Key Insights

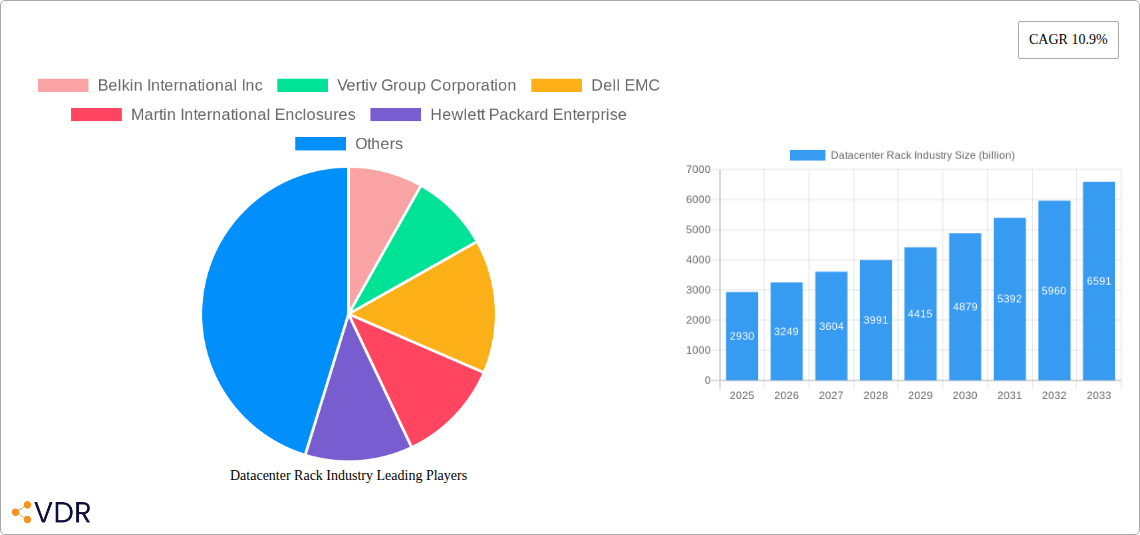

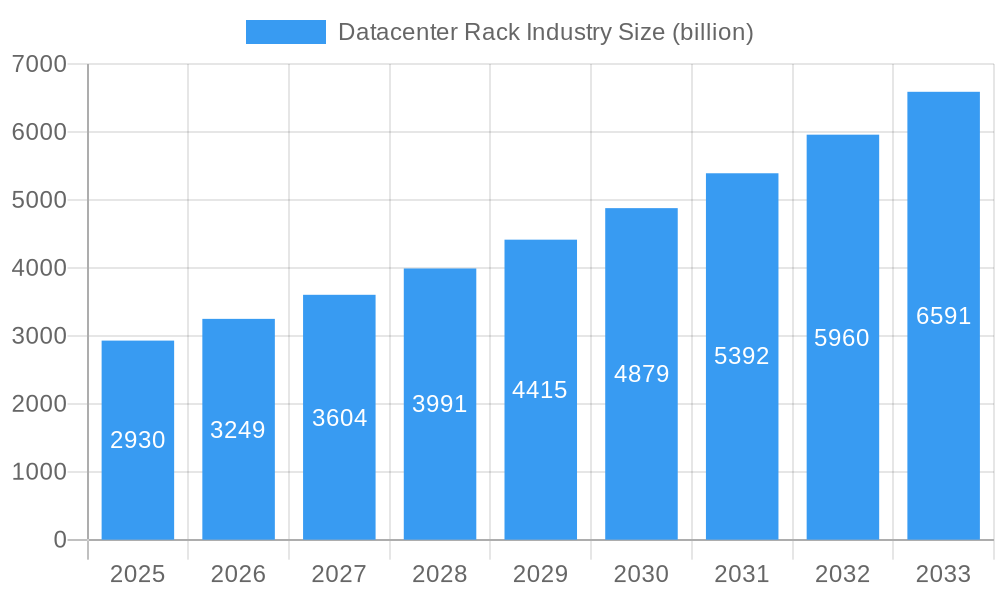

The global Datacenter Rack Industry is poised for significant expansion, with a projected market size of USD 2.93 billion in 2025. Driven by the relentless surge in data generation and consumption, the industry is expected to witness a robust Compound Annual Growth Rate (CAGR) of 10.9% during the forecast period of 2025-2033. This impressive growth is underpinned by several key factors, including the escalating demand for efficient and scalable IT infrastructure. The increasing adoption of cloud computing, the proliferation of IoT devices, and the continuous evolution of Big Data analytics are creating an insatiable need for advanced datacenter solutions. Furthermore, the trend towards edge computing, which necessitates smaller, distributed data processing hubs, also contributes to the demand for versatile and compact rack solutions. The industry is witnessing a strong emphasis on smart racks and integrated solutions that offer enhanced cooling, power management, and security features, reflecting a shift towards intelligent datacenter infrastructure.

Datacenter Rack Industry Market Size (In Billion)

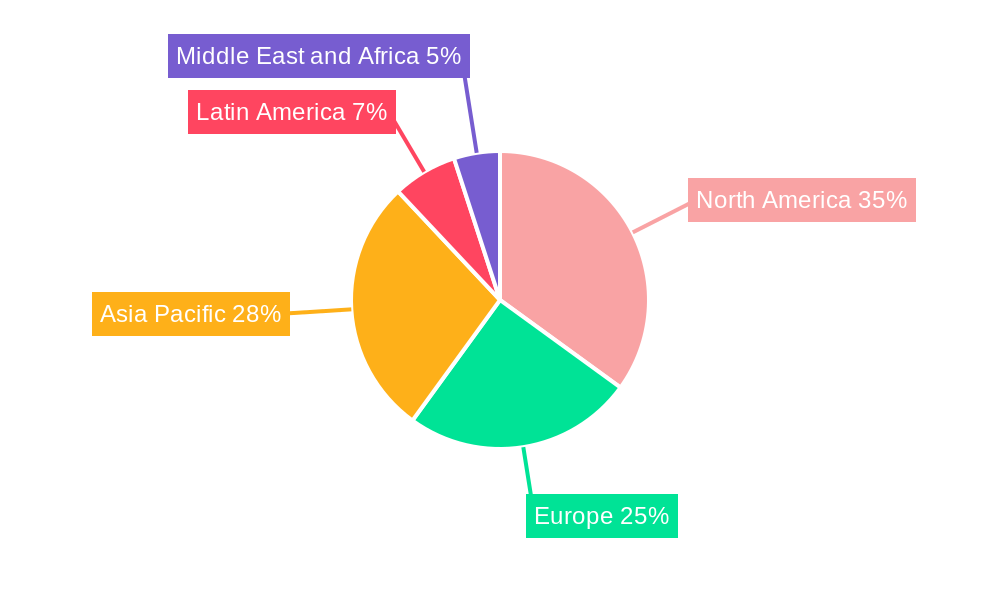

The market is segmented into various rack unit sizes – Small, Medium, and Large – catering to diverse deployment needs, from small enterprise setups to hyperscale data centers. Key end-user industries like BFSI, IT and Telecom, Manufacturing, and Retail are the primary consumers of datacenter racks, all of which are undergoing digital transformations that require substantial IT infrastructure. While the market exhibits strong growth drivers, certain restraints such as high initial investment costs for advanced datacenter facilities and potential supply chain disruptions could pose challenges. However, these are likely to be mitigated by technological advancements and strategic partnerships among key players, including established names like Vertiv Group Corporation, Schneider Electric SE, and Rittal GmbH & Co KG, alongside emerging innovators. Geographically, North America and Asia Pacific are anticipated to lead the market in terms of size and growth, fueled by substantial investments in digital infrastructure and cloud services.

Datacenter Rack Industry Company Market Share

Comprehensive Datacenter Rack Industry Report: Market Size, Trends, and Forecast (2019-2033)

Gain unparalleled insights into the dynamic Datacenter Rack Industry with this in-depth market research report. Covering a historical period from 2019-2024, a base and estimated year of 2025, and a robust forecast period from 2025-2033, this report provides a definitive analysis of market size, growth drivers, key players, and future opportunities. Explore the intricate parent and child market structures, crucial for understanding the competitive landscape and identifying high-growth segments within the global datacenter infrastructure. Leverage high-traffic SEO keywords to ensure maximum visibility and engagement within the IT and datacenter professional community.

Datacenter Rack Industry Market Dynamics & Structure

The global datacenter rack industry is characterized by a moderately consolidated market structure, driven by significant technological innovation and an increasing demand for high-density computing solutions. Key innovation drivers include advancements in power distribution, cooling technologies, and intelligent rack management systems, enabling more efficient and reliable datacenter operations. Regulatory frameworks, particularly those focused on energy efficiency and data security, are shaping product development and deployment strategies. Competitive product substitutes, such as modular data centers and pre-integrated infrastructure solutions, are emerging, pushing traditional rack manufacturers to innovate. End-user demographics are shifting towards industries requiring massive data processing and storage, influencing the types and sizes of racks in demand. Mergers and acquisitions (M&A) trends are active, as larger players seek to expand their product portfolios and market reach, consolidating the industry further.

- Market Concentration: Moderate, with key players holding substantial market share but with room for smaller, specialized vendors.

- Technological Innovation Drivers: High-density power, advanced cooling, intelligent rack monitoring, and cybersecurity integrations.

- Regulatory Frameworks: Energy efficiency standards (e.g., ASHRAE), data sovereignty laws, and environmental regulations.

- Competitive Product Substitutes: Modular data centers, pre-integrated IT solutions, and containerized data centers.

- End-User Demographics: Growing demand from BFSI, IT and Telecom, and Manufacturing sectors.

- M&A Trends: Strategic acquisitions to broaden product offerings and geographical presence.

Datacenter Rack Industry Growth Trends & Insights

The datacenter rack industry is poised for substantial growth, with an estimated market size reaching $XX billion in 2025 and projected to expand at a Compound Annual Growth Rate (CAGR) of XX% through 2033. This expansion is fueled by the relentless surge in data generation and consumption, necessitating more sophisticated and scalable datacenter infrastructure. Adoption rates of advanced rack solutions, including those with integrated cooling and power management, are accelerating as organizations prioritize operational efficiency and reduced energy footprints. Technological disruptions, such as the rise of edge computing and the increasing demand for AI and machine learning capabilities, are creating new market segments and driving demand for specialized rack configurations. Consumer behavior shifts, marked by a greater reliance on cloud services and digital platforms, are indirectly boosting the demand for underlying datacenter capacity. The market penetration of intelligent and modular rack solutions is expected to rise significantly as businesses seek greater agility and cost-effectiveness in their IT deployments.

Dominant Regions, Countries, or Segments in Datacenter Rack Industry

The IT and Telecom end-user industry stands as a primary driver of growth within the global datacenter rack market, projected to account for a significant market share exceeding XX% in 2025. This dominance is attributed to the industry's continuous need for expansion and upgrades to support cloud computing, 5G deployment, and the proliferation of digital services. North America is anticipated to be the leading region, driven by its mature IT infrastructure, substantial investments in hyperscale data centers, and a high concentration of technology companies. The United States, in particular, will spearhead this growth, fueled by robust economic policies that encourage technological advancement and significant private sector investment in data center development.

- Dominant End-User Industry: IT and Telecom (estimated XX% market share in 2025).

- Key Drivers: Cloud services expansion, 5G infrastructure build-out, digital transformation initiatives, and increasing demand for data analytics.

- Growth Potential: Continuous innovation in networking and computing necessitates frequent infrastructure upgrades and expansions.

- Dominant Region: North America (estimated XX% market share in 2025).

- Key Drivers: High concentration of hyperscale data centers, substantial private sector investment, favorable regulatory environment for tech innovation.

- Growth Potential: Ongoing expansion of colocation facilities and enterprise data centers.

- Dominant Country: United States.

- Key Drivers: Leading technology companies, significant R&D investment, and government support for digital infrastructure.

- Growth Potential: Greenfield data center projects and expansion of existing facilities.

- Dominant Rack Unit Segment: Large rack units will continue to lead demand, driven by hyperscale and enterprise data centers requiring high-density solutions to house substantial server and networking equipment.

Datacenter Rack Industry Product Landscape

The datacenter rack industry is witnessing a surge in product innovations focused on enhanced cooling, power management, and increased density. Manufacturers are developing advanced rack enclosures with integrated liquid cooling solutions, intelligent power distribution units (PDUs) offering granular monitoring, and modular designs for flexible deployment. These innovations are crucial for supporting high-performance computing (HPC), AI workloads, and edge computing applications, which generate significant heat and require robust power infrastructure. Unique selling propositions revolve around improved energy efficiency, reduced operational costs, and enhanced reliability, catering to the growing demand for sustainable and high-performing data center environments.

Key Drivers, Barriers & Challenges in Datacenter Rack Industry

Key Drivers: The datacenter rack industry is propelled by the exponential growth of data, the proliferation of cloud computing, and the increasing adoption of AI and IoT technologies. Advancements in server density and processing power necessitate more sophisticated rack solutions. Government initiatives supporting digitalization and digital infrastructure development also act as significant catalysts.

- Data Growth: Ever-increasing data volumes require expanded and efficient storage and processing capabilities.

- Cloud Computing Adoption: The shift to cloud services fuels the demand for hyperscale and colocation data centers.

- AI & IoT: These technologies drive the need for high-performance computing and dense rack deployments.

- Digitalization Initiatives: Government and corporate focus on digital transformation boosts data center investments.

Barriers & Challenges: Supply chain disruptions, rising raw material costs, and the complexity of integrating advanced cooling and power technologies pose significant challenges. Stringent environmental regulations and the high initial investment required for state-of-the-art rack solutions can also act as barriers to adoption, particularly for smaller enterprises. Intense competition and the need for continuous innovation to keep pace with rapidly evolving technology trends further complicate the market landscape.

- Supply Chain Volatility: Disruptions in global supply chains can lead to delays and increased costs.

- Raw Material Costs: Fluctuations in prices of metals and other components impact manufacturing expenses.

- Integration Complexity: Implementing advanced cooling and power solutions requires specialized expertise.

- Environmental Regulations: Compliance with evolving energy efficiency and sustainability standards can be challenging and costly.

- High Initial Investment: Advanced rack solutions often require significant upfront capital expenditure.

- Intense Competition: A crowded market necessitates constant innovation and competitive pricing.

Emerging Opportunities in Datacenter Rack Industry

Emerging opportunities lie in the rapidly expanding edge computing sector, requiring specialized, compact, and ruggedized rack solutions for distributed deployments. The growing demand for sustainable data centers presents a significant opportunity for manufacturers offering energy-efficient racks with advanced cooling and power management features. Furthermore, the increasing adoption of AI and machine learning workloads is driving the need for high-density racks capable of supporting power-hungry GPUs and specialized server architectures. The "as-a-service" model for data center infrastructure is also gaining traction, creating opportunities for providers of modular and scalable rack solutions that can be deployed and managed remotely.

Growth Accelerators in the Datacenter Rack Industry Industry

Key growth accelerators for the datacenter rack industry include the continued global expansion of hyperscale data centers, driven by major cloud service providers. Strategic partnerships between rack manufacturers, IT hardware vendors, and colocation providers are crucial for developing integrated solutions and expanding market reach. The ongoing digital transformation across various industries, from BFSI to manufacturing, is a constant source of demand for new and upgraded data center capacity. Furthermore, the increasing focus on energy efficiency and sustainability is spurring innovation in rack design and cooling technologies, creating new market opportunities.

Key Players Shaping the Datacenter Rack Industry Market

- Belkin International Inc

- Vertiv Group Corporation

- Dell EMC

- Martin International Enclosures

- Hewlett Packard Enterprise

- Schneider Electric SE

- Rittal GmbH & Co KG

- Legrand SA

- Black Box Corporation

- Kendall Howard LLC

- Oracle Corporation

- Fujitsu Corporation

Notable Milestones in Datacenter Rack Industry Sector

- October 2022: NetRack launched iRack Block, designed to cater to large requirements, representing a step towards intelligent infra capsules or modular data centers with self-cooking, self-powered, and self-contained capabilities.

- June 2022: Schneider Electric, in partnership with Stratus Technologies and Avnet Integrated, announced advancements aimed at delivering streamlined, zero-touch edge computing, enabling the next wave of industrial innovation.

In-Depth Datacenter Rack Industry Market Outlook

The datacenter rack industry is set for robust growth, driven by the insatiable demand for data processing and storage. Future market potential is significantly amplified by the ongoing expansion of edge computing infrastructure, requiring specialized and resilient rack solutions. Strategic opportunities abound for manufacturers who can offer innovative, energy-efficient designs that align with global sustainability goals. The increasing complexity of AI and HPC workloads will continue to push the boundaries of rack density and thermal management, creating avenues for technological leadership and market expansion. The shift towards modular and scalable datacenter designs will also favor vendors offering flexible and easily deployable rack systems.

Datacenter Rack Industry Segmentation

-

1. Rack Units

- 1.1. Small

- 1.2. Medium

- 1.3. Large

-

2. End-user Industry

- 2.1. BFSI

- 2.2. IT and Telecom

- 2.3. Manufacturing

- 2.4. Retail

- 2.5. Other End-user Industries

Datacenter Rack Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Datacenter Rack Industry Regional Market Share

Geographic Coverage of Datacenter Rack Industry

Datacenter Rack Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Rack Units

- 5.1.1. Small

- 5.1.2. Medium

- 5.1.3. Large

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. BFSI

- 5.2.2. IT and Telecom

- 5.2.3. Manufacturing

- 5.2.4. Retail

- 5.2.5. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Rack Units

- 6. Global Datacenter Rack Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Rack Units

- 6.1.1. Small

- 6.1.2. Medium

- 6.1.3. Large

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. BFSI

- 6.2.2. IT and Telecom

- 6.2.3. Manufacturing

- 6.2.4. Retail

- 6.2.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Rack Units

- 7. North America Datacenter Rack Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Rack Units

- 7.1.1. Small

- 7.1.2. Medium

- 7.1.3. Large

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. BFSI

- 7.2.2. IT and Telecom

- 7.2.3. Manufacturing

- 7.2.4. Retail

- 7.2.5. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Rack Units

- 8. Europe Datacenter Rack Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Rack Units

- 8.1.1. Small

- 8.1.2. Medium

- 8.1.3. Large

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. BFSI

- 8.2.2. IT and Telecom

- 8.2.3. Manufacturing

- 8.2.4. Retail

- 8.2.5. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Rack Units

- 9. Asia Pacific Datacenter Rack Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Rack Units

- 9.1.1. Small

- 9.1.2. Medium

- 9.1.3. Large

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. BFSI

- 9.2.2. IT and Telecom

- 9.2.3. Manufacturing

- 9.2.4. Retail

- 9.2.5. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Rack Units

- 10. Latin America Datacenter Rack Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Rack Units

- 10.1.1. Small

- 10.1.2. Medium

- 10.1.3. Large

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. BFSI

- 10.2.2. IT and Telecom

- 10.2.3. Manufacturing

- 10.2.4. Retail

- 10.2.5. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Rack Units

- 11. Middle East and Africa Datacenter Rack Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Rack Units

- 11.1.1. Small

- 11.1.2. Medium

- 11.1.3. Large

- 11.2. Market Analysis, Insights and Forecast - by End-user Industry

- 11.2.1. BFSI

- 11.2.2. IT and Telecom

- 11.2.3. Manufacturing

- 11.2.4. Retail

- 11.2.5. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Rack Units

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Belkin International Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Vertiv Group Corporation

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Dell EMC

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Martin International Enclosures

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Hewlett Packard Enterprise

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Schneider Electric SE

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Rittal GmbH & Co KG

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Legrand SA*List Not Exhaustive

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Black Box Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Kendall Howard LLC

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Oracle Corporation

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Fujitsu Corporation

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Belkin International Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Datacenter Rack Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Datacenter Rack Industry Revenue (billion), by Rack Units 2025 & 2033

- Figure 3: North America Datacenter Rack Industry Revenue Share (%), by Rack Units 2025 & 2033

- Figure 4: North America Datacenter Rack Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 5: North America Datacenter Rack Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 6: North America Datacenter Rack Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Datacenter Rack Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Datacenter Rack Industry Revenue (billion), by Rack Units 2025 & 2033

- Figure 9: Europe Datacenter Rack Industry Revenue Share (%), by Rack Units 2025 & 2033

- Figure 10: Europe Datacenter Rack Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 11: Europe Datacenter Rack Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 12: Europe Datacenter Rack Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Datacenter Rack Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Datacenter Rack Industry Revenue (billion), by Rack Units 2025 & 2033

- Figure 15: Asia Pacific Datacenter Rack Industry Revenue Share (%), by Rack Units 2025 & 2033

- Figure 16: Asia Pacific Datacenter Rack Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 17: Asia Pacific Datacenter Rack Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 18: Asia Pacific Datacenter Rack Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific Datacenter Rack Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America Datacenter Rack Industry Revenue (billion), by Rack Units 2025 & 2033

- Figure 21: Latin America Datacenter Rack Industry Revenue Share (%), by Rack Units 2025 & 2033

- Figure 22: Latin America Datacenter Rack Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 23: Latin America Datacenter Rack Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: Latin America Datacenter Rack Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Latin America Datacenter Rack Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Datacenter Rack Industry Revenue (billion), by Rack Units 2025 & 2033

- Figure 27: Middle East and Africa Datacenter Rack Industry Revenue Share (%), by Rack Units 2025 & 2033

- Figure 28: Middle East and Africa Datacenter Rack Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 29: Middle East and Africa Datacenter Rack Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 30: Middle East and Africa Datacenter Rack Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Middle East and Africa Datacenter Rack Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Datacenter Rack Industry Revenue billion Forecast, by Rack Units 2020 & 2033

- Table 2: Global Datacenter Rack Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 3: Global Datacenter Rack Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Datacenter Rack Industry Revenue billion Forecast, by Rack Units 2020 & 2033

- Table 5: Global Datacenter Rack Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 6: Global Datacenter Rack Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Datacenter Rack Industry Revenue billion Forecast, by Rack Units 2020 & 2033

- Table 8: Global Datacenter Rack Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 9: Global Datacenter Rack Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Global Datacenter Rack Industry Revenue billion Forecast, by Rack Units 2020 & 2033

- Table 11: Global Datacenter Rack Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 12: Global Datacenter Rack Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global Datacenter Rack Industry Revenue billion Forecast, by Rack Units 2020 & 2033

- Table 14: Global Datacenter Rack Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 15: Global Datacenter Rack Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global Datacenter Rack Industry Revenue billion Forecast, by Rack Units 2020 & 2033

- Table 17: Global Datacenter Rack Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 18: Global Datacenter Rack Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Datacenter Rack Industry?

The projected CAGR is approximately 10.9%.

2. Which companies are prominent players in the Datacenter Rack Industry?

Key companies in the market include Belkin International Inc, Vertiv Group Corporation, Dell EMC, Martin International Enclosures, Hewlett Packard Enterprise, Schneider Electric SE, Rittal GmbH & Co KG, Legrand SA*List Not Exhaustive, Black Box Corporation, Kendall Howard LLC, Oracle Corporation, Fujitsu Corporation.

3. What are the main segments of the Datacenter Rack Industry?

The market segments include Rack Units, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.93 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Deployment of Data Center Facilities; Growing Cloud Computing Adoption Leading to Investment in Hyperscale Data Centers; BFSI Sector Expected to Hold a Significant Share.

6. What are the notable trends driving market growth?

BFSI Sector Expected to Hold a Significant Share.

7. Are there any restraints impacting market growth?

Increasing Utilization of Blade Servers.

8. Can you provide examples of recent developments in the market?

October 2022 - In contrast to the smaller installations provided by the iRack solution, NetRack created iRack Block to cater to large requirements primarily. The rack is a step toward intelligent infra capsules or modular data centers because it includes self-cooking, self-powered, and self-contained capabilities.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Datacenter Rack Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Datacenter Rack Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Datacenter Rack Industry?

To stay informed about further developments, trends, and reports in the Datacenter Rack Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence