Key Insights

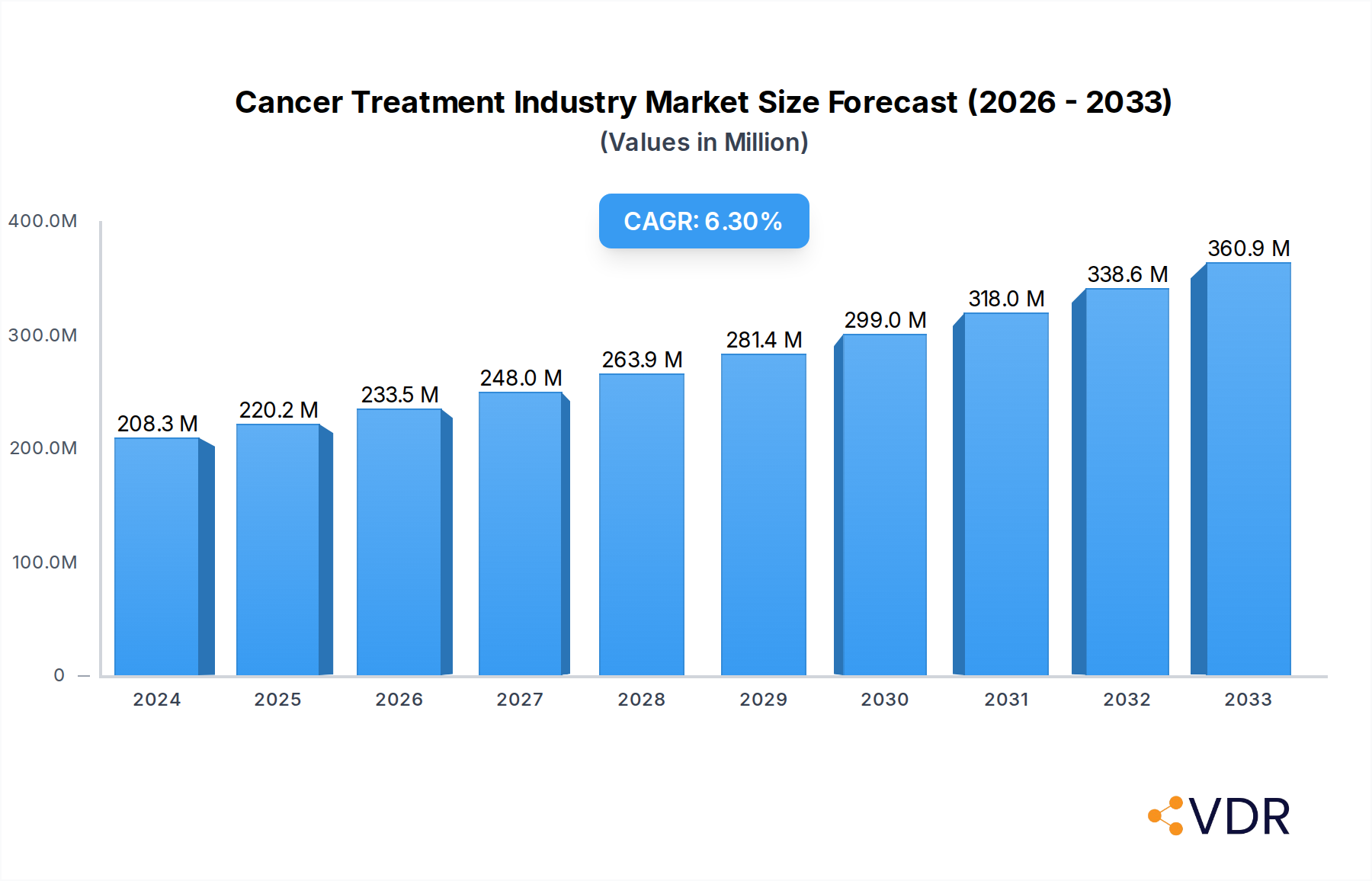

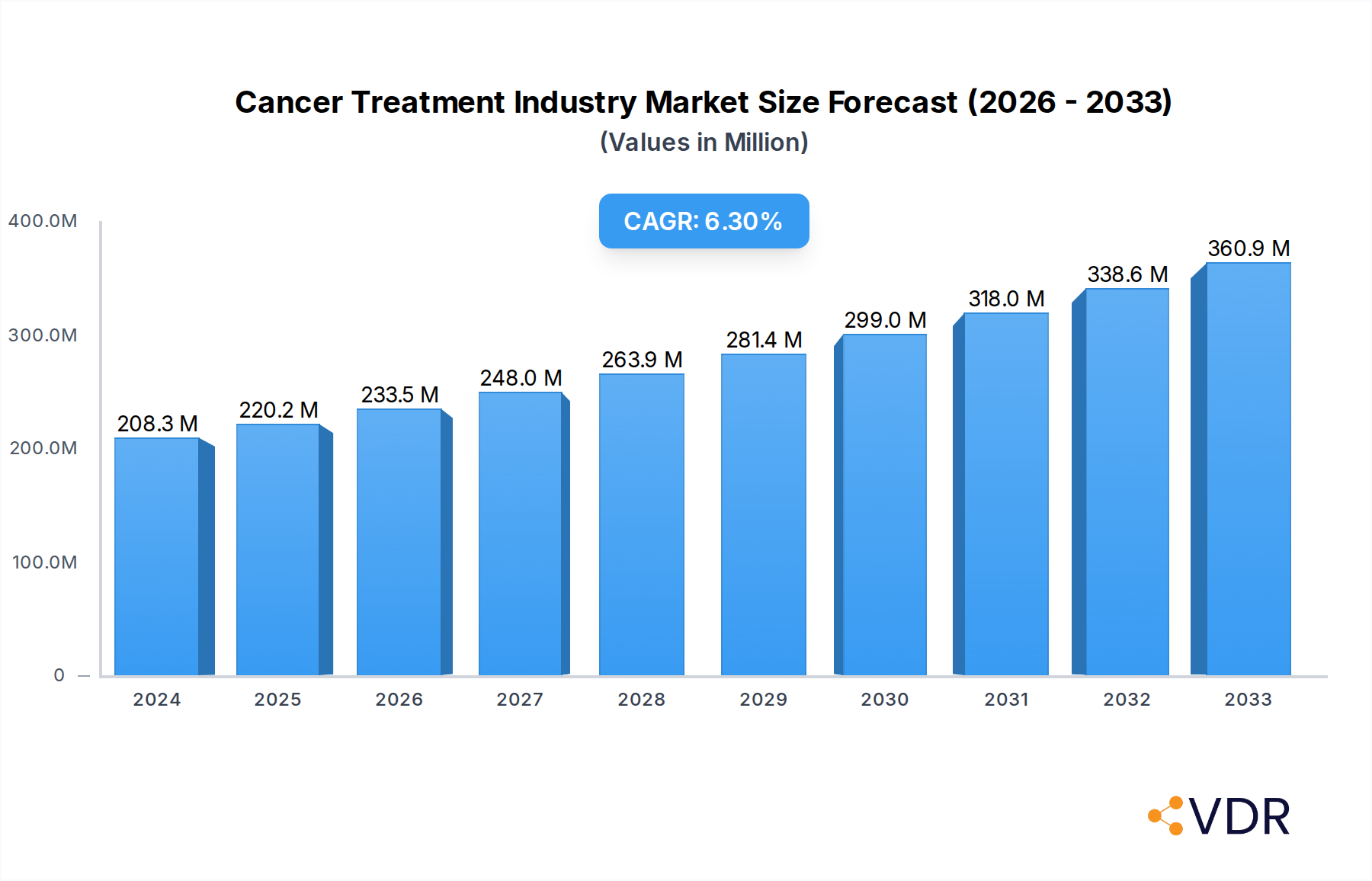

The global Cancer Treatment Market is poised for significant expansion, projected to reach $220.24 million by 2025. This robust growth is fueled by a compound annual growth rate (CAGR) of 10.64%, indicating a dynamic and evolving landscape driven by advancements in therapeutic approaches and increasing cancer prevalence worldwide. Key growth drivers include the escalating demand for targeted therapies and immunotherapies, which offer more precise and less toxic treatment options compared to traditional chemotherapy. Furthermore, the growing incidence of prevalent cancer types such as breast cancer, lung cancer, and blood cancer, coupled with an aging global population, contributes substantially to market expansion. The market is segmented across various therapy types, including chemotherapy, targeted therapy, immunotherapy, and hormonal therapy, reflecting the diverse and specialized nature of modern cancer care. End-user segments, encompassing hospitals, specialty clinics, and cancer and radiation therapy centers, are all experiencing increased demand for advanced treatment modalities.

Cancer Treatment Industry Market Size (In Million)

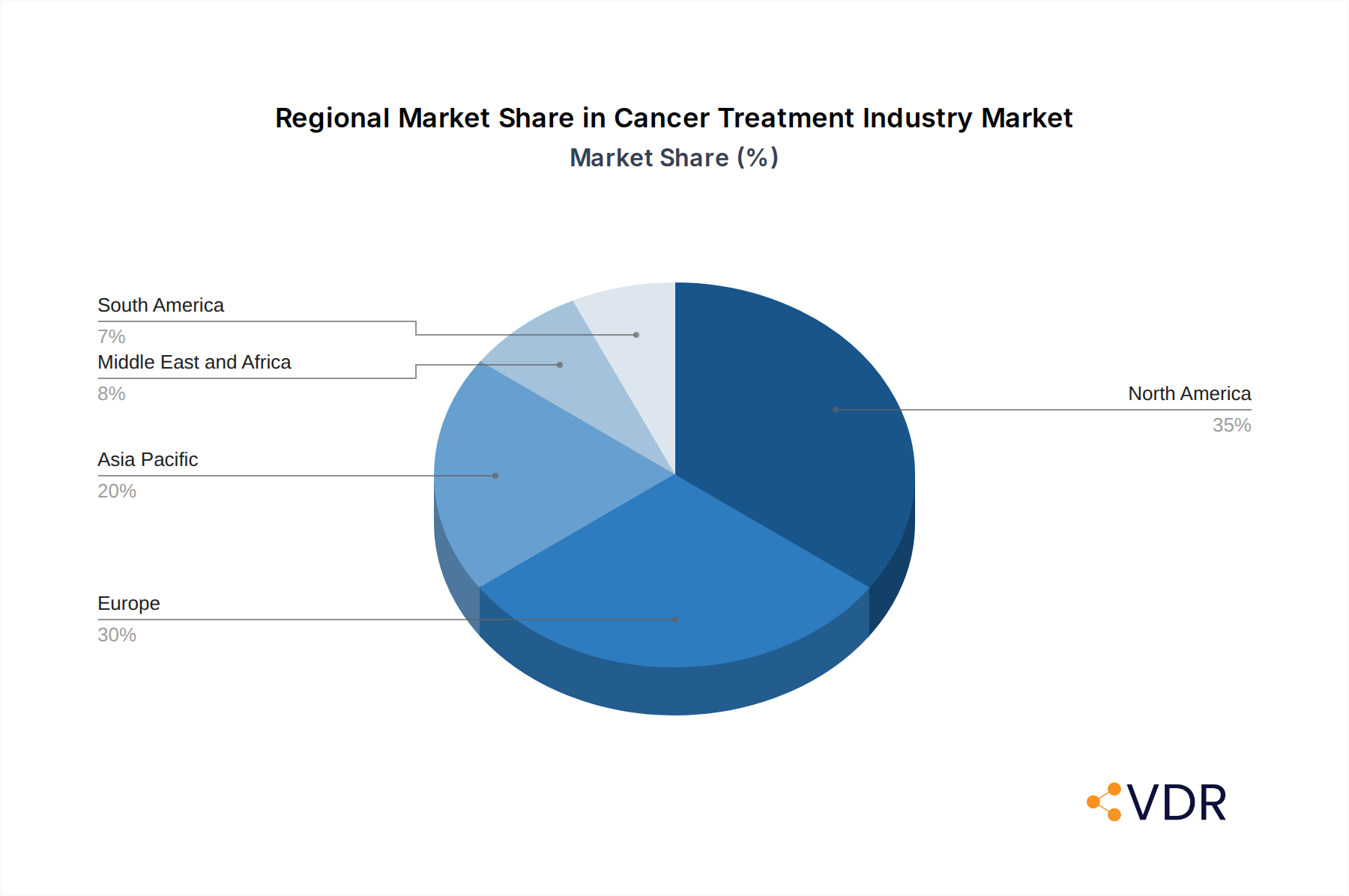

The market's trajectory is further shaped by a focus on personalized medicine and innovative drug development, with major pharmaceutical and biotechnology companies heavily investing in research and development. While the market benefits from these advancements, it also faces certain restraints. These may include the high cost of novel cancer therapies, the complexities associated with clinical trials and regulatory approvals, and the potential for side effects associated with certain treatments. Nevertheless, the increasing global efforts in cancer research, early detection initiatives, and improved healthcare infrastructure are expected to mitigate these challenges. Regions like North America and Europe currently dominate the market due to advanced healthcare systems and higher healthcare spending, but the Asia Pacific region is anticipated to witness the fastest growth due to increasing investment in healthcare and a rising cancer burden.

Cancer Treatment Industry Company Market Share

Comprehensive Cancer Treatment Industry Report: Market Insights, Growth Drivers, and Key Players (2019–2033)

This in-depth report offers a panoramic view of the global Cancer Treatment Industry, meticulously analyzing its current landscape, historical trajectory, and future projections. Covering the period from 2019 to 2033, with a base and estimated year of 2025, this research provides unparalleled insights into market dynamics, growth trends, dominant segments, product innovations, key drivers, emerging opportunities, and the competitive ecosystem. With a focus on high-traffic keywords such as "cancer therapy market," "oncology drugs," "chemotherapy," "targeted therapy," "immunotherapy," "blood cancer treatment," "breast cancer solutions," and "lung cancer therapies," this report is engineered to maximize search engine visibility and deliver actionable intelligence to industry professionals. We explore both parent and child market segments to offer a holistic understanding of value chains and sub-sector growth. All monetary values are presented in Million units.

Cancer Treatment Industry Market Dynamics & Structure

The Cancer Treatment Industry is characterized by a dynamic interplay of innovation, regulation, and strategic consolidation. Market concentration is influenced by the significant R&D investments required, leading to a landscape dominated by large pharmaceutical and biotechnology firms, alongside a growing number of agile biotechs focusing on niche therapies. Technological innovation is a primary driver, with breakthroughs in precision medicine, immunotherapy, and gene therapy continuously reshaping treatment paradigms. Regulatory frameworks, particularly those of the FDA and EMA, play a crucial role in approving novel therapies and ensuring patient safety, acting as both enablers and gatekeepers. Competitive product substitutes are emerging rapidly, especially in areas like immunotherapy, challenging traditional chemotherapy approaches. End-user demographics are shifting, with an aging global population and increasing cancer incidence driving demand, while advancements in diagnostics influence treatment selection. Mergers and acquisitions (M&A) are frequent, as larger companies seek to acquire innovative technologies and expand their oncology portfolios. For instance, the historical period (2019-2024) saw an estimated 45 major M&A deals valued at over $10 billion collectively, aimed at bolstering market share and pipeline diversity.

- Market Concentration: Dominated by a blend of large pharmaceutical giants and specialized biotechs, with an estimated 70% of market share held by the top 10 companies.

- Technological Innovation: Driven by advancements in genomics, molecular diagnostics, AI-driven drug discovery, and novel drug delivery systems.

- Regulatory Impact: Strict approval processes for novel oncology drugs, with average approval times for innovative therapies ranging from 8-12 years.

- Competitive Substitutes: Rising adoption of immunotherapies and targeted therapies reducing reliance on traditional chemotherapy in certain cancer types.

- End-User Demographics: Increasing demand due to aging populations and rising cancer prevalence; an estimated 35% increase in cancer diagnoses globally from 2019-2024.

- M&A Trends: Active consolidation, with approximately 10-15 significant acquisitions per year within the oncology space during the historical period, focusing on pipeline assets and innovative platforms.

Cancer Treatment Industry Growth Trends & Insights

The Cancer Treatment Industry is poised for robust growth, driven by a confluence of escalating cancer incidence, significant advancements in therapeutic modalities, and increasing healthcare expenditure globally. The market size evolution is a testament to sustained innovation and expanding treatment options. The global oncology market experienced a compound annual growth rate (CAGR) of approximately 8.5% from 2019 to 2024. Looking ahead, the forecast period (2025–2033) is expected to witness a CAGR of around 9.2%, projecting a market value to reach an estimated $350,000 million by 2033. Adoption rates for newer therapies, particularly immunotherapies and targeted agents, are accelerating, with an estimated 40% penetration in eligible patient populations for select indications. Technological disruptions, such as the development of CAR T-cell therapies and bispecific antibodies, are fundamentally altering treatment outcomes and patient survival rates. Consumer behavior shifts are also playing a critical role, with patients and caregivers becoming more informed and actively involved in treatment decisions, often seeking personalized and less toxic therapeutic options. The growing emphasis on early detection and personalized treatment plans, enabled by sophisticated diagnostic tools, is further fueling the demand for advanced cancer therapies. The expanding oncology drug pipeline, with hundreds of novel candidates in various stages of clinical development, promises a continuous stream of innovative solutions to address unmet medical needs across a spectrum of cancers. The increased survival rates observed in many cancer types, attributed to these therapeutic advancements, contribute to a larger patient pool requiring ongoing or adjuvant treatments, further bolstering market expansion. The penetration of precision medicine approaches, where treatments are tailored to an individual's genetic makeup, is steadily increasing, signifying a major shift towards more effective and less debilitating therapies. This personalized approach is driving demand for companion diagnostics and a deeper understanding of tumor biology, fostering innovation across the entire cancer care continuum. The increasing prevalence of lifestyle-related cancers and the ongoing improvement in diagnostic capabilities are also significant contributors to the sustained growth trajectory of the cancer treatment market.

Dominant Regions, Countries, or Segments in Cancer Treatment Industry

North America, particularly the United States, currently dominates the Cancer Treatment Industry, driven by a highly developed healthcare infrastructure, substantial R&D investments, favorable regulatory pathways, and a high prevalence of cancer cases. The region’s market share is estimated at approximately 40% of the global market in 2025. Key drivers include significant government and private funding for cancer research, a robust ecosystem of pharmaceutical and biotechnology companies, and a strong patient advocacy landscape that drives demand for advanced therapies. The country’s advanced healthcare reimbursement policies and high adoption rates for novel treatments further solidify its leading position.

Within the global Cancer Treatment Industry, Immunotherapy as a therapy type is experiencing explosive growth and is a significant driver of market dominance, projected to capture over 35% of the market share by 2025. Its efficacy in treating various solid tumors and hematologic malignancies, coupled with a strong pipeline of novel agents and combinations, positions it as a leading segment.

Breast Cancer and Blood Cancer are dominant cancer types driving market growth, with breast cancer accounting for an estimated 15% and blood cancer (including leukemia, lymphoma, and multiple myeloma) another 12% of the total cancer treatment market. These cancers have seen significant advancements in targeted therapies and immunotherapies, leading to improved patient outcomes and increased demand for innovative treatments.

In terms of end-users, Hospitals remain the primary channel for cancer treatment, accounting for over 60% of the market. This is due to their comprehensive facilities, specialized oncology departments, and ability to administer complex treatments like chemotherapy and immunotherapy.

- Dominant Region: North America (USA)

- Estimated Market Share: ~40% (2025)

- Drivers: High R&D spending, advanced infrastructure, robust regulatory framework, high cancer incidence, strong reimbursement policies.

- Dominant Therapy Type: Immunotherapy

- Projected Market Share: ~35% (2025)

- Key Factors: Breakthrough efficacy in various cancers, extensive pipeline, increasing approvals for novel agents.

- Leading Products: Checkpoint inhibitors, CAR T-cell therapies, bispecific antibodies.

- Dominant Cancer Types:

- Breast Cancer:

- Estimated Market Share: ~15% (2025)

- Drivers: Advances in hormonal therapy, targeted therapy, and immunotherapy; high prevalence.

- Blood Cancer (Leukemia, Lymphoma, Multiple Myeloma):

- Estimated Market Share: ~12% (2025)

- Drivers: Significant progress in CAR T-cell therapy, targeted agents, and stem cell transplantation.

- Breast Cancer:

- Dominant End User: Hospitals

- Market Share: ~60% (2025)

- Reasons: Comprehensive cancer centers, infusion services, inpatient care capabilities, specialized oncologists.

Cancer Treatment Industry Product Landscape

The Cancer Treatment Industry product landscape is characterized by relentless innovation, focusing on increasing therapeutic efficacy, reducing side effects, and personalizing treatment regimens. Key product innovations include novel immunotherapies like checkpoint inhibitors and CAR T-cell therapies, which harness the patient's own immune system to fight cancer. Targeted therapies, designed to specifically attack cancer cells based on their genetic mutations, represent another significant area of advancement, offering greater precision and fewer off-target effects compared to traditional chemotherapy. The performance metrics of these advanced therapies are demonstrably superior in many indications, with improved response rates and prolonged progression-free survival. Unique selling propositions revolve around enhanced patient outcomes, improved quality of life, and the potential for long-term remission or cure. Technological advancements, such as antibody-drug conjugates (ADCs) that deliver potent chemotherapy directly to cancer cells, are further refining treatment strategies.

Key Drivers, Barriers & Challenges in Cancer Treatment Industry

Key Drivers: The Cancer Treatment Industry is propelled by several powerful forces. Technological advancements in areas like immunotherapy, targeted therapies, and gene editing are continuously offering novel and more effective treatment options. The increasing global cancer incidence and prevalence, driven by aging populations and lifestyle factors, create a sustained and growing demand for cancer drugs and therapies. Significant investments in R&D by pharmaceutical and biotechnology companies, coupled with supportive government funding and policies, are crucial for pipeline development. Furthermore, the growing awareness among patients and healthcare providers regarding the benefits of early detection and personalized medicine fosters the adoption of advanced treatments.

Barriers & Challenges: Despite strong growth potential, the industry faces significant hurdles. The high cost of developing and obtaining regulatory approval for new cancer drugs, often exceeding $1 billion per drug, poses a substantial financial barrier. Stringent and lengthy regulatory approval processes can delay market entry for life-saving therapies. The emergence of drug resistance in certain cancer types remains a persistent challenge, necessitating continuous innovation. Intense competition among pharmaceutical companies, particularly in crowded therapeutic areas, can lead to pricing pressures and market access difficulties. Supply chain complexities, especially for biologic drugs and advanced cell therapies, require robust and resilient manufacturing and distribution networks to ensure consistent patient access. The estimated annual R&D expenditure for a single novel oncology drug can range from $500 million to $2 billion.

Emerging Opportunities in Cancer Treatment Industry

Emerging opportunities in the Cancer Treatment Industry are vast and multifaceted, driven by unmet medical needs and evolving scientific understanding. The development of highly personalized cancer vaccines, tailored to an individual's tumor neoantigens, represents a significant frontier with immense potential for improving treatment outcomes, particularly in combination therapies. The expansion of cell and gene therapies into a wider range of cancer types beyond hematological malignancies, including solid tumors, presents a major growth avenue. Advancements in liquid biopsy technologies are creating opportunities for earlier cancer detection, recurrence monitoring, and personalized treatment selection with greater ease and less invasiveness than traditional tissue biopsies. Furthermore, the increasing focus on combination therapies, leveraging synergistic effects of different treatment modalities like immunotherapy with targeted agents or chemotherapy, offers novel strategies to overcome treatment resistance and enhance patient responses. The growing demand for affordable and accessible cancer treatments in emerging markets also presents substantial untapped potential for market expansion.

Growth Accelerators in the Cancer Treatment Industry Industry

Several catalysts are accelerating the long-term growth of the Cancer Treatment Industry. Breakthroughs in understanding tumor microenvironments and the complex interplay of cancer cells with the immune system are fueling the development of next-generation immunotherapies with broader applicability and improved safety profiles. Strategic partnerships between pharmaceutical companies, academic institutions, and technology providers are fostering collaborative innovation and accelerating the drug discovery and development process. Market expansion strategies, including penetration into emerging economies and the development of treatments for rare or neglected cancers, are opening new revenue streams. The increasing adoption of real-world evidence (RWE) to support drug approvals and demonstrate post-market effectiveness is also becoming a key growth accelerator, allowing for more agile and data-driven decision-making. Furthermore, the growing emphasis on companion diagnostics and predictive biomarkers is enabling more precise patient stratification, leading to higher success rates for clinical trials and more effective treatment delivery.

Key Players Shaping the Cancer Treatment Industry Market

- F Hoffmann-La Roche AG

- Celldex Therapeutics Inc

- Gilead Sciences Inc (Kite Pharma)

- Bayer AG

- Astellas Pharma Inc

- Novartis AG

- Amgen Inc

- Merck & Co Inc

- Takeda Pharmaceutical Company Limited

- AstraZeneca

- Abbvie Inc

- GSK PLC

- Lilly

- Bristol Myers Squibb Company

- Johnson & Johnson Services Inc

- Alaunos Therapeutics Inc

- Pfizer Inc

Notable Milestones in Cancer Treatment Industry Sector

- May 2023: Genmab A/S received USFDA approval for its T-cell engaging bispecific antibody, EPKINLY (epcoritamab-bysp), for relapsed or refractory (R/R) diffuse large B-cell lymphoma (DLBCL) in adult patients.

- April 2023: Genentech (Roche Group) received USFDA approval for Polivy (polatuzumab vedotin-piiq) in combination with Rituxan (rituximab), cyclophosphamide, doxorubicin, and prednisone (R-CHP) for previously untreated diffuse large B-cell lymphoma (DLBCL) in adult patients.

- April 2023: Gamida Cell Ltd received USFDA approval for its allogeneic cell therapy, Omisirge (omidubicel-onlv), for adult and pediatric patients aged 12 years and older with hematologic malignancies.

In-Depth Cancer Treatment Industry Market Outlook

The future market potential for the Cancer Treatment Industry is exceptionally bright, driven by ongoing scientific breakthroughs and an increasing understanding of cancer biology. Growth will be significantly fueled by the expanding pipeline of personalized immunotherapies, advanced targeted agents, and innovative cell and gene therapies that promise higher efficacy and reduced toxicity. Strategic collaborations and mergers will continue to shape the competitive landscape, enabling faster development and broader market access for novel treatments. The increasing focus on early detection through liquid biopsies and AI-driven diagnostics will also create new avenues for therapeutic intervention. As healthcare systems globally prioritize oncology, investment in research and development is expected to remain robust, leading to a continuous stream of innovative solutions that will fundamentally transform cancer care and improve patient outcomes, driving the market towards an estimated value of $350,000 million by 2033.

Cancer Treatment Industry Segmentation

-

1. Therapy Type

- 1.1. Chemotherapy

- 1.2. Targeted Therapy

- 1.3. Immunotherapy

- 1.4. Hormonal Therapy

- 1.5. Other Treatment Types

-

2. Cancer Type

- 2.1. Blood Cancer

- 2.2. Breast Cancer

- 2.3. Prostate Cancer

- 2.4. Gastrointestinal Cancer

- 2.5. Gynaecologic Cancer

- 2.6. Respiratory/Lung Cancer

- 2.7. Other Cancer Types

-

3. End User

- 3.1. Hospitals

- 3.2. Specialty Clinics

- 3.3. Cancer and Radiation Therapy Centers

Cancer Treatment Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Cancer Treatment Industry Regional Market Share

Geographic Coverage of Cancer Treatment Industry

Cancer Treatment Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.64% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Therapy Type

- 5.1.1. Chemotherapy

- 5.1.2. Targeted Therapy

- 5.1.3. Immunotherapy

- 5.1.4. Hormonal Therapy

- 5.1.5. Other Treatment Types

- 5.2. Market Analysis, Insights and Forecast - by Cancer Type

- 5.2.1. Blood Cancer

- 5.2.2. Breast Cancer

- 5.2.3. Prostate Cancer

- 5.2.4. Gastrointestinal Cancer

- 5.2.5. Gynaecologic Cancer

- 5.2.6. Respiratory/Lung Cancer

- 5.2.7. Other Cancer Types

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Hospitals

- 5.3.2. Specialty Clinics

- 5.3.3. Cancer and Radiation Therapy Centers

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Middle East and Africa

- 5.4.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Therapy Type

- 6. Global Cancer Treatment Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Therapy Type

- 6.1.1. Chemotherapy

- 6.1.2. Targeted Therapy

- 6.1.3. Immunotherapy

- 6.1.4. Hormonal Therapy

- 6.1.5. Other Treatment Types

- 6.2. Market Analysis, Insights and Forecast - by Cancer Type

- 6.2.1. Blood Cancer

- 6.2.2. Breast Cancer

- 6.2.3. Prostate Cancer

- 6.2.4. Gastrointestinal Cancer

- 6.2.5. Gynaecologic Cancer

- 6.2.6. Respiratory/Lung Cancer

- 6.2.7. Other Cancer Types

- 6.3. Market Analysis, Insights and Forecast - by End User

- 6.3.1. Hospitals

- 6.3.2. Specialty Clinics

- 6.3.3. Cancer and Radiation Therapy Centers

- 6.1. Market Analysis, Insights and Forecast - by Therapy Type

- 7. North America Cancer Treatment Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Therapy Type

- 7.1.1. Chemotherapy

- 7.1.2. Targeted Therapy

- 7.1.3. Immunotherapy

- 7.1.4. Hormonal Therapy

- 7.1.5. Other Treatment Types

- 7.2. Market Analysis, Insights and Forecast - by Cancer Type

- 7.2.1. Blood Cancer

- 7.2.2. Breast Cancer

- 7.2.3. Prostate Cancer

- 7.2.4. Gastrointestinal Cancer

- 7.2.5. Gynaecologic Cancer

- 7.2.6. Respiratory/Lung Cancer

- 7.2.7. Other Cancer Types

- 7.3. Market Analysis, Insights and Forecast - by End User

- 7.3.1. Hospitals

- 7.3.2. Specialty Clinics

- 7.3.3. Cancer and Radiation Therapy Centers

- 7.1. Market Analysis, Insights and Forecast - by Therapy Type

- 8. Europe Cancer Treatment Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Therapy Type

- 8.1.1. Chemotherapy

- 8.1.2. Targeted Therapy

- 8.1.3. Immunotherapy

- 8.1.4. Hormonal Therapy

- 8.1.5. Other Treatment Types

- 8.2. Market Analysis, Insights and Forecast - by Cancer Type

- 8.2.1. Blood Cancer

- 8.2.2. Breast Cancer

- 8.2.3. Prostate Cancer

- 8.2.4. Gastrointestinal Cancer

- 8.2.5. Gynaecologic Cancer

- 8.2.6. Respiratory/Lung Cancer

- 8.2.7. Other Cancer Types

- 8.3. Market Analysis, Insights and Forecast - by End User

- 8.3.1. Hospitals

- 8.3.2. Specialty Clinics

- 8.3.3. Cancer and Radiation Therapy Centers

- 8.1. Market Analysis, Insights and Forecast - by Therapy Type

- 9. Asia Pacific Cancer Treatment Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Therapy Type

- 9.1.1. Chemotherapy

- 9.1.2. Targeted Therapy

- 9.1.3. Immunotherapy

- 9.1.4. Hormonal Therapy

- 9.1.5. Other Treatment Types

- 9.2. Market Analysis, Insights and Forecast - by Cancer Type

- 9.2.1. Blood Cancer

- 9.2.2. Breast Cancer

- 9.2.3. Prostate Cancer

- 9.2.4. Gastrointestinal Cancer

- 9.2.5. Gynaecologic Cancer

- 9.2.6. Respiratory/Lung Cancer

- 9.2.7. Other Cancer Types

- 9.3. Market Analysis, Insights and Forecast - by End User

- 9.3.1. Hospitals

- 9.3.2. Specialty Clinics

- 9.3.3. Cancer and Radiation Therapy Centers

- 9.1. Market Analysis, Insights and Forecast - by Therapy Type

- 10. Middle East and Africa Cancer Treatment Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Therapy Type

- 10.1.1. Chemotherapy

- 10.1.2. Targeted Therapy

- 10.1.3. Immunotherapy

- 10.1.4. Hormonal Therapy

- 10.1.5. Other Treatment Types

- 10.2. Market Analysis, Insights and Forecast - by Cancer Type

- 10.2.1. Blood Cancer

- 10.2.2. Breast Cancer

- 10.2.3. Prostate Cancer

- 10.2.4. Gastrointestinal Cancer

- 10.2.5. Gynaecologic Cancer

- 10.2.6. Respiratory/Lung Cancer

- 10.2.7. Other Cancer Types

- 10.3. Market Analysis, Insights and Forecast - by End User

- 10.3.1. Hospitals

- 10.3.2. Specialty Clinics

- 10.3.3. Cancer and Radiation Therapy Centers

- 10.1. Market Analysis, Insights and Forecast - by Therapy Type

- 11. South America Cancer Treatment Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Therapy Type

- 11.1.1. Chemotherapy

- 11.1.2. Targeted Therapy

- 11.1.3. Immunotherapy

- 11.1.4. Hormonal Therapy

- 11.1.5. Other Treatment Types

- 11.2. Market Analysis, Insights and Forecast - by Cancer Type

- 11.2.1. Blood Cancer

- 11.2.2. Breast Cancer

- 11.2.3. Prostate Cancer

- 11.2.4. Gastrointestinal Cancer

- 11.2.5. Gynaecologic Cancer

- 11.2.6. Respiratory/Lung Cancer

- 11.2.7. Other Cancer Types

- 11.3. Market Analysis, Insights and Forecast - by End User

- 11.3.1. Hospitals

- 11.3.2. Specialty Clinics

- 11.3.3. Cancer and Radiation Therapy Centers

- 11.1. Market Analysis, Insights and Forecast - by Therapy Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 F Hoffmann-La Roche AG

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Celldex Therapeutics Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Gilead Sciences Inc (Kite Pharma)

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Bayer AG

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Astellas Pharma Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Novartis AG

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Amgen Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Merck & Co Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Takeda Pharmaceutical Company Limited

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 AstraZeneca

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Abbvie Inc

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 GSK PLC

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Lilly

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Bristol Myers Squibb Company

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Johnson & Johnson Services Inc

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Alaunos Therapeutics Inc

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Pfizer Inc

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.1 F Hoffmann-La Roche AG

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Cancer Treatment Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Cancer Treatment Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Cancer Treatment Industry Revenue (Million), by Therapy Type 2025 & 2033

- Figure 4: North America Cancer Treatment Industry Volume (K Unit), by Therapy Type 2025 & 2033

- Figure 5: North America Cancer Treatment Industry Revenue Share (%), by Therapy Type 2025 & 2033

- Figure 6: North America Cancer Treatment Industry Volume Share (%), by Therapy Type 2025 & 2033

- Figure 7: North America Cancer Treatment Industry Revenue (Million), by Cancer Type 2025 & 2033

- Figure 8: North America Cancer Treatment Industry Volume (K Unit), by Cancer Type 2025 & 2033

- Figure 9: North America Cancer Treatment Industry Revenue Share (%), by Cancer Type 2025 & 2033

- Figure 10: North America Cancer Treatment Industry Volume Share (%), by Cancer Type 2025 & 2033

- Figure 11: North America Cancer Treatment Industry Revenue (Million), by End User 2025 & 2033

- Figure 12: North America Cancer Treatment Industry Volume (K Unit), by End User 2025 & 2033

- Figure 13: North America Cancer Treatment Industry Revenue Share (%), by End User 2025 & 2033

- Figure 14: North America Cancer Treatment Industry Volume Share (%), by End User 2025 & 2033

- Figure 15: North America Cancer Treatment Industry Revenue (Million), by Country 2025 & 2033

- Figure 16: North America Cancer Treatment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 17: North America Cancer Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: North America Cancer Treatment Industry Volume Share (%), by Country 2025 & 2033

- Figure 19: Europe Cancer Treatment Industry Revenue (Million), by Therapy Type 2025 & 2033

- Figure 20: Europe Cancer Treatment Industry Volume (K Unit), by Therapy Type 2025 & 2033

- Figure 21: Europe Cancer Treatment Industry Revenue Share (%), by Therapy Type 2025 & 2033

- Figure 22: Europe Cancer Treatment Industry Volume Share (%), by Therapy Type 2025 & 2033

- Figure 23: Europe Cancer Treatment Industry Revenue (Million), by Cancer Type 2025 & 2033

- Figure 24: Europe Cancer Treatment Industry Volume (K Unit), by Cancer Type 2025 & 2033

- Figure 25: Europe Cancer Treatment Industry Revenue Share (%), by Cancer Type 2025 & 2033

- Figure 26: Europe Cancer Treatment Industry Volume Share (%), by Cancer Type 2025 & 2033

- Figure 27: Europe Cancer Treatment Industry Revenue (Million), by End User 2025 & 2033

- Figure 28: Europe Cancer Treatment Industry Volume (K Unit), by End User 2025 & 2033

- Figure 29: Europe Cancer Treatment Industry Revenue Share (%), by End User 2025 & 2033

- Figure 30: Europe Cancer Treatment Industry Volume Share (%), by End User 2025 & 2033

- Figure 31: Europe Cancer Treatment Industry Revenue (Million), by Country 2025 & 2033

- Figure 32: Europe Cancer Treatment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 33: Europe Cancer Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Europe Cancer Treatment Industry Volume Share (%), by Country 2025 & 2033

- Figure 35: Asia Pacific Cancer Treatment Industry Revenue (Million), by Therapy Type 2025 & 2033

- Figure 36: Asia Pacific Cancer Treatment Industry Volume (K Unit), by Therapy Type 2025 & 2033

- Figure 37: Asia Pacific Cancer Treatment Industry Revenue Share (%), by Therapy Type 2025 & 2033

- Figure 38: Asia Pacific Cancer Treatment Industry Volume Share (%), by Therapy Type 2025 & 2033

- Figure 39: Asia Pacific Cancer Treatment Industry Revenue (Million), by Cancer Type 2025 & 2033

- Figure 40: Asia Pacific Cancer Treatment Industry Volume (K Unit), by Cancer Type 2025 & 2033

- Figure 41: Asia Pacific Cancer Treatment Industry Revenue Share (%), by Cancer Type 2025 & 2033

- Figure 42: Asia Pacific Cancer Treatment Industry Volume Share (%), by Cancer Type 2025 & 2033

- Figure 43: Asia Pacific Cancer Treatment Industry Revenue (Million), by End User 2025 & 2033

- Figure 44: Asia Pacific Cancer Treatment Industry Volume (K Unit), by End User 2025 & 2033

- Figure 45: Asia Pacific Cancer Treatment Industry Revenue Share (%), by End User 2025 & 2033

- Figure 46: Asia Pacific Cancer Treatment Industry Volume Share (%), by End User 2025 & 2033

- Figure 47: Asia Pacific Cancer Treatment Industry Revenue (Million), by Country 2025 & 2033

- Figure 48: Asia Pacific Cancer Treatment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Asia Pacific Cancer Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Asia Pacific Cancer Treatment Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Middle East and Africa Cancer Treatment Industry Revenue (Million), by Therapy Type 2025 & 2033

- Figure 52: Middle East and Africa Cancer Treatment Industry Volume (K Unit), by Therapy Type 2025 & 2033

- Figure 53: Middle East and Africa Cancer Treatment Industry Revenue Share (%), by Therapy Type 2025 & 2033

- Figure 54: Middle East and Africa Cancer Treatment Industry Volume Share (%), by Therapy Type 2025 & 2033

- Figure 55: Middle East and Africa Cancer Treatment Industry Revenue (Million), by Cancer Type 2025 & 2033

- Figure 56: Middle East and Africa Cancer Treatment Industry Volume (K Unit), by Cancer Type 2025 & 2033

- Figure 57: Middle East and Africa Cancer Treatment Industry Revenue Share (%), by Cancer Type 2025 & 2033

- Figure 58: Middle East and Africa Cancer Treatment Industry Volume Share (%), by Cancer Type 2025 & 2033

- Figure 59: Middle East and Africa Cancer Treatment Industry Revenue (Million), by End User 2025 & 2033

- Figure 60: Middle East and Africa Cancer Treatment Industry Volume (K Unit), by End User 2025 & 2033

- Figure 61: Middle East and Africa Cancer Treatment Industry Revenue Share (%), by End User 2025 & 2033

- Figure 62: Middle East and Africa Cancer Treatment Industry Volume Share (%), by End User 2025 & 2033

- Figure 63: Middle East and Africa Cancer Treatment Industry Revenue (Million), by Country 2025 & 2033

- Figure 64: Middle East and Africa Cancer Treatment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 65: Middle East and Africa Cancer Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 66: Middle East and Africa Cancer Treatment Industry Volume Share (%), by Country 2025 & 2033

- Figure 67: South America Cancer Treatment Industry Revenue (Million), by Therapy Type 2025 & 2033

- Figure 68: South America Cancer Treatment Industry Volume (K Unit), by Therapy Type 2025 & 2033

- Figure 69: South America Cancer Treatment Industry Revenue Share (%), by Therapy Type 2025 & 2033

- Figure 70: South America Cancer Treatment Industry Volume Share (%), by Therapy Type 2025 & 2033

- Figure 71: South America Cancer Treatment Industry Revenue (Million), by Cancer Type 2025 & 2033

- Figure 72: South America Cancer Treatment Industry Volume (K Unit), by Cancer Type 2025 & 2033

- Figure 73: South America Cancer Treatment Industry Revenue Share (%), by Cancer Type 2025 & 2033

- Figure 74: South America Cancer Treatment Industry Volume Share (%), by Cancer Type 2025 & 2033

- Figure 75: South America Cancer Treatment Industry Revenue (Million), by End User 2025 & 2033

- Figure 76: South America Cancer Treatment Industry Volume (K Unit), by End User 2025 & 2033

- Figure 77: South America Cancer Treatment Industry Revenue Share (%), by End User 2025 & 2033

- Figure 78: South America Cancer Treatment Industry Volume Share (%), by End User 2025 & 2033

- Figure 79: South America Cancer Treatment Industry Revenue (Million), by Country 2025 & 2033

- Figure 80: South America Cancer Treatment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 81: South America Cancer Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 82: South America Cancer Treatment Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Cancer Treatment Industry Revenue Million Forecast, by Therapy Type 2020 & 2033

- Table 2: Global Cancer Treatment Industry Volume K Unit Forecast, by Therapy Type 2020 & 2033

- Table 3: Global Cancer Treatment Industry Revenue Million Forecast, by Cancer Type 2020 & 2033

- Table 4: Global Cancer Treatment Industry Volume K Unit Forecast, by Cancer Type 2020 & 2033

- Table 5: Global Cancer Treatment Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 6: Global Cancer Treatment Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 7: Global Cancer Treatment Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Global Cancer Treatment Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: Global Cancer Treatment Industry Revenue Million Forecast, by Therapy Type 2020 & 2033

- Table 10: Global Cancer Treatment Industry Volume K Unit Forecast, by Therapy Type 2020 & 2033

- Table 11: Global Cancer Treatment Industry Revenue Million Forecast, by Cancer Type 2020 & 2033

- Table 12: Global Cancer Treatment Industry Volume K Unit Forecast, by Cancer Type 2020 & 2033

- Table 13: Global Cancer Treatment Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 14: Global Cancer Treatment Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 15: Global Cancer Treatment Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Cancer Treatment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: United States Cancer Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: United States Cancer Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Canada Cancer Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Canada Cancer Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 21: Mexico Cancer Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Mexico Cancer Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: Global Cancer Treatment Industry Revenue Million Forecast, by Therapy Type 2020 & 2033

- Table 24: Global Cancer Treatment Industry Volume K Unit Forecast, by Therapy Type 2020 & 2033

- Table 25: Global Cancer Treatment Industry Revenue Million Forecast, by Cancer Type 2020 & 2033

- Table 26: Global Cancer Treatment Industry Volume K Unit Forecast, by Cancer Type 2020 & 2033

- Table 27: Global Cancer Treatment Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 28: Global Cancer Treatment Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 29: Global Cancer Treatment Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 30: Global Cancer Treatment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 31: Germany Cancer Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Germany Cancer Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: United Kingdom Cancer Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: United Kingdom Cancer Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: France Cancer Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: France Cancer Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Italy Cancer Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Italy Cancer Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 39: Spain Cancer Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Spain Cancer Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 41: Rest of Europe Cancer Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Rest of Europe Cancer Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 43: Global Cancer Treatment Industry Revenue Million Forecast, by Therapy Type 2020 & 2033

- Table 44: Global Cancer Treatment Industry Volume K Unit Forecast, by Therapy Type 2020 & 2033

- Table 45: Global Cancer Treatment Industry Revenue Million Forecast, by Cancer Type 2020 & 2033

- Table 46: Global Cancer Treatment Industry Volume K Unit Forecast, by Cancer Type 2020 & 2033

- Table 47: Global Cancer Treatment Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 48: Global Cancer Treatment Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 49: Global Cancer Treatment Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 50: Global Cancer Treatment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 51: China Cancer Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 52: China Cancer Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 53: Japan Cancer Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 54: Japan Cancer Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 55: India Cancer Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 56: India Cancer Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 57: Australia Cancer Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 58: Australia Cancer Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 59: South Korea Cancer Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 60: South Korea Cancer Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 61: Rest of Asia Pacific Cancer Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 62: Rest of Asia Pacific Cancer Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 63: Global Cancer Treatment Industry Revenue Million Forecast, by Therapy Type 2020 & 2033

- Table 64: Global Cancer Treatment Industry Volume K Unit Forecast, by Therapy Type 2020 & 2033

- Table 65: Global Cancer Treatment Industry Revenue Million Forecast, by Cancer Type 2020 & 2033

- Table 66: Global Cancer Treatment Industry Volume K Unit Forecast, by Cancer Type 2020 & 2033

- Table 67: Global Cancer Treatment Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 68: Global Cancer Treatment Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 69: Global Cancer Treatment Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 70: Global Cancer Treatment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 71: GCC Cancer Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 72: GCC Cancer Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 73: South Africa Cancer Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 74: South Africa Cancer Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 75: Rest of Middle East and Africa Cancer Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 76: Rest of Middle East and Africa Cancer Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 77: Global Cancer Treatment Industry Revenue Million Forecast, by Therapy Type 2020 & 2033

- Table 78: Global Cancer Treatment Industry Volume K Unit Forecast, by Therapy Type 2020 & 2033

- Table 79: Global Cancer Treatment Industry Revenue Million Forecast, by Cancer Type 2020 & 2033

- Table 80: Global Cancer Treatment Industry Volume K Unit Forecast, by Cancer Type 2020 & 2033

- Table 81: Global Cancer Treatment Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 82: Global Cancer Treatment Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 83: Global Cancer Treatment Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 84: Global Cancer Treatment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 85: Brazil Cancer Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 86: Brazil Cancer Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 87: Argentina Cancer Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 88: Argentina Cancer Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 89: Rest of South America Cancer Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 90: Rest of South America Cancer Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Cancer Treatment Industry?

The projected CAGR is approximately 10.64%.

2. Which companies are prominent players in the Cancer Treatment Industry?

Key companies in the market include F Hoffmann-La Roche AG, Celldex Therapeutics Inc , Gilead Sciences Inc (Kite Pharma), Bayer AG, Astellas Pharma Inc, Novartis AG, Amgen Inc, Merck & Co Inc, Takeda Pharmaceutical Company Limited, AstraZeneca, Abbvie Inc, GSK PLC, Lilly, Bristol Myers Squibb Company, Johnson & Johnson Services Inc, Alaunos Therapeutics Inc, Pfizer Inc.

3. What are the main segments of the Cancer Treatment Industry?

The market segments include Therapy Type, Cancer Type, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 220.24 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Patient Assistance Programs (PAPs) and Rising Demand for Personalized Medicine; Growing Government Initiatives for Cancer Awareness; Rising Prevalence of Cancer Worldwide; Strong R&D Initiatives from Key Players.

6. What are the notable trends driving market growth?

The Targeted Therapy Segment is Expected to Witness Significant Growth during the the Forecast Period.

7. Are there any restraints impacting market growth?

Fluctuation in Reimbursement Policies; High Cost of Cancer Therapies.

8. Can you provide examples of recent developments in the market?

In May 2023, Genmab A/S received USFDA approval for its T-cell engaging bispecific antibody, EPKINLY (epcoritamab-bysp), which was intended for the treatment of relapsed or refractory (R/R) diffuse large B-cell lymphoma (DLBCL) in adult patients.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Cancer Treatment Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Cancer Treatment Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Cancer Treatment Industry?

To stay informed about further developments, trends, and reports in the Cancer Treatment Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence