Key Insights

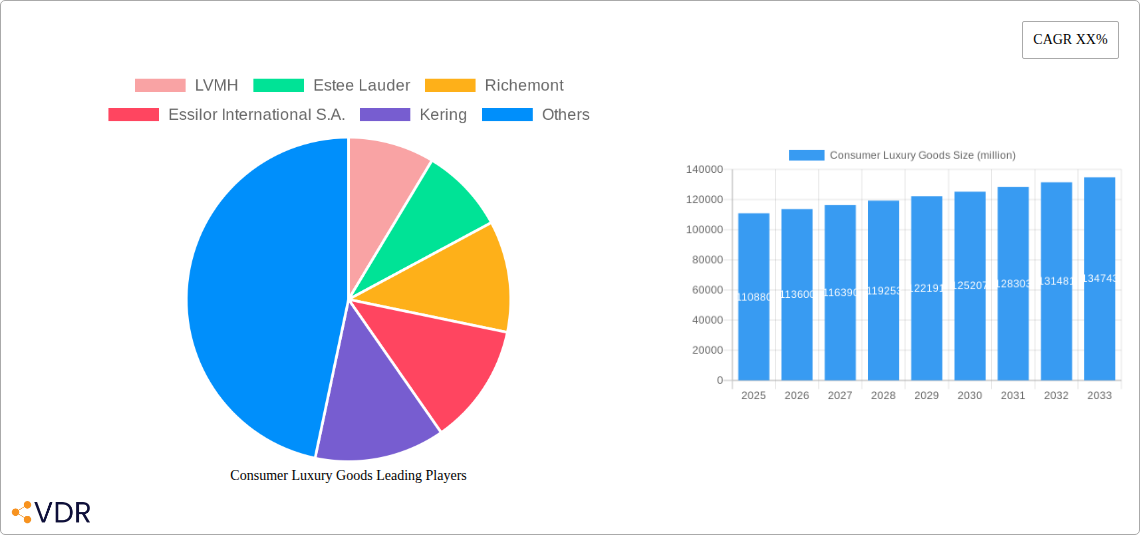

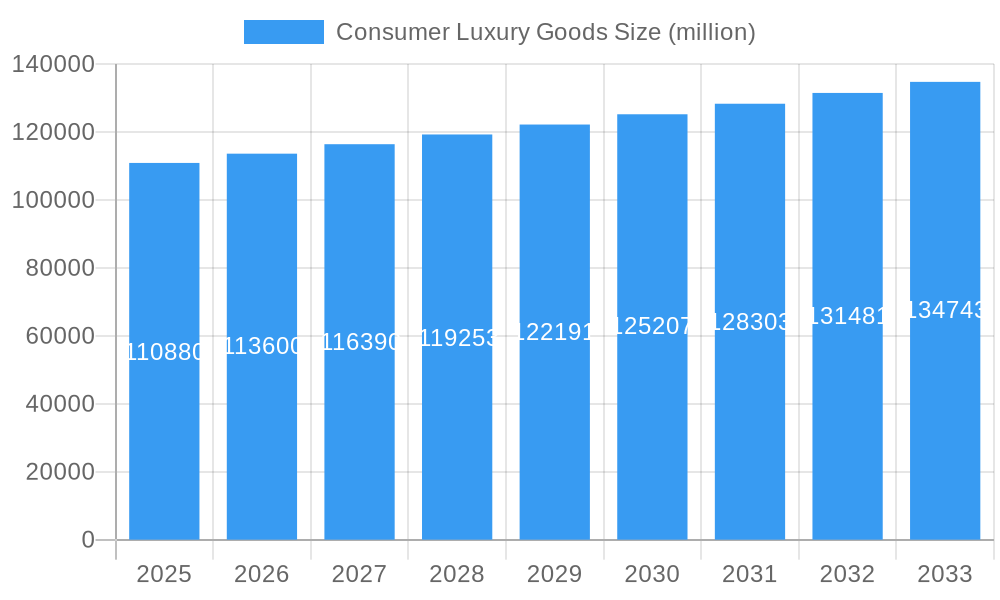

The global Consumer Luxury Goods market is poised for steady expansion, projected to reach a valuation of $110.88 billion in 2025, with a Compound Annual Growth Rate (CAGR) of 2.5% from 2025 to 2033. This robust growth is underpinned by a confluence of factors, including an escalating global disposable income, a growing affluent consumer base, and the increasing influence of digital channels in driving luxury purchases. The market's resilience is further bolstered by evolving consumer preferences towards experiential luxury, personalization, and sustainable offerings. Key drivers include the aspirational nature of luxury products, the desire for unique and high-quality items, and the significant investments made by major players in brand building and innovative product development. Geographically, the Asia Pacific region, particularly China and India, is emerging as a dominant force, driven by a rapidly growing middle class and an increasing appetite for premium goods.

Consumer Luxury Goods Market Size (In Billion)

The Consumer Luxury Goods market is segmented across various applications and product types, reflecting the diverse demands of its discerning clientele. Online sales channels are experiencing a significant surge, driven by enhanced e-commerce platforms and digital marketing strategies that offer convenience and a wider selection to consumers. Simultaneously, offline sales, particularly within flagship stores and exclusive boutiques, continue to hold their appeal, offering an immersive and personalized brand experience. Apparel, bags and accessories, cosmetics, and watches and jewelry represent the core product categories, each exhibiting distinct growth trajectories influenced by fashion trends, technological advancements, and shifting consumer tastes. Emerging markets and the increasing digital savviness of consumers are expected to further fuel this growth, while the sector's ability to adapt to evolving sustainability demands and geopolitical shifts will be crucial for sustained success.

Consumer Luxury Goods Company Market Share

Consumer Luxury Goods Market Dynamics & Structure

The global consumer luxury goods market is characterized by a moderate to high degree of concentration, with a few dominant players like LVMH, Richemont, and Kering holding significant market share. These conglomerates leverage strategic acquisitions and brand portfolio diversification to maintain their competitive edge. Technological innovation, particularly in e-commerce platforms, AI-driven personalization, and augmented reality (AR) for virtual try-ons, is a critical driver. However, the luxury sector also faces unique regulatory frameworks focused on intellectual property protection, authenticity verification, and increasingly, sustainability standards. The threat of competitive product substitutes is relatively low within the core luxury segments, as the perceived value is intrinsically tied to brand heritage, craftsmanship, and exclusivity. End-user demographics are evolving, with a growing influence of affluent millennials and Gen Z consumers who prioritize experiences, sustainability, and digital engagement. Mergers and acquisitions (M&A) activity remains a significant trend, with companies seeking to expand their geographical reach, acquire niche brands, or integrate complementary technologies. For instance, in the historical period, M&A deals focused on acquiring digital native luxury brands or enhancing supply chain transparency. The market size for consumer luxury goods was estimated at $300 billion in 2024, with a projected market share for the top 5 companies at approximately 65%. Innovation barriers include the inherent need to maintain exclusivity and craftsmanship while scaling operations, alongside the challenge of adapting traditional luxury retail models to digital-first consumer expectations.

- Market Concentration: Moderate to high, dominated by LVMH, Richemont, Kering.

- Technological Innovation Drivers: E-commerce, AI personalization, AR virtual try-ons, blockchain for authenticity.

- Regulatory Frameworks: IP protection, authenticity, sustainability standards, data privacy.

- Competitive Product Substitutes: Low within core luxury, but adjacent markets like premium affordable luxury are emerging.

- End-User Demographics: Growing influence of Millennials and Gen Z, demand for experiential luxury and sustainability.

- M&A Trends: Acquisitions of digital brands, supply chain integration, expansion into emerging markets.

- M&A Deal Volume (2019-2024): Approximately 50 significant deals, totaling over $50 billion in value.

- Innovation Barriers: Balancing exclusivity with scalability, digital transformation of heritage brands.

Consumer Luxury Goods Growth Trends & Insights

The global consumer luxury goods market is poised for robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 6.5% during the forecast period of 2025–2033. This expansion is driven by a confluence of factors, including increasing disposable incomes in emerging economies, a growing aspirational consumer base, and the continued resilience of high-net-worth individuals. The market size, estimated at $300 billion in 2024, is expected to reach over $500 billion by 2033. Adoption rates for digital luxury channels are surging, with online sales projected to account for over 40% of the total market by 2033, a significant leap from approximately 20% in the historical period. This shift is fueled by enhanced customer experiences offered through sophisticated e-commerce platforms, virtual showrooms, and personalized digital marketing. Technological disruptions are reshaping the luxury landscape, with the integration of Artificial Intelligence (AI) for hyper-personalized recommendations, augmented reality (AR) for virtual try-ons, and blockchain technology for ensuring product authenticity and traceability. These innovations not only enhance customer engagement but also build trust and transparency, crucial elements in the luxury sector.

Consumer behavior has undergone a notable transformation. The post-pandemic era has seen a heightened emphasis on sustainable and ethically sourced luxury goods, with consumers actively seeking brands that align with their values. Experiential luxury, encompassing travel, fine dining, and exclusive events, continues to gain traction as consumers prioritize memorable moments over material possessions. The "quiet luxury" trend, characterized by understated elegance and superior craftsmanship, is also influencing purchasing decisions, signaling a move away from overt branding. Geographically, Asia-Pacific, particularly China, remains a pivotal growth engine, driven by a rapidly expanding middle and upper class with a strong appetite for Western and local luxury brands. North America and Europe continue to exhibit steady growth, buoyed by established luxury markets and a sustained demand for heritage brands. The watches and jewelry segment is expected to maintain its dominance, driven by the intrinsic value and investment appeal of these items. However, significant growth is also anticipated in the luxury apparel and bags & accessories segments, as brands adeptly blend traditional craftsmanship with contemporary design and digital accessibility. The "Others" category, which includes luxury experiences and services, is also experiencing rapid expansion, reflecting the broader shift in consumer preferences. The market penetration of luxury goods is increasing across a wider demographic, though the core affluent segment continues to be the primary driver. This dynamic evolution underscores the industry's adaptability and its capacity to innovate in response to changing consumer desires and technological advancements.

- Market Size Evolution: Projected to grow from $300 billion (2024) to over $500 billion (2033).

- CAGR: Approximately 6.5% during the forecast period (2025–2033).

- Online Sales Growth: Expected to reach over 40% of the total market by 2033.

- Technological Advancements: AI for personalization, AR for virtual try-ons, blockchain for authenticity.

- Consumer Behavior Shifts: Increased demand for sustainability, ethical sourcing, and experiential luxury.

- Geographic Growth Engines: Asia-Pacific (especially China), North America, Europe.

- Dominant Segments: Watches & Jewelry, Apparel, Bags & Accessories.

- Emerging Trend: "Quiet Luxury."

Dominant Regions, Countries, or Segments in Consumer Luxury Goods

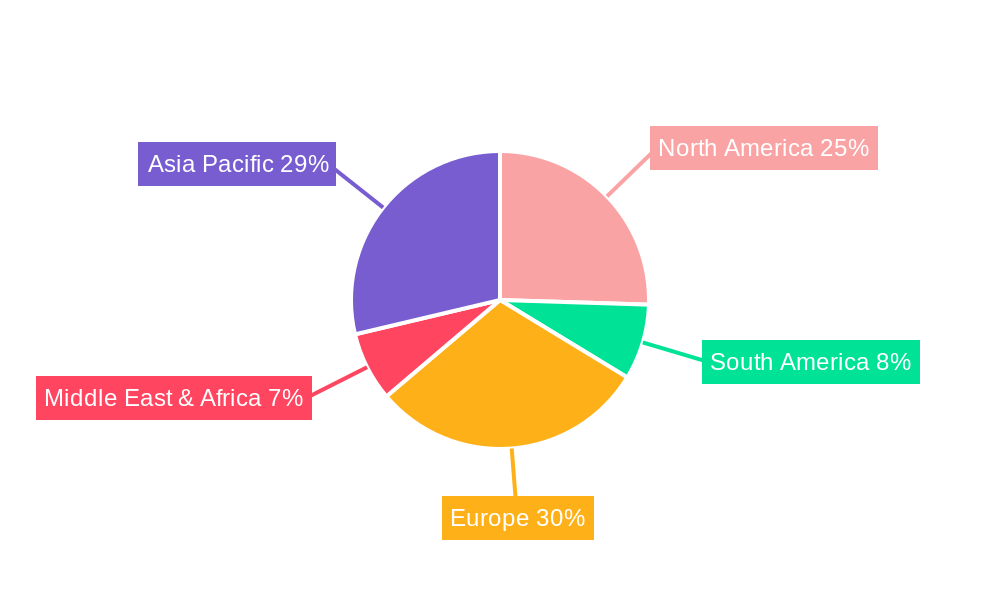

The Asia-Pacific region stands as the most dominant and rapidly expanding force within the global consumer luxury goods market, driven by a potent combination of economic prosperity, a burgeoning affluent demographic, and evolving consumer preferences. China, in particular, is a powerhouse, accounting for a significant portion of global luxury sales and exhibiting exceptional growth potential. This dominance is underpinned by several key factors.

Economically, many Asia-Pacific nations have experienced sustained periods of high GDP growth, leading to a significant increase in disposable income and the creation of a vast aspirational consumer base. This rise in wealth directly translates into a greater capacity and desire to purchase high-value luxury items. Furthermore, the region's vibrant digital ecosystem and high smartphone penetration have facilitated the rapid adoption of online luxury sales channels. Brands have invested heavily in localized e-commerce platforms, social commerce initiatives, and engaging digital content, catering to the tech-savvy Asian consumer. For instance, online sales in China within the luxury segment are estimated to have reached $75 billion in 2024, a substantial portion of the global online luxury market.

Infrastructure development in major Asian cities has also played a crucial role. The establishment of world-class luxury retail destinations, sophisticated logistics networks, and an increasing presence of flagship stores of global luxury houses have enhanced accessibility and desirability. This physical presence complements the digital push, offering a complete omnichannel experience.

Within the Types segment, Watches and Jewelry continue to be a leading driver of market growth, with an estimated market size of $80 billion in 2024. This enduring appeal stems from the intrinsic value, craftsmanship, and heritage associated with luxury timepieces and exquisite jewelry. Brands like Rolex, Chow Tai Fook Jewellery, and Lao Feng Xiang are pivotal players, commanding strong brand loyalty and a discerning clientele. The investment aspect of watches and jewelry also contributes to their sustained demand, particularly among older, established wealth segments and increasingly, younger investors.

However, the Apparel and Bags & Accessories segments are exhibiting remarkable growth, driven by brands like LVMH (Louis Vuitton, Dior), Kering (Gucci, Saint Laurent), and Hermes. These categories are highly responsive to fashion trends and celebrity endorsements, making them dynamic and influential. The estimated market size for Apparel was $70 billion in 2024, and for Bags & Accessories, it was $65 billion. The increasing adoption of "affordable luxury" or accessible luxury by brands like Michael Kors and Tapestry (Coach) is also expanding the consumer base within these segments.

The Cosmetics segment, with an estimated market size of $45 billion in 2024, is another significant contributor, spearheaded by giants like L'Oreal Luxe and Estee Lauder. This segment benefits from continuous product innovation, personalized beauty solutions, and strong demand from both online and offline channels. The growing influence of social media beauty influencers and the rising trend of self-care are further propelling its growth.

The Application of Online Sales is rapidly gaining prominence, projected to capture over 40% of the total luxury market by 2033. This shift is not just about convenience but also about brands leveraging digital platforms for immersive storytelling, virtual try-ons, and personalized customer journeys. The estimated online sales for luxury goods in 2024 were $60 billion, representing 20% of the total market. While offline sales still hold a majority, their growth is increasingly intertwined with digital strategies, creating an omnichannel experience.

- Dominant Region: Asia-Pacific, driven by China's economic growth and digital adoption.

- Key Asian Countries: China, South Korea, Japan, Singapore.

- Dominant Type Segment: Watches and Jewelry (estimated $80 billion in 2024).

- High-Growth Type Segments: Apparel ($70 billion in 2024), Bags and Accessories ($65 billion in 2024).

- Significant Type Segment: Cosmetics ($45 billion in 2024).

- Dominant Application: Online Sales (projected to exceed 40% by 2033, estimated $60 billion in 2024).

- Key Drivers in Asia-Pacific: Increasing disposable income, tech-savvy consumers, robust digital infrastructure.

- Key Drivers for Watches & Jewelry: Intrinsic value, craftsmanship, investment appeal.

- Key Drivers for Apparel & Bags: Fashion trends, celebrity influence, accessible luxury.

Consumer Luxury Goods Product Landscape

The consumer luxury goods product landscape is defined by an unwavering commitment to unparalleled craftsmanship, innovative materials, and unique design aesthetics. Brands are continuously pushing the boundaries of what is possible, integrating cutting-edge technologies to enhance both the product and the customer experience. For instance, in the Watches and Jewelry segment, advancements in material science are yielding incredibly durable and lightweight alloys, while the integration of smart functionalities is subtly appearing in high-end timepieces without compromising their classic appeal. In Apparel and Bags & Accessories, we are witnessing a rise in the use of sustainable and traceable materials, alongside intricate detailing and personalized customization options. Companies like Hermes are renowned for their artisanal leather goods, while Ralph Lauren and Burberry consistently deliver collections that blend heritage with contemporary relevance. The Cosmetics sector is characterized by a relentless pursuit of efficacy through advanced formulations, personalized skincare solutions driven by AI, and the growing popularity of clean beauty and ethically sourced ingredients. Essilor International S.A., while primarily known for eyewear, also influences the luxury accessories space with its focus on premium vision solutions. The overall product strategy emphasizes exclusivity, durability, and a narrative of heritage and innovation, ensuring that each piece holds enduring value and desirability.

Key Drivers, Barriers & Challenges in Consumer Luxury Goods

The consumer luxury goods market is propelled by several key drivers. The burgeoning global affluent population, particularly in emerging markets, represents a significant and growing customer base. Technological innovation, encompassing personalized digital experiences, AI-driven recommendations, and advanced e-commerce platforms, is crucial for engaging modern luxury consumers. The enduring allure of brand heritage, exclusivity, and superior craftsmanship continues to be a fundamental draw. Furthermore, a rising consumer consciousness towards sustainability and ethical sourcing is increasingly influencing purchasing decisions, creating new avenues for growth and brand differentiation. Strategic marketing, including collaborations with influential figures and immersive brand storytelling, also plays a vital role in shaping perception and demand.

However, the industry faces significant barriers and challenges. Maintaining exclusivity and authenticity in an increasingly digital and globalized market is a constant struggle. The threat of counterfeiting remains pervasive, requiring continuous investment in intellectual property protection and authentication technologies. Supply chain disruptions, exacerbated by geopolitical events and logistical complexities, can impact production and timely delivery of high-value goods. Evolving regulatory landscapes concerning data privacy, sustainability reporting, and trade policies can create compliance hurdles. Moreover, the intense competition among established luxury houses and the emergence of digitally native luxury brands necessitate constant innovation and adaptation to stay ahead. The substantial capital investment required for brand building, R&D, and maintaining premium retail experiences also acts as a barrier to entry for new players.

- Key Drivers: Growing global affluent population, technological innovation, brand heritage & exclusivity, sustainability focus, strategic marketing.

- Barriers & Challenges: Maintaining exclusivity & authenticity, counterfeiting, supply chain disruptions, evolving regulations, intense competition, high capital investment.

Emerging Opportunities in Consumer Luxury Goods

Emerging opportunities in the consumer luxury goods industry lie in the continued expansion of personalized and experiential luxury. The metaverse and NFTs present novel avenues for digital ownership, virtual goods, and immersive brand experiences, tapping into younger, digitally native consumers. A deeper integration of sustainability and circular economy principles, beyond mere compliance, can foster brand loyalty and attract ethically conscious consumers. The untapped potential in developing markets outside of traditional luxury hubs, coupled with localized product offerings that resonate with regional cultural nuances, represents a significant growth frontier. Furthermore, leveraging data analytics for hyper-personalization of product recommendations, customer service, and exclusive offers can deepen customer relationships and drive repeat purchases.

Growth Accelerators in the Consumer Luxury Goods Industry

Several catalysts are accelerating long-term growth in the consumer luxury goods industry. The ongoing digital transformation, including the adoption of AI for enhanced customer engagement and e-commerce optimization, is fundamental. Strategic partnerships and collaborations, whether with artists, influencers, or complementary luxury brands, can create unique value propositions and expand market reach. Market expansion into underdeveloped luxury markets, supported by tailored marketing strategies and localized retail approaches, will unlock new revenue streams. The continued emphasis on product innovation, particularly in sustainable materials and smart technologies, will cater to evolving consumer demands and maintain brand relevance. Furthermore, a focus on cultivating strong brand communities through exclusive events, loyalty programs, and engaging digital content will foster enduring customer relationships.

Key Players Shaping the Consumer Luxury Goods Market

- LVMH

- Estee Lauder

- Richemont

- Essilor International S.A.

- Kering

- L'Oreal Luxe

- The Swatch Group

- Ralph Lauren

- PVH

- Chow Tai Fook Jewellery

- Hermes

- Rolex

- Lao Feng Xiang

- Michael Kors

- Tapestry (Coach)

- Tiffany

- Shiseido

- Burberry

- Prada

- Pandora

Notable Milestones in Consumer Luxury Goods Sector

- 2019: LVMH acquires Tiffany & Co. for $16.2 billion, consolidating its jewelry portfolio.

- 2020: The COVID-19 pandemic significantly impacts physical retail, accelerating the shift to online sales and digital engagement strategies.

- 2021: Increased focus on sustainability and ethical sourcing as key consumer demands, leading to more transparent supply chains and eco-friendly product lines.

- 2022: Brands begin experimenting with the Metaverse and NFTs, launching digital collectibles and virtual experiences to engage younger demographics.

- 2023: Rise of "quiet luxury" trend, emphasizing understated elegance and quality craftsmanship over overt branding.

- 2024: Continued growth in online sales and omnichannel strategies become standard for leading luxury brands.

In-Depth Consumer Luxury Goods Market Outlook

The future outlook for the consumer luxury goods market is exceptionally bright, propelled by a persistent global economic expansion and an ever-growing affluent consumer base. Growth accelerators such as the increasing adoption of digital technologies for hyper-personalization and immersive brand experiences will continue to redefine customer engagement. Strategic market expansion into untapped regions, coupled with a heightened focus on sustainability and ethical production, will resonate with conscious consumers and foster long-term brand loyalty. The industry's capacity for innovation in product design, material science, and integrated smart functionalities will ensure its continued appeal. Expect to witness further consolidation through strategic M&A activities and a stronger emphasis on cultivating robust brand communities, all contributing to a sustained period of robust growth and evolving market dynamics.

Consumer Luxury Goods Segmentation

-

1. Application

- 1.1. Online Sales

- 1.2. Offline Sales

-

2. Types

- 2.1. Apparel

- 2.2. Bags and Accessories

- 2.3. Cosmetics

- 2.4. Watches and Jewelry

- 2.5. Others

Consumer Luxury Goods Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Consumer Luxury Goods Regional Market Share

Geographic Coverage of Consumer Luxury Goods

Consumer Luxury Goods REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Consumer Luxury Goods Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Online Sales

- 5.1.2. Offline Sales

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Apparel

- 5.2.2. Bags and Accessories

- 5.2.3. Cosmetics

- 5.2.4. Watches and Jewelry

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Consumer Luxury Goods Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Online Sales

- 6.1.2. Offline Sales

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Apparel

- 6.2.2. Bags and Accessories

- 6.2.3. Cosmetics

- 6.2.4. Watches and Jewelry

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Consumer Luxury Goods Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Online Sales

- 7.1.2. Offline Sales

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Apparel

- 7.2.2. Bags and Accessories

- 7.2.3. Cosmetics

- 7.2.4. Watches and Jewelry

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Consumer Luxury Goods Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Online Sales

- 8.1.2. Offline Sales

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Apparel

- 8.2.2. Bags and Accessories

- 8.2.3. Cosmetics

- 8.2.4. Watches and Jewelry

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Consumer Luxury Goods Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Online Sales

- 9.1.2. Offline Sales

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Apparel

- 9.2.2. Bags and Accessories

- 9.2.3. Cosmetics

- 9.2.4. Watches and Jewelry

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Consumer Luxury Goods Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Online Sales

- 10.1.2. Offline Sales

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Apparel

- 10.2.2. Bags and Accessories

- 10.2.3. Cosmetics

- 10.2.4. Watches and Jewelry

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 LVMH

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Estee Lauder

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Richemont

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Essilor International S.A.

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Kering

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 L'Oreal Luxe

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 The Swatch Group

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Ralph Lauren

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 PVH

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Chow Tai Fook Jewellery

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Hermes

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Rolex

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Lao Feng Xiang

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Michael Kors

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Tapestry (Coach)

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Tiffany

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Shiseido

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Burberry

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Prada

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Pandora

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.1 LVMH

List of Figures

- Figure 1: Global Consumer Luxury Goods Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Consumer Luxury Goods Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Consumer Luxury Goods Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Consumer Luxury Goods Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Consumer Luxury Goods Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Consumer Luxury Goods Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Consumer Luxury Goods Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Consumer Luxury Goods Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Consumer Luxury Goods Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Consumer Luxury Goods Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Consumer Luxury Goods Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Consumer Luxury Goods Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Consumer Luxury Goods Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Consumer Luxury Goods Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Consumer Luxury Goods Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Consumer Luxury Goods Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Consumer Luxury Goods Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Consumer Luxury Goods Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Consumer Luxury Goods Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Consumer Luxury Goods Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Consumer Luxury Goods Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Consumer Luxury Goods Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Consumer Luxury Goods Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Consumer Luxury Goods Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Consumer Luxury Goods Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Consumer Luxury Goods Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Consumer Luxury Goods Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Consumer Luxury Goods Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Consumer Luxury Goods Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Consumer Luxury Goods Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Consumer Luxury Goods Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Consumer Luxury Goods Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Consumer Luxury Goods Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Consumer Luxury Goods Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Consumer Luxury Goods Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Consumer Luxury Goods Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Consumer Luxury Goods Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Consumer Luxury Goods Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Consumer Luxury Goods Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Consumer Luxury Goods Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Consumer Luxury Goods Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Consumer Luxury Goods Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Consumer Luxury Goods Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Consumer Luxury Goods Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Consumer Luxury Goods Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Consumer Luxury Goods Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Consumer Luxury Goods Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Consumer Luxury Goods Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Consumer Luxury Goods Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Consumer Luxury Goods Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Consumer Luxury Goods Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Consumer Luxury Goods Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Consumer Luxury Goods Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Consumer Luxury Goods Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Consumer Luxury Goods Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Consumer Luxury Goods Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Consumer Luxury Goods Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Consumer Luxury Goods Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Consumer Luxury Goods Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Consumer Luxury Goods Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Consumer Luxury Goods Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Consumer Luxury Goods Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Consumer Luxury Goods Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Consumer Luxury Goods Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Consumer Luxury Goods Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Consumer Luxury Goods Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Consumer Luxury Goods Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Consumer Luxury Goods Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Consumer Luxury Goods Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Consumer Luxury Goods Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Consumer Luxury Goods Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Consumer Luxury Goods Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Consumer Luxury Goods Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Consumer Luxury Goods Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Consumer Luxury Goods Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Consumer Luxury Goods Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Consumer Luxury Goods Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Consumer Luxury Goods?

The projected CAGR is approximately 2.5%.

2. Which companies are prominent players in the Consumer Luxury Goods?

Key companies in the market include LVMH, Estee Lauder, Richemont, Essilor International S.A., Kering, L'Oreal Luxe, The Swatch Group, Ralph Lauren, PVH, Chow Tai Fook Jewellery, Hermes, Rolex, Lao Feng Xiang, Michael Kors, Tapestry (Coach), Tiffany, Shiseido, Burberry, Prada, Pandora.

3. What are the main segments of the Consumer Luxury Goods?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Consumer Luxury Goods," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Consumer Luxury Goods report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Consumer Luxury Goods?

To stay informed about further developments, trends, and reports in the Consumer Luxury Goods, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence