Key Insights

The Autonomous Vehicles Sensor Industry is poised for explosive growth, with an estimated market size of USD 0.99 billion in 2025. This remarkable expansion is driven by an exceptional Compound Annual Growth Rate (CAGR) of 21.16% anticipated between 2019 and 2033. This surge is fueled by the relentless pursuit of enhanced vehicle safety, improved driver convenience, and the ongoing development of sophisticated self-driving technologies. Key drivers include advancements in artificial intelligence and machine learning, the increasing adoption of Advanced Driver-Assistance Systems (ADAS) as a stepping stone to full autonomy, and supportive government regulations and initiatives promoting the integration of autonomous features. The market is segmented across various vehicle types, including Passenger Cars, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs), and other emerging autonomous vehicle categories, all contributing to the escalating demand for a diverse array of sensors.

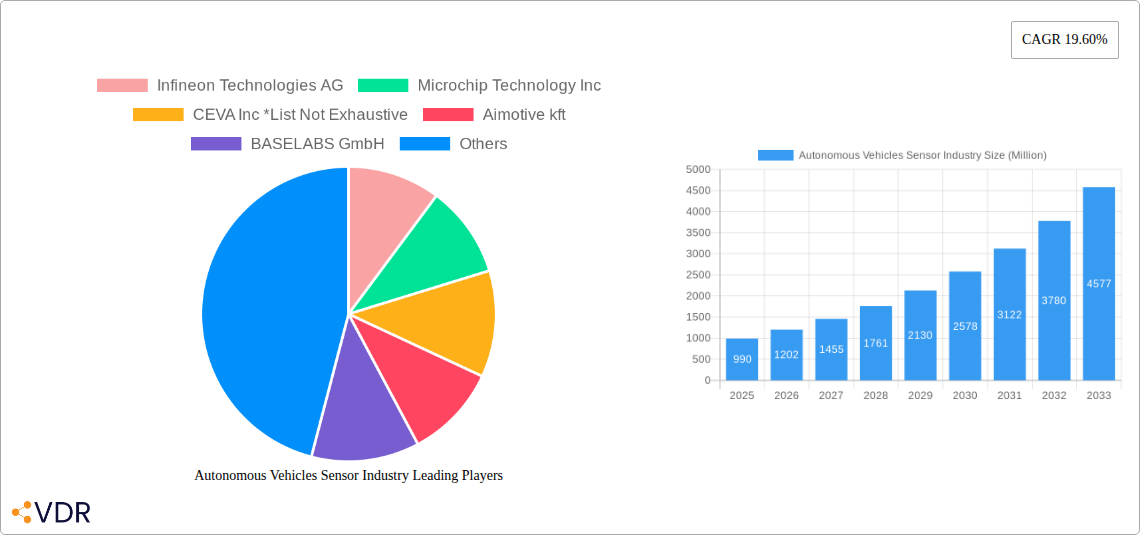

Autonomous Vehicles Sensor Industry Market Size (In Million)

The competitive landscape is characterized by innovation and strategic collaborations among major players such as Infineon Technologies AG, Microchip Technology Inc, NXP Semiconductors, Robert Bosch GmbH, and STMicroelectronics NV. These companies are investing heavily in research and development to create more accurate, reliable, and cost-effective sensor solutions, including LiDAR, radar, cameras, and ultrasonic sensors. Emerging trends include the miniaturization of sensors, the integration of sensor fusion technologies for enhanced perception, and the development of specialized sensors for extreme weather conditions and complex urban environments. While the industry benefits from robust growth, it also faces certain restraints, such as the high cost of sensor development and integration, challenges in achieving universal regulatory compliance across different regions, and public perception concerns regarding the safety and security of autonomous systems. The Asia Pacific region is expected to emerge as a significant growth engine, owing to strong government backing for smart mobility and the presence of major automotive manufacturing hubs.

Autonomous Vehicles Sensor Industry Company Market Share

Autonomous Vehicles Sensor Industry: Comprehensive Market Analysis & Future Outlook (2019-2033)

This in-depth report provides a definitive analysis of the global Autonomous Vehicles Sensor Industry, exploring market dynamics, growth trends, key players, and future opportunities from 2019 to 2033. Dive into parent and child market segments, understand technological innovations, and gain strategic insights to navigate this rapidly evolving sector.

Autonomous Vehicles Sensor Industry Market Dynamics & Structure

The Autonomous Vehicles Sensor Industry is characterized by dynamic market concentration and intense technological innovation, driven by the escalating demand for enhanced safety and efficiency in transportation. Key technological innovation drivers include advancements in artificial intelligence (AI) for data processing, the miniaturization and cost reduction of sensor hardware, and the development of robust perception algorithms. Regulatory frameworks, such as evolving safety standards and data privacy laws, play a crucial role in shaping market entry and product development. Competitive product substitutes, while not yet directly replacing the need for sensor suites, are influencing the selection and integration of specific sensor types. End-user demographics, particularly the increasing acceptance of advanced driver-assistance systems (ADAS) and the growing potential for autonomous fleet operations, are significant market shapers. Mergers and acquisitions (M&A) trends are evident as larger Tier-1 suppliers and tech giants consolidate their positions and acquire specialized expertise.

- Market Concentration: Dominated by a few major players, but with increasing fragmentation due to specialized startups.

- Technological Innovation Drivers: AI/ML algorithms, sensor fusion, LiDAR, radar, camera resolution, and V2X communication.

- Regulatory Frameworks: Evolving safety standards (e.g., ISO 26262, NHTSA guidelines), cybersecurity mandates, and data privacy regulations are crucial.

- Competitive Product Substitutes: While no direct replacement, advanced software algorithms can augment or reduce the reliance on certain hardware sensors in specific scenarios.

- End-User Demographics: Growing demand from ride-sharing services, logistics companies, and increasingly, individual consumers seeking advanced safety features.

- M&A Trends: Strategic acquisitions to gain access to crucial sensor technologies, AI capabilities, and established supply chains. The volume of M&A deals is expected to rise by approximately 15% during the forecast period, indicating consolidation.

Autonomous Vehicles Sensor Industry Growth Trends & Insights

The Autonomous Vehicles Sensor Industry is poised for exponential growth, driven by a confluence of technological advancements, increasing adoption rates of autonomous features, and evolving consumer behavior. The market size is projected to witness a compound annual growth rate (CAGR) of approximately 18.5% during the forecast period, expanding from an estimated $22.5 billion in 2025 to $75.8 billion by 2033. This robust expansion is fueled by the relentless pursuit of higher levels of autonomy (SAE Levels 3-5) across various vehicle types. Technological disruptions, particularly in the realm of solid-state LiDAR, advanced radar systems, and high-resolution imaging sensors, are continuously enhancing the capabilities and reducing the cost of sensor suites. Consumer behavior is shifting from a preference for basic safety features to a strong demand for sophisticated ADAS and eventually, fully autonomous driving experiences, especially in urban environments and for long-haul transportation. The penetration of advanced sensor technologies in new vehicle sales is expected to surge, driven by both regulatory mandates and consumer preference.

- Market Size Evolution: From an estimated $22.5 billion in 2025 to $75.8 billion by 2033.

- CAGR: Approximately 18.5% during the forecast period.

- Adoption Rates: Rapid increase in the adoption of ADAS features, laying the groundwork for higher levels of autonomy.

- Technological Disruptions: Innovations in LiDAR, radar, ultrasonic, and camera sensor technologies are improving performance, reducing costs, and enhancing sensor fusion capabilities.

- Consumer Behavior Shifts: Growing acceptance of autonomous driving features and a willingness to pay for enhanced safety and convenience.

- Market Penetration: Expected to rise significantly, with a substantial percentage of new vehicles equipped with advanced sensor suites by 2033.

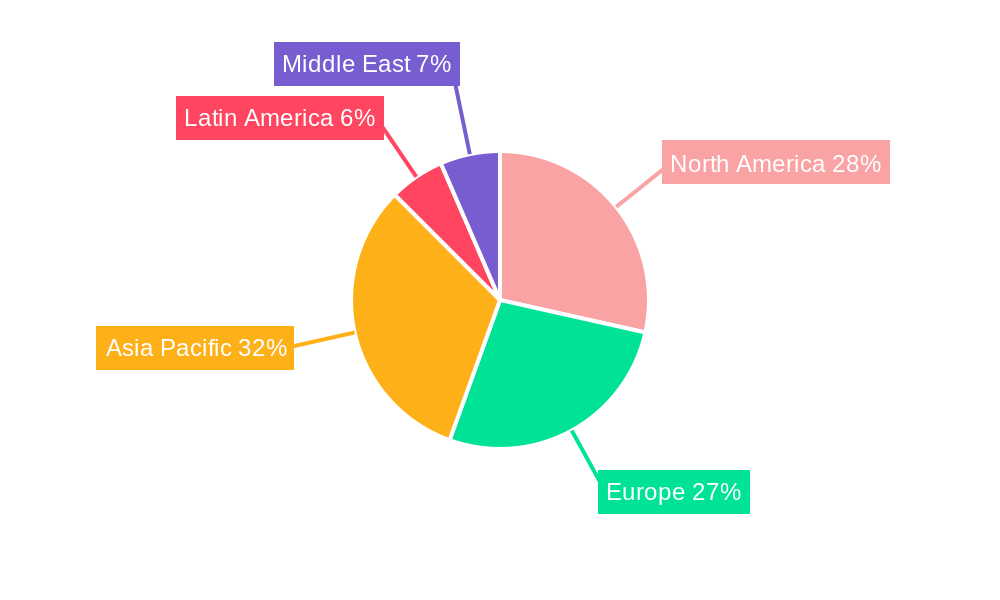

Dominant Regions, Countries, or Segments in Autonomous Vehicles Sensor Industry

North America, specifically the United States, is emerging as a dominant region in the Autonomous Vehicles Sensor Industry, driven by robust government support for innovation, significant investments in R&D by leading automotive and technology companies, and a strong consumer appetite for advanced vehicle technologies. Passenger Cars represent the most dominant segment within the Types of Vehicle category, accounting for an estimated 65% of the total market share. This dominance is attributed to the high volume of passenger car production globally and the increasing integration of ADAS and semi-autonomous features in mainstream models. Key drivers for North America's leadership include proactive regulatory initiatives encouraging autonomous vehicle testing and deployment, substantial venture capital funding flowing into AV startups, and the presence of major automotive manufacturers and technology hubs like Silicon Valley. The economic policies in the region are conducive to large-scale investment in autonomous driving technology, further accelerating market growth.

- Dominant Region: North America, with the United States at the forefront.

- Key Drivers:

- Favorable government policies and incentives for AV development and testing.

- Significant R&D investments from major automotive OEMs and tech giants.

- High consumer acceptance and demand for advanced safety and convenience features.

- Presence of a strong ecosystem of AV technology companies and research institutions.

- Early adoption of autonomous driving features in ride-sharing fleets.

- Key Drivers:

- Dominant Segment: Passenger Cars.

- Market Share: Estimated at 65% of the total sensor market for autonomous vehicles.

- Growth Potential: Continuous integration of ADAS and increasing demand for higher levels of automation in personal vehicles.

- Factors Contributing to Dominance:

- High production volumes of passenger vehicles globally.

- Consumer willingness to invest in enhanced safety and comfort.

- Increasingly stringent safety regulations mandating advanced driver assistance systems.

Autonomous Vehicles Sensor Industry Product Landscape

The product landscape of the Autonomous Vehicles Sensor Industry is characterized by a diverse array of sensor technologies, including LiDAR, radar, cameras, ultrasonic sensors, and IMUs, each contributing vital data for perception and decision-making. Innovations focus on improving resolution, range, accuracy, and robustness in various environmental conditions. LiDAR technology is seeing advancements in solid-state designs for cost reduction and increased durability, while radar systems are evolving with higher resolution and better object detection capabilities. Advanced camera systems offer enhanced low-light performance and wider fields of view. The trend towards sensor fusion, combining data from multiple sensor types, is crucial for creating a comprehensive 360-degree view and overcoming individual sensor limitations, leading to more reliable autonomous operation.

Key Drivers, Barriers & Challenges in Autonomous Vehicles Sensor Industry

The Autonomous Vehicles Sensor Industry is propelled by several key drivers, including the unyielding pursuit of enhanced vehicle safety, the potential for increased transportation efficiency and reduced congestion, and the growing demand for autonomous mobility solutions. Technological advancements in AI, sensor fusion, and processing power are critical enablers.

- Key Drivers:

- Safety Enhancement: Reducing human error-related accidents.

- Efficiency & Convenience: Optimizing traffic flow and offering new mobility services.

- Technological Advancement: Continuous innovation in sensors and AI.

- Regulatory Support: Growing government initiatives to facilitate AV deployment.

Conversely, the industry faces significant barriers and challenges. High development and component costs remain a hurdle, especially for widespread consumer adoption. Regulatory fragmentation across different regions and countries creates complexity for manufacturers. Cybersecurity threats to vehicle systems and data privacy concerns also pose substantial challenges, requiring robust security measures. Supply chain disruptions, particularly for specialized semiconductor components, can impact production timelines and costs.

- Barriers & Challenges:

- High Development & Component Costs: Affecting affordability.

- Regulatory Hurdles: Inconsistent standards and approval processes globally.

- Cybersecurity Threats: Protecting vehicles and data from malicious attacks.

- Public Perception & Trust: Building confidence in autonomous technology.

- Supply Chain Vulnerabilities: Ensuring consistent availability of critical components.

Emerging Opportunities in Autonomous Vehicles Sensor Industry

Emerging opportunities lie in the development of ultra-reliable, cost-effective sensor solutions for specific use cases, such as last-mile delivery vehicles and specialized industrial autonomous systems. The integration of V2X (Vehicle-to-Everything) communication capabilities with sensor data presents a significant avenue for enhanced situational awareness and cooperative driving. Furthermore, the growing demand for in-cabin monitoring systems to ensure driver readiness and passenger safety opens up new market segments for specialized sensors. The development of AI-powered sensor analytics for predictive maintenance and fleet management also represents a burgeoning opportunity.

- Untapped Markets: Specialized autonomous applications (e.g., logistics, agriculture), non-automotive autonomous systems.

- Innovative Applications: Enhanced sensor fusion algorithms, AI-driven perception for edge cases.

- Evolving Consumer Preferences: Personalized in-cabin experiences, advanced safety monitoring.

Growth Accelerators in the Autonomous Vehicles Sensor Industry Industry

The long-term growth of the Autonomous Vehicles Sensor Industry will be accelerated by breakthroughs in next-generation sensor technologies, such as advanced solid-state LiDAR and high-frequency radar, promising lower costs and enhanced performance. Strategic partnerships between sensor manufacturers, AI software developers, and automotive OEMs are crucial for creating integrated, end-to-end solutions. The expansion of autonomous vehicle testing and deployment initiatives in new geographical markets, supported by favorable government policies, will also serve as significant growth accelerators. Furthermore, the standardization of sensor interfaces and data protocols will streamline integration and foster wider adoption across the industry.

Key Players Shaping the Autonomous Vehicles Sensor Industry Market

- Infineon Technologies AG

- Microchip Technology Inc

- CEVA Inc

- Aimotive kft

- BASELABS GmbH

- NXP Semiconductor

- STMicroelectronics NV

- Kionix Inc (Rohm Co Ltd)

- Robert Bosch GmbH

- TDK Corporation

Notable Milestones in Autonomous Vehicles Sensor Industry Sector

- January 2022: Ambarella Inc. launched the CV3 AI domain controller family during CES, offering up to 500 eTOPS of AI processing performance for multi-sensor perception and AV path planning.

- January 2022: Qualcomm launched the Snapdragon Ride Vision System, an open and scalable platform for automated driving, featuring a modular architecture for integrating driver monitoring systems (DMS), map crowdsourcing, parking systems, V2X technologies, and localization modules.

In-Depth Autonomous Vehicles Sensor Industry Market Outlook

The future of the Autonomous Vehicles Sensor Industry is exceptionally bright, with growth accelerators including continuous technological innovation in sensing and AI, strategic collaborations fostering ecosystem development, and the progressive expansion of autonomous mobility services across diverse sectors. As sensor costs decline and performance metrics improve, the adoption of advanced sensor suites will become increasingly ubiquitous, driving significant market potential. Strategic investments in research and development, coupled with favorable regulatory environments, will continue to propel the industry forward, creating substantial opportunities for market leaders and innovative disruptors. The trend towards centralized processing and advanced sensor fusion will be a defining characteristic of future autonomous systems.

Autonomous Vehicles Sensor Industry Segmentation

-

1. Types of Vehicle

- 1.1. Passenger Cars

- 1.2. Light Commercial Vehicle (LCV)

- 1.3. Heavy Commercial Vehicle (HCV)

- 1.4. Other Autonomous Vehicles

Autonomous Vehicles Sensor Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East

Autonomous Vehicles Sensor Industry Regional Market Share

Geographic Coverage of Autonomous Vehicles Sensor Industry

Autonomous Vehicles Sensor Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 5.1.1. Passenger Cars

- 5.1.2. Light Commercial Vehicle (LCV)

- 5.1.3. Heavy Commercial Vehicle (HCV)

- 5.1.4. Other Autonomous Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. Latin America

- 5.2.5. Middle East

- 5.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 6. Global Autonomous Vehicles Sensor Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 6.1.1. Passenger Cars

- 6.1.2. Light Commercial Vehicle (LCV)

- 6.1.3. Heavy Commercial Vehicle (HCV)

- 6.1.4. Other Autonomous Vehicles

- 6.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 7. North America Autonomous Vehicles Sensor Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 7.1.1. Passenger Cars

- 7.1.2. Light Commercial Vehicle (LCV)

- 7.1.3. Heavy Commercial Vehicle (HCV)

- 7.1.4. Other Autonomous Vehicles

- 7.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 8. Europe Autonomous Vehicles Sensor Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 8.1.1. Passenger Cars

- 8.1.2. Light Commercial Vehicle (LCV)

- 8.1.3. Heavy Commercial Vehicle (HCV)

- 8.1.4. Other Autonomous Vehicles

- 8.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 9. Asia Pacific Autonomous Vehicles Sensor Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 9.1.1. Passenger Cars

- 9.1.2. Light Commercial Vehicle (LCV)

- 9.1.3. Heavy Commercial Vehicle (HCV)

- 9.1.4. Other Autonomous Vehicles

- 9.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 10. Latin America Autonomous Vehicles Sensor Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 10.1.1. Passenger Cars

- 10.1.2. Light Commercial Vehicle (LCV)

- 10.1.3. Heavy Commercial Vehicle (HCV)

- 10.1.4. Other Autonomous Vehicles

- 10.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 11. Middle East Autonomous Vehicles Sensor Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 11.1.1. Passenger Cars

- 11.1.2. Light Commercial Vehicle (LCV)

- 11.1.3. Heavy Commercial Vehicle (HCV)

- 11.1.4. Other Autonomous Vehicles

- 11.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Infineon Technologies AG

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Microchip Technology Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 CEVA Inc *List Not Exhaustive

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Aimotive kft

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 BASELABS GmbH

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 NXP Semiconductor

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 STMicroelectronics NV

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Kionix Inc (Rohm Co Ltd)

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Robert Bosch GmbH

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 TDK Corporation

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Infineon Technologies AG

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Autonomous Vehicles Sensor Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Autonomous Vehicles Sensor Industry Revenue (billion), by Types of Vehicle 2025 & 2033

- Figure 3: North America Autonomous Vehicles Sensor Industry Revenue Share (%), by Types of Vehicle 2025 & 2033

- Figure 4: North America Autonomous Vehicles Sensor Industry Revenue (billion), by Country 2025 & 2033

- Figure 5: North America Autonomous Vehicles Sensor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Europe Autonomous Vehicles Sensor Industry Revenue (billion), by Types of Vehicle 2025 & 2033

- Figure 7: Europe Autonomous Vehicles Sensor Industry Revenue Share (%), by Types of Vehicle 2025 & 2033

- Figure 8: Europe Autonomous Vehicles Sensor Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: Europe Autonomous Vehicles Sensor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Pacific Autonomous Vehicles Sensor Industry Revenue (billion), by Types of Vehicle 2025 & 2033

- Figure 11: Asia Pacific Autonomous Vehicles Sensor Industry Revenue Share (%), by Types of Vehicle 2025 & 2033

- Figure 12: Asia Pacific Autonomous Vehicles Sensor Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Asia Pacific Autonomous Vehicles Sensor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Latin America Autonomous Vehicles Sensor Industry Revenue (billion), by Types of Vehicle 2025 & 2033

- Figure 15: Latin America Autonomous Vehicles Sensor Industry Revenue Share (%), by Types of Vehicle 2025 & 2033

- Figure 16: Latin America Autonomous Vehicles Sensor Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: Latin America Autonomous Vehicles Sensor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Middle East Autonomous Vehicles Sensor Industry Revenue (billion), by Types of Vehicle 2025 & 2033

- Figure 19: Middle East Autonomous Vehicles Sensor Industry Revenue Share (%), by Types of Vehicle 2025 & 2033

- Figure 20: Middle East Autonomous Vehicles Sensor Industry Revenue (billion), by Country 2025 & 2033

- Figure 21: Middle East Autonomous Vehicles Sensor Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Autonomous Vehicles Sensor Industry Revenue billion Forecast, by Types of Vehicle 2020 & 2033

- Table 2: Global Autonomous Vehicles Sensor Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Global Autonomous Vehicles Sensor Industry Revenue billion Forecast, by Types of Vehicle 2020 & 2033

- Table 4: Global Autonomous Vehicles Sensor Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 5: Global Autonomous Vehicles Sensor Industry Revenue billion Forecast, by Types of Vehicle 2020 & 2033

- Table 6: Global Autonomous Vehicles Sensor Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Autonomous Vehicles Sensor Industry Revenue billion Forecast, by Types of Vehicle 2020 & 2033

- Table 8: Global Autonomous Vehicles Sensor Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: Global Autonomous Vehicles Sensor Industry Revenue billion Forecast, by Types of Vehicle 2020 & 2033

- Table 10: Global Autonomous Vehicles Sensor Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 11: Global Autonomous Vehicles Sensor Industry Revenue billion Forecast, by Types of Vehicle 2020 & 2033

- Table 12: Global Autonomous Vehicles Sensor Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Autonomous Vehicles Sensor Industry?

The projected CAGR is approximately 11.9%.

2. Which companies are prominent players in the Autonomous Vehicles Sensor Industry?

Key companies in the market include Infineon Technologies AG, Microchip Technology Inc, CEVA Inc *List Not Exhaustive, Aimotive kft, BASELABS GmbH, NXP Semiconductor, STMicroelectronics NV, Kionix Inc (Rohm Co Ltd), Robert Bosch GmbH, TDK Corporation.

3. What are the main segments of the Autonomous Vehicles Sensor Industry?

The market segments include Types of Vehicle.

4. Can you provide details about the market size?

The market size is estimated to be USD 39.5 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand for Autonomous Vehicles; Efficient Real Time Data Processing and Data Sharing Capabilities to Drive the Demand.

6. What are the notable trends driving market growth?

Passenger Cars to Hold a Significant Market Share.

7. Are there any restraints impacting market growth?

Lack of Standardization in Sensor Fusion Technology.

8. Can you provide examples of recent developments in the market?

January 2022 - Ambarella Inc., an AI vision silicon company, launched the CV3 AI domain controller family during CES. This power-efficient and fully scalable CVflow family of SoCs provides the automotive industry's highest AI processing performance at up to 500 eTOPS. Furthermore, the product family enables centralized, single-chip processing for multi-sensor perception-including radar, high-resolution vision, ultrasonic, and lidar- and AV path planning and deep fusion for multiple sensor modalities.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Autonomous Vehicles Sensor Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Autonomous Vehicles Sensor Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Autonomous Vehicles Sensor Industry?

To stay informed about further developments, trends, and reports in the Autonomous Vehicles Sensor Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence