Key Insights

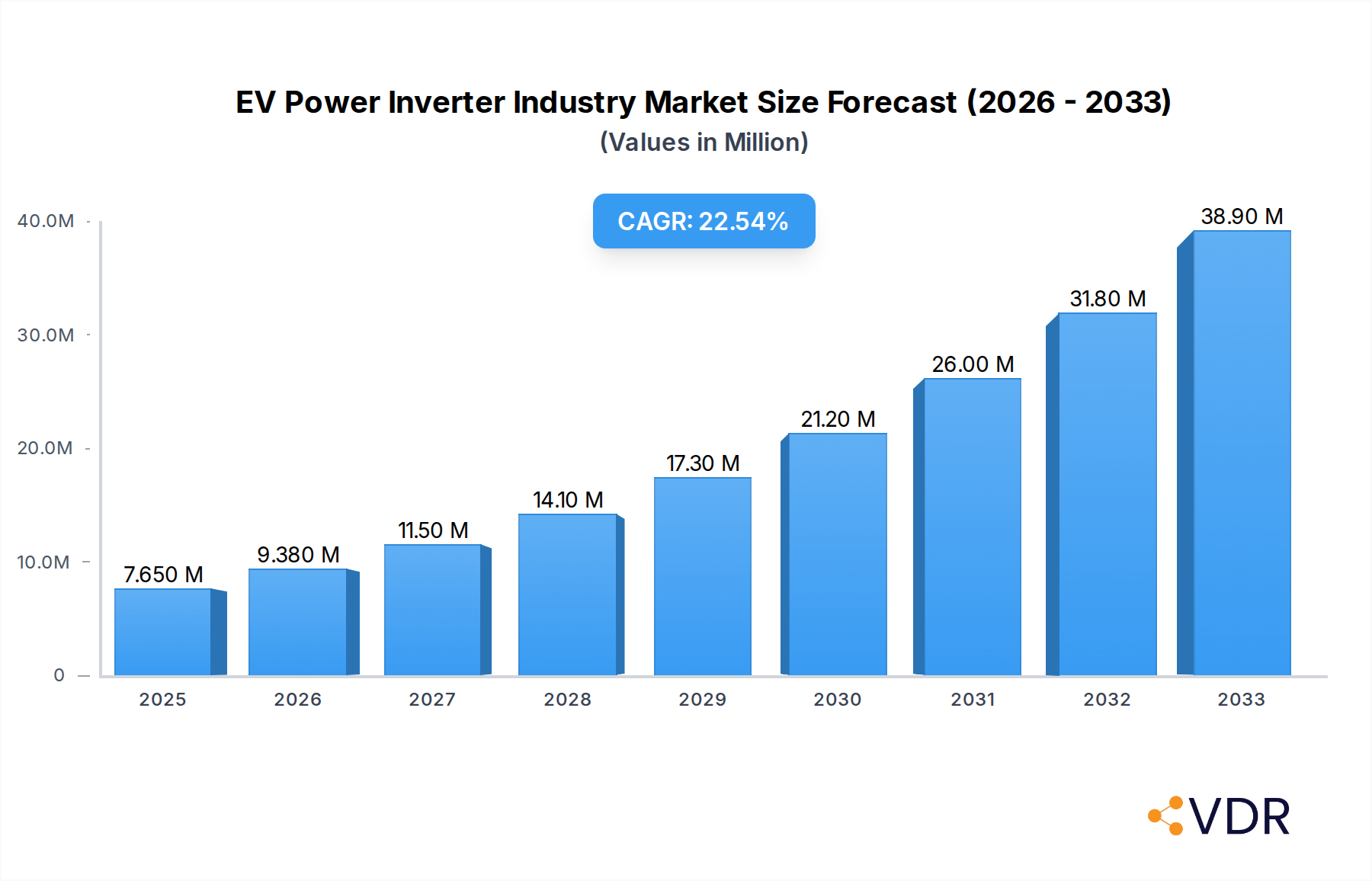

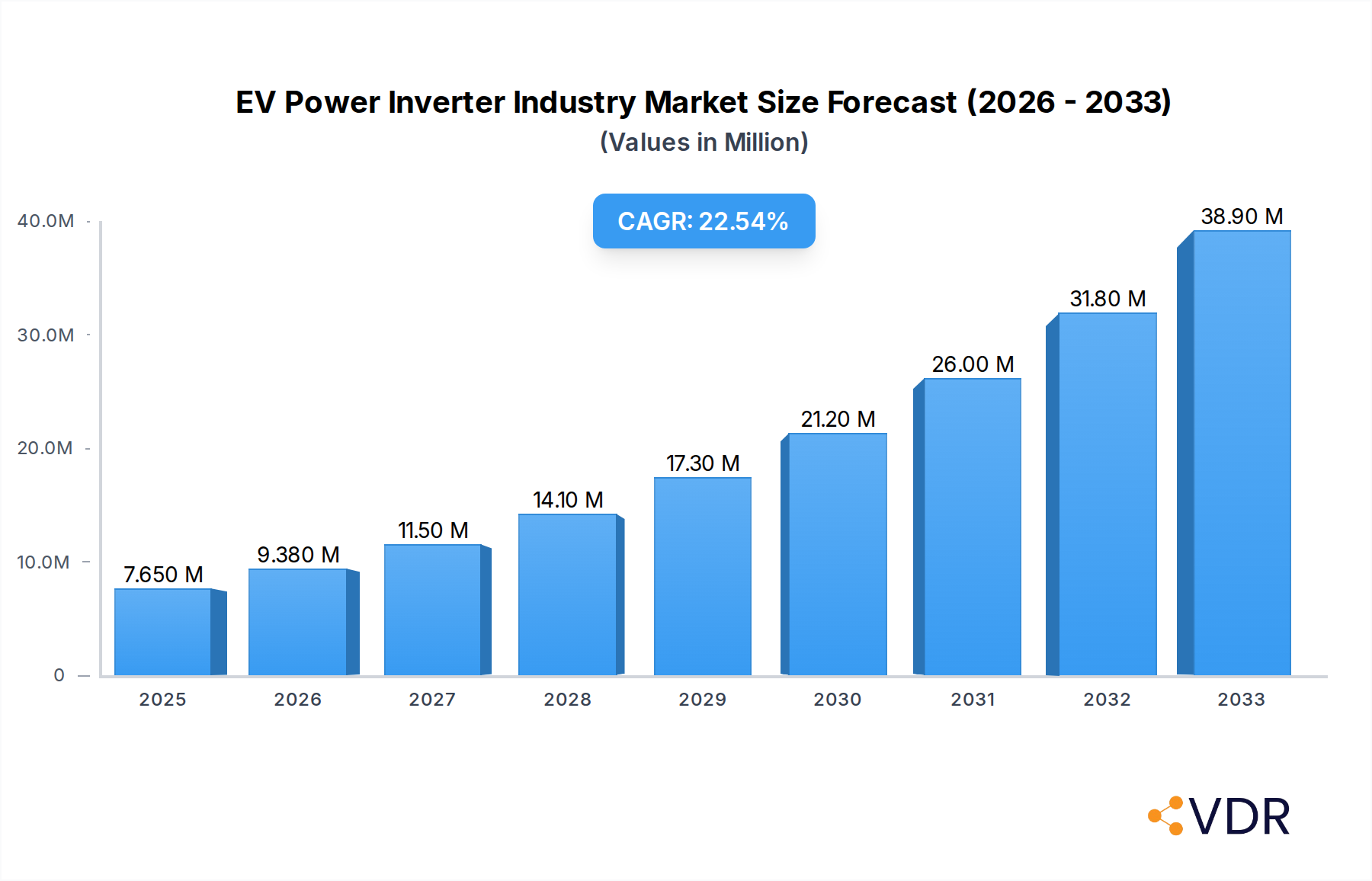

The global EV Power Inverter market is experiencing unprecedented growth, projected to reach a substantial $7.65 million by 2025, fueled by a remarkable CAGR of 22.66%. This significant expansion is primarily driven by the escalating demand for electric vehicles (EVs) across all segments. Key drivers include stringent government regulations promoting zero-emission transportation, substantial advancements in battery technology leading to increased EV range and affordability, and a growing consumer preference for sustainable mobility solutions. The burgeoning EV infrastructure, encompassing charging stations and grid modernization efforts, also plays a crucial role in accelerating market adoption. Furthermore, technological innovations in power electronics, such as the integration of silicon carbide (SiC) and gallium nitride (GaN) semiconductors, are enhancing inverter efficiency, power density, and reliability, thereby reducing overall EV costs and improving performance.

EV Power Inverter Industry Market Size (In Million)

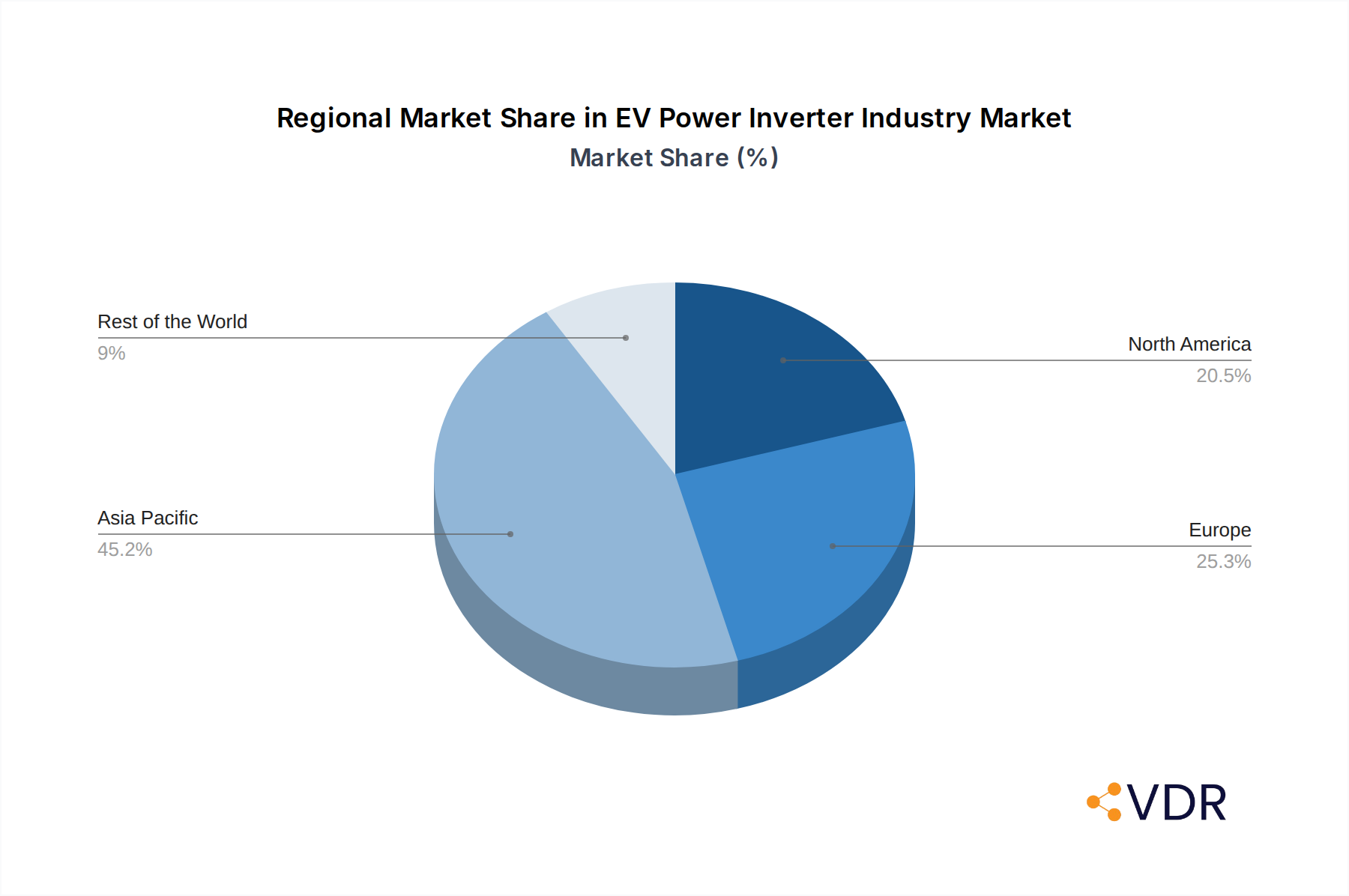

The market is segmented across various propulsion types, with Battery Electric Vehicles (BEVs) dominating due to their widespread adoption and increasing model availability. Plug-in Hybrid Electric Vehicles (PHEVs) also represent a significant segment, offering a transitional solution for consumers. Fuel Cell Electric Vehicles (FCEVs) are poised for future growth as hydrogen infrastructure develops. In terms of vehicle types, passenger cars are the largest segment, followed by commercial vehicles, which are increasingly electrifying for logistical efficiency and environmental compliance. Geographically, the Asia Pacific region, particularly China, is a dominant force, driven by robust government support, a mature automotive manufacturing base, and a rapidly growing EV consumer market. North America and Europe are also witnessing substantial growth, propelled by favorable policies and a strong emphasis on sustainability. Key players like Robert Bosch GmbH, Infineon Technologies AG, and DENSO Corporation are actively investing in research and development to lead this dynamic market.

EV Power Inverter Industry Company Market Share

This comprehensive report delves into the dynamic EV power inverter market, analyzing its intricate structure, growth trajectory, and future potential. With the global shift towards electric mobility, power inverters, crucial components for converting DC power from batteries to AC power for electric motors, are experiencing unprecedented demand. Our analysis covers the parent EV power inverter market and its key child markets, including inverters for hybrid electric vehicles (HEVs), plug-in hybrid electric vehicles (PHEVs), battery electric vehicles (BEVs), and fuel cell electric vehicles (FCEVs). We meticulously examine the influence of passenger cars and commercial vehicles on this evolving landscape.

The report provides deep insights into market dynamics, growth trends, regional dominance, product innovations, key players, and significant milestones shaping the electric vehicle inverter industry. With a focus on data-driven analysis and industry expertise, this report is an indispensable resource for stakeholders seeking to navigate and capitalize on the rapidly expanding automotive power electronics market and the broader electrification of transport.

EV Power Inverter Industry Market Dynamics & Structure

The EV power inverter industry is characterized by intense technological innovation, driven by the relentless pursuit of higher efficiency, smaller form factors, and improved thermal management. Regulatory frameworks, such as stringent emission standards and government incentives for EV adoption, are significant market shapers. Competitive product substitutes, while currently limited to traditional internal combustion engine components, are rapidly being outpaced by the advancements in EV power electronics. End-user demographics are shifting towards environmentally conscious consumers and fleet operators seeking cost savings and improved performance. Mergers and acquisitions (M&A) are a notable trend, with larger players consolidating their market positions and acquiring specialized technological capabilities.

- Market Concentration: The market exhibits moderate concentration, with several key global players dominating market share.

- Technological Innovation Drivers: Demand for longer EV range, faster charging, and improved driving dynamics directly fuels innovation in inverter technology, particularly in areas like wide-bandgap semiconductor adoption.

- Regulatory Frameworks: Government mandates on EV sales and emissions targets are a primary catalyst for inverter market growth.

- Competitive Product Substitutes: While direct substitutes are scarce for the core function, advancements in integrated drive units are transforming the competitive landscape.

- End-User Demographics: Growing consumer awareness of climate change and rising fuel costs are driving demand for EVs and, consequently, power inverters.

- M&A Trends: Expect continued consolidation as companies seek to achieve economies of scale and expand their product portfolios.

EV Power Inverter Industry Growth Trends & Insights

The EV power inverter market is poised for substantial growth, driven by the accelerating adoption of electric vehicles globally. This upward trajectory is underpinned by several interconnected factors, including advancements in battery technology, the increasing availability of charging infrastructure, and supportive government policies aimed at decarbonizing transportation. As the automotive industry transitions from internal combustion engines to electric powertrains, the demand for sophisticated and efficient power inverters is set to surge. This evolution is not merely about replacing components but fundamentally re-architecting vehicle propulsion systems, leading to a demand for higher power density and superior thermal performance from inverters.

The market is witnessing a significant CAGR, as projected by our analysis, fueled by both the increasing penetration of Battery Electric Vehicles (BEVs) and the sustained demand from Hybrid Electric Vehicles (HEVs) and Plug-in Hybrid Electric Vehicles (PHEVs). Technological disruptions, such as the widespread adoption of silicon carbide (SiC) and gallium nitride (GaN) semiconductors, are enabling inverters to operate at higher frequencies and temperatures, leading to increased efficiency and reduced size. Consumer behavior is also shifting, with a growing preference for EVs driven by lower running costs, enhanced driving experience, and environmental consciousness. This confluence of technological, economic, and social factors is creating a robust growth environment for the EV power inverter industry. The base year of 2025 is a pivotal point, reflecting current market penetration, while the forecast period through 2033 anticipates exponential expansion.

Dominant Regions, Countries, or Segments in EV Power Inverter Industry

The Battery Electric Vehicle (BEV) segment is unequivocally the dominant force driving growth in the EV power inverter industry. This dominance stems from the sheer volume of BEVs being deployed globally, driven by advancements in battery technology, increasing model availability, and supportive government policies. Within the BEV segment, Passenger Cars represent the largest sub-segment, accounting for a significant portion of inverter demand due to their widespread consumer adoption and expanding model lineups across various price points.

Key drivers for this dominance include:

- Government Policies and Incentives: Many countries are implementing aggressive targets for EV adoption and offering substantial subsidies, tax credits, and charging infrastructure investments, which directly boost BEV sales.

- Technological Advancements in BEVs: Continuous improvements in battery energy density, charging speeds, and overall vehicle range make BEVs increasingly attractive to consumers, directly translating to higher inverter demand.

- Automaker Commitments: Major automotive manufacturers are heavily investing in and committing to electrifying their fleets, with BEVs being the primary focus, leading to substantial production volumes and inverter procurement.

- Growing Consumer Acceptance: As awareness of the environmental benefits and long-term cost savings of BEVs increases, consumer demand is steadily rising, creating a positive feedback loop for the market.

- Infrastructure Development: The expanding public and private charging infrastructure network is alleviating range anxiety, further accelerating BEV adoption.

While Hybrid Electric Vehicles (HEVs) and Plug-in Hybrid Electric Vehicles (PHEVs) continue to play a vital role, particularly in regions with evolving charging infrastructure, their growth trajectory is outpaced by the rapid expansion of the BEV market. Fuel Cell Electric Vehicles (FCEVs) represent a nascent but promising segment, with significant long-term potential, but their current market share in terms of inverter demand is considerably smaller. Consequently, the strategic focus for power inverter manufacturers remains firmly on the burgeoning BEV segment.

EV Power Inverter Industry Product Landscape

The EV power inverter product landscape is defined by rapid innovation in power electronics, driven by the need for higher efficiency, greater power density, and improved thermal management. Manufacturers are increasingly adopting wide-bandgap semiconductor technologies like Silicon Carbide (SiC) and Gallium Nitride (GaN), enabling inverters to operate at higher switching frequencies and withstand elevated temperatures. This leads to smaller, lighter, and more efficient inverter units. Innovations include integrated drive units that combine the inverter, motor, and gearbox into a single module, optimizing packaging and reducing complexity. Furthermore, advanced cooling solutions, such as direct water-cooling and advanced thermal interface materials, are crucial for dissipating heat generated by high-power inverters, ensuring reliability and performance.

Key Drivers, Barriers & Challenges in EV Power Inverter Industry

Key Drivers:

- Government Regulations and Incentives: Stringent emission standards and subsidies for EVs are primary growth catalysts.

- Technological Advancements: The adoption of SiC and GaN semiconductors is improving inverter efficiency and performance.

- Increasing EV Adoption Rates: The global shift towards electrification, particularly in passenger cars and commercial vehicles, fuels demand.

- Declining Battery Costs: As battery prices decrease, EVs become more accessible, boosting inverter sales.

- Growing Environmental Consciousness: Consumer and corporate demand for sustainable transportation solutions is on the rise.

Barriers & Challenges:

- Supply Chain Volatility: Shortages of critical components and raw materials, especially semiconductors, can disrupt production.

- High Manufacturing Costs: The advanced technology and complex manufacturing processes contribute to higher initial costs for inverters.

- Thermal Management: Efficiently dissipating heat generated by high-power inverters remains a significant engineering challenge.

- Standardization and Interoperability: A lack of universal standards for inverter interfaces and communication protocols can create integration complexities.

- Intense Competition: The market is competitive, with established players and new entrants vying for market share, leading to pricing pressures.

Emerging Opportunities in EV Power Inverter Industry

Emerging opportunities in the EV power inverter industry are abundant, driven by the accelerating pace of electrification across various vehicle types and applications. The expansion of the commercial vehicle segment, including electric trucks, vans, and buses, presents a significant untapped market with unique power requirements. Furthermore, the development of advanced charging solutions, such as bi-directional charging (Vehicle-to-Grid/Vehicle-to-Home), is creating new avenues for inverter functionality and integration. The increasing interest in autonomous driving systems also presents opportunities for intelligent inverters capable of sophisticated control and communication. Finally, niche applications in off-highway vehicles, marine applications, and industrial power systems are beginning to explore electric propulsion, opening new markets for power inverter technologies.

Growth Accelerators in the EV Power Inverter Industry Industry

Several key catalysts are accelerating the long-term growth of the EV power inverter industry. Technological breakthroughs, particularly in wide-bandgap semiconductor materials like Silicon Carbide (SiC) and Gallium Nitride (GaN), are enabling higher efficiencies, smaller footprints, and improved thermal performance, making EVs more viable and attractive. Strategic partnerships between inverter manufacturers, automotive OEMs, and battery suppliers are crucial for co-development and integration, ensuring seamless performance and optimizing supply chains. Market expansion strategies, including the penetration of emerging economies and the development of specialized inverter solutions for different vehicle segments (e.g., heavy-duty trucks, performance vehicles), are also significant growth drivers. The continuous innovation in energy management systems and the increasing demand for electrification in other transportation sectors beyond passenger cars will further fuel this growth.

Key Players Shaping the EV Power Inverter Industry Market

- Infineon Technologies AG

- Hitachi Astemo Ltd

- Vitesco Technologies

- Toyota Industries Corporation

- Mitsubishi Electric Corporation

- Meidensha Corporation

- Robert Bosch GmbH

- Aptiv PLC (Borgwarner Inc )

- Lear Corporation

- Valeo Group

- DENSO Corporation

- Eaton Corporation

- Marelli Corporation

Notable Milestones in EV Power Inverter Industry Sector

- September 2022: Robert Bosch GmbH introduced a new drive unit consisting of an electric motor plus an integrated inverter for small trucks. Bosch has reduced electrical losses by more than 20% with new semiconductors, which enables an inverter efficiency of 97% and thus increases the range.

- August 2022: AVL List GmbH developed a new Inverter Test System for testing inverters separately from the e-motor and battery.

- December 2021: Hitachi Astemo Ltd announced that the company's inverter had been adopted for the hybrid powertrain platform "Leishen Hi-X" of Geely Automobile Holdings Limited. It is equipped with a direct water-cooled double-sided cooling power module characterized by its small size and high output.

- March 2021: Continental informed that it has developed high-power electronics including controllers and a DC-AC inverter system solution for Jaguar Land Rover that is specifically adapted to the requirements of sporty, performance-oriented powertrains. The power electronics module is claimed to have a high current-bearing capacity of up to 650A.

In-Depth EV Power Inverter Industry Market Outlook

The EV power inverter industry is set for a robust and sustained period of growth, driven by the irreversible global transition towards electrified mobility. The increasing demand for higher efficiency, reduced cost, and compact power electronics will continue to fuel innovation, particularly in advanced semiconductor technologies. Strategic collaborations between industry players, coupled with supportive government policies and infrastructure development, will act as significant growth accelerators. Emerging opportunities in commercial vehicle electrification, bi-directional charging, and niche applications will further diversify and expand the market. Stakeholders who can effectively navigate supply chain complexities, embrace technological advancements, and align with evolving regulatory landscapes will be well-positioned to capitalize on the immense future potential of this dynamic sector.

EV Power Inverter Industry Segmentation

-

1. Propulsion Type

- 1.1. Hybrid Electric Vehicles

- 1.2. Plug-in Hybrid Electric Vehicle

- 1.3. Battery Electric Vehicle

- 1.4. Fuel Cell Electric Vehicle

-

2. Vehicle Type

- 2.1. Passenger Cars

- 2.2. Commercial Vehicles

EV Power Inverter Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Rest of North America

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

-

4. Rest of the World

- 4.1. South America

- 4.2. Middle East and Africa

EV Power Inverter Industry Regional Market Share

Geographic Coverage of EV Power Inverter Industry

EV Power Inverter Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 22.66% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Propulsion Type

- 5.1.1. Hybrid Electric Vehicles

- 5.1.2. Plug-in Hybrid Electric Vehicle

- 5.1.3. Battery Electric Vehicle

- 5.1.4. Fuel Cell Electric Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.2.1. Passenger Cars

- 5.2.2. Commercial Vehicles

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Propulsion Type

- 6. Global EV Power Inverter Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Propulsion Type

- 6.1.1. Hybrid Electric Vehicles

- 6.1.2. Plug-in Hybrid Electric Vehicle

- 6.1.3. Battery Electric Vehicle

- 6.1.4. Fuel Cell Electric Vehicle

- 6.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.2.1. Passenger Cars

- 6.2.2. Commercial Vehicles

- 6.1. Market Analysis, Insights and Forecast - by Propulsion Type

- 7. North America EV Power Inverter Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Propulsion Type

- 7.1.1. Hybrid Electric Vehicles

- 7.1.2. Plug-in Hybrid Electric Vehicle

- 7.1.3. Battery Electric Vehicle

- 7.1.4. Fuel Cell Electric Vehicle

- 7.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 7.2.1. Passenger Cars

- 7.2.2. Commercial Vehicles

- 7.1. Market Analysis, Insights and Forecast - by Propulsion Type

- 8. Europe EV Power Inverter Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Propulsion Type

- 8.1.1. Hybrid Electric Vehicles

- 8.1.2. Plug-in Hybrid Electric Vehicle

- 8.1.3. Battery Electric Vehicle

- 8.1.4. Fuel Cell Electric Vehicle

- 8.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 8.2.1. Passenger Cars

- 8.2.2. Commercial Vehicles

- 8.1. Market Analysis, Insights and Forecast - by Propulsion Type

- 9. Asia Pacific EV Power Inverter Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Propulsion Type

- 9.1.1. Hybrid Electric Vehicles

- 9.1.2. Plug-in Hybrid Electric Vehicle

- 9.1.3. Battery Electric Vehicle

- 9.1.4. Fuel Cell Electric Vehicle

- 9.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 9.2.1. Passenger Cars

- 9.2.2. Commercial Vehicles

- 9.1. Market Analysis, Insights and Forecast - by Propulsion Type

- 10. Rest of the World EV Power Inverter Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Propulsion Type

- 10.1.1. Hybrid Electric Vehicles

- 10.1.2. Plug-in Hybrid Electric Vehicle

- 10.1.3. Battery Electric Vehicle

- 10.1.4. Fuel Cell Electric Vehicle

- 10.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 10.2.1. Passenger Cars

- 10.2.2. Commercial Vehicles

- 10.1. Market Analysis, Insights and Forecast - by Propulsion Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Infineon Technologies AG

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Hitachi Astemo Ltd

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Vitesco Technologies

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Toyota Industries Corporation

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Mitsubishi Electric Corporation

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Meidensha Corporation

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Robert Bosch GmbH

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Aptiv PLC (Borgwarner Inc )

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Lear Corporation

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Valeo Group

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 DENSO Corporation

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 Eaton Corporatio

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.13 Marelli Corporation

- 11.1.13.1. Company Overview

- 11.1.13.2. Products

- 11.1.13.3. Company Financials

- 11.1.13.4. SWOT Analysis

- 11.1.1 Infineon Technologies AG

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global EV Power Inverter Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America EV Power Inverter Industry Revenue (Million), by Propulsion Type 2025 & 2033

- Figure 3: North America EV Power Inverter Industry Revenue Share (%), by Propulsion Type 2025 & 2033

- Figure 4: North America EV Power Inverter Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 5: North America EV Power Inverter Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 6: North America EV Power Inverter Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America EV Power Inverter Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe EV Power Inverter Industry Revenue (Million), by Propulsion Type 2025 & 2033

- Figure 9: Europe EV Power Inverter Industry Revenue Share (%), by Propulsion Type 2025 & 2033

- Figure 10: Europe EV Power Inverter Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 11: Europe EV Power Inverter Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 12: Europe EV Power Inverter Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe EV Power Inverter Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific EV Power Inverter Industry Revenue (Million), by Propulsion Type 2025 & 2033

- Figure 15: Asia Pacific EV Power Inverter Industry Revenue Share (%), by Propulsion Type 2025 & 2033

- Figure 16: Asia Pacific EV Power Inverter Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 17: Asia Pacific EV Power Inverter Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 18: Asia Pacific EV Power Inverter Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Pacific EV Power Inverter Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Rest of the World EV Power Inverter Industry Revenue (Million), by Propulsion Type 2025 & 2033

- Figure 21: Rest of the World EV Power Inverter Industry Revenue Share (%), by Propulsion Type 2025 & 2033

- Figure 22: Rest of the World EV Power Inverter Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 23: Rest of the World EV Power Inverter Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 24: Rest of the World EV Power Inverter Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Rest of the World EV Power Inverter Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global EV Power Inverter Industry Revenue Million Forecast, by Propulsion Type 2020 & 2033

- Table 2: Global EV Power Inverter Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 3: Global EV Power Inverter Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global EV Power Inverter Industry Revenue Million Forecast, by Propulsion Type 2020 & 2033

- Table 5: Global EV Power Inverter Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 6: Global EV Power Inverter Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States EV Power Inverter Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada EV Power Inverter Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Rest of North America EV Power Inverter Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Global EV Power Inverter Industry Revenue Million Forecast, by Propulsion Type 2020 & 2033

- Table 11: Global EV Power Inverter Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 12: Global EV Power Inverter Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Germany EV Power Inverter Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: United Kingdom EV Power Inverter Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: France EV Power Inverter Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Italy EV Power Inverter Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Rest of Europe EV Power Inverter Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Global EV Power Inverter Industry Revenue Million Forecast, by Propulsion Type 2020 & 2033

- Table 19: Global EV Power Inverter Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 20: Global EV Power Inverter Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: China EV Power Inverter Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Japan EV Power Inverter Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: India EV Power Inverter Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: South Korea EV Power Inverter Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Rest of Asia Pacific EV Power Inverter Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Global EV Power Inverter Industry Revenue Million Forecast, by Propulsion Type 2020 & 2033

- Table 27: Global EV Power Inverter Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 28: Global EV Power Inverter Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 29: South America EV Power Inverter Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Middle East and Africa EV Power Inverter Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the EV Power Inverter Industry?

The projected CAGR is approximately 22.66%.

2. Which companies are prominent players in the EV Power Inverter Industry?

Key companies in the market include Infineon Technologies AG, Hitachi Astemo Ltd, Vitesco Technologies, Toyota Industries Corporation, Mitsubishi Electric Corporation, Meidensha Corporation, Robert Bosch GmbH, Aptiv PLC (Borgwarner Inc ), Lear Corporation, Valeo Group, DENSO Corporation, Eaton Corporatio, Marelli Corporation.

3. What are the main segments of the EV Power Inverter Industry?

The market segments include Propulsion Type, Vehicle Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 7.65 Million as of 2022.

5. What are some drivers contributing to market growth?

Rise in demand for Electric Vehicles.

6. What are the notable trends driving market growth?

Growing Sales of Electric Vehicles.

7. Are there any restraints impacting market growth?

High Cost Associated With Product.

8. Can you provide examples of recent developments in the market?

In September 2022, Robert Bosch GmbH introduced a new drive unit consisting of an electric motor plus an integrated inverter for small trucks. Bosch has reduced electrical losses by more than 20% with new semiconductors, which enables an inverter efficiency of 97% and thus increases the range.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "EV Power Inverter Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the EV Power Inverter Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the EV Power Inverter Industry?

To stay informed about further developments, trends, and reports in the EV Power Inverter Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence