Key Insights

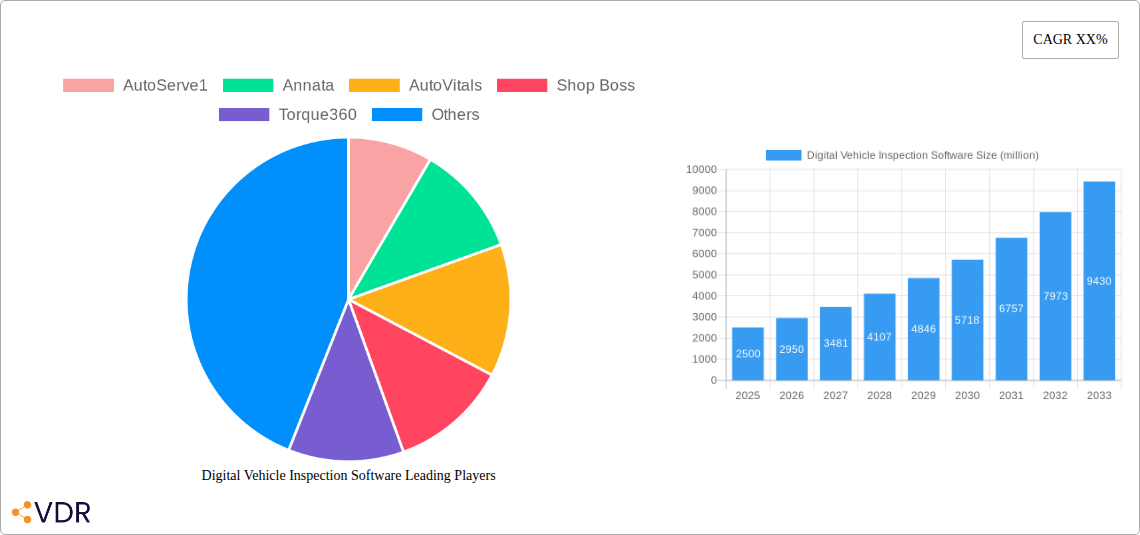

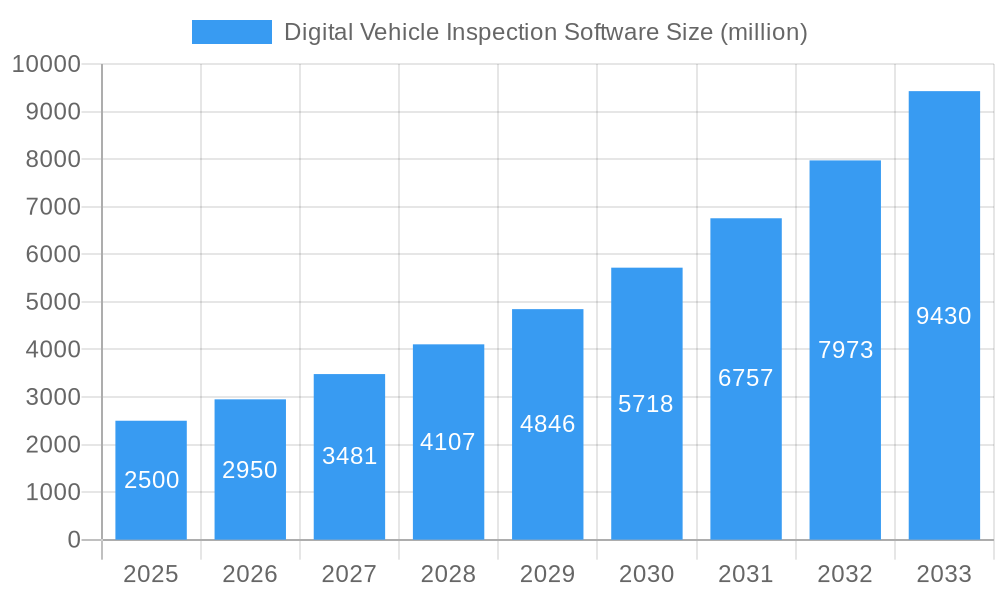

The Digital Vehicle Inspection Software market is poised for significant expansion, projected to reach a valuation of approximately USD 2,500 million by 2025 and witness a Compound Annual Growth Rate (CAGR) of around 18% from 2025 to 2033. This robust growth is primarily fueled by the increasing adoption of digital solutions across the automotive aftermarket and dealership sectors. The demand for enhanced efficiency, accuracy, and customer transparency in vehicle inspections is a key driver. Auto repair and reconditioning businesses, vehicle dealerships, and fleet management operations are actively seeking software that streamlines the inspection process, reduces errors, and improves communication with customers. The ability of these platforms to generate detailed detection data records, facilitate real-time tracking, and produce comprehensive DIV reports directly contributes to improved operational workflows and customer satisfaction. Furthermore, the growing emphasis on vehicle maintenance and safety standards globally further bolsters the market's upward trajectory.

Digital Vehicle Inspection Software Market Size (In Billion)

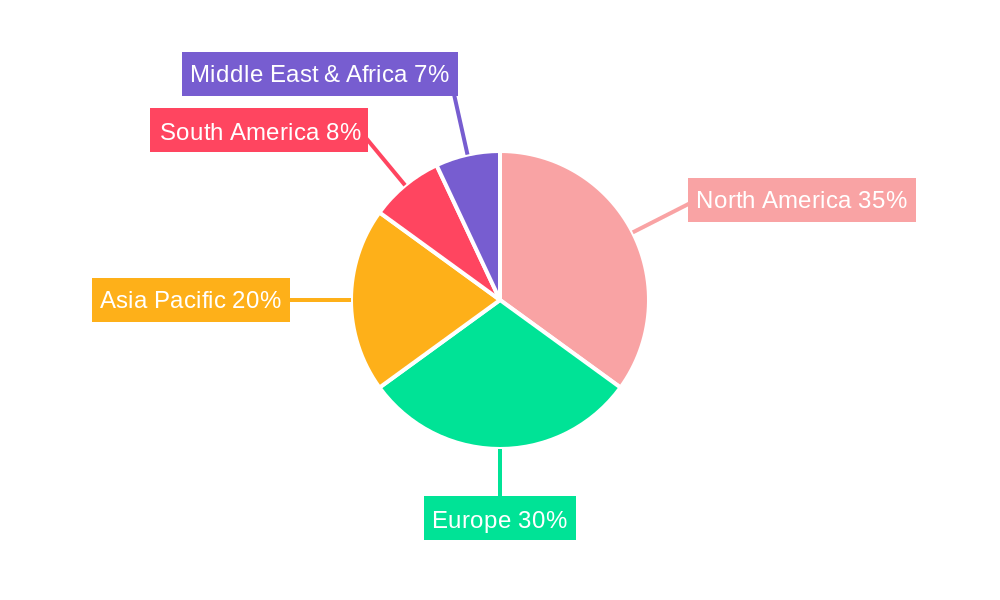

The market is characterized by intense competition and innovation, with numerous companies offering diverse solutions tailored to specific industry needs. Trends such as the integration of AI and machine learning for advanced defect detection, mobile-first inspection capabilities, and seamless integration with existing dealership management systems (DMS) are shaping the competitive landscape. While the market presents substantial opportunities, certain restraints exist, including the initial cost of software implementation, resistance to adopting new technologies within some segments of the automotive industry, and concerns regarding data security and privacy. However, the long-term benefits of enhanced operational efficiency, cost savings through reduced paperwork, and improved customer trust are expected to outweigh these challenges, driving sustained market growth throughout the forecast period. The Asia Pacific region, with its rapidly expanding automotive sector and increasing technological adoption, is anticipated to emerge as a significant growth market, alongside the established dominance of North America and Europe.

Digital Vehicle Inspection Software Company Market Share

Digital Vehicle Inspection Software Market Dynamics & Structure

The digital vehicle inspection software market is characterized by a moderately concentrated landscape, with key players like AutoServe1, Annata, AutoVitals, and AutoLeap establishing significant footholds. Technological innovation remains the primary driver, fueled by advancements in AI, cloud computing, and mobile accessibility, enabling real-time data capture and analysis. Regulatory frameworks are gradually evolving to embrace digital documentation, though standardization remains a challenge. Competitive product substitutes include traditional paper-based inspection methods and less sophisticated digital tools, but the efficiency and accuracy of comprehensive DIV solutions are increasingly outmaneuvering them. End-user demographics are diverse, encompassing auto repair shops, dealerships, fleet managers, and car rental agencies, each with specific integration needs and adoption timelines. Mergers and acquisitions (M&A) are becoming a strategic tool for consolidation and expanding service offerings, with an estimated 15-20 M&A deals occurring annually during the historical period, indicating a growing trend towards industry consolidation.

- Market Concentration: Moderately concentrated with a few dominant players.

- Technological Innovation Drivers: AI-powered diagnostics, cloud integration, mobile-first solutions, predictive maintenance capabilities.

- Regulatory Frameworks: Evolving, with a push towards digital compliance and data security standards.

- Competitive Product Substitutes: Traditional paper forms, basic digital checklists, manual inspection processes.

- End-User Demographics: Auto Repairing and Reconditioning Businesses, Vehicle Dealerships, Fleet Management, Car Rental Companies.

- M&A Trends: Increasing consolidation to gain market share and enhance product portfolios.

Digital Vehicle Inspection Software Growth Trends & Insights

The digital vehicle inspection software market is poised for significant expansion, projected to grow from an estimated $1.2 billion in 2025 to $3.5 billion by 2033, exhibiting a robust Compound Annual Growth Rate (CAGR) of approximately 14.5% during the forecast period. This surge is primarily attributed to the increasing demand for enhanced operational efficiency, improved customer transparency, and the imperative to streamline maintenance and repair processes across various automotive segments. The adoption rate of DIV software has steadily climbed, moving from a niche solution to a critical operational tool, particularly within the Auto Repairing and Reconditioning Businesses and Vehicle Dealerships segments, where it is estimated that over 60% of these businesses will have implemented some form of digital inspection by 2027.

Technological disruptions are continually reshaping the market. The integration of Artificial Intelligence (AI) for automated defect detection, image recognition for damage assessment, and predictive analytics for maintenance scheduling is significantly enhancing the capabilities of DIV solutions. This is leading to a shift from basic data recording to more sophisticated real-time tracking and advanced DIV report generation, providing actionable insights rather than just static documentation. Consumer behavior is also evolving, with a growing expectation for transparent and digital communication regarding vehicle health and repair needs. Customers increasingly value the ability to review digital inspection reports with visual evidence, fostering trust and informed decision-making.

The COVID-19 pandemic accelerated digital transformation across industries, and the automotive sector was no exception. Businesses recognized the importance of contactless service options and efficient digital workflows, further bolstering the adoption of DIV software. The rising complexity of modern vehicles, with their integrated electronic systems and advanced safety features, necessitates more sophisticated inspection tools that can accurately diagnose potential issues. The increasing emphasis on vehicle longevity and preventative maintenance also plays a crucial role, as DIV software empowers service providers to identify and address minor issues before they escalate into costly repairs.

Fleet management companies are increasingly leveraging DIV software to monitor the health of their vehicle fleets, optimize maintenance schedules, and reduce downtime, contributing to significant cost savings. Car rental companies are also adopting these solutions to ensure vehicle readiness and streamline the check-in/check-out process, enhancing customer experience and operational efficiency. The shift from one-time inspections to continuous monitoring and data analysis is a key trend, enabling proactive rather than reactive maintenance strategies. The ongoing development of integrated platforms that connect DIV software with other dealership management systems (DMS) or fleet management software (FMS) is also driving market growth by offering a more holistic view of vehicle operations and maintenance.

Dominant Regions, Countries, or Segments in Digital Vehicle Inspection Software

North America currently stands as the dominant region in the digital vehicle inspection software market, driven by its advanced automotive ecosystem, high adoption rates of technology, and a strong emphasis on operational efficiency. Within North America, the United States, representing an estimated 70% of the regional market share, leads in DIV software adoption due to the large number of auto repair businesses, vehicle dealerships, and extensive fleet operations. The regulatory environment in the U.S. is also conducive to the implementation of digital solutions, with a growing focus on data security and compliance. Economic policies that encourage business modernization and investment in technology further bolster this dominance. Infrastructure, including widespread internet access and advanced mobile penetration, supports the seamless deployment and utilization of cloud-based DIV solutions.

The Application segment of Auto Repairing and Reconditioning Businesses is a primary growth engine, accounting for an estimated 45% of the global market in 2025. These businesses are actively seeking to improve customer experience through transparent digital reports, streamline workflow for technicians, and reduce administrative overhead. Vehicle Dealerships follow closely, with an estimated 30% market share, utilizing DIV software for pre-sale inspections, trade-in assessments, and service department efficiency. The Fleet Management segment, estimated at 20% market share, is rapidly expanding as companies prioritize cost savings, uptime, and safety through continuous vehicle health monitoring. Car Rental Companies, while a smaller segment at approximately 5%, are increasingly adopting DIV for efficient vehicle turnarounds and damage assessment.

The Type segment of DIV Report Generation is currently the most mature and widely adopted, indicating a strong preference for comprehensive, visually rich inspection reports. However, Detection Real-time Tracking is experiencing the fastest growth, driven by the need for immediate insights into vehicle condition during inspections and by fleets. Detection Data Record, while foundational, is being integrated into more advanced solutions.

Key drivers for dominance in these regions and segments include:

- Technological Readiness: High consumer and business adoption of smartphones, tablets, and cloud services.

- Economic Factors: Strong automotive aftermarket industry, high disposable incomes, and a focus on vehicle maintenance and longevity.

- Regulatory Support: Evolving standards for digital documentation and data privacy that favor digital solutions.

- Competitive Landscape: Presence of established automotive service providers and tech companies driving innovation.

Emerging markets in Europe and Asia-Pacific are also showing significant growth potential, fueled by increasing vehicle ownership, a growing automotive service sector, and government initiatives promoting digitalization. As these markets mature, they are expected to contribute substantially to the global DIV software market.

Digital Vehicle Inspection Software Product Landscape

The digital vehicle inspection software market is witnessing a rapid evolution in product innovation, moving beyond basic checklists to offer comprehensive, AI-driven diagnostic tools. Leading solutions now integrate high-resolution image and video capture, allowing technicians to document vehicle conditions with unparalleled detail. Performance metrics are increasingly focused on diagnostic accuracy, speed of inspection, and ease of use for technicians, with advanced platforms achieving over 95% accuracy in initial defect identification. Unique selling propositions often revolve around seamless integration with existing Dealer Management Systems (DMS) and Fleet Management Software (FMS), offering end-to-end workflow automation. Technological advancements include predictive analytics for maintenance needs, real-time communication features for customer engagement, and the ability to generate professional, branded inspection reports in multiple languages, enhancing global market appeal.

Key Drivers, Barriers & Challenges in Digital Vehicle Inspection Software

Key Drivers:

- Enhanced Operational Efficiency: Streamlining inspection processes, reducing paperwork, and improving technician productivity are major catalysts.

- Improved Customer Transparency and Trust: Digital reports with visual evidence foster confidence and informed decision-making for vehicle owners.

- Cost Reduction: Minimizing errors, preventing unnecessary repairs, and optimizing maintenance schedules lead to significant cost savings for businesses.

- Technological Advancements: AI, cloud computing, and mobile technology enable more accurate, real-time data capture and analysis.

- Regulatory Compliance: The shift towards digital record-keeping and data security standards favors sophisticated DIV solutions.

Key Barriers & Challenges:

- Initial Investment Costs: The upfront cost of software, hardware, and training can be a deterrent for smaller businesses.

- Resistance to Change: Overcoming ingrained paper-based habits and ensuring technician buy-in requires effective change management strategies.

- Data Security and Privacy Concerns: Protecting sensitive vehicle and customer data from cyber threats is paramount and requires robust security measures.

- Integration Complexities: Integrating DIV software with diverse existing systems (e.g., DMS, FMS) can be challenging and time-consuming.

- Standardization Issues: Lack of universal standards for digital inspection data can hinder interoperability between different platforms and stakeholders. The global market is estimated to face a potential 5-8% slowdown in adoption due to these integration hurdles.

Emerging Opportunities in Digital Vehicle Inspection Software

Emerging opportunities in the digital vehicle inspection software sector lie in the expansion of AI-powered diagnostic capabilities, particularly in identifying subtle or intermittent issues that traditional methods might miss. The growing demand for contactless vehicle services presents a significant opportunity for remote inspection features and digital pre-purchase inspections. Furthermore, the untapped potential in developing countries with rapidly expanding automotive markets offers substantial room for growth. Innovative applications in the used car market for enhanced quality assurance and the integration with smart city initiatives for vehicle data management are also promising avenues.

Growth Accelerators in the Digital Vehicle Inspection Software Industry

Long-term growth in the digital vehicle inspection software industry will be significantly accelerated by breakthroughs in predictive maintenance algorithms, enabling businesses to forecast component failures with high accuracy. Strategic partnerships between software providers and original equipment manufacturers (OEMs) will foster deeper integration and data-sharing, leading to more comprehensive insights. Market expansion strategies targeting underpenetrated regions and segments, coupled with the development of more intuitive and user-friendly interfaces, will further drive adoption. The continuous refinement of AI and machine learning models to interpret complex diagnostic data will be a pivotal growth accelerator, pushing the boundaries of what is possible in vehicle health assessment.

Key Players Shaping the Digital Vehicle Inspection Software Market

- AutoServe1

- Annata

- AutoVitals

- Shop Boss

- Torque360

- AutoLeap

- Ravin AI

- Repair Shop Solutions

- 5iQ

- Fleetio

- Omnique

- Autoflow

- Shop-Ware

- GEM-CHECK

- Branch Automotive

- The Auto Station

- Kerridge Commercial Systems

- TÜV SÜD

- COSTAR

Notable Milestones in Digital Vehicle Inspection Software Sector

- 2020 October: AutoVitals launches enhanced AI-driven inspection features.

- 2021 April: AutoLeap secures Series A funding, signaling strong investor confidence.

- 2021 November: Ravin AI pioneers AI-powered visual inspection technology for automotive.

- 2022 February: Fleetio acquires a competitor, expanding its fleet management solutions.

- 2022 August: AutoServe1 introduces advanced integration capabilities with major DMS providers.

- 2023 January: TÜV SÜD partners with a leading software provider to offer digital inspection services.

- 2023 July: Shop-Ware enhances its mobile application for improved technician user experience.

- 2024 March: Annata expands its cloud-based platform to include real-time vehicle tracking.

- 2024 September: Repair Shop Solutions integrates telematics data into its DIV reporting.

- 2025 February: COSTAR develops predictive maintenance modules for fleet management.

In-Depth Digital Vehicle Inspection Software Market Outlook

The future outlook for the digital vehicle inspection software market is exceptionally bright, driven by a confluence of technological advancements and evolving industry demands. Growth accelerators such as the widespread adoption of AI for predictive analytics and anomaly detection will empower businesses to move beyond reactive repairs to proactive maintenance strategies. Strategic alliances between DIV software providers, OEMs, and telematics companies will create integrated ecosystems, offering unparalleled data insights. The increasing global focus on sustainability and extending vehicle lifespan further fuels the demand for efficient inspection and maintenance solutions. The market is anticipated to continue its upward trajectory, offering substantial opportunities for innovation and expansion as businesses across the automotive spectrum prioritize digital transformation for competitive advantage.

Digital Vehicle Inspection Software Segmentation

-

1. Application

- 1.1. Auto Repairing and Reconditioning Businesses

- 1.2. Vehicle Dealerships

- 1.3. Fleet Management

- 1.4. Car Rental Companies

- 1.5. Other

-

2. Types

- 2.1. Detection Data Record

- 2.2. Detection Real-time Tracking

- 2.3. DIV Report Generation

Digital Vehicle Inspection Software Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Digital Vehicle Inspection Software Regional Market Share

Geographic Coverage of Digital Vehicle Inspection Software

Digital Vehicle Inspection Software REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Digital Vehicle Inspection Software Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Auto Repairing and Reconditioning Businesses

- 5.1.2. Vehicle Dealerships

- 5.1.3. Fleet Management

- 5.1.4. Car Rental Companies

- 5.1.5. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Detection Data Record

- 5.2.2. Detection Real-time Tracking

- 5.2.3. DIV Report Generation

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Digital Vehicle Inspection Software Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Auto Repairing and Reconditioning Businesses

- 6.1.2. Vehicle Dealerships

- 6.1.3. Fleet Management

- 6.1.4. Car Rental Companies

- 6.1.5. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Detection Data Record

- 6.2.2. Detection Real-time Tracking

- 6.2.3. DIV Report Generation

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Digital Vehicle Inspection Software Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Auto Repairing and Reconditioning Businesses

- 7.1.2. Vehicle Dealerships

- 7.1.3. Fleet Management

- 7.1.4. Car Rental Companies

- 7.1.5. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Detection Data Record

- 7.2.2. Detection Real-time Tracking

- 7.2.3. DIV Report Generation

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Digital Vehicle Inspection Software Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Auto Repairing and Reconditioning Businesses

- 8.1.2. Vehicle Dealerships

- 8.1.3. Fleet Management

- 8.1.4. Car Rental Companies

- 8.1.5. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Detection Data Record

- 8.2.2. Detection Real-time Tracking

- 8.2.3. DIV Report Generation

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Digital Vehicle Inspection Software Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Auto Repairing and Reconditioning Businesses

- 9.1.2. Vehicle Dealerships

- 9.1.3. Fleet Management

- 9.1.4. Car Rental Companies

- 9.1.5. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Detection Data Record

- 9.2.2. Detection Real-time Tracking

- 9.2.3. DIV Report Generation

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Digital Vehicle Inspection Software Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Auto Repairing and Reconditioning Businesses

- 10.1.2. Vehicle Dealerships

- 10.1.3. Fleet Management

- 10.1.4. Car Rental Companies

- 10.1.5. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Detection Data Record

- 10.2.2. Detection Real-time Tracking

- 10.2.3. DIV Report Generation

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 AutoServe1

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Annata

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 AutoVitals

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Shop Boss

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Torque360

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 AutoLeap

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Ravin AI

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Repair Shop Solutions

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 5iQ

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Fleetio

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Omnique

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Autoflow

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Shop-Ware

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 GEM-CHECK

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Branch Automotive

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 The Auto Station

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Kerridge Commercial Systems

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 TÜV SÜD

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 COSTAR

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.1 AutoServe1

List of Figures

- Figure 1: Global Digital Vehicle Inspection Software Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Digital Vehicle Inspection Software Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Digital Vehicle Inspection Software Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Digital Vehicle Inspection Software Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Digital Vehicle Inspection Software Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Digital Vehicle Inspection Software Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Digital Vehicle Inspection Software Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Digital Vehicle Inspection Software Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Digital Vehicle Inspection Software Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Digital Vehicle Inspection Software Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Digital Vehicle Inspection Software Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Digital Vehicle Inspection Software Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Digital Vehicle Inspection Software Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Digital Vehicle Inspection Software Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Digital Vehicle Inspection Software Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Digital Vehicle Inspection Software Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Digital Vehicle Inspection Software Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Digital Vehicle Inspection Software Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Digital Vehicle Inspection Software Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Digital Vehicle Inspection Software Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Digital Vehicle Inspection Software Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Digital Vehicle Inspection Software Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Digital Vehicle Inspection Software Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Digital Vehicle Inspection Software Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Digital Vehicle Inspection Software Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Digital Vehicle Inspection Software Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Digital Vehicle Inspection Software Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Digital Vehicle Inspection Software Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Digital Vehicle Inspection Software Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Digital Vehicle Inspection Software Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Digital Vehicle Inspection Software Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Digital Vehicle Inspection Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Digital Vehicle Inspection Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Digital Vehicle Inspection Software Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Digital Vehicle Inspection Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Digital Vehicle Inspection Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Digital Vehicle Inspection Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Digital Vehicle Inspection Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Digital Vehicle Inspection Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Digital Vehicle Inspection Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Digital Vehicle Inspection Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Digital Vehicle Inspection Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Digital Vehicle Inspection Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Digital Vehicle Inspection Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Digital Vehicle Inspection Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Digital Vehicle Inspection Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Digital Vehicle Inspection Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Digital Vehicle Inspection Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Digital Vehicle Inspection Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Digital Vehicle Inspection Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Digital Vehicle Inspection Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Digital Vehicle Inspection Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Digital Vehicle Inspection Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Digital Vehicle Inspection Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Digital Vehicle Inspection Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Digital Vehicle Inspection Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Digital Vehicle Inspection Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Digital Vehicle Inspection Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Digital Vehicle Inspection Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Digital Vehicle Inspection Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Digital Vehicle Inspection Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Digital Vehicle Inspection Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Digital Vehicle Inspection Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Digital Vehicle Inspection Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Digital Vehicle Inspection Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Digital Vehicle Inspection Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Digital Vehicle Inspection Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Digital Vehicle Inspection Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Digital Vehicle Inspection Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Digital Vehicle Inspection Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Digital Vehicle Inspection Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Digital Vehicle Inspection Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Digital Vehicle Inspection Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Digital Vehicle Inspection Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Digital Vehicle Inspection Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Digital Vehicle Inspection Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Digital Vehicle Inspection Software Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Digital Vehicle Inspection Software?

The projected CAGR is approximately 7.5%.

2. Which companies are prominent players in the Digital Vehicle Inspection Software?

Key companies in the market include AutoServe1, Annata, AutoVitals, Shop Boss, Torque360, AutoLeap, Ravin AI, Repair Shop Solutions, 5iQ, Fleetio, Omnique, Autoflow, Shop-Ware, GEM-CHECK, Branch Automotive, The Auto Station, Kerridge Commercial Systems, TÜV SÜD, COSTAR.

3. What are the main segments of the Digital Vehicle Inspection Software?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Digital Vehicle Inspection Software," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Digital Vehicle Inspection Software report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Digital Vehicle Inspection Software?

To stay informed about further developments, trends, and reports in the Digital Vehicle Inspection Software, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence