KUREHA CORPORATION, Zrunek Gummiwaren GmbH*List Not Exhaustive, AGC Inc, Zhonghao Chenguang Research Institute of Chemical Industry, Parker Hannifin Corp, Minor Rubber Products, Gujarat Fluorochemicals Limited.

3. What are the main segments of the Fluoroelastomer Industry?

The market segments include Product Type, Application, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 2157 million as of 2022.

5. What are some drivers contributing to market growth?

Rising Usage in Sealing Applications; Surging Applications in the Automotive Industry.

6. What are the notable trends driving market growth?

Increasing Demand for Fluorocarbon Elastomers.

7. Are there any restraints impacting market growth?

Increasingly Stringent Environmental Regulations and Hazardous Working Conditions; Other Restraints.

8. Can you provide examples of recent developments in the market?

January 2022: AGC Chemicals Americas Inc. (AGCCA) announced an expansion at its Thorndale, Pennsylvania, production facility that will add up to 50% more manufacturing, quality control lab, and office space. The multi-use facility will be configured to meet the growing needs of the current business and accommodate future production increases and new capabilities.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Fluoroelastomer Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Fluoroelastomer Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Fluoroelastomer Industry?

To stay informed about further developments, trends, and reports in the Fluoroelastomer Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence