Key Insights

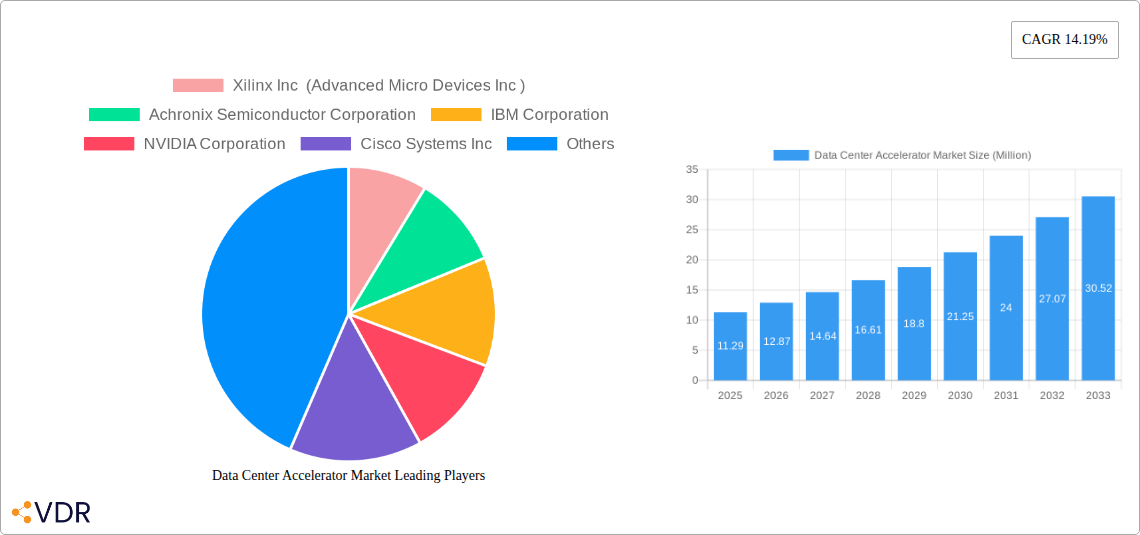

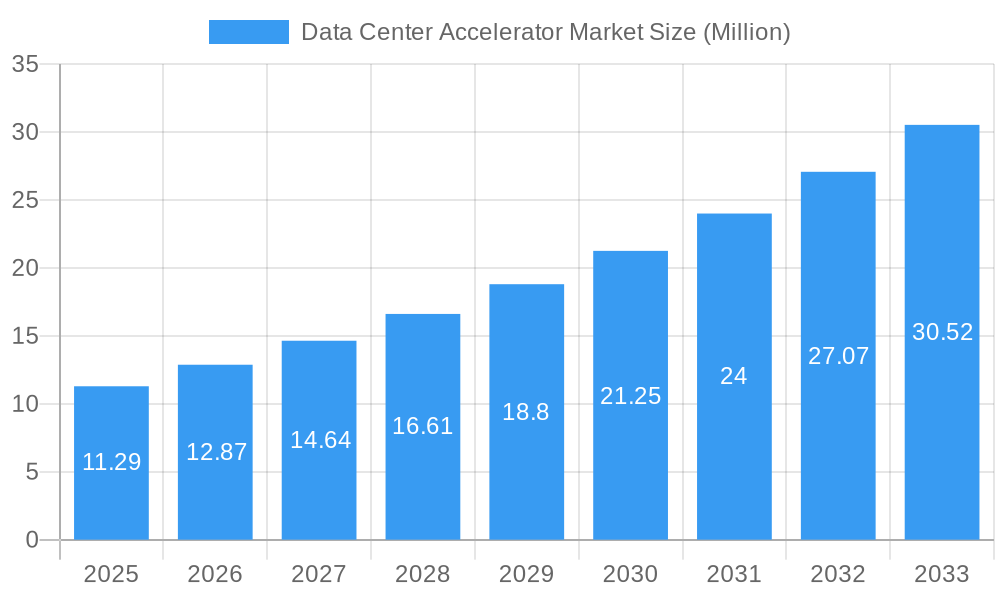

The Data Center Accelerator Market is poised for remarkable expansion, currently valued at approximately USD 11.29 billion. This growth is fueled by an impressive compound annual growth rate (CAGR) of 14.19%, projecting significant market evolution through 2033. The insatiable demand for enhanced processing power in modern data centers, driven by the exponential rise of big data analytics, artificial intelligence (AI), and high-performance computing (HPC), forms the bedrock of this robust market trajectory. As businesses increasingly rely on real-time insights and complex simulations, the need for specialized hardware solutions that accelerate these demanding workloads becomes paramount. This surge in demand necessitates advanced processing units, with Graphics Processing Units (GPUs) and Application-Specific Integrated Circuits (ASICs) emerging as frontrunners due to their superior parallel processing capabilities. Field-Programmable Gate Arrays (FPGAs) also play a crucial role in offering customizable acceleration for specific tasks.

Data Center Accelerator Market Market Size (In Million)

The market's upward momentum is further propelled by ongoing technological innovations and strategic collaborations among key industry players like NVIDIA, Intel, AMD, and Xilinx. These companies are continuously developing more powerful and energy-efficient accelerators, pushing the boundaries of computational performance. However, challenges such as the high initial investment costs for these advanced technologies and the ongoing need for specialized talent to manage and optimize them could present some restraints. Despite these hurdles, the overwhelming benefits of accelerated data processing, including reduced latency, improved efficiency, and the ability to handle more complex computational problems, are expected to drive sustained adoption across diverse applications, from cloud computing infrastructure to sophisticated scientific research. The Asia Pacific region is anticipated to witness particularly strong growth due to increasing digitalization and a burgeoning tech ecosystem.

Data Center Accelerator Market Company Market Share

This in-depth report provides a comprehensive analysis of the global Data Center Accelerator Market, dissecting its intricate dynamics, growth trajectories, and future potential. Driven by the insatiable demand for faster processing, reduced latency, and enhanced energy efficiency in data-intensive workloads, the market is poised for significant expansion. Explore parent and child market segments, identifying key drivers, emerging opportunities, and the strategic landscapes of major industry players. With a forecast period spanning from 2025 to 2033, this report offers actionable insights for stakeholders seeking to capitalize on the transformative power of data center acceleration.

Data Center Accelerator Market Dynamics & Structure

The Data Center Accelerator Market is characterized by a dynamic interplay of technological innovation, increasing data volumes, and evolving regulatory landscapes. Market concentration remains moderately fragmented, with key players investing heavily in Research and Development (R&D) to gain a competitive edge. Technological innovation drivers are primarily focused on developing more powerful and energy-efficient processing units, alongside advancements in interconnectivity and memory technologies. Regulatory frameworks, particularly those pertaining to data privacy and security, indirectly influence the adoption of accelerators by dictating performance and compliance requirements. Competitive product substitutes, such as advancements in traditional CPUs and increasingly powerful GPUs, present a constant challenge, pushing accelerator vendors to highlight unique value propositions. End-user demographics are expanding beyond traditional high-performance computing (HPC) to include a broader range of industries embracing AI and machine learning. Mergers and acquisitions (M&A) are prevalent, as larger tech giants seek to integrate specialized acceleration technologies into their broader portfolios, exemplified by numerous acquisitions in the semiconductor and cloud computing sectors, with an estimated XX major M&A deals recorded during the historical period (2019-2024). Innovation barriers include the high cost of R&D, the complexity of integration, and the need for specialized expertise.

- Market Concentration: Moderately fragmented with significant R&D investment.

- Technological Drivers: Enhanced processing power, energy efficiency, reduced latency.

- Regulatory Influence: Data privacy and security mandates driving performance needs.

- Competitive Landscape: Intense competition from advanced CPUs and GPUs.

- End-User Evolution: Expansion beyond HPC to AI, ML, and cloud services.

- M&A Activity: Strategic acquisitions to integrate specialized acceleration IP.

- Innovation Barriers: High R&D costs, integration complexity, talent scarcity.

Data Center Accelerator Market Growth Trends & Insights

The Data Center Accelerator Market is experiencing robust growth, fueled by the exponential rise in data generation and the increasing computational demands of modern applications. The market size is projected to witness substantial expansion from an estimated USD XX Million in the base year of 2025 to reach USD XX Million by 2033, exhibiting a compelling Compound Annual Growth Rate (CAGR) of XX% during the forecast period. Adoption rates are accelerating across various industries, driven by the imperative to process massive datasets, perform complex simulations, and deploy sophisticated artificial intelligence and machine learning models. Technological disruptions are at the forefront, with continuous advancements in processor architectures, memory technologies, and interconnect fabrics enabling unprecedented performance gains. Consumer behavior shifts are also playing a crucial role, as businesses increasingly rely on data-driven insights and cloud-based services, necessitating powerful and scalable data center infrastructure. The market penetration of specialized accelerators, particularly in AI/ML workloads and HPC, is rapidly increasing, displacing traditional computing paradigms in specific applications. The inherent limitations of general-purpose processors in handling these specialized, highly parallelizable tasks are creating a strong demand for tailored acceleration solutions. This demand is further amplified by the growing need for faster inference and training times in AI models, which directly impacts time-to-market and competitive advantage for businesses. The evolution of cloud computing, with its emphasis on elasticity and on-demand resources, also positions accelerators as a critical component for delivering high-performance computing services efficiently.

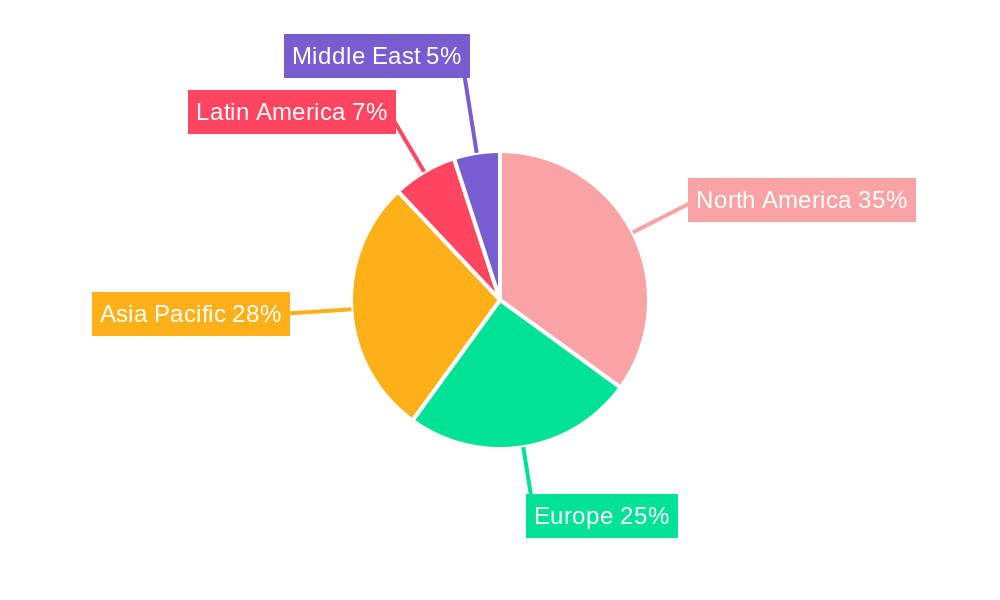

Dominant Regions, Countries, or Segments in Data Center Accelerator Market

The Data Center Accelerator Market is witnessing significant growth across several regions and segments, with North America and Asia Pacific emerging as dominant forces. Within the Processor Type segment, GPU (Graphics Processing Unit) currently holds a leading position due to its inherent parallel processing capabilities, making it highly suitable for AI, machine learning, and high-performance computing workloads. The Application segment of Artificial Intelligence is the primary growth driver, with an estimated market share of XX% in 2025, followed closely by High-performance Computing.

Dominant Regions:

- North America: Driven by a strong presence of major cloud providers, research institutions, and a robust AI/ML ecosystem, accounting for an estimated XX% market share.

- Asia Pacific: Experiencing rapid growth due to increasing digital transformation initiatives, burgeoning data center infrastructure development, and a significant manufacturing base for semiconductor components.

Key Growth Drivers in Dominant Segments:

- GPU Dominance:

- Unparalleled parallel processing power for AI/ML training and inference.

- Widespread adoption in cloud-based AI services and scientific research.

- Continuous architectural improvements leading to significant performance leaps.

- AI Application Dominance:

- Explosive growth in AI model development and deployment across industries like healthcare, finance, and autonomous driving.

- Demand for faster model training and real-time inference.

- Investment in AI infrastructure by major technology companies and startups.

- High-Performance Computing (HPC) Significance:

- Critical for scientific research, climate modeling, drug discovery, and complex simulations.

- Need for massive computational power to solve grand challenges.

- Government and institutional investments in supercomputing initiatives.

- GPU Dominance:

The FPGA (Field-Programmable Gate Array) segment is also witnessing considerable traction due to its flexibility and reconfigurability, particularly for specialized workloads and edge computing applications. While CPU (Central Processing Unit) remains foundational, its role in pure acceleration is diminishing for highly parallel tasks. ASIC (Application-specific Integrated Circuit) solutions are gaining momentum for specific, high-volume applications where cost-effectiveness and extreme optimization are paramount.

Data Center Accelerator Market Product Landscape

The Data Center Accelerator Market is characterized by a dynamic product landscape featuring continuous innovation in processing architectures and integrated solutions. Leading vendors are introducing accelerators with significantly enhanced processing densities, reduced power consumption per operation, and improved memory bandwidth. Key product innovations include specialized AI accelerators (e.g., TPUs, NPUs), reconfigurable FPGAs with integrated AI capabilities, and high-performance GPUs optimized for data center environments. These products are designed to address the stringent performance requirements of applications such as deep learning inference, natural language processing, computer vision, and large-scale scientific simulations. Unique selling propositions often revolve around tailored performance for specific workloads, lower Total Cost of Ownership (TCO) through improved energy efficiency, and seamless integration with existing cloud and on-premises infrastructure.

Key Drivers, Barriers & Challenges in Data Center Accelerator Market

Key Drivers:

- Explosive Data Growth: The relentless surge in data volume necessitates accelerated processing capabilities.

- AI/ML Adoption: The widespread integration of artificial intelligence and machine learning across industries is a primary growth engine.

- HPC Demand: Continued need for high-performance computing in scientific research, engineering, and complex simulations.

- Cloud Computing Expansion: The growth of cloud infrastructure demands efficient and scalable compute solutions.

- Energy Efficiency Focus: Increasing pressure to reduce data center power consumption and operational costs.

- Technological Advancements: Continuous innovation in semiconductor technology, leading to more powerful and efficient accelerators.

Barriers & Challenges:

- High Initial Investment: The cost of developing and deploying advanced accelerator hardware can be substantial.

- Integration Complexity: Integrating accelerators into existing data center architectures requires specialized expertise and can be challenging.

- Talent Scarcity: A shortage of skilled professionals in areas like hardware design, software optimization for accelerators, and AI/ML deployment.

- Rapid Technological Obsolescence: The fast pace of innovation can lead to products becoming outdated quickly, requiring continuous upgrades.

- Software Ecosystem Development: Ensuring robust and mature software stacks and development tools for new accelerator architectures is critical for adoption.

- Supply Chain Disruptions: Global supply chain volatility can impact the availability and cost of critical components.

Emerging Opportunities in Data Center Accelerator Market

Emerging opportunities within the Data Center Accelerator Market are numerous and poised for significant growth. The burgeoning field of edge computing presents a substantial opportunity for specialized, low-power accelerators capable of performing complex computations closer to the data source, reducing latency and bandwidth requirements. The increasing demand for personalized medicine and genomics research is driving the need for accelerated data analysis and simulation capabilities. Furthermore, the metaverse and immersive technologies will require immense processing power for rendering and real-time interaction, creating a new frontier for accelerator applications. Opportunities also lie in the development of hybrid acceleration solutions that intelligently combine CPUs, GPUs, FPGAs, and ASICs to optimize performance and cost for diverse workloads. The growing focus on sustainability and green computing will also foster innovation in energy-efficient accelerator designs.

Growth Accelerators in the Data Center Accelerator Market Industry

Several key catalysts are propelling long-term growth within the Data Center Accelerator Market. Technological breakthroughs in next-generation semiconductor materials and advanced packaging techniques are enabling the creation of even more powerful and efficient accelerators. Strategic partnerships between hardware manufacturers, software developers, and cloud service providers are crucial for creating integrated, end-to-end solutions that simplify adoption and accelerate time-to-value for end-users. Market expansion strategies, particularly into emerging economies and specialized industry verticals, are opening up new revenue streams. The continuous evolution of AI algorithms and the increasing complexity of machine learning models will continue to drive demand for specialized hardware acceleration. Furthermore, the growing emphasis on data sovereignty and localized processing will spur investment in on-premises and edge acceleration solutions.

Key Players Shaping the Data Center Accelerator Market Market

- Xilinx Inc (Advanced Micro Devices Inc)

- Achronix Semiconductor Corporation

- IBM Corporation

- NVIDIA Corporation

- Cisco Systems Inc

- Advanced Micro Devices Inc

- Qualcomm Technologies Inc

- NEC Corporation

- Dell Technologies Inc

- Intel Corporation

Notable Milestones in Data Center Accelerator Market Sector

- December 2022: Atos announced the development of "Atos' AWS Data Lake Accelerator for SAP," a new solution in collaboration with AWS, enabling clients to expedite and monitor KPIs through simplified access to SAP and non-SAP data silos, offering self-service and enterprise-wide reporting for significant insights.

- October 2022: Accenture and Google Cloud announced an expansion of their global partnership, focusing on growing talent pools, expanding joint capabilities, developing new data and AI solutions, and providing enhanced support for clients building digital cores and reinventing enterprises on the cloud.

- June 2022: Sanofi launched its first digital accelerator to foster its goal of becoming a premier digital healthcare company, aiming to create products and solutions that transform medicine through digital, data, and AI.

- June 2022: GE Digital announced the launch of its new accelerator product line, including software solutions to enable customers in asset-intensive energy industries to quickly set up Asset Performance Management (APM) and other services, accelerating time to value and extending APM capabilities.

In-Depth Data Center Accelerator Market Market Outlook

The future outlook for the Data Center Accelerator Market is exceptionally promising, driven by an accelerating demand for computational power and sophisticated data processing capabilities. Growth accelerators will continue to be powered by ongoing advancements in AI and machine learning, necessitating increasingly specialized hardware for model training and inference. The expansion of the metaverse and the growing need for real-time data analytics in industries such as autonomous vehicles and smart cities will create new avenues for accelerator adoption. Furthermore, the global push towards sustainability will drive innovation in energy-efficient accelerator designs, presenting strategic opportunities for market players. The ongoing evolution of cloud infrastructure and the increasing adoption of hybrid cloud models will further solidify the role of accelerators in delivering scalable and high-performance computing solutions. Companies that focus on developing flexible, reconfigurable, and power-efficient acceleration technologies, coupled with robust software ecosystems, are well-positioned to capitalize on the significant growth potential in this dynamic market.

Data Center Accelerator Market Segmentation

-

1. Processor Type

- 1.1. CPU (Central Processing Unit)

- 1.2. GPU (Graphics Processing Unit)

- 1.3. FPGA (Field-Programmable Gate Array)

- 1.4. ASIC (Application-specific Integrated Circuit)

-

2. Application

- 2.1. High-performance Computing

- 2.2. Artificial Intelligence

- 2.3. Other Applications

Data Center Accelerator Market Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East

Data Center Accelerator Market Regional Market Share

Geographic Coverage of Data Center Accelerator Market

Data Center Accelerator Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.19% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Processor Type

- 5.1.1. CPU (Central Processing Unit)

- 5.1.2. GPU (Graphics Processing Unit)

- 5.1.3. FPGA (Field-Programmable Gate Array)

- 5.1.4. ASIC (Application-specific Integrated Circuit)

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. High-performance Computing

- 5.2.2. Artificial Intelligence

- 5.2.3. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East

- 5.1. Market Analysis, Insights and Forecast - by Processor Type

- 6. Global Data Center Accelerator Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Processor Type

- 6.1.1. CPU (Central Processing Unit)

- 6.1.2. GPU (Graphics Processing Unit)

- 6.1.3. FPGA (Field-Programmable Gate Array)

- 6.1.4. ASIC (Application-specific Integrated Circuit)

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. High-performance Computing

- 6.2.2. Artificial Intelligence

- 6.2.3. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Processor Type

- 7. North America Data Center Accelerator Market Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Processor Type

- 7.1.1. CPU (Central Processing Unit)

- 7.1.2. GPU (Graphics Processing Unit)

- 7.1.3. FPGA (Field-Programmable Gate Array)

- 7.1.4. ASIC (Application-specific Integrated Circuit)

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. High-performance Computing

- 7.2.2. Artificial Intelligence

- 7.2.3. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Processor Type

- 8. Europe Data Center Accelerator Market Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Processor Type

- 8.1.1. CPU (Central Processing Unit)

- 8.1.2. GPU (Graphics Processing Unit)

- 8.1.3. FPGA (Field-Programmable Gate Array)

- 8.1.4. ASIC (Application-specific Integrated Circuit)

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. High-performance Computing

- 8.2.2. Artificial Intelligence

- 8.2.3. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Processor Type

- 9. Asia Pacific Data Center Accelerator Market Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Processor Type

- 9.1.1. CPU (Central Processing Unit)

- 9.1.2. GPU (Graphics Processing Unit)

- 9.1.3. FPGA (Field-Programmable Gate Array)

- 9.1.4. ASIC (Application-specific Integrated Circuit)

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. High-performance Computing

- 9.2.2. Artificial Intelligence

- 9.2.3. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Processor Type

- 10. Latin America Data Center Accelerator Market Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Processor Type

- 10.1.1. CPU (Central Processing Unit)

- 10.1.2. GPU (Graphics Processing Unit)

- 10.1.3. FPGA (Field-Programmable Gate Array)

- 10.1.4. ASIC (Application-specific Integrated Circuit)

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. High-performance Computing

- 10.2.2. Artificial Intelligence

- 10.2.3. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Processor Type

- 11. Middle East Data Center Accelerator Market Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Processor Type

- 11.1.1. CPU (Central Processing Unit)

- 11.1.2. GPU (Graphics Processing Unit)

- 11.1.3. FPGA (Field-Programmable Gate Array)

- 11.1.4. ASIC (Application-specific Integrated Circuit)

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. High-performance Computing

- 11.2.2. Artificial Intelligence

- 11.2.3. Other Applications

- 11.1. Market Analysis, Insights and Forecast - by Processor Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Xilinx Inc (Advanced Micro Devices Inc )

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Achronix Semiconductor Corporation

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 IBM Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 NVIDIA Corporation

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Cisco Systems Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Advanced Micro Devices Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Qualcomm Technologies Inc *List Not Exhaustive

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 NEC Corporation

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Dell Technologies Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Intel Corporation

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Xilinx Inc (Advanced Micro Devices Inc )

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Data Center Accelerator Market Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Data Center Accelerator Market Revenue (Million), by Processor Type 2025 & 2033

- Figure 3: North America Data Center Accelerator Market Revenue Share (%), by Processor Type 2025 & 2033

- Figure 4: North America Data Center Accelerator Market Revenue (Million), by Application 2025 & 2033

- Figure 5: North America Data Center Accelerator Market Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Data Center Accelerator Market Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Data Center Accelerator Market Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Data Center Accelerator Market Revenue (Million), by Processor Type 2025 & 2033

- Figure 9: Europe Data Center Accelerator Market Revenue Share (%), by Processor Type 2025 & 2033

- Figure 10: Europe Data Center Accelerator Market Revenue (Million), by Application 2025 & 2033

- Figure 11: Europe Data Center Accelerator Market Revenue Share (%), by Application 2025 & 2033

- Figure 12: Europe Data Center Accelerator Market Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Data Center Accelerator Market Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Data Center Accelerator Market Revenue (Million), by Processor Type 2025 & 2033

- Figure 15: Asia Pacific Data Center Accelerator Market Revenue Share (%), by Processor Type 2025 & 2033

- Figure 16: Asia Pacific Data Center Accelerator Market Revenue (Million), by Application 2025 & 2033

- Figure 17: Asia Pacific Data Center Accelerator Market Revenue Share (%), by Application 2025 & 2033

- Figure 18: Asia Pacific Data Center Accelerator Market Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Pacific Data Center Accelerator Market Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America Data Center Accelerator Market Revenue (Million), by Processor Type 2025 & 2033

- Figure 21: Latin America Data Center Accelerator Market Revenue Share (%), by Processor Type 2025 & 2033

- Figure 22: Latin America Data Center Accelerator Market Revenue (Million), by Application 2025 & 2033

- Figure 23: Latin America Data Center Accelerator Market Revenue Share (%), by Application 2025 & 2033

- Figure 24: Latin America Data Center Accelerator Market Revenue (Million), by Country 2025 & 2033

- Figure 25: Latin America Data Center Accelerator Market Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East Data Center Accelerator Market Revenue (Million), by Processor Type 2025 & 2033

- Figure 27: Middle East Data Center Accelerator Market Revenue Share (%), by Processor Type 2025 & 2033

- Figure 28: Middle East Data Center Accelerator Market Revenue (Million), by Application 2025 & 2033

- Figure 29: Middle East Data Center Accelerator Market Revenue Share (%), by Application 2025 & 2033

- Figure 30: Middle East Data Center Accelerator Market Revenue (Million), by Country 2025 & 2033

- Figure 31: Middle East Data Center Accelerator Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Data Center Accelerator Market Revenue Million Forecast, by Processor Type 2020 & 2033

- Table 2: Global Data Center Accelerator Market Revenue Million Forecast, by Application 2020 & 2033

- Table 3: Global Data Center Accelerator Market Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Data Center Accelerator Market Revenue Million Forecast, by Processor Type 2020 & 2033

- Table 5: Global Data Center Accelerator Market Revenue Million Forecast, by Application 2020 & 2033

- Table 6: Global Data Center Accelerator Market Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Global Data Center Accelerator Market Revenue Million Forecast, by Processor Type 2020 & 2033

- Table 8: Global Data Center Accelerator Market Revenue Million Forecast, by Application 2020 & 2033

- Table 9: Global Data Center Accelerator Market Revenue Million Forecast, by Country 2020 & 2033

- Table 10: Global Data Center Accelerator Market Revenue Million Forecast, by Processor Type 2020 & 2033

- Table 11: Global Data Center Accelerator Market Revenue Million Forecast, by Application 2020 & 2033

- Table 12: Global Data Center Accelerator Market Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global Data Center Accelerator Market Revenue Million Forecast, by Processor Type 2020 & 2033

- Table 14: Global Data Center Accelerator Market Revenue Million Forecast, by Application 2020 & 2033

- Table 15: Global Data Center Accelerator Market Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Data Center Accelerator Market Revenue Million Forecast, by Processor Type 2020 & 2033

- Table 17: Global Data Center Accelerator Market Revenue Million Forecast, by Application 2020 & 2033

- Table 18: Global Data Center Accelerator Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Data Center Accelerator Market?

The projected CAGR is approximately 14.19%.

2. Which companies are prominent players in the Data Center Accelerator Market?

Key companies in the market include Xilinx Inc (Advanced Micro Devices Inc ), Achronix Semiconductor Corporation, IBM Corporation, NVIDIA Corporation, Cisco Systems Inc, Advanced Micro Devices Inc, Qualcomm Technologies Inc *List Not Exhaustive, NEC Corporation, Dell Technologies Inc, Intel Corporation.

3. What are the main segments of the Data Center Accelerator Market?

The market segments include Processor Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 11.29 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Deployment of AI in HPC Data Centers; Increasing Deployment of Data Center Facilities and Cloud-Based Services.

6. What are the notable trends driving market growth?

FPGA Processor Type Segemnt is Expected to Hold Significant Market Share.

7. Are there any restraints impacting market growth?

Limited AI Hardware Experts Coupled with Infrastructural Concerns.

8. Can you provide examples of recent developments in the market?

December 2022 - Atos has announced the development of a new solution in collaboration with AWS that allows clients to expedite and properly monitor company key performance indicators (KPIs) by offering simple access to SAP and non-SAP data silos. "Atos' AWS Data Lake Accelerator for SAP" is a new solution that delivers self-service and enterprise-wide reporting for significant insights into daily changes that swiftly influence choices to drive the bottom line.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Data Center Accelerator Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Data Center Accelerator Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Data Center Accelerator Market?

To stay informed about further developments, trends, and reports in the Data Center Accelerator Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence