Key Insights

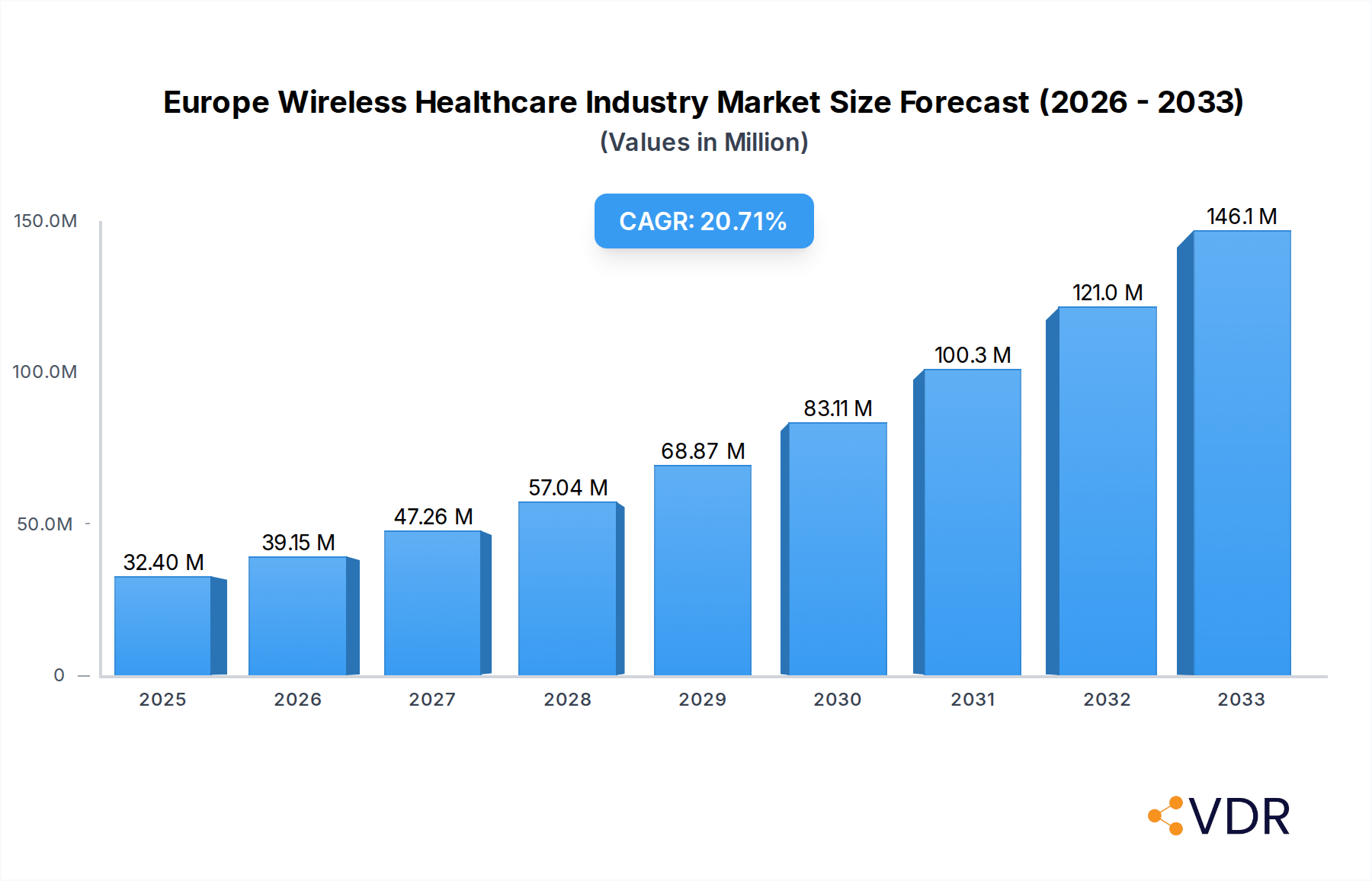

The Europe Wireless Healthcare Industry is poised for substantial expansion, with a projected market size of $32.40 million and a compelling Compound Annual Growth Rate (CAGR) of 20.82%. This robust growth is fueled by a confluence of transformative drivers, primarily the escalating adoption of advanced wireless technologies in healthcare delivery and the increasing demand for remote patient monitoring solutions. The integration of IoT devices, AI-powered diagnostics, and secure wireless communication networks is revolutionizing patient care, enhancing operational efficiency for healthcare providers, and enabling more personalized treatment pathways. Furthermore, the ongoing digital transformation within European healthcare systems, coupled with government initiatives promoting telehealth and connected health, is creating a fertile ground for market expansion. Key trends such as the rise of wearable health trackers, the implementation of 5G in healthcare for faster data transmission and real-time analytics, and the growing preference for home-based care are all contributing to this upward trajectory.

Europe Wireless Healthcare Industry Market Size (In Million)

Despite this promising outlook, the industry faces certain restraints that could temper growth. These include stringent data privacy regulations, cybersecurity concerns surrounding sensitive patient information, and the significant upfront investment required for implementing new wireless healthcare infrastructure. Interoperability challenges between disparate healthcare systems and the need for extensive staff training to effectively utilize new technologies also present hurdles. However, the unwavering focus on improving patient outcomes, reducing healthcare costs, and increasing accessibility to medical services across Europe is expected to drive innovation and overcome these limitations. The market segments, including hardware, software, and services, are all anticipated to witness significant growth, with applications spanning hospitals, nursing homes, home care, and the pharmaceutical sector, indicating a broad-based adoption across the healthcare ecosystem.

Europe Wireless Healthcare Industry Company Market Share

This comprehensive report delivers an in-depth analysis of the Europe Wireless Healthcare Industry, projecting significant growth and transformative innovation. Covering the period from 2019 to 2033, with a base year of 2025, this research explores key market dynamics, growth trends, regional dominance, product landscapes, and the strategic imperatives shaping the future of connected healthcare across Europe.

Europe Wireless Healthcare Industry Market Dynamics & Structure

The Europe Wireless Healthcare Industry is characterized by a moderately concentrated market structure, driven by significant investments in technological innovation and a growing demand for remote patient monitoring and digital health solutions. Key drivers include the increasing prevalence of chronic diseases, the aging population, and government initiatives promoting telehealth adoption. Regulatory frameworks, while evolving, are increasingly supportive of wireless health technologies, fostering innovation and market penetration. However, concerns regarding data privacy, cybersecurity, and the interoperability of different systems present persistent barriers. Competitive product substitutes, such as wired monitoring systems and traditional healthcare delivery models, still exist, but the agility and efficiency offered by wireless solutions are rapidly gaining traction. End-user demographics are shifting, with a growing tech-savvy patient population and healthcare providers actively seeking cost-effective and patient-centric care delivery methods. Mergers and acquisitions (M&A) are a notable trend, with companies seeking to consolidate market share, acquire innovative technologies, and expand their service offerings. For instance, the acquisition of BeWo Unternehmensgruppe by Tunstall Healthcare exemplifies this trend, strengthening the latter's presence in the German telehealth market.

- Market Concentration: Moderately concentrated with a few key players holding significant market share.

- Technological Innovation Drivers: Miniaturization of sensors, advancements in IoT connectivity, AI for data analysis, and cloud computing are paramount.

- Regulatory Frameworks: GDPR compliance, medical device regulations (e.g., MDR), and national telehealth policies influence market entry and product development.

- Competitive Product Substitutes: Wired patient monitoring systems, manual data collection, and traditional in-hospital care.

- End-User Demographics: Aging populations, individuals with chronic conditions, and a growing demand for remote and home-based care.

- M&A Trends: Strategic acquisitions to gain market access, acquire new technologies, and enhance integrated service portfolios.

- Estimated M&A Deal Volume (2019-2024): XX deals.

- Barriers to Innovation: Data security concerns, interoperability challenges, and the need for robust reimbursement models.

Europe Wireless Healthcare Industry Growth Trends & Insights

The Europe Wireless Healthcare Industry is poised for remarkable expansion, driven by a confluence of technological advancements, shifting patient expectations, and supportive healthcare policies. The market size is projected to witness a substantial Compound Annual Growth Rate (CAGR) of approximately XX% from 2025 to 2033. This growth is underpinned by the accelerating adoption of wireless patient monitoring systems, wearable health trackers, and remote diagnostic tools. The COVID-19 pandemic significantly accelerated the acceptance and implementation of telehealth and remote care solutions, permanently altering the healthcare landscape. This has led to increased investment in the underlying infrastructure and services required to support these innovations.

Consumer behavior is evolving rapidly, with a growing segment of the population embracing digital health tools for proactive health management, early disease detection, and convenient access to care. The demand for personalized medicine, enabled by the continuous data streams from wireless devices, is a significant trend. Technological disruptions, such as the advancement of 5G networks, are crucial enablers, providing the high bandwidth and low latency required for real-time data transmission and sophisticated telemedicine applications. Furthermore, the integration of Artificial Intelligence (AI) and Machine Learning (ML) into wireless healthcare platforms is enhancing diagnostic accuracy, enabling predictive analytics for patient deterioration, and personalizing treatment plans. The market penetration of wireless healthcare solutions is expected to reach XX% of the total European healthcare market by 2033. This surge in adoption is fueled by the demonstrable benefits of reduced hospital readmissions, improved patient outcomes, and cost efficiencies for healthcare providers. The shift towards value-based care models further incentivizes the adoption of technologies that can demonstrate improved patient well-being and reduced long-term healthcare expenditure. The increasing awareness of remote patient monitoring's efficacy in managing chronic conditions like diabetes, cardiovascular diseases, and respiratory illnesses is a major catalyst.

- Market Size Evolution (2025): Estimated at $XX Billion.

- Projected Market Size (2033): Expected to reach $XX Billion.

- CAGR (2025-2033): XX%.

- Adoption Rates: Steadily increasing across all segments, with rapid growth in hospitals and home care.

- Technological Disruptions: 5G deployment, AI/ML integration, advanced sensor technology, and cloud-native platforms.

- Consumer Behavior Shifts: Increased demand for proactive health management, personalized care, and convenience.

- Market Penetration: Projected to reach XX% by 2033.

- Key Adoption Catalysts: Chronic disease management, aging population, cost containment pressures, and patient empowerment.

- Value-Based Care Impact: Driving demand for outcome-focused wireless health solutions.

Dominant Regions, Countries, or Segments in Europe Wireless Healthcare Industry

The Hospitals and Nursing Homes segment is currently the dominant force within the Europe Wireless Healthcare Industry, driven by the critical need for enhanced patient monitoring, improved operational efficiency, and reduced healthcare-associated infections. This segment's dominance is further bolstered by substantial investments from healthcare institutions seeking to upgrade their infrastructure and embrace digital transformation. The increasing adoption of wireless patient monitoring systems, such as GE Healthcare's Portrait Mobile, directly caters to the stringent monitoring requirements of hospital environments, enabling continuous patient surveillance and early detection of adverse events. The sheer volume of patient data generated within these settings necessitates robust wireless solutions for real-time access and analysis.

Within this dominant segment, the Hardware component, encompassing sophisticated sensors, wearable devices, and robust networking equipment, plays a pivotal role. Companies like Qualcomm are instrumental in providing the foundational wireless technologies that power these devices. However, the Software segment, including electronic health record (EHR) integration, data analytics platforms, and telehealth applications, is experiencing rapid growth and is crucial for deriving actionable insights from the collected data. Services, such as system integration, maintenance, and data management, are also critical enablers, ensuring the seamless functioning of these complex wireless healthcare ecosystems.

Geographically, Western Europe, particularly countries like Germany, the United Kingdom, France, and the Netherlands, leads the market. This leadership is attributed to their well-established healthcare infrastructures, high levels of technological adoption, significant government funding for digital health initiatives, and a strong emphasis on patient outcomes and preventative care. For example, the United Kingdom's National Health Service (NHS) has been actively promoting the adoption of digital health solutions. The presence of major industry players and a supportive regulatory environment further solidifies the dominance of these regions.

- Dominant Segment: Hospitals and Nursing Homes.

- Key Drivers: Need for continuous patient monitoring, infection control, operational efficiency, and integration with existing EHR systems.

- Market Share (Hospitals & Nursing Homes): Approximately XX%.

- Growth Potential: High, driven by ongoing digital transformation initiatives.

- Leading Component: Hardware.

- Key Drivers: Advancements in sensor technology, miniaturization, and connectivity solutions.

- Market Share (Hardware): Approximately XX%.

- Growth Potential: Strong, fueled by demand for advanced monitoring devices.

- Fastest Growing Component: Software.

- Key Drivers: Demand for data analytics, AI integration, telehealth platforms, and interoperability solutions.

- Market Share (Software): Approximately XX%.

- Growth Potential: Very High, as data utilization becomes paramount.

- Dominant Region: Western Europe.

- Key Drivers: Advanced healthcare infrastructure, high disposable income, strong government support for digital health, and aging population.

- Market Share (Western Europe): Approximately XX%.

- Growth Potential: Sustained growth driven by innovation and adoption.

- Key Country Example: Germany.

- Drivers: Strong R&D capabilities, government funding for digital healthcare, and a focus on patient data security.

- Market Share (Germany): Approximately XX% of Western Europe.

Europe Wireless Healthcare Industry Product Landscape

The Europe Wireless Healthcare Industry product landscape is characterized by rapid innovation and a diverse range of solutions designed to enhance patient care and streamline healthcare operations. Key product developments include advanced wireless patient monitoring systems like GE Healthcare's Portrait Mobile, which leverages patient-worn sensors for continuous monitoring and early detection of patient deterioration. Wearable health trackers and smart medical devices are increasingly sophisticated, offering real-time data on vital signs, activity levels, and sleep patterns.

Software solutions are central to this landscape, enabling seamless data integration, remote diagnostics, and personalized treatment plans. Telehealth platforms facilitate virtual consultations and remote patient management, extending the reach of healthcare providers. The performance metrics of these products are continuously improving, focusing on accuracy, reliability, battery life, and user-friendliness. Unique selling propositions revolve around enhanced patient outcomes, reduced healthcare costs, improved clinician workflow, and greater patient convenience and engagement. Technological advancements are driving miniaturization, improved connectivity (e.g., Bluetooth Low Energy, Wi-Fi, 5G), and the integration of AI for predictive analytics and personalized health insights.

Key Drivers, Barriers & Challenges in Europe Wireless Healthcare Industry

The Europe Wireless Healthcare Industry is propelled by several key drivers, including the escalating burden of chronic diseases, the growing demand for remote patient monitoring, and favorable government initiatives promoting digital health adoption. Technological advancements, such as the evolution of IoT, AI, and 5G, are creating new possibilities for connected healthcare solutions. The increasing preference for home-based care and the desire for greater patient autonomy further fuel market growth.

However, significant barriers and challenges exist. Data security and privacy concerns remain paramount, necessitating robust cybersecurity measures to protect sensitive patient information. Regulatory hurdles, including the need for medical device certifications and compliance with data protection laws like GDPR, can slow down product development and market entry. Interoperability issues between different healthcare IT systems and wireless devices present a challenge to seamless data flow. Furthermore, the initial investment cost for implementing wireless healthcare infrastructure can be a deterrent for some smaller healthcare providers.

- Key Drivers:

- Rising prevalence of chronic diseases (e.g., cardiovascular, diabetes).

- Aging population and demand for elderly care.

- Government support for digital health and telehealth initiatives.

- Technological advancements in IoT, AI, and 5G.

- Patient demand for convenience and remote care options.

- Key Barriers & Challenges:

- Data security and privacy concerns (XX% of providers cite this as a major concern).

- Stringent regulatory requirements and lengthy approval processes.

- Interoperability challenges between diverse healthcare systems.

- High initial implementation costs for some solutions.

- Limited digital literacy among certain patient demographics.

- Reimbursement policy uncertainties in some regions.

Emerging Opportunities in Europe Wireless Healthcare Industry

Emerging opportunities in the Europe Wireless Healthcare Industry lie in the expansion of remote patient monitoring for specialized conditions, the integration of AI-powered predictive analytics, and the development of personalized wellness solutions. The growing elderly population presents a significant untapped market for continuous health monitoring and fall detection systems. Furthermore, the increasing focus on preventative care and chronic disease management opens avenues for proactive health interventions through wearable devices and smart health applications. The potential for using wireless technologies in remote areas to improve healthcare access and equity is another promising avenue.

- Untapped Markets: Remote rural areas, specialized chronic disease management, mental health monitoring.

- Innovative Applications: AI-driven diagnostics, personalized treatment adherence monitoring, remote rehabilitation.

- Evolving Consumer Preferences: Proactive health tracking, virtual wellness coaching, seamless integration with daily life.

- Technological Integration: Combining wearables with augmented reality for enhanced remote consultations.

- Data Monetization: Developing secure platforms for anonymized data analysis to drive public health research.

Growth Accelerators in the Europe Wireless Healthcare Industry Industry

Several critical growth accelerators are poised to propel the Europe Wireless Healthcare Industry forward. The continuous innovation in sensor technology, leading to smaller, more accurate, and power-efficient devices, is a fundamental driver. The widespread deployment of 5G networks will provide the necessary infrastructure for real-time data transmission and advanced telemedicine services. Strategic partnerships between technology providers, healthcare institutions, and pharmaceutical companies are accelerating the development and adoption of integrated solutions. Furthermore, evolving reimbursement policies that recognize the value of remote patient monitoring and telehealth are incentivizing investment and adoption by healthcare providers.

- Technological Breakthroughs: Advanced bio-sensors, miniaturized medical devices, edge computing for on-device data processing.

- Strategic Partnerships: Collaborations between tech giants and healthcare providers (e.g., Apple and various health systems), and alliances with pharmaceutical companies for remote drug adherence monitoring.

- Market Expansion Strategies: Focusing on underserved populations, developing tailored solutions for specific chronic conditions, and expanding into emerging European markets.

- Government Support: Increased funding for digital health infrastructure and incentives for adopting innovative healthcare technologies.

Key Players Shaping the Europe Wireless Healthcare Industry Market

- Motorola Solutions Inc

- Allscripts Healthcare Solutions Inc

- Verizon Communication Inc

- Samsung Electronics Co Ltd

- Cisco Systems Inc

- Philips Healthcare

- Extreme Networks Inc

- Apple Inc

- AT&T Inc

- Qualcomm Inc

Notable Milestones in Europe Wireless Healthcare Industry Sector

- June 2022: GE Healthcare introduced Portrait Mobile, a wireless patient monitoring system that is continuously monitoring a patient’s stay. The wireless patient monitoring system assists clinicians in detecting patient deterioration. Portrait Mobile comprises patient-worn wireless sensors that communicate with a mobile monitor.

- March 2022: Tunstall Healthcare, the United Kingdom-based provider of software solutions, services, and technology for telehealth and telecare, expanded its existence in the German market and service offering with the acquisition of BeWo Unternehmensgruppe (BeWo).

In-Depth Europe Wireless Healthcare Industry Market Outlook

The future outlook for the Europe Wireless Healthcare Industry is exceptionally promising, driven by a synergistic interplay of technological advancements, demographic shifts, and evolving healthcare paradigms. Growth accelerators such as the maturation of 5G infrastructure, the widespread adoption of AI for predictive diagnostics, and the increasing focus on personalized medicine will significantly expand market opportunities. Strategic partnerships between technology innovators and established healthcare providers are expected to foster the development of integrated, end-to-end solutions, enhancing patient care and operational efficiency. The growing demand for remote patient monitoring, driven by chronic disease management and the aging population, will continue to be a primary market engine. Continued investment in research and development, coupled with supportive regulatory frameworks, will ensure a dynamic and rapidly evolving market landscape.

Europe Wireless Healthcare Industry Segmentation

-

1. Component

- 1.1. Hardware

- 1.2. Software

- 1.3. Services

-

2. Application

- 2.1. Hospitals and Nursing Homes

- 2.2. Home Care

- 2.3. Pharmaceuticals

- 2.4. Other Applications

Europe Wireless Healthcare Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Wireless Healthcare Industry Regional Market Share

Geographic Coverage of Europe Wireless Healthcare Industry

Europe Wireless Healthcare Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 20.82% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Hardware

- 5.1.2. Software

- 5.1.3. Services

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Hospitals and Nursing Homes

- 5.2.2. Home Care

- 5.2.3. Pharmaceuticals

- 5.2.4. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. Europe Wireless Healthcare Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Component

- 6.1.1. Hardware

- 6.1.2. Software

- 6.1.3. Services

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Hospitals and Nursing Homes

- 6.2.2. Home Care

- 6.2.3. Pharmaceuticals

- 6.2.4. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Component

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Motorola Solutions Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Allscripts Healthcare Solutions Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Verizon Communication Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Samsung Electronics Co Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Cisco Systems Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Philips Healthcare

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Extreme Networks Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Apple Inc

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 AT&T Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Qualcomm Inc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Motorola Solutions Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Wireless Healthcare Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe Wireless Healthcare Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Wireless Healthcare Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 2: Europe Wireless Healthcare Industry Volume K Unit Forecast, by Component 2020 & 2033

- Table 3: Europe Wireless Healthcare Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 4: Europe Wireless Healthcare Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 5: Europe Wireless Healthcare Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Europe Wireless Healthcare Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: Europe Wireless Healthcare Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 8: Europe Wireless Healthcare Industry Volume K Unit Forecast, by Component 2020 & 2033

- Table 9: Europe Wireless Healthcare Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 10: Europe Wireless Healthcare Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 11: Europe Wireless Healthcare Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Europe Wireless Healthcare Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 13: United Kingdom Europe Wireless Healthcare Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: United Kingdom Europe Wireless Healthcare Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 15: Germany Europe Wireless Healthcare Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Germany Europe Wireless Healthcare Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 17: France Europe Wireless Healthcare Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: France Europe Wireless Healthcare Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Italy Europe Wireless Healthcare Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Italy Europe Wireless Healthcare Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 21: Spain Europe Wireless Healthcare Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Spain Europe Wireless Healthcare Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: Netherlands Europe Wireless Healthcare Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Netherlands Europe Wireless Healthcare Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 25: Belgium Europe Wireless Healthcare Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Belgium Europe Wireless Healthcare Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 27: Sweden Europe Wireless Healthcare Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Sweden Europe Wireless Healthcare Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 29: Norway Europe Wireless Healthcare Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Norway Europe Wireless Healthcare Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 31: Poland Europe Wireless Healthcare Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Poland Europe Wireless Healthcare Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: Denmark Europe Wireless Healthcare Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Denmark Europe Wireless Healthcare Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Wireless Healthcare Industry?

The projected CAGR is approximately 20.82%.

2. Which companies are prominent players in the Europe Wireless Healthcare Industry?

Key companies in the market include Motorola Solutions Inc, Allscripts Healthcare Solutions Inc , Verizon Communication Inc, Samsung Electronics Co Ltd, Cisco Systems Inc, Philips Healthcare, Extreme Networks Inc, Apple Inc, AT&T Inc, Qualcomm Inc.

3. What are the main segments of the Europe Wireless Healthcare Industry?

The market segments include Component, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 32.40 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Adoption of Connected Devices in Healthcare; Increasing Adoption of Internet of Things (IoT) and Wearable Devices in Healthcare to Drive the Wireless Healthcare Market.

6. What are the notable trends driving market growth?

Home Care is Expected to Gain Significant Share.

7. Are there any restraints impacting market growth?

Lack of Networking Infrastructure; Data Security and Device Certification Challenges; Impact of COVID-19 on the Industry.

8. Can you provide examples of recent developments in the market?

June 2022: GE Healthcare introduced Portrait Mobile, a wireless patient monitoring system that is continuously monitoring a patient’s stay. The wireless patient monitoring system assists clinicians in detecting patient deterioration. Portrait Mobile comprises patient-worn wireless sensors that communicate with a mobile monitor.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Wireless Healthcare Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Wireless Healthcare Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Wireless Healthcare Industry?

To stay informed about further developments, trends, and reports in the Europe Wireless Healthcare Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence